Home Insurance Tips for First-Time Buyers: A Guide to Getting Started

Buying your first home is exciting, but the insurance part often feels overwhelming. We at Grimes Insurance Agency know that home insurance tips for first-time buyers aren’t always easy to find in one place.

This guide walks you through the coverage types you actually need, how to calculate the right amounts, and how to compare quotes without overpaying. You’ll have the clarity to make a confident decision.

Understanding Home Insurance Coverage Types

The Four Core Pieces of Home Insurance

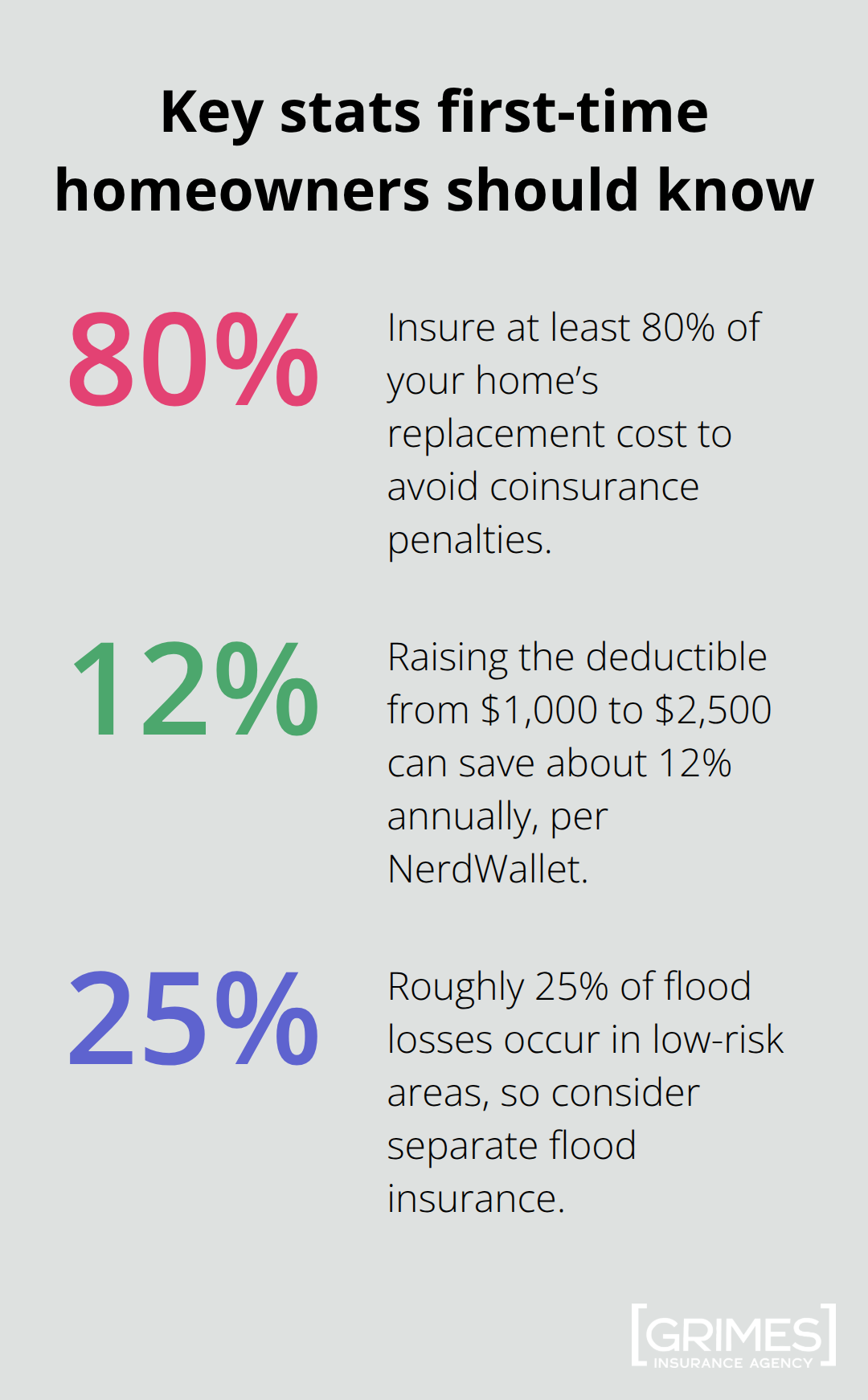

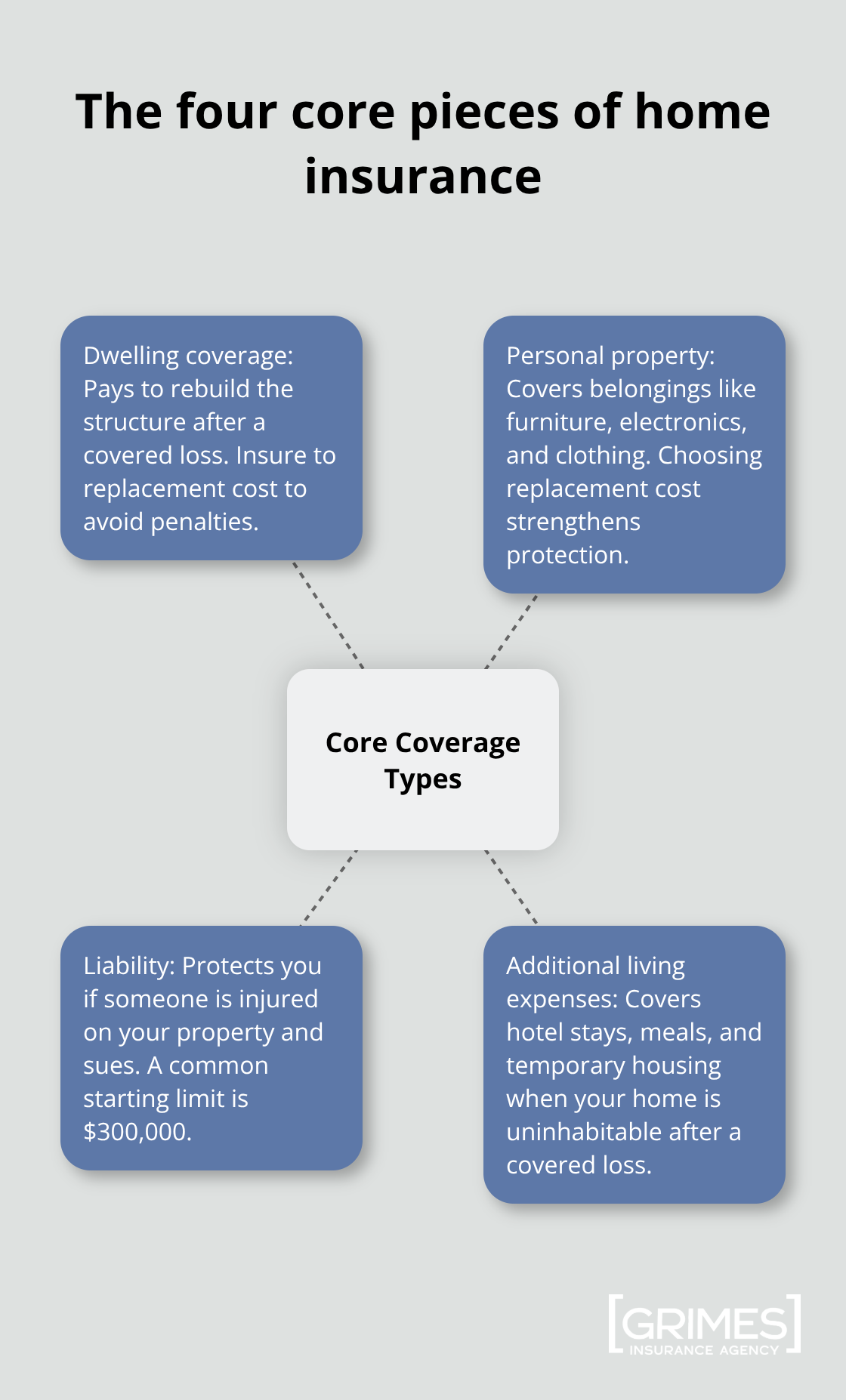

Home insurance has four core pieces, and understanding each one prevents costly gaps when you need protection most. Dwelling coverage pays to rebuild your house itself-the walls, roof, foundation, and attached structures-if a covered disaster strikes. This is the foundation of your policy, and the Insurance Information Institute recommends insuring your home for at least 80 percent of its replacement cost to avoid coinsurance penalties if you file a claim. If your home costs $300,000 to rebuild and you only insure it for $200,000, you’ll face out-of-pocket costs on any major loss.

Personal property coverage protects your belongings inside the home-furniture, electronics, clothing, and kitchen items. The Insurance Information Institute notes this typically covers 50 to 70 percent of your dwelling coverage amount, so a $300,000 home usually gets $150,000 to $210,000 in personal property protection. That sounds reasonable until you realize most first-time buyers underestimate what they actually own. A basic inventory of a three-bedroom home easily exceeds $100,000 when you count everything from appliances to clothes to tools.

Liability coverage protects you if someone is injured on your property and sues. A common starting point is $300,000, though the Insurance Information Institute suggests $500,000 for larger assets or higher-risk situations. Additional living expenses cover hotel stays, meals, and temporary housing if your home becomes uninhabitable after a covered loss-this protection is often overlooked but essential.

Replacement Cost vs. Actual Cash Value

The real problem most first-time buyers face is the choice between replacement cost coverage and actual cash value for personal property. Replacement cost pays what it costs to buy new items today; actual cash value subtracts depreciation, so a five-year-old television worth $800 new might only pay out $300. You should always choose replacement cost-the premium difference is small, typically around 10 to 15 percent more, but the protection is dramatically better.

For high-value items like jewelry, art, or collectibles, standard coverage has limits that won’t fully protect them. A scheduled personal property endorsement lists these items separately with current appraisals, so you receive full coverage without sublimits. This costs extra but prevents major financial loss on your most valuable possessions.

Deductibles and Location-Specific Risks

Deductibles directly affect your premium, and raising yours from $1,000 to $2,500 can save roughly 12 percent annually according to NerdWallet data. The catch is selecting a deductible you can actually afford to pay out of pocket after a loss-there’s no point saving $250 a year if a $2,500 deductible would devastate your finances.

Location matters significantly too. Flood damage is not covered by any standard homeowners policy; you need separate flood insurance through the National Flood Insurance Program or a private carrier. About 25 percent of flood losses occur in low-risk areas, so don’t skip this just because you’re not in a designated flood zone. Earthquake coverage is similarly excluded and requires a separate endorsement. Understanding these exclusions before disaster strikes is the difference between being protected and being broke.

Now that you understand what your policy covers and what it doesn’t, the next step is calculating exactly how much coverage you actually need for your specific home and belongings.

Calculating Your Home’s True Coverage Need

Understanding Replacement Cost vs. Market Value

Most first-time buyers get this wrong, and it costs them thousands. Your home’s replacement cost is not what you paid for it or what it would sell for today-it’s what it would cost to rebuild from the ground up with current labor and materials. A $400,000 home in Lubbock might cost $450,000 to rebuild due to construction inflation, and that’s the number you need to insure. The National Association of Insurance Commissioners and the Insurance Information Institute both stress the 80 percent rule: insure at least 80 percent of replacement cost to avoid coinsurance penalties. If your rebuild cost is $450,000 and you only insure for $300,000, the insurer treats you as underinsured and pays claims proportionally-meaning a $50,000 loss might net you only $33,000. Your mortgage lender will require proof of adequate coverage anyway, so there’s no escaping this calculation.

Finding Your Accurate Rebuild Cost

Contact a local contractor or use online rebuild calculators specific to your region to estimate replacement cost accurately. Add 10 to 15 percent as a safety margin for inflation. This step takes time but protects you from massive financial exposure later.

Inventorying Your Personal Property

Personal property coverage demands a hard reality check because most people drastically underestimate what they own. Furniture, electronics, kitchen items, tools, clothing, and seasonal gear add up fast-a typical three-bedroom home contains $100,000 to $150,000 in belongings. Create a detailed inventory by walking through each room with your phone and photographing items, then note serial numbers and purchase prices. This takes a few hours but saves enormous time and dispute during a claim.

Standard personal property coverage tops out at 50 to 70 percent of dwelling coverage, which often leaves gaps. If your dwelling is insured for $400,000, you get roughly $200,000 to $280,000 in personal property protection-potentially not enough. For high-value items like jewelry, art, or electronics, purchase scheduled personal property endorsements with current appraisals so sublimits don’t cap your recovery.

Addressing Location-Specific Risks

Location-specific risks also affect coverage needs. Flood damage strikes about 25 percent of claims in low-risk areas, yet standard policies exclude it entirely, so flood insurance through the National Flood Insurance Program becomes essential if you’re within a mile of water or in any flood-prone region. Similarly, earthquake coverage requires a separate endorsement in most states. Don’t skip these because you think your area is safe-FEMA data shows flood damage happens in unexpected places, and the cost of separate coverage is negligible compared to a total loss with no payout.

Once you’ve calculated your coverage amounts and identified location-specific gaps, the next critical step is comparing quotes across multiple insurers to find the best rate without sacrificing protection.

How to Compare Quotes and Find the Best Rate

Shop Multiple Insurers with Identical Coverage

Shopping for homeowners insurance means comparing quotes from at least three different insurers with identical coverage limits and deductibles to see real price differences. NerdWallet data shows dwelling coverage cost varies dramatically by carrier: a $300,000 policy averages $2,110 annually across the market, but individual insurers range from significantly cheaper to substantially more expensive. Travelers often offers the lowest average price among major carriers, while USAA consistently ranks as cheapest for eligible members like active military and veterans. When you gather quotes online or through an agent, compare apples to apples-same $300,000 dwelling limit, same $1,000 deductible, same personal property coverage-or the numbers become meaningless.

Verify Financial Strength Before Deciding

Check each insurer’s financial strength rating with A.M. Best or Standard & Poor’s because the cheapest quote means nothing if the company cannot pay claims after a major disaster. Your mortgage lender will require proof of coverage anyway, so spending an extra hour comparing quotes from three to five carriers could save you $300 to $500 annually. Financial strength ratings tell you whether an insurer has the reserves to handle large claims during disaster seasons when many policyholders file simultaneously.

Use Deductibles to Control Your Premium

Deductible selection directly controls your premium without sacrificing actual protection because you simply decide how much you will contribute to claims yourself. Raising your deductible from $1,000 to $2,500 saves approximately 12 percent on your annual premium according to NerdWallet analysis, which translates to roughly $250 per year on a $2,110 baseline policy. The critical rule is choosing a deductible you can afford out of pocket without financial strain-a $2,500 deductible saves money only if you have $2,500 in emergency savings available when you need it.

Some policies use percentage-based deductibles for specific perils like wind or hail, meaning a 2 percent deductible on $150,000 dwelling coverage equals a $3,000 out-of-pocket cost for that specific peril. Understanding your deductible structure prevents surprises when you file a claim.

Maximize Discounts Available to New Homeowners

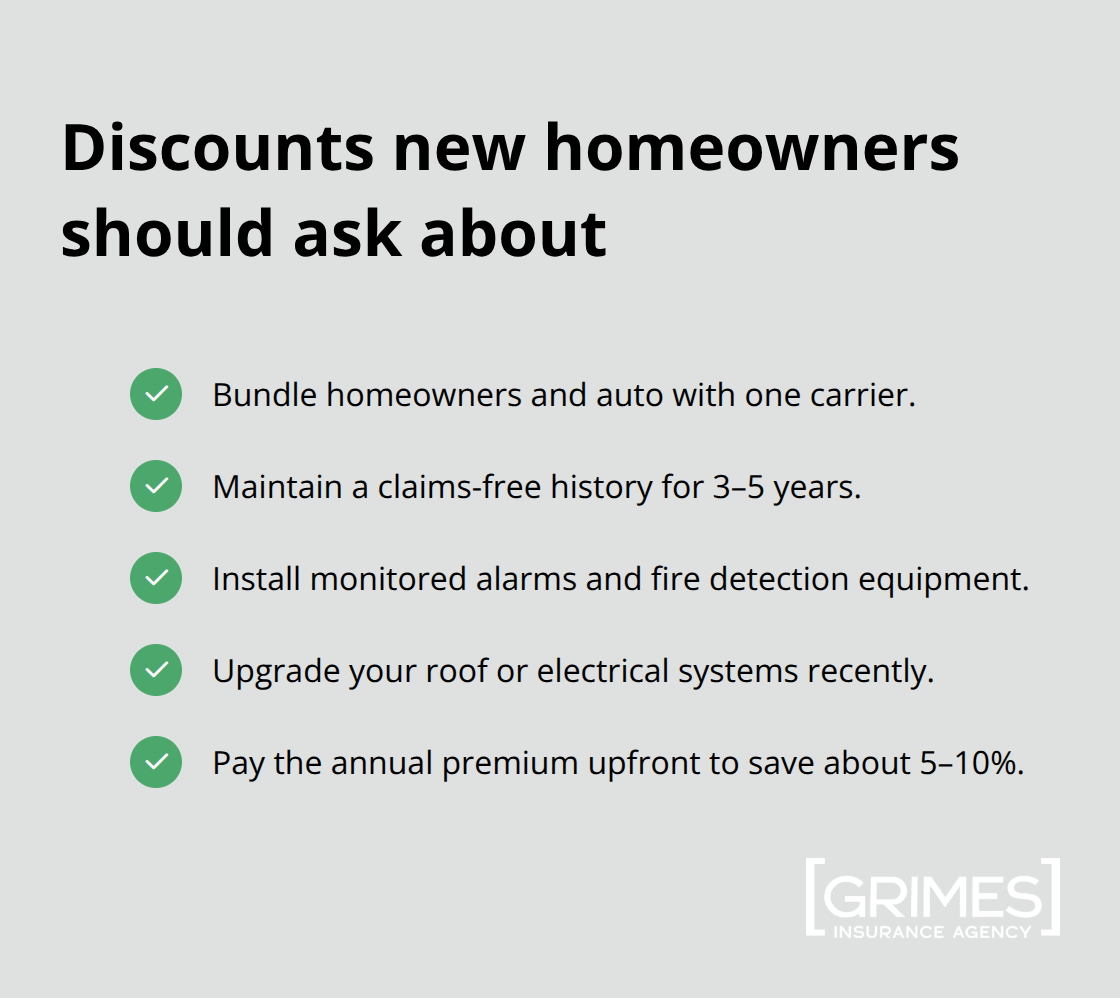

Bundling homeowners and auto insurance with the same carrier can reduce your combined cost, making this one of the highest-impact discounts available. New homeowners often qualify for additional discounts: claims-free history discounts apply if you have had no claims in the past three to five years, safety device discounts reward monitored alarm systems and fire detection equipment, and home upgrade discounts apply if you have recently replaced your roof or updated electrical wiring. Ask each insurer specifically about these discounts because they do not always appear in online quotes automatically. Some carriers offer discounts for paying your annual premium upfront rather than monthly, which can reduce costs by another 5 to 10 percent.

Final Thoughts

You now have the foundation to make a confident home insurance decision. The core takeaway is simple: insure your home for at least 80 percent of its replacement cost, choose replacement cost coverage for your belongings, and select a deductible you can actually afford. These three decisions eliminate the biggest mistakes first-time buyers make, and location-specific risks like flood and earthquake damage require separate policies, not optional add-ons.

Your next step is gathering quotes immediately after your offer is accepted. Contact insurers directly or work with an independent agent who can access multiple carriers at once, saving you time and ensuring you compare apples to apples. Verify financial strength ratings for any carrier you consider, then ask about bundling discounts, claims-free discounts, and safety device discounts specific to your situation.

Working with a local agent makes a real difference because they understand your specific market, know which carriers offer the best rates in your area, and can tailor coverage to your actual needs rather than pushing generic policies. Contact Grimes Insurance Agency in Lubbock to discuss your specific situation and receive personalized quotes that reflect your home, your belongings, and your budget-our team knows Texas homes, Texas risks, and Texas insurance requirements in ways national call centers simply cannot match.