Flood Insurance Flood Zones Explained: Understanding Your Risk in Lubbock

Flooding poses a real threat to Lubbock homeowners, yet many don’t understand their actual risk level. FEMA flood zones determine whether your property needs flood insurance and how much coverage you should carry.

We at Grimes Insurance Agency help local residents decode flood insurance and flood zones explained so they can make informed decisions about protecting their homes. This guide walks you through the zones, Lubbock’s specific risks, and the coverage options available to you.

How FEMA Flood Zones Shape Your Insurance Requirements

FEMA’s Flood Insurance Rate Maps divide properties into zones based on their flood risk, and this designation directly determines whether your lender will require flood insurance and how much you’ll pay. The zones fall into three main categories: high-risk areas labeled A and AE, moderate-risk zones, and low-risk areas.

High-Risk Zones A and AE

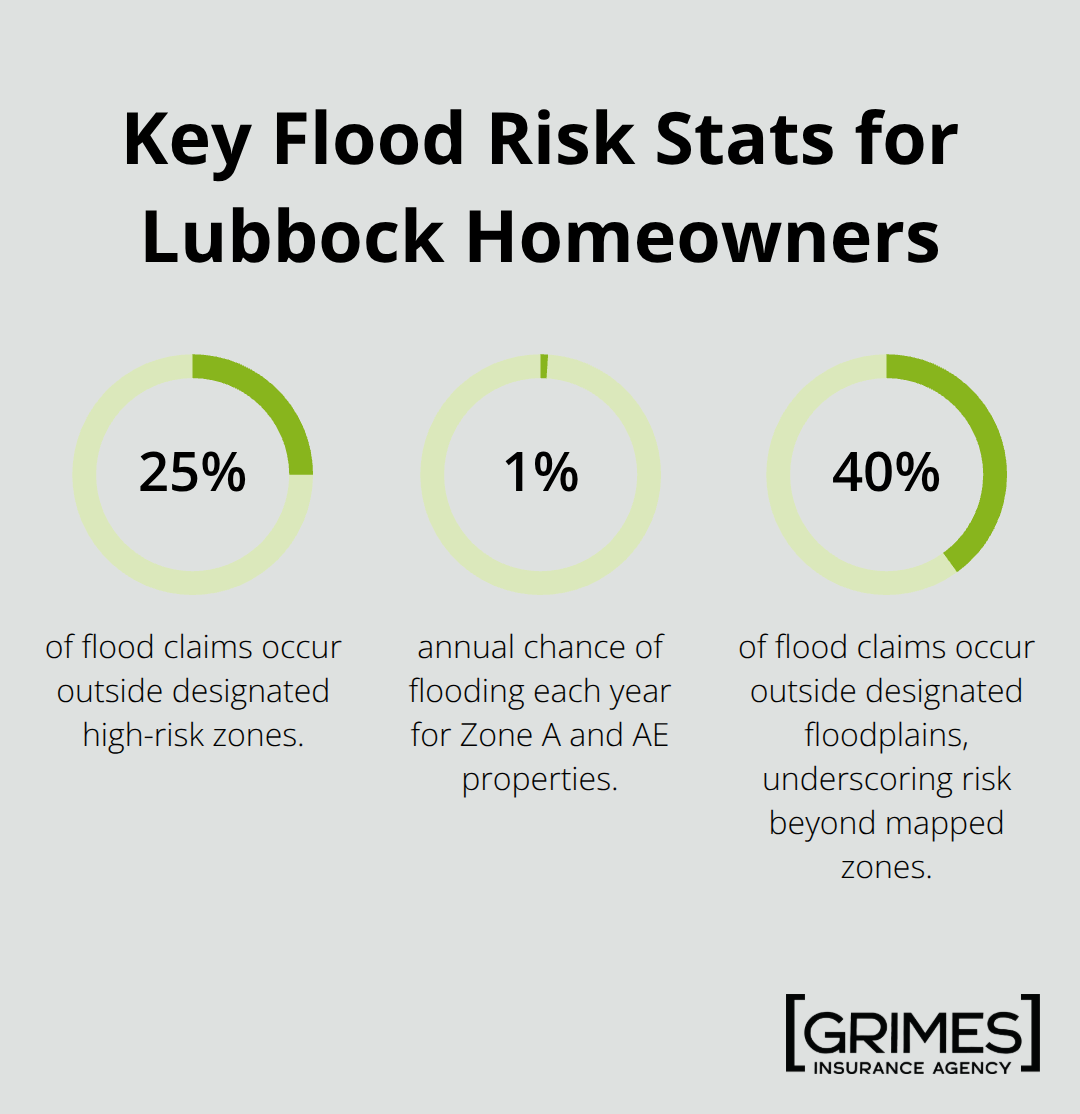

Zone A and AE properties sit in Special Flood Hazard Areas with a 1% annual chance of flooding, meaning federally regulated lenders almost always require flood coverage as a loan condition. These zones include base flood elevations, which represent the height that water is expected to reach during a 100-year flood event. In Lubbock, high-risk areas include Primrose Pointe, McAlister Park, Kings Park, Melonie Park along Restaurant Row, Ballenger, Bayless Atkins, and the area around the Lubbock County Courthouse. If your property falls in Zone A or AE, your flood insurance premiums will reflect the elevated risk, though the actual cost depends on your home’s elevation relative to the base flood elevation, construction type, and deductible choice.

Understanding Zone X and Lower-Risk Areas

Zone X properties present a different picture. The unshaded portions of Zone X indicate minimal flood risk and typically don’t require lender-mandated coverage, while shaded Zone X areas fall into moderate-risk territory. However, many Lubbock homeowners make a critical mistake: they assume no zone designation means no flood risk. FEMA data shows that approximately 25% of flood claims occur outside designated high-risk zones, and during Hurricane Harvey in 2017, more than half of flooded homes in Texas were outside mapped floodplains.

Why Lubbock’s Flood Risk Extends Beyond Maps

Lubbock’s rapid, intense rainfall patterns trigger flash flooding along creeks and arroyos even in areas not traditionally considered high-risk, making flood coverage prudent regardless of your zone. The 1970 Lubbock flood serves as a historical reminder that strong rainfall can cause significant damage across the area. FEMA determines zone boundaries by analyzing historical flood data, rainfall patterns, topography, and stream flow information, then updates maps periodically as development and climate patterns change.

Your next step involves confirming your current zone designation and understanding what that means for your specific property’s protection needs.

Lubbock’s Flood Threat and What It Means for Your Home

Lubbock sits in a region where flash flooding strikes without warning, driven by the intense rainfall that characterizes the Texas High Plains. The 1970 Lubbock flood demonstrated the area’s vulnerability to severe weather events. Today, that risk persists and has intensified. SERVPRO of Southwest Lubbock reports that storms in the area now occur with increasing frequency and heavier rainfall than in previous decades, making flood preparedness non-negotiable for any homeowner.

Urban Sprawl Amplifies Flood Risk

Urban expansion compounds Lubbock’s flood problem. As the city grows, developers replace permeable ground with concrete, rooftops, and parking lots. This reduces the soil’s ability to absorb water, forcing rainfall to run off rapidly into drainage systems and waterways. When a heavy storm hits, these systems become overwhelmed, and flooding spreads beyond traditional floodplains. This is why about 40% of flood claims occur outside designated floodplains, meaning your property faces genuine risk regardless of current FEMA maps. During Hurricane Harvey in 2017, more than half of the flooded homes across Texas sat outside mapped floodplains. Your address on a FEMA map does not guarantee your safety.

High-Risk Neighborhoods in Lubbock

Specific neighborhoods in Lubbock face elevated risk. Primrose Pointe, McAlister Park, Kings Park, and Melonie Park along Restaurant Row all sit within flood zones where lenders require coverage. Ballenger and Bayless Atkins experience similar pressures, and properties near the Lubbock County Courthouse sit in mapped high-risk areas. But this is only part of the picture.

The Standard Homeowners Insurance Gap

Standard homeowners insurance policies explicitly exclude flood damage, a fact that shocks most Lubbock residents who discover it only after water enters their homes. Your homeowners policy covers wind, hail, fire, and theft, but not flooding from any source: heavy rain, overflowing creeks, failed drainage systems, or water that backs up through drains and sewers. Mortgage lenders know this gap exists, which is why they require a separate flood insurance policy for properties in Special Flood Hazard Areas.

Why Flood Insurance Costs Less Than Flood Damage

Even if your lender does not mandate coverage because your property sits outside a mapped zone, flood insurance remains practical protection. The cost of flood damage is substantial. Repairs typically involve flooring replacement, drywall removal, mold remediation, and restoration of personal belongings, often totaling tens of thousands of dollars. A standard disaster loan from FEMA averages less than ten thousand dollars, leaving homeowners to cover the rest from savings or debt. Flood insurance premiums in Texas typically run under seven hundred dollars annually for high-risk properties and around three hundred dollars for those outside floodplains, making coverage far cheaper than absorbing a loss yourself.

Understanding your flood risk and the gaps in standard homeowners coverage sets the stage for selecting the right protection. The next section explores your flood insurance options and how to determine which coverage fits your property’s actual needs.

Getting the Right Flood Insurance Coverage for Your Property

NFIP and Private Flood Insurance: Two Distinct Paths

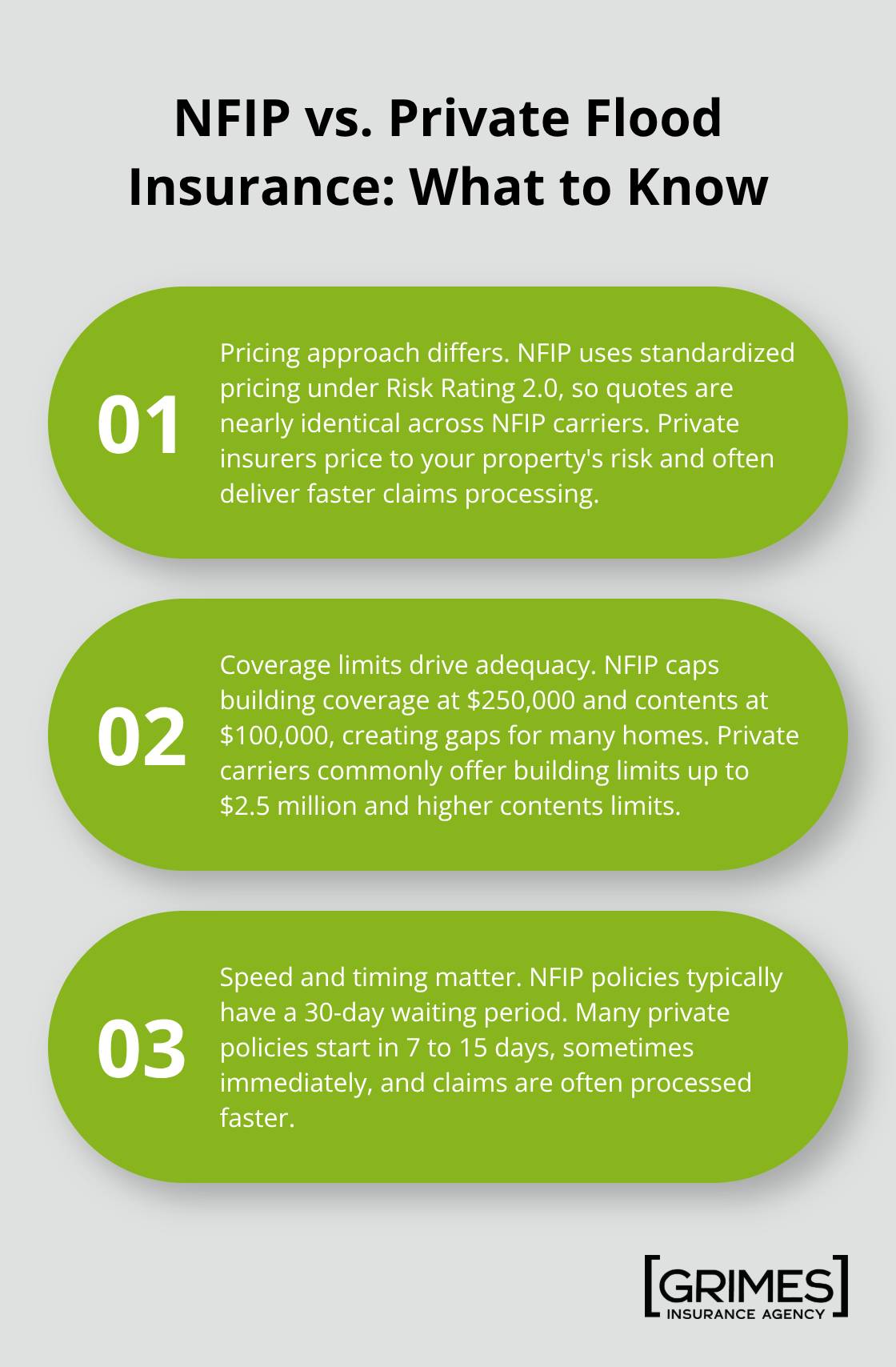

Two main paths exist for flood coverage in Lubbock: the National Flood Insurance Program administered by FEMA and private flood insurance from carriers like Wright Flood, Chubb, and Aon Edge. NFIP offers standardized pricing using Risk Rating 2.0, meaning quotes are nearly identical across all NFIP carriers, while private insurers price based on your property’s actual risk profile and often deliver faster claims processing.

NFIP caps building coverage at $250,000 and contents at $100,000, which creates a significant protection gap for homes valued above these limits. Private carriers commonly offer building limits up to $2.5 million or higher and contents limits well above NFIP maximums.

Coverage Limits and Protection Gaps

Your home’s replacement cost determines whether NFIP coverage suffices or whether you need private flood insurance to close the gap. If your home’s replacement value exceeds $250,000 for the structure alone, NFIP leaves you underinsured. NFIP also excludes basement contents coverage and loss of use expenses, meaning you won’t recover temporary housing costs after a flood. Private policies frequently include these protections, reducing your out-of-pocket recovery costs significantly. High-value items in your home may also exceed standard NFIP limits, requiring additional coverage through private carriers.

Waiting Periods and Claims Speed

NFIP policies carry a standard 30-day waiting period before coverage activates, whereas private policies typically begin in 7 to 15 days, sometimes immediately. In Lubbock’s high-risk zones, private options often cost substantially less than NFIP. Claims processing speed tends to be faster with private flood insurers due to specialized flood claims teams; NFIP relies on the broader federal system.

Steps to Select Your Coverage

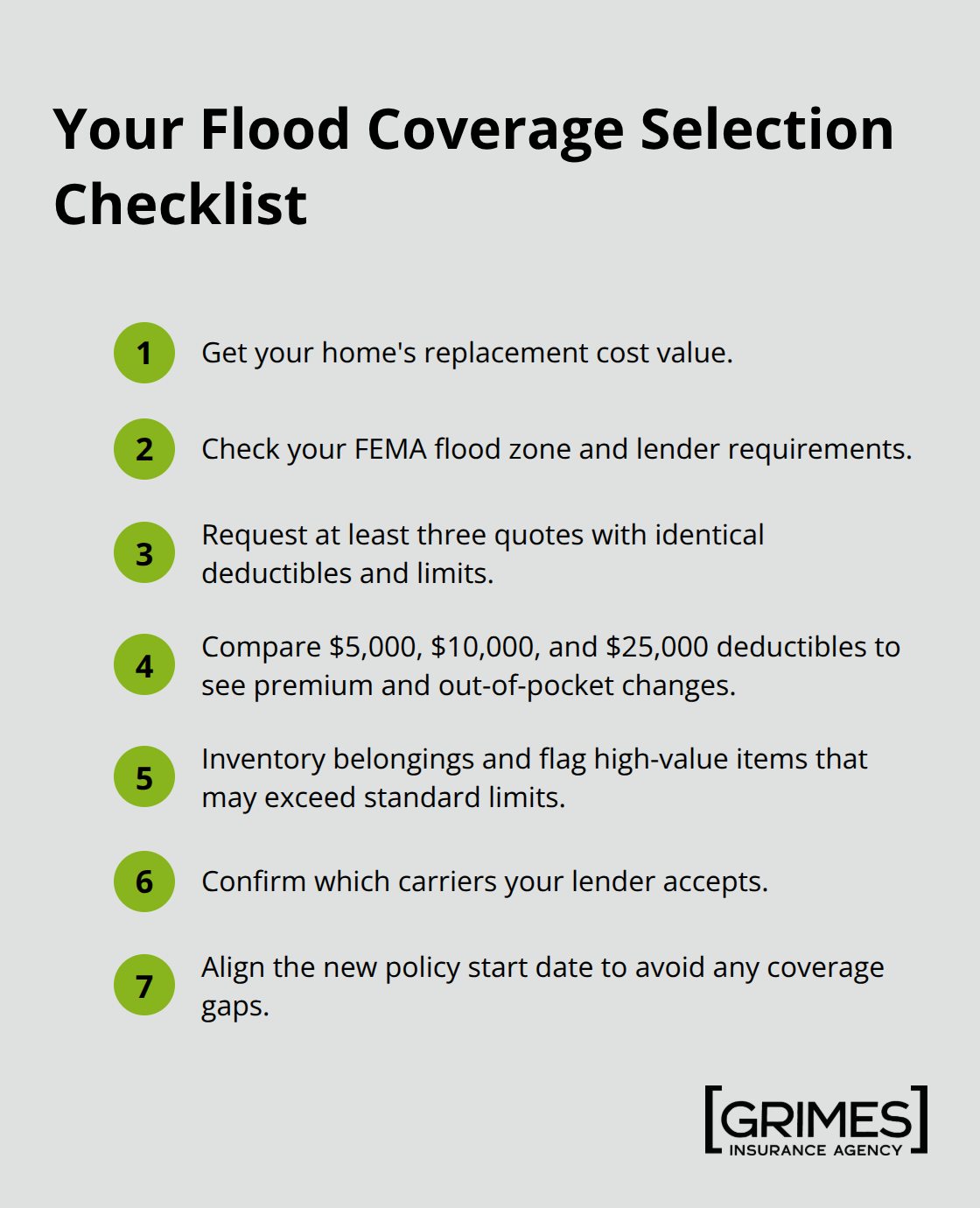

Start by obtaining your home’s replacement cost value from your homeowners insurer or a qualified appraiser, then check your flood zone on FEMA’s Flood Map Service Center to confirm whether lender-mandated coverage applies. Request quotes from at least three carriers using identical deductibles and coverage limits-testing multiple deductible levels like $5,000, $10,000, and $25,000 reveals how your total premium and out-of-pocket exposure shift. Document your personal belongings inventory and their values, paying special attention to high-value items that might exceed standard coverage limits. Contact your lender to confirm which carriers they’ll accept, as this often eliminates certain private options from consideration.

Time your new policy to start when your current coverage ends, avoiding any gaps in protection.

Final Thoughts

Your flood zone designation marks the start of your protection strategy, not the finish line. Whether you occupy a high-risk area like Primrose Pointe or a lower-risk zone, understanding flood insurance and flood zones explained allows you to act on facts rather than guesses. The data speaks clearly: one in four flood claims occur outside mapped zones, and your standard homeowners policy will not cover water damage anywhere in Lubbock.

The right flood insurance choice hinges on three factors-your home’s replacement cost, your property’s actual flood risk, and which coverage gaps matter most to your family. NFIP offers predictable pricing but caps coverage at $250,000 for the structure and $100,000 for contents, while private carriers provide higher limits, faster claims processing, and additional protections like loss of use coverage. Contact Grimes Insurance Agency to review your current coverage and explore options tailored to your property’s real risk profile.

Act now, before the next storm arrives. Waiting until heavy rain is forecast means facing the 30-day waiting period that leaves you uninsured when you need protection most. Request your flood zone confirmation today, inventory your home’s replacement value, and obtain quotes from multiple carriers to protect your largest asset from flood damage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation