Deductibles Are Levers: A Proven Way to Lower Your Insurance Premiums

A re you looking for ways to lower your insurance premiums without sacrificing protection? You’re not alone. In today’s world, the cost of insurance—whether it’s home, auto, commercial, or health insurance—has gone up dramatically. Families and business owners are asking the same question: “How can I save money on my insurance?”

re you looking for ways to lower your insurance premiums without sacrificing protection? You’re not alone. In today’s world, the cost of insurance—whether it’s home, auto, commercial, or health insurance—has gone up dramatically. Families and business owners are asking the same question: “How can I save money on my insurance?”

One of the simplest, most effective answers is to adjust your deductible.

The Lever Analogy: How Deductibles Work

Think of your insurance premium like a giant boulder. On your own, it feels impossible to move. But just like early civilizations used a lever to shift heavy rocks, you can use your deductible as a lever to move the cost of your insurance.

- The premium is the boulder.

- The deductible is the lever.

- The higher your deductible, the longer the lever—and the more savings you can unlock.

Why Higher Deductibles Lower Insurance Costs

While many factors affect your rate—like your driving record, the type of car you drive, or how many miles you put on it each year—the deductible is one of the most powerful levers you control.

When you raise your deductible, your insurance company is taking on less risk for smaller claims. In return, they reward you with lower annual premiums. This simple shift can save hundreds, even thousands, over time.

Insurance for Catastrophic Events

The biggest savers adopt a smart mindset: insurance is for catastrophic events, not everyday expenses. That means:

- Paying small to medium claims out of pocket.

- Avoiding unnecessary claims that raise your rates.

- Keeping your deductible high to maximize premium savings.

This strategy keeps your insurance affordable while still protecting you when you truly need it most.

Real-Life Examples

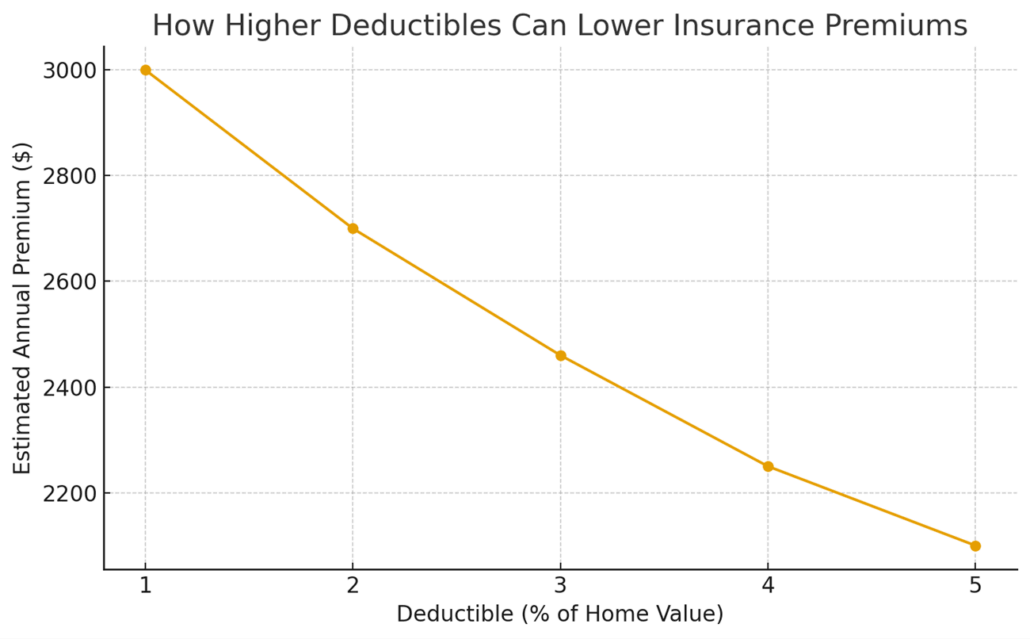

Let’s compare two identical home insurance policies:

- Policy A: 1% deductible

- Policy B: 5% deductible

In this case, Policy A would have a higher premium than Policy B. When considering which option makes the most sense, ask yourself:

- How much will I save annually by increasing my deductible?

- If I don’t file a claim for 4 years, how much will I have saved in total?

- If I do file a claim, do I have enough savings to cover the larger deductible?

These questions help you think constructively about whether a higher deductible fits your financial situation. Remember, the goal is not just to cut costs—it’s to manage risk responsibly.

Here’s a chart to illustrate how deductibles and premiums have an inverse relationship:

Time to Take Action

Now that you understand how deductibles act as levers to lower your insurance premiums, it may be time to have a conversation with your agent. Ask them to run quotes showing your premium options with varying higher deductibles.

Be sure to review this for both your home insurance and auto insurance policies.

And if you’re not currently working with an independent insurance agency, that’s where we come in. Independent agents like Grimes Insurance Agency can compare multiple carriers to find you the most competitive rates.

📞 Call us today at 806-589-9565

🌐 Visit us online at www.GrimesInsurance.com

Let us help you leverage deductibles the smart way—so you can save money while keeping your family and business protected.