Most renters assume their landlord’s insurance covers their belongings. It doesn’t-and that gap can cost thousands if disaster strikes.

At Grimes Insurance Agency, we’ve seen renters lose everything from fires, theft, and water damage without a safety net. Home insurance for renters is affordable and fills the protection holes that landlord policies leave wide open. This guide walks you through what you actually need to know.

Why Renters Need Insurance

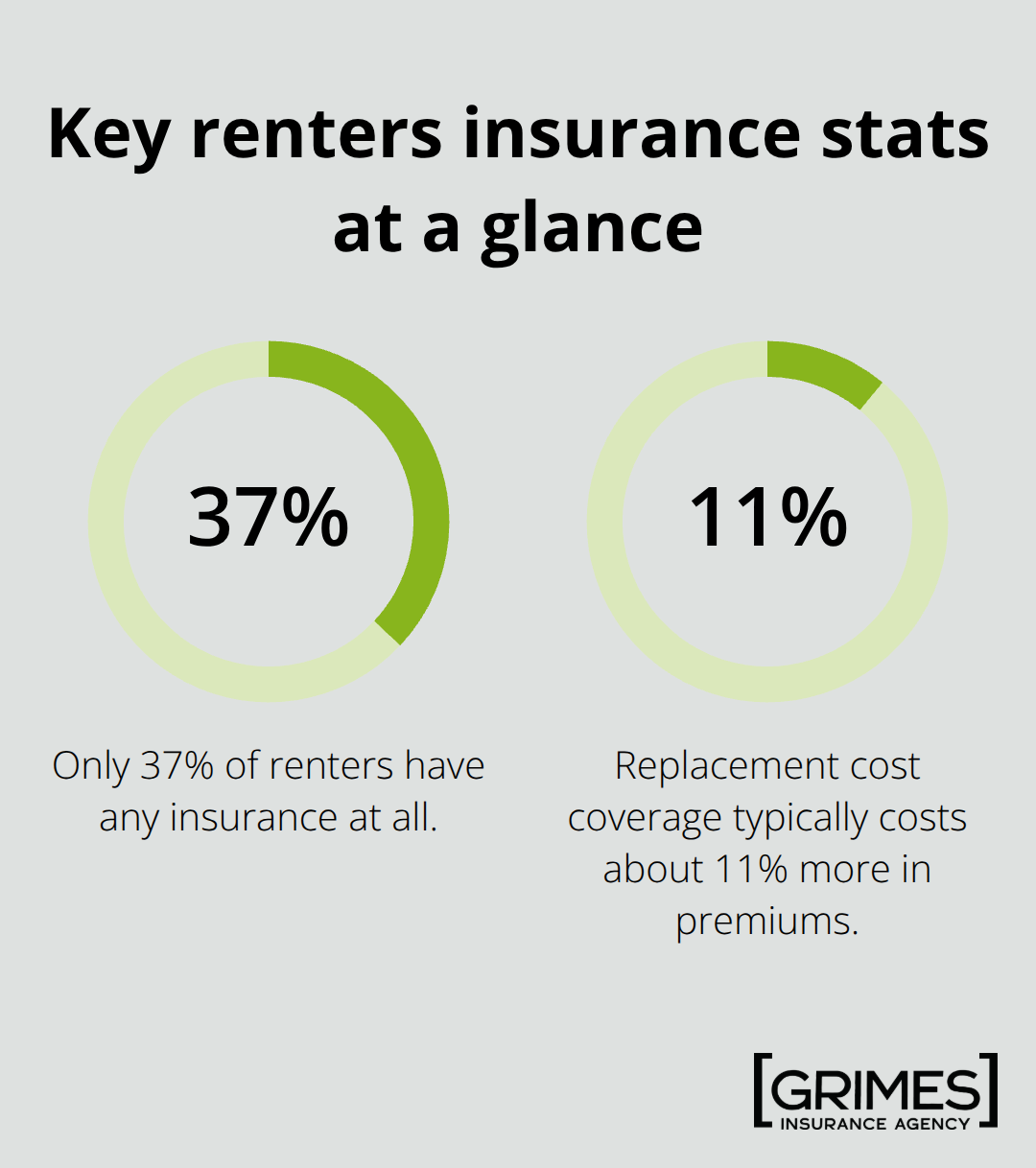

Your personal belongings are worth far more than you probably realize. The average renter owns about $30,000 worth of possessions, yet only 37% of renters carry any insurance at all. That gap between what you own and what you protect creates serious financial exposure. If a fire breaks out, a pipe bursts, or theft occurs, your landlord’s insurance won’t cover a single item in your apartment.

Landlord policies protect the building structure only-not tenant belongings. This means you’re personally liable for replacing everything from furniture and electronics to clothing and kitchenware. The cost of rebuilding your life after a loss without coverage can reach tens of thousands of dollars, which most people cannot absorb.

Personal property coverage protects what you own

Renters insurance reimburses you for belongings damaged or stolen during covered events like fire, smoke, theft, vandalism, wind, and hail. If a water pipe bursts and ruins your couch, television, and clothing, your policy pays to replace them. The Insurance Information Institute reports that renters insurance costs only $15–$20 per month on average, making it remarkably affordable compared to the replacement cost of your possessions. You choose your coverage limit based on what you own-typically ranging from $20,000 to $40,000 for standard renters. For high-value items like jewelry, cameras, or electronics, you can add scheduled coverage to ensure full replacement value. Without this protection, you absorb 100% of the loss yourself.

Liability coverage shields you from lawsuits

Accidents happen. Someone trips on your stairs and breaks their leg. Your guest damages a neighbor’s property while visiting you. You accidentally damage a rental car. Your personal liability coverage pays for medical bills, legal fees, and damages you’re legally responsible for-up to your policy limit. Standard liability limits start at $100,000, though you can purchase up to $300,000 or more. The Insurance Information Institute notes that raising your liability limit from $100,000 to $300,000 costs only about $1 more per month. This modest increase protects your wages and assets in case someone sues you for a serious injury. Without liability coverage, a lawsuit judgment could force you to pay thousands out of pocket or face wage garnishment.

Additional living expenses cover temporary relocation

If your rental becomes uninhabitable due to a covered loss, additional living expenses coverage pays for hotel stays, meals, and other temporary housing costs while repairs happen. This coverage typically ties to your personal property limit or provides a separate amount. After a fire or major water damage, you shouldn’t have to pay for a hotel out of pocket while waiting for repairs. This protection keeps you financially stable during a crisis when you’re already stressed about your damaged belongings and displaced life. Understanding what renters insurance covers-and what it doesn’t-helps you avoid surprises when you need protection most.

What Renters Insurance Covers and Doesn’t Cover

Personal property coverage protects your belongings

Personal property coverage pays the replacement cost of your belongings when damage or theft occurs from covered perils. Fire, smoke, theft, vandalism, wind, and hail all trigger coverage for items inside your rental. A water pipe bursts and destroys your furniture, appliances, and clothing-your policy reimburses you. A thief breaks in and takes your laptop and jewelry-you’re covered. However, your coverage limit matters enormously. Most renters carry between $20,000 and $40,000 in personal property protection, according to the Insurance Information Institute. If you own $35,000 in belongings but only purchase $20,000 in coverage, you absorb the $15,000 gap yourself.

High-value items create a specific problem. Standard policies cap coverage on jewelry, watches, and electronics at around $1,500 to $2,500 per item. If you own a $4,000 camera or $3,000 engagement ring, you need scheduled coverage-an endorsement that lists these items separately and guarantees full replacement value. Without scheduling, you face a partial loss.

Your deductible also affects what you actually recover. A $500 deductible means you pay the first $500 of any claim; the insurer covers the rest. Jump to a $1,000 deductible and your premium drops slightly, but you’re responsible for twice as much out-of-pocket. The Insurance Information Institute reports that deductibles typically range from $250 to $1,000, so choose based on what you can actually afford to pay in an emergency.

Liability and medical payments protect you from lawsuits

Liability coverage protects you when someone is injured at your rental or you damage someone else’s property. A guest slips on your wet kitchen floor and breaks their arm-your liability coverage pays their medical bills and legal costs if they sue. You accidentally damage your neighbor’s wall during a party-liability covers the repair bill. Standard liability starts at $100,000, which many renters consider baseline protection. However, raising that limit to $300,000 costs only about $12 more per year, according to rate analyses by NerdWallet.

Medical payments coverage is separate and smaller-typically $1,000 to $5,000-and pays a guest’s immediate medical expenses without requiring them to sue you. This coverage exists to prevent lawsuits in the first place.

Major exclusions leave critical gaps

Flood and earthquake damage are the major exclusions renters encounter. Standard policies don’t cover either, meaning a basement flood or seismic event leaves you unprotected. If you live in a flood-prone area, you need separate flood insurance through the National Flood Insurance Program or a private insurer.

Earthquake coverage requires a separate endorsement in most states.

Water damage from burst pipes is covered, but water intrusion from outside-like heavy rain seeping under a door-typically isn’t. Wear and tear, maintenance issues, and damage from pests or rodents fall outside coverage. Your landlord’s responsibility for repairs doesn’t trigger your renters policy.

Business property and work-from-home equipment face coverage limits too. If you run a home business and your office equipment is stolen, standard renters policies may not cover it fully or at all. Some insurers exclude business property entirely, so you’ll need to ask about coverage options when you shop for a policy.

Document your belongings to support claims

Create an inventory of your belongings with photos and estimated values to confirm your coverage limit is adequate. Store this inventory digitally or offsite so you have proof if you need to file a claim. Include serial numbers for electronics and receipts for expensive items (jewelry, appliances, furniture). This documentation speeds up the claims process and prevents disputes over replacement value. When you understand what your policy covers and what it excludes, you can identify gaps and add endorsements before a loss occurs. The next step is selecting the right coverage limits and comparing quotes to find the best protection for your situation.

How to Choose the Right Renters Insurance Policy

Start by walking through your apartment and honestly assessing what you’d need to replace. Open your closet, kitchen cabinets, drawers, and storage areas. Write down major items: furniture, electronics, clothing, kitchenware, books, sports equipment, tools. Most renters drastically underestimate their belongings until they actually count them. The average renter owns about $30,000 in possessions, according to Allstate, yet many purchase policies with only $15,000 or $20,000 in coverage.

Take photos of each room and any high-value items, then research replacement prices online. A decent couch runs $800 to $2,000, a bedroom set costs $1,500 to $4,000, and electronics add up fast. Once you have a realistic total, add 10 to 15 percent as a buffer for items you forgot. This number becomes your personal property coverage target. Your coverage limit directly determines how much you recover after a loss, so accuracy matters enormously.

Compare quotes from at least three insurers

Shopping for renters insurance takes about an hour but saves hundreds over time. Contact three to five insurers-major carriers like State Farm, Allstate, and Liberty Mutual, plus regional options-and request quotes with identical coverage limits and deductibles. NerdWallet’s analysis found that the same policy from different insurers varies by hundreds of dollars annually depending on your location and credit score.

A non-smoking tenant with good credit in a two-bedroom apartment might pay $151 per year for a baseline policy with $30,000 personal property coverage, $100,000 liability, and a $500 deductible, but your location dramatically shifts this. Louisiana renters pay about $266 annually on average, while Vermont renters pay roughly $110. Houston averages $241 per year while Seattle averages $130. Your zip code, local crime rates, and proximity to fire services are the primary price drivers.

When comparing quotes, verify whether each includes replacement cost coverage-not actual cash value-because replacement cost pays to replace items at current prices without depreciation. Actual cash value pays depreciated value, leaving you short on older belongings. Replacement cost typically costs about 11 percent more in premiums but protects you far better.

Select a deductible you can actually afford

Your deductible is the amount you pay out of pocket before insurance kicks in. Standard deductibles range from $250 to $1,000, according to the Insurance Information Institute. Choose a higher deductible only if you can actually afford to pay that amount in an emergency. A renter with $500 in savings should never pick a $1,000 deductible because they couldn’t afford the out-of-pocket cost if they filed a claim.

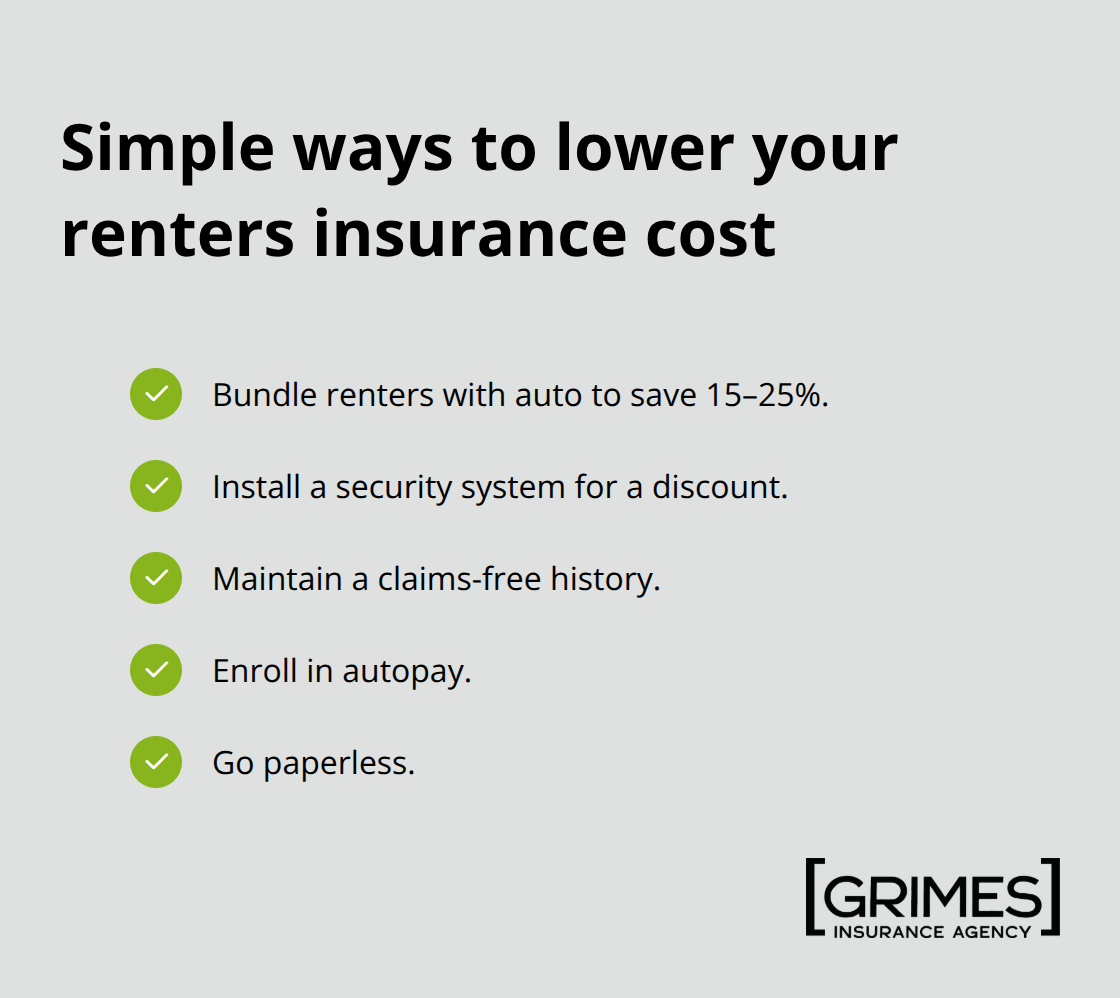

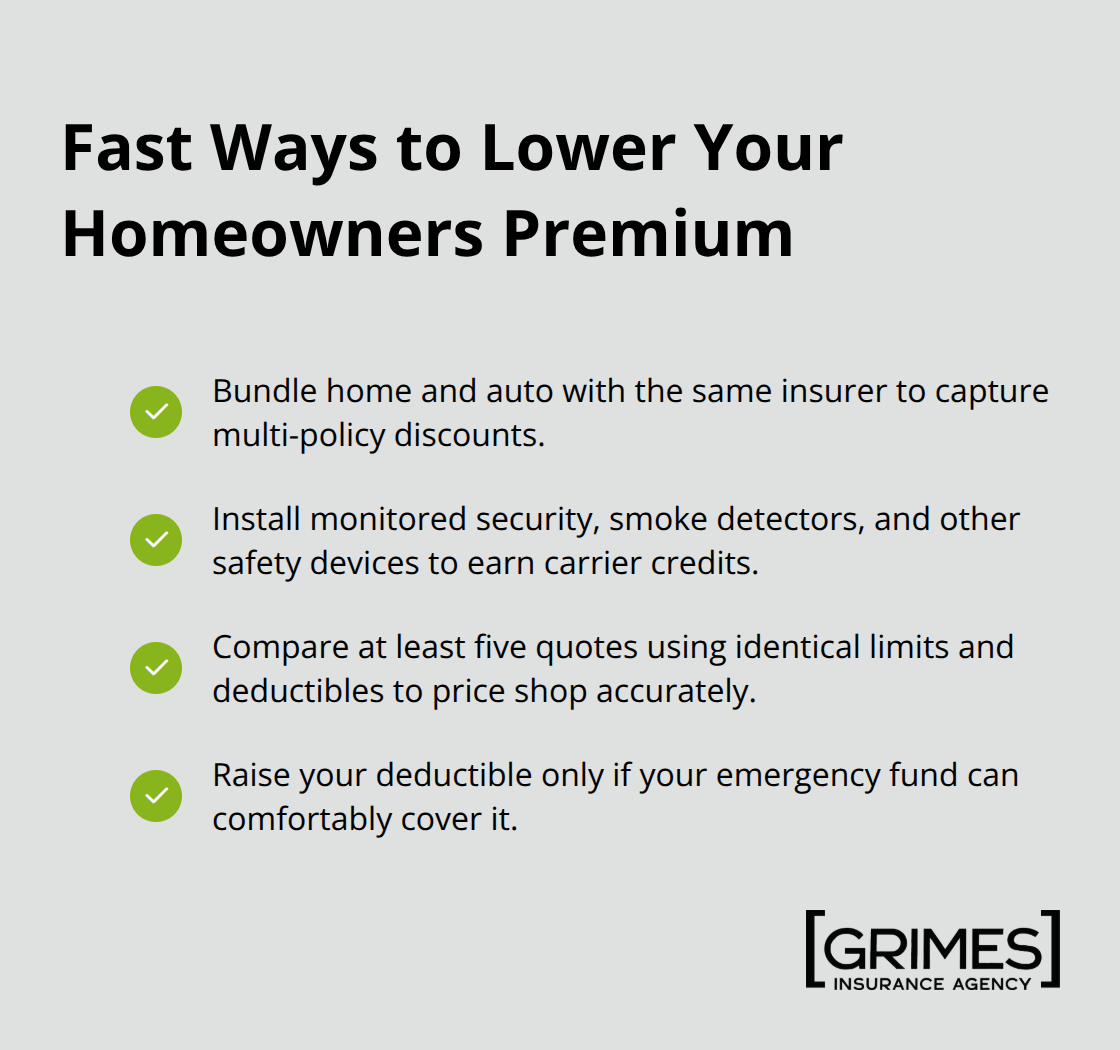

The monthly premium savings rarely justify the financial strain. NerdWallet’s analysis shows that jumping from a $500 deductible to $1,000 saves money monthly but not dramatically-often just $3 to $8 per month depending on your profile. Instead, select a deductible you could cover within 30 days if needed, then focus on bundling discounts to lower your overall cost. Bundling renters insurance with auto insurance typically saves 15 to 25 percent on each policy.

Other discounts include installing a security system, maintaining a claims-free history, paying by autopay, and going paperless. These discounts stack and often exceed any premium savings from raising your deductible.

Increase liability limits and schedule high-value items

Liability coverage deserves attention beyond the standard $100,000 limit. Most renters select this baseline, but NerdWallet found that upgrading to $300,000 costs only about $12 more annually. Given the legal costs and potential judgment from a serious injury lawsuit, this small increase protects your assets significantly.

Schedule high-value items separately-jewelry, cameras, instruments, or collectibles-because standard policies cap individual item coverage at roughly $1,500 to $2,500. Your engagement ring or camera equipment needs its own rider to guarantee full replacement value. Once you’ve gathered quotes and adjusted coverage limits to match your actual situation, you’re ready to finalize your choice and get protected.

Final Thoughts

Renters insurance protects your belongings and finances at a cost most people can afford-typically $15 to $20 per month. Your landlord’s policy covers only the building structure, leaving your possessions completely unprotected if fire, theft, or water damage strikes. Home insurance for renters fills that gap and prevents a single disaster from derailing your financial stability.

Start by walking through your apartment and photographing your belongings, then request quotes from three to five insurers with identical coverage limits. Most people complete this process in under an hour and discover significant price differences between carriers. When comparing quotes, prioritize replacement cost coverage, verify your liability limit protects your assets, and schedule high-value items separately to guarantee full replacement value.

We at Grimes Insurance Agency work with multiple carriers to find you the best protection at competitive pricing. Our team can answer your questions about coverage options and help you select the right limits for your situation. Contact us today to get a quote and protect what matters most.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

“I was involved in an accident, and to make matters worse, the other party doesn’t have insurance.” It’s a frustrating and stressful situation that no one wants to experience. However, there are measures you can take to protect yourself from such incidents. One important aspect is having the right insurance coverage, specifically uninsured motorist coverage, which can provide you with the necessary financial support in these unfortunate circumstances.

“I was involved in an accident, and to make matters worse, the other party doesn’t have insurance.” It’s a frustrating and stressful situation that no one wants to experience. However, there are measures you can take to protect yourself from such incidents. One important aspect is having the right insurance coverage, specifically uninsured motorist coverage, which can provide you with the necessary financial support in these unfortunate circumstances.

Experiencing a home disaster is a situation nobody wants to face, but unfortunately, it can happen unexpectedly. If such a disaster were to strike, would you be able to provide a detailed list of all the valuables in your home? If your answer is uncertain or no, it’s crucial to create a comprehensive home inventory list that includes all your valuable possessions.

Experiencing a home disaster is a situation nobody wants to face, but unfortunately, it can happen unexpectedly. If such a disaster were to strike, would you be able to provide a detailed list of all the valuables in your home? If your answer is uncertain or no, it’s crucial to create a comprehensive home inventory list that includes all your valuable possessions.