3 Common Reasons for Commercial Claim Denials

Many business owners would agree that claim denials are the most frustrating part of insurance. It’s difficult trying to protect your business, customers, and employees when it seems like every claim you make gets denied.

We’ve heard hundreds of questions and complaints. Was it something you did? Was your policy missing coverage? Could you have prevented it?

At Grimes Insurance Agency, we’ve helped West Texas businesses protect themselves since 1948. And while every insurance claim is different, we’ve seen that most commercial claim denials happened for a handful of common reasons. Whether you’re a contractor, retailer, or service business, understanding these issues helps you identify possible coverage gaps before they become expensive surprises.

By the end of this guide, you will know the most common reasons commercial insurance claims get denied, how these situations happen, and what business owners and contractors (like you!) can do to avoid costly coverage gaps.

Why Do Commercial Insurance Claims Get Denied?

Despite how it feels, insurance companies don’t deny claims simply because they don’t want to pay them.

Instead, claims are typically denied for a variety of reasons:

- Undocumented business operation changes

- Incorrect or insufficient coverage

- Claim doesn’t meet policy requirements

Let’s explore these reasons in depth.

1. Your Business Changed, but Your Policy Didn’t

One of the most common reasons commercial insurance claims get denied is that the business has changed, but the insurance policy still reflects the old version of the company.

Your insurance policy is based on the information provided when coverage was purchased. If your operations expand, your policy needs to change with them.

Many business owners unintentionally create coverage gaps when they:

- Add new services

- Expand their operations

- Hire additional employees

- Take on different types of projects

A policy that accurately covered your business five years ago may not provide the same protection today.

Did you add services that aren’t listed on your commercial insurance policy?

Owners often worry that telling their insurance agent about every service they offer will increase their premiums. Sometimes, additional services do affect pricing. However, paying slightly more for accurate coverage is often far less expensive than paying out of pocket when a major claim isn’t covered.

For example:

- A landscaping company begins offering herbicide and pesticide application

- A handyman business begins performing electrical or plumbing work

- A general contractor starts taking on excavation projects

These changes may seem like natural business growth, but they can significantly change your insurance risk.

Think of your insurance policy like clothing. What fit your business when it started may not fit after years of growth. Commercial insurance policies are editable, not automatically adaptable. Your coverage needs to be reviewed when your business changes. Does your business’s coverage need to be readjusted? Request a commercial lines quote with Grimes Insurance Agency to explore your options.

Did you take on a project you’re not certified for?

It’s important to remember that the same goes for attempting projects that you don’t have the certification or resources for.

Imagine this:

A carpenter working on a residential project is asked by their client to assist with trench work around their home. Although outside of their normal operations, they agree to the project, but end up hitting a major gas line in the process. This avoidable incident could cost the carpenter up to $45,000 out of pocket!

Remember, it’s normal for smaller businesses to eventually expand their skillsets. However, offering services you’re not qualified for often results in paying out of pocket for related damage.

2. You Didn’t Have the Right Coverage for the Situation

Insurance policy language is specific. A claim can be denied simply because the policy didn’t include the type of coverage needed for that specific loss. We know, sigh.

It’s easy to assume that having “commercial insurance” means that everything related to your business is covered. However, commercial insurance is made up of different lines of coverage designed to work together and protect against different risks.

Understand your commercial policy definitions

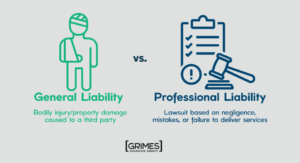

We’ve seen commercial coverage options get lumped together or left out completely, making it easy for gaps and claim denials to appear. For example, general liability and professional liability are two separate protections (despite them sounding very similar):

- General liability covers bodily injury or property damage caused to a third party.

- Professional liability covers your business in the event of a lawsuit based on negligence, mistakes, or failure to deliver professional service claims against your business.

A business having one but not the other leaves it exposed and with greater risk.

So, let’s imagine together. Say a construction company has general liability insurance, but not professional.

During construction, a subcontractor drops a steel beam, causing damage to a parked delivery truck. The incident, however, is covered by general liability.

On the other hand, the contractor misreads blueprints and builds a weak foundation. The accident causes the building to become unstable, shut down, and the building’s owner sues for damages. Since it’s due to faulty workmanship, general liability won’t cover the claim– and without professional liability, the contractor must pay for repairs out of pocket.

Having insurance doesn’t always mean having the right insurance. The details of your coverage matter. It’s important to understand the difference between your coverage options and where risk might lie. To learn how liability insurance can protect your business’s assets, read about the importance of liability insurance for businesses.

3. The Claim Didn’t Qualify Under Your Policy

Even when a loss appears covered, failing to follow your policy requirements can create problems during the claims process.

In addition to specific language, insurance policies include conditions that businesses must follow. Missing these requirements can affect whether your claim is paid.

Common policy requirements can include:

Late reporting

Most policies require businesses to report claims or potential claims within a certain time frame. Waiting too long can make it more difficult for the insurance company to investigate what happened.

Policy exclusions

Every insurance policy has certain exclusions. Exclusions are specific situations that are not covered under your policy. Some exclusion examples include:

- Natural disasters (such as an earthquake, etc.)

- Criminal acts you’ve committed

- Maintenance issues

Deductibles

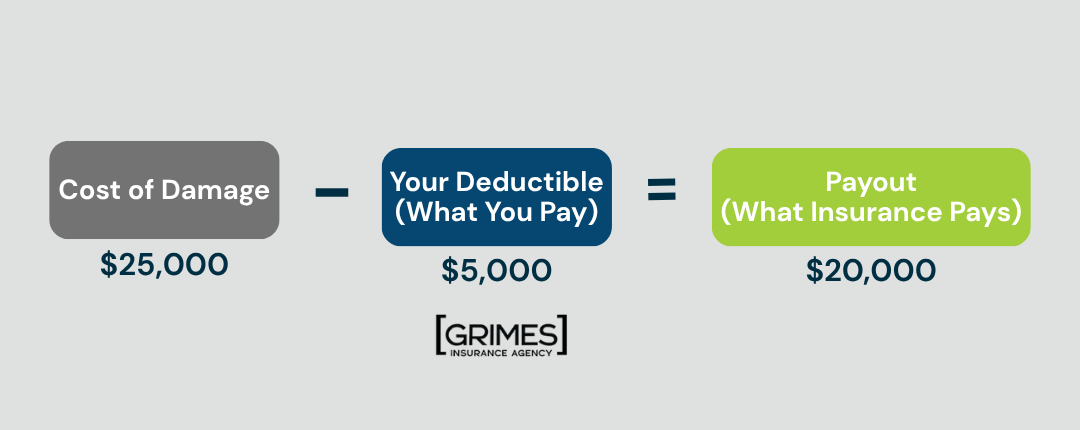

Your policy deductible is the amount you’re responsible for paying before insurance coverage applies to a claim. For example, if you had a claim worth $25,000, and your deductible was $5,000, the amount your insurance would pay is $20,000.

It’s important to understand how deductibles work for your business’s specific policy. It’s worth discussing with your agent ahead of time, so you’re not surprised when it comes time to file a costly claim.

Documentation

A general rule of thumb? Document everything. Yes… everything. Proper documentation can make the claims process much smoother.

The more information you can provide, the easier it is to demonstrate what happened and why the claim should be covered.

How Can You Avoid a Commercial Insurance Claim Denial?

The best way to prevent a denied claim is to regularly review your coverage. Ensure that your insurance reflects your current business and offerings.

The majority of claim denials boil down to the same issue: a lack of transparency. Be clear about your business, the services you provide, and the work you do so that you can get the coverage you actually need.

Grimes Helps You Identify Coverage Gaps Before They Cost You

Running a business comes with risks, but a denied insurance claim doesn’t have to be one of them. If your business has grown, added services, or changed how you operate, your insurance coverage should change with it.

Now that you understand why commercial claim denials occur, it’s time for you to reevaluate your business’s coverage. At Grimes Insurance Agency, we believe your business is worth protecting. Our team can help you review your current coverage, identify potential gaps, and make sure your policy matches your current business risks.

Are you a West Texas business owner unsure about what coverage your business needs? Read our guide on understanding business insurance requirements in Texas before connecting with an agent to discuss your commercial insurance policy.