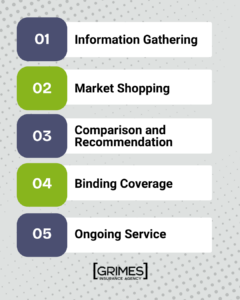

The Insurance Quote Process at Grimes Insurance Agency

Wondering what happens after you request an insurance quote? Confused about what the insurance quote process even looks like?

Well, don’t worry– you’re not the only one who’s unsure.

Since 1948, Grimes Insurance Agency has helped West Texans navigate insurance decisions with confidence. Whether you’re shopping for auto, home, or life insurance, our goal is to make the quoting process clear and easy to understand.

In this article, we’ll walk through what happens when you request an insurance quote, the information you’ll need to provide, and how to get answers about what your policy actually means.

Step 1: Start the Insurance Quote Process Online

The first step is to complete the online quote form. Whether you are requesting a quote for personal insurance or commercial insurance, both forms are listed on our website and only take about 3-5 minutes to complete.

What Kind of Information Will You Need?

You will be prompted to supply your personal details, such as your:

- First and last name

- Date of birth

- Gender

- Marital status

- Phone number

- Email address

- Physical address

Depending on the type of insurance, additional details will vary.

Home Quote |

Auto Quote |

|

House Type |

Driver’s License Number |

|

Year Built |

Vehicle Make and Model |

| Roof Age and Condition |

Driver’s License Plate |

| Square Footage |

Driving History |

| Occupancy Details |

Current Insurance Information |

For example, if you are requesting a quote for auto insurance, you will need to supply vehicle-specific information like your driver’s license number, the state you are registered in, and your car’s license plate.

Unsure about sharing details over the web? Watch this video to understand what to expect after pressing submit.

While submitting the form online is the quickest way to get your information sorted, you can always reach out to our team for questions and guidance. We are available Monday through Friday, 8:30 a.m. to 5 p.m. CDT via phone call, email, or in-office.

Step 2: Speak With a Grimes Insurance Agent About Your Quote

Once you submit the online form, your information will be given to a Grimes Insurance agent.

Your agent will be available to guide you through the process and answer any questions you might have. Their goal is to ensure that you have all the information you need to make a well-informed decision.

The assigned agent will contact you to discuss your needs in detail.

We know what you’re thinking… more information? And we get it.

However, the more information you provide, the greater the chance of finding a policy that fits you well.

Your insurance agent will ask you for additional details about your home, vehicle, and other dependents on your policy.

Why is this information important?

Insurance premiums, coverages, and quote options are all influenced by the information you provide. Multiple factors can affect the policy options available to you. Such factors include:

Home Insurance |

Auto Insurance |

|

Recent Renovations or Updates |

Annual Mileage |

|

Security Systems |

Accident History |

| Roof Age and Condition |

Driver Training |

| Construction Materials |

Driver Discounts |

| Foundations Type |

Additional Vehicles |

To learn more about the information insurance companies use when determining rates, read How Auto Insurance Premiums Are Calculated.

The more complete the picture, the more accurate your quote will be.

Step 4: Grimes Shops Multiple Insurance Providers

Shopping time! This is where you pass the baton, and we get to work.

How We Find the Best Coverage Options

Using the information from your conversation and online form, your Grimes Insurance agent begins searching to find the best personalized quote package for you.

We apply your details and coverage needs to the multiple carriers we represent. The quotes we receive back are collected and ranked from least to most expensive. From there, we compile the options and narrow the quotes that make the most sense for your situation.

Insurance shopping is what makes this process different from purchasing insurance from a provider.

Grimes is an independent insurance agency and not a carrier. The insurance company you choose (like Progressive or Allstate) provides and writes your coverage policy. The Grimes Insurance team helps you compare options, answer questions, and understand your coverage.

If insurance were a chasm (and let’s face it, it is sometimes), we would be the bridge that connects you and your carrier.

Read to learn more about How Independent Insurance Agents Work.

Before presenting you with quote options, our team double-checks and triple-checks all information. This looks like verifying personal details and identifying anything that could affect eligibility or pricing.

Consider this the quality control stage.

We review coverage limits, deductibles, policy requirements, and rating information to ensure the quotes you see accurately reflect your situation. The goal is to catch potential issues before they become surprises later.

For example, missing drivers in the household, inaccurate property details, prior claims, or other reporting discrepancies can affect a policy’s final premium or eligibility. Taking the time to review these details upfront helps create a smoother experience once you’re ready to move forward.

Step 6: Reviewing Your Options

Once everything has been reviewed, we’ll present you with the options that best fit your needs. Here, you decide which policy makes the most sense to you.

Questions to Ask When Reviewing Your Quote

As you review your quote options, don’t be afraid to ask questions. Insurance can be complicated, and a good agent should be able to explain your options in plain English. Consider asking:

- What does this insurance actually cover?

- How much would I have to pay out of pocket if I filed a claim?

- Are there any other discounts I qualify for?

- How does this compare to the insurance I have now?

- What would you choose if you were in my situation?

The goal here isn’t just to find the lowest premium, but to actually understand what your policy includes and what you’ll pay for.

Your Quote Can Be Revised

The great thing about this stage is that we can always go back to the drawing board. If something doesn’t seem to fit, or you want to see other options, you can request an adjustment.

Feeling comfortable with your decision is crucial. At the end of the day, it’s your coverage and protection, so you should know what you’re protecting and why.

Step 7: Choosing a Policy and Setting an Effective Date

Once you’ve reviewed your options and selected a policy, the final steps are fairly straightforward.

Our team will walk you through any required paperwork, collect payment information, and prepare the policy for issuance. If you’re purchasing home insurance, this is also when we will coordinate important dates, such as the home closing.

What Happens After I Choose My Policy?

After your policy is issued, the insurance provider may conduct an additional review to verify information provided during the quoting process. This additional review is known as an underwriting period.

For example, a home insurance company may inspect a property to confirm its condition or identify maintenance concerns that need to be addressed.

While this review process is common, it doesn’t typically affect coverage immediately. If a carrier identifies an issue, they will generally provide notice and time to make any necessary corrections.

Still curious about the underwriting process? Check out this video to learn more about what happens during an underwriting period.

When Does My Coverage Start?

In many cases, coverage can begin the same day. However, some customers choose a future effective date, especially when purchasing a new home or planning to take advantage of the available discounts.

The Next Step to Getting an Insurance Quote

Requesting an insurance quote involves more than receiving a price. Along the way, you’ll share information about your needs, review coverage options, compare carriers, and decide which policy makes the most sense for your situation.

While the process may seem intimidating at first, knowing what happens at each stage can make it easier to move forward and ask the right questions along the way.

For the past 78 years, our transparency and passion for educating customers have helped West Texans make insurance decisions they feel good about. At Grimes Insurance, we believe you should understand your coverage before committing, not after.

If you’re ready to explore your options, start a quote with Grimes Insurance Agency. Our team is prepared to help you compare coverage options, answer your questions, and determine which policy fits you the best.

Leaving your home for an extended period of time, whether for a vacation or as a snowbird seeking warmer climates, requires careful preparation to ensure the safety and security of your property. The last thing you want is to return to a home damaged by a burst pipe or burglarized. To protect your home and give yourself peace of mind while you’re away, follow this comprehensive checklist:

Leaving your home for an extended period of time, whether for a vacation or as a snowbird seeking warmer climates, requires careful preparation to ensure the safety and security of your property. The last thing you want is to return to a home damaged by a burst pipe or burglarized. To protect your home and give yourself peace of mind while you’re away, follow this comprehensive checklist: