Most homeowners buy insurance without fully understanding what they’re actually protected against. At Grimes Insurance Agency, we’ve seen firsthand how gaps in coverage can leave families vulnerable when they need protection most.

Home insurance basics matter more than you might think. This guide walks you through what your policy covers, how to set the right limits, and the mistakes that could cost you thousands.

What Your Policy Actually Covers

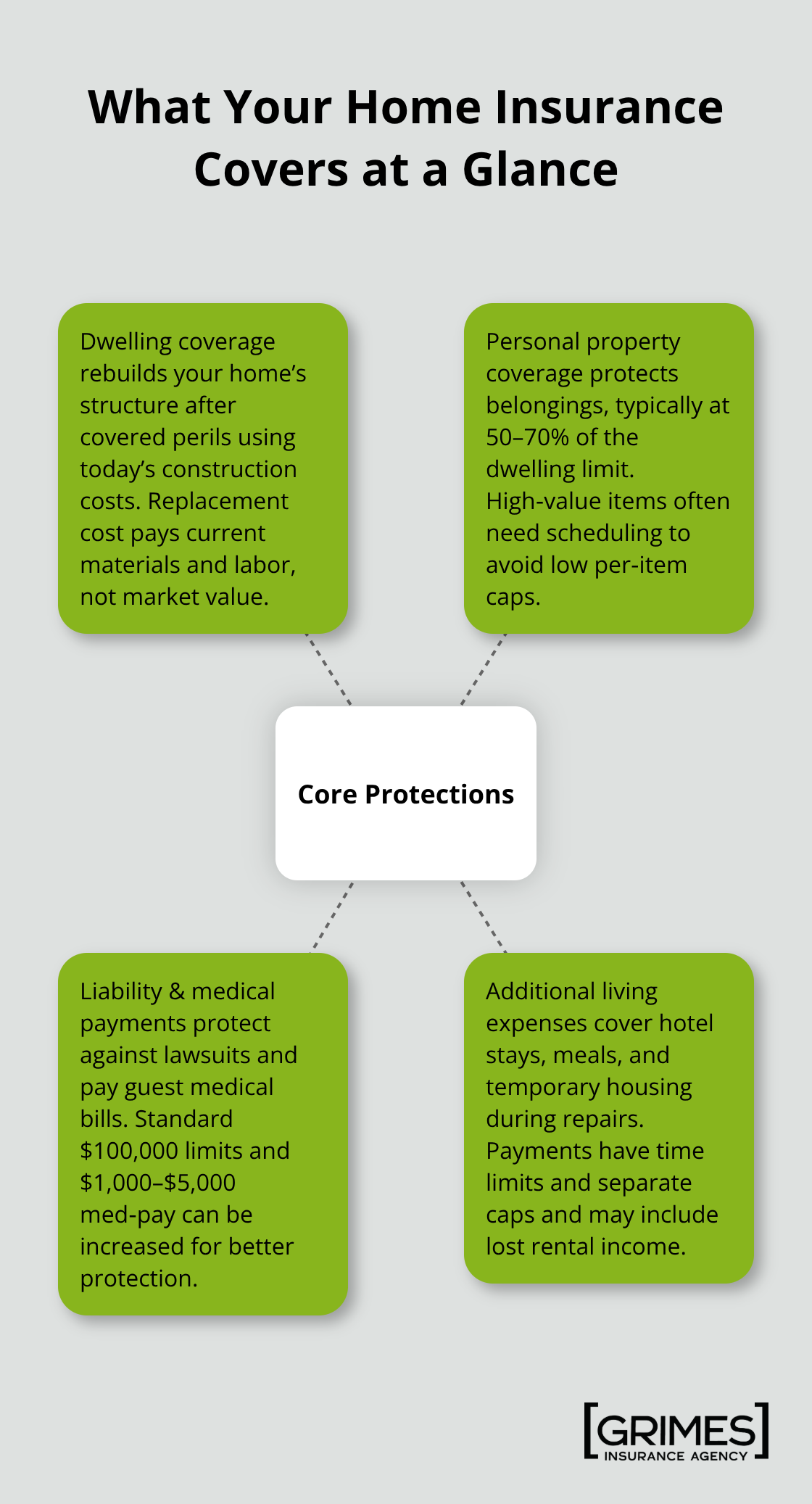

Your homeowners policy protects three core areas: your home’s structure, your personal belongings inside it, and your liability if someone gets injured on your property. Understanding exactly what falls under each category prevents costly surprises when you file a claim. According to the Insurance Information Institute, nearly 98 percent of homeowners insurance claims are for property damage, while liability claims happen less often but tend to be far more expensive. This split matters because it shapes how you should allocate your coverage limits.

Dwelling Coverage Protects Your Structure

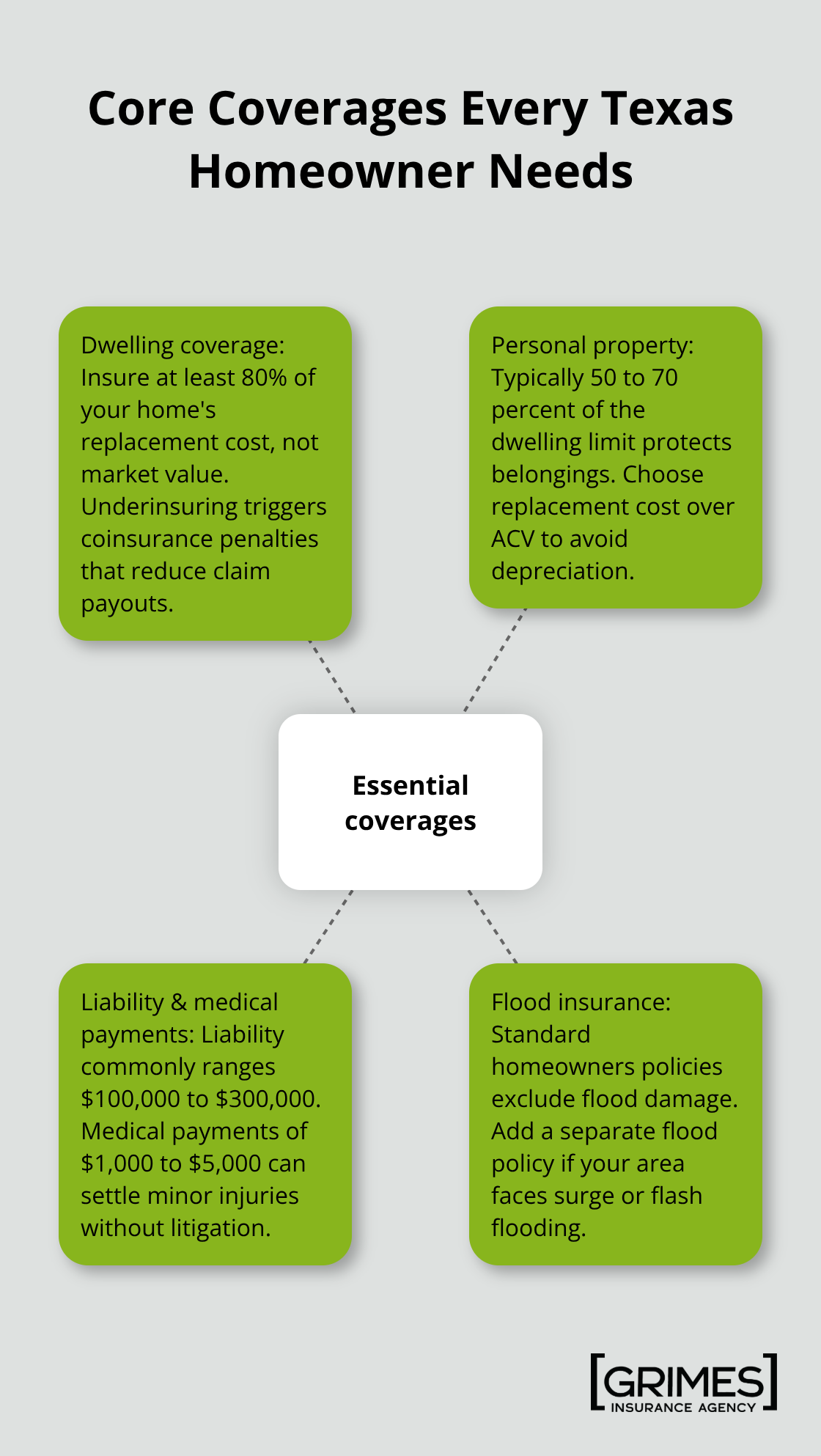

Dwelling coverage pays to repair or rebuild your home after covered disasters like fire, wind, hail, or theft. Wind and hail claims alone represent about 40.7 percent of all homeowners claims, making this protection essential. However, this coverage does not include floods, earthquakes, or damage from neglect and poor maintenance. If your roof has leaked slowly for months and water damages your ceiling, that claim gets denied because it stems from lack of maintenance, not a sudden accident. Your policy covers the structure itself-the walls, roof, foundation, built-in appliances, and permanently attached items. When setting your dwelling limit, try to cover the full replacement cost to rebuild your home as it currently stands, not the market value. A home worth $400,000 might cost $500,000 to rebuild due to labor and material costs, so underestimating this figure leaves you exposed.

Personal Property Coverage Has Real Limits

Personal property coverage typically equals 50 to 70 percent of your dwelling coverage amount. If your home is insured for $500,000, your belongings might only be covered up to $350,000. That coverage extends worldwide, meaning items you take on vacation receive protection unless you explicitly opt out. However, expensive items face strict dollar limits. Jewelry, furs, silverware, and collectibles usually max out at $500 to $2,500 per item depending on your policy. If you own a diamond ring worth $8,000, standard coverage pays only a fraction of that. You need a scheduled personal property endorsement or floater to insure high-value items to their full appraised value. Create a detailed home inventory with photos and receipts of your belongings (this single step streamlines claims and prevents arguments about what you actually owned and its condition).

Liability Coverage Protects Your Assets

Liability protection covers legal defense costs and court-ordered damages if you or family members cause injury or property damage to others. This includes damages caused by your pets. A guest slips on your wet kitchen floor and breaks their arm, or your dog bites a neighbor-your liability coverage handles these situations. Standard policies typically start at around $100,000 in liability limits, but this amount is often inadequate. If you own significant assets, that $100,000 limit disappears quickly in a serious lawsuit. Someone suing for $250,000 in damages leaves you personally responsible for the gap. Setting your liability limit at $300,000 provides better protection for most homeowners, though your actual needs depend on your net worth and circumstances. An umbrella or excess liability policy adds another $1 million or more in coverage beyond your homeowners policy and costs surprisingly little (this extra layer protects your assets when liability claims exceed your base policy limits).

What Gets Left Out

Standard homeowners policies exclude certain perils that require separate coverage. Floods and earthquakes do not appear in your dwelling or personal property protection, which means you must purchase these separately through the National Flood Insurance Program or private carriers. Damage from poor maintenance also falls outside coverage-slow roof leaks, rotting siding, pest infestations, and neglected systems all get denied. This distinction matters because it shifts responsibility to you to maintain your property and protect your coverage eligibility.

Now that you understand what your policy covers, the next step involves determining how much coverage you actually need. Setting limits too low leaves gaps that cost thousands when disaster strikes, while setting them too high wastes money on unnecessary protection.

How to Calculate the Right Coverage Limits

Start with Replacement Cost, Not Market Value

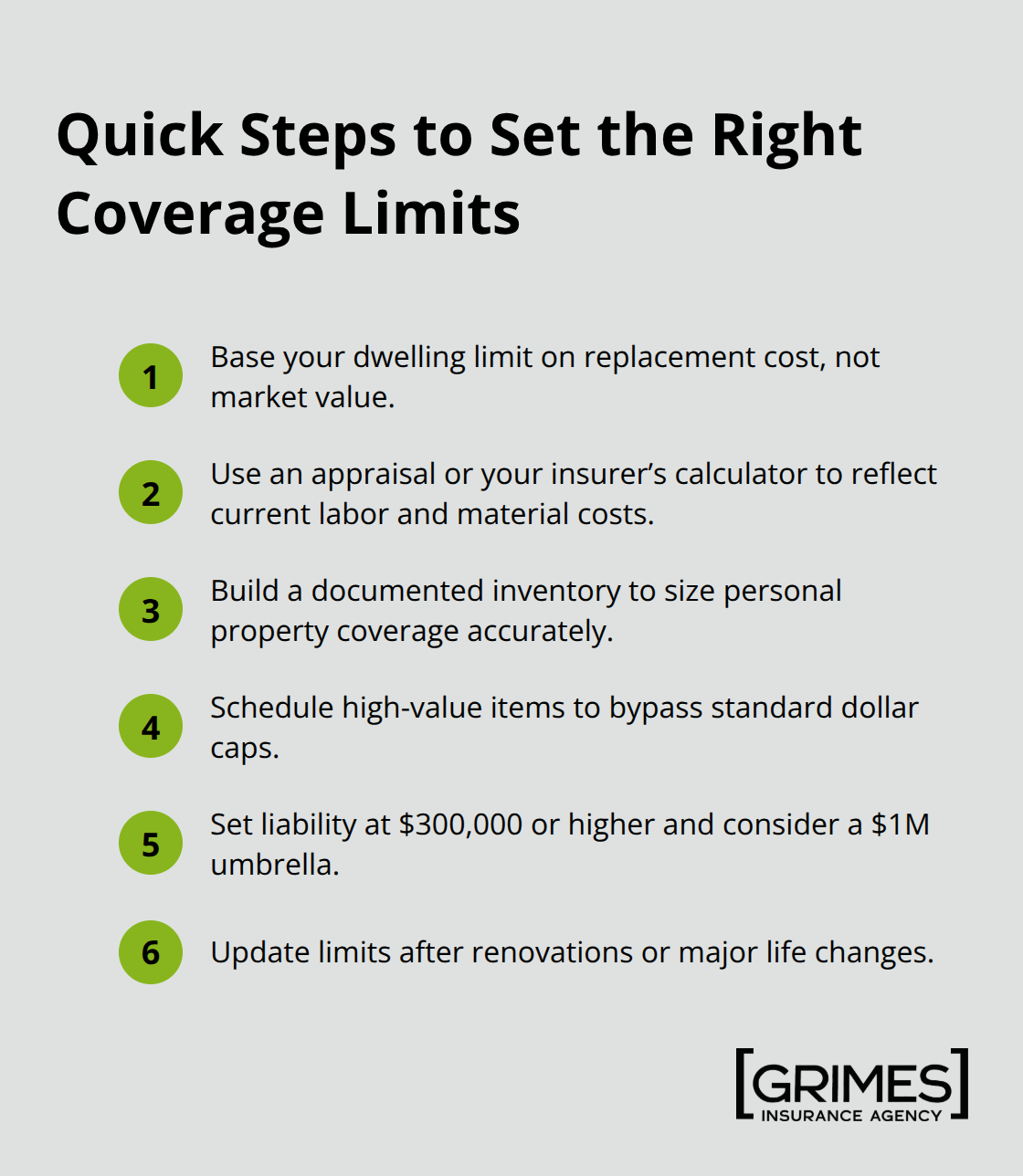

Picking coverage limits feels like guessing in the dark for most homeowners. The truth is that calculating proper limits requires real numbers, not rough estimates. Start with your home’s replacement cost, not its market value. A professional home appraisal or your insurer’s replacement cost calculator gives you an accurate figure that reflects current labor and material expenses in your area. If your home sold for $350,000 but would cost $420,000 to rebuild from scratch, that $420,000 figure is what matters for your dwelling limit. Underestimating by even $50,000 means you absorb that loss yourself if disaster strikes.

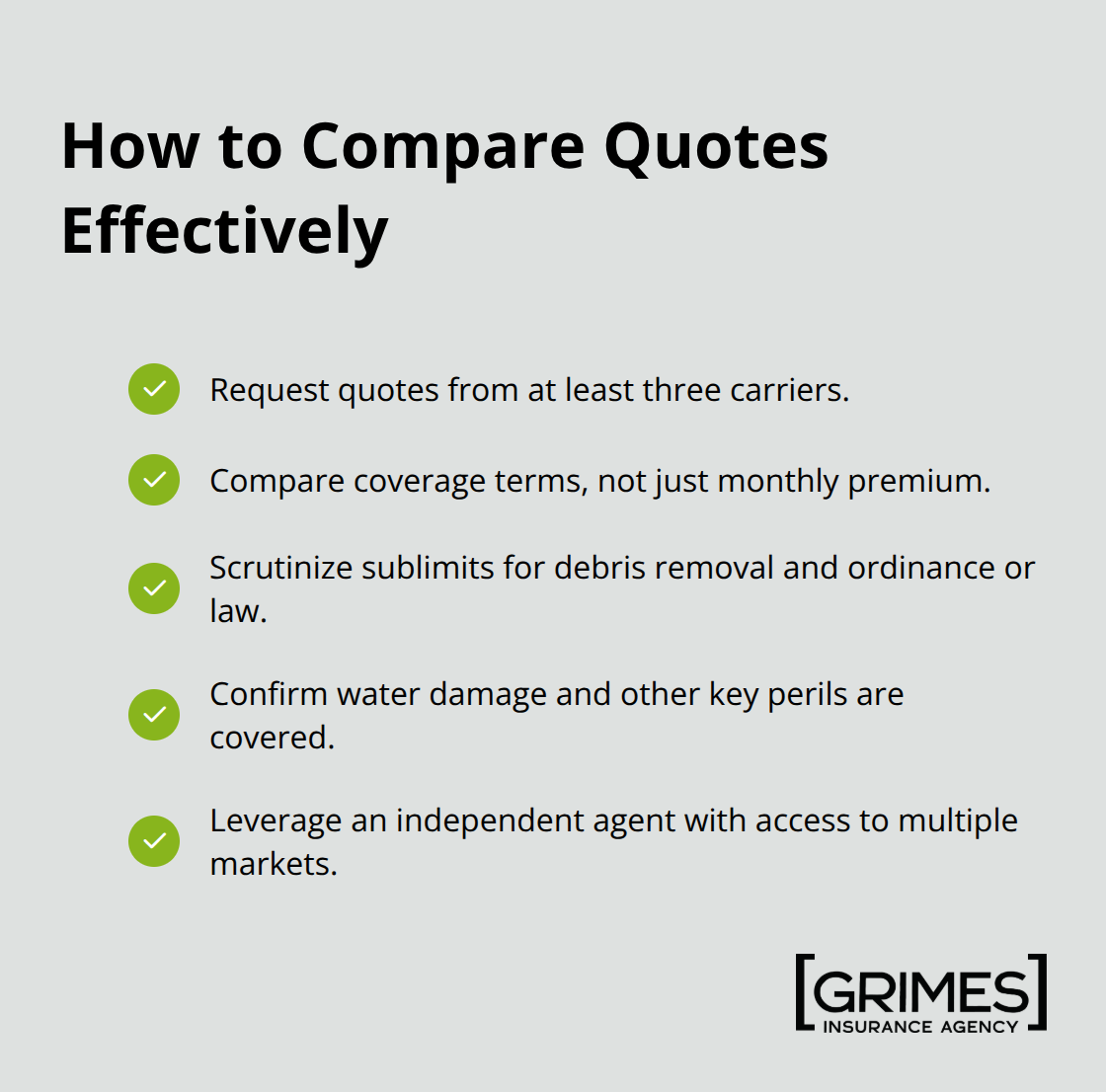

The National Association of Insurance Commissioners recommends obtaining multiple quotes with identical coverage baselines so you can compare apples to apples instead of getting confused by different limit combinations. This approach prevents you from accidentally selecting inadequate protection because you focused on the lowest premium rather than the actual coverage.

Match Personal Property Coverage to Your Inventory

For personal property coverage, your 50 to 70 percent standard limit rarely matches what you actually own. Pull together receipts, photos, and honest estimates of your belongings-furniture, electronics, clothing, tools, and everything else. Most homeowners shock themselves at how high this number climbs. If your inventory totals $200,000 but your policy caps personal property at $280,000 (70 percent of a $400,000 dwelling limit), you’re covered. If your inventory hits $350,000, you’re underinsured and facing a significant shortfall.

Schedule high-value items separately through endorsements; jewelry, art, firearms, and collectibles deserve individual attention and documentation rather than relying on blanket coverage. This step protects you from the dollar limits that standard policies impose on expensive items.

Set Liability Limits Aggressively

Liability limits deserve aggressive thinking. That $100,000 baseline coverage vanishes instantly in serious injury cases. Someone suing for $300,000 after a permanent injury on your property leaves you personally liable for the $200,000 gap. Try setting your homeowners liability at $300,000 minimum, and if you own real estate, have a swimming pool, or have substantial assets, push that to $500,000 or higher.

An umbrella policy adds another $1 million in protection for roughly $150 to $300 annually, making it absurdly cheap insurance against catastrophic liability exposure. The Insurance Information Institute notes that liability claims represent only 1.6 percent of all claims but average $31,690 per claim-far exceeding typical property damage claims. This skewed risk profile means liability deserves more attention than most homeowners give it.

Update Coverage When Your Life Changes

After setting these numbers, review them every two years or whenever you make significant home improvements, buy expensive items, or increase your net worth. A kitchen renovation that adds $75,000 to your home’s replacement cost demands a dwelling limit increase. Purchasing a $15,000 engagement ring requires a scheduled endorsement. Ignoring these updates leaves you underinsured when it matters most.

Once you’ve calculated your coverage limits, the next challenge involves identifying the mistakes that undermine even well-intentioned policies-and how to avoid them.

Common Mistakes Homeowners Make with Their Policies

Underinsuring Your Home Structure

Most homeowners set a dwelling limit and never touch it again. Five years pass, construction costs rise 15 percent, you add a second story, or you simply never revisit the number. The Insurance Information Institute reports that many homeowners carry dwelling coverage below actual replacement cost, meaning they absorb a massive portion of rebuild expenses personally. A home that requires $500,000 to rebuild but carries only $400,000 in coverage leaves you paying $100,000 out of pocket after disaster. This gap grows silently until the moment you file a claim.

The solution requires annual discipline. Review your dwelling limit every year and adjust it whenever your home appreciates, you complete renovations, or local construction costs spike. Your mortgage lender’s appraisal from three years ago means nothing today. Construction inflation compounds quickly, and ignoring it costs far more than the few minutes spent updating your policy.

Failing to Update Coverage After Major Life Changes

Life transforms dramatically-you purchase expensive jewelry, install a pool, add a garage, or your net worth climbs substantially-yet your insurance stays frozen in time. A scheduled personal property endorsement for that $12,000 diamond ring costs $30 to $50 annually but prevents a $2,000 claim limit from destroying your financial security. Failing to add this coverage proves negligent when the fix costs so little.

Similarly, many homeowners skip umbrella policies despite their absurdly low cost. An additional $1 million in liability protection runs roughly $150 to $300 per year, yet most homeowners earning six figures carry only the base $100,000 liability limit. When someone sues for $250,000 after a serious injury on your property, that decision becomes catastrophically expensive. The gap between what your homeowners policy covers and what a lawsuit demands falls directly on your shoulders.

Missing Discounts and Bundling Savings

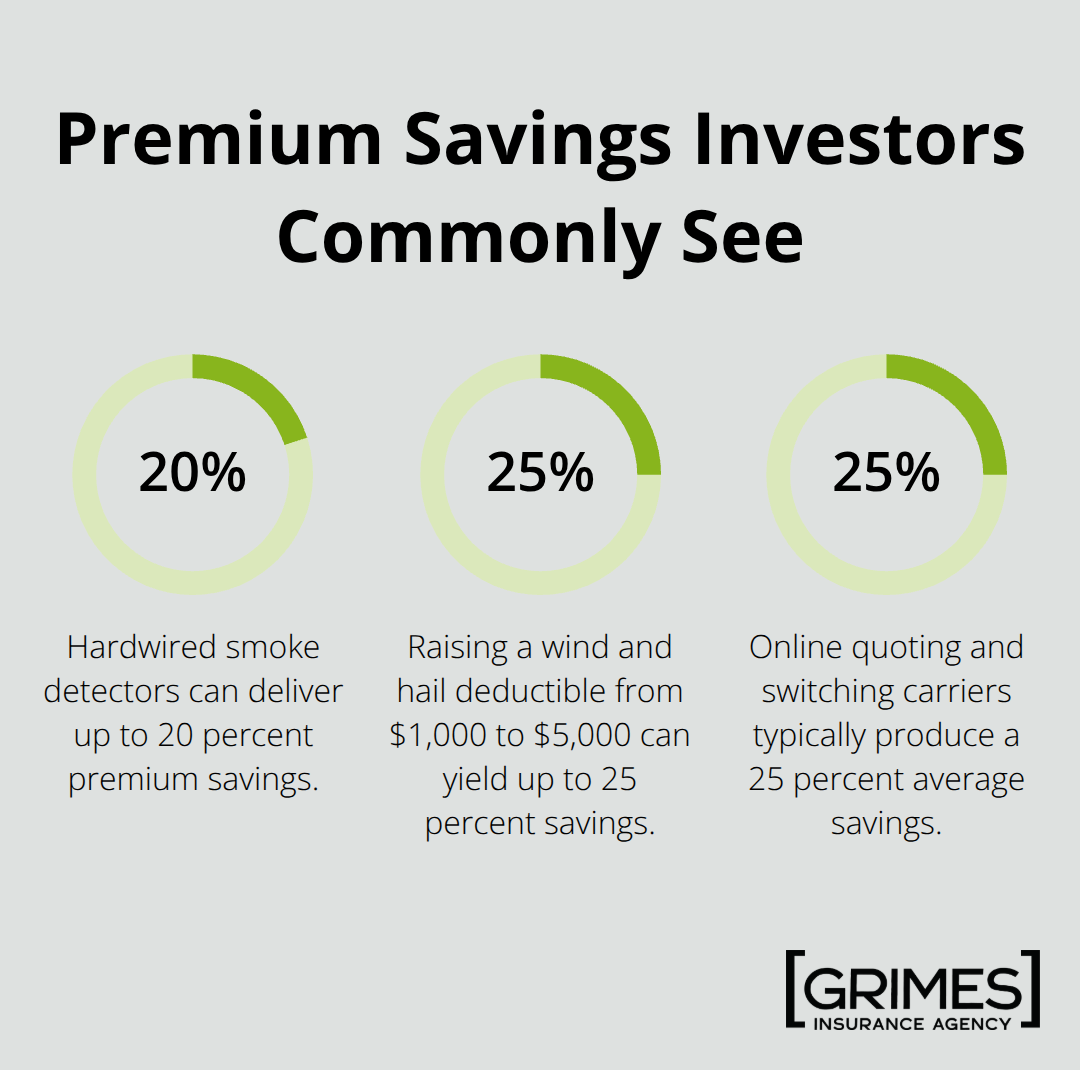

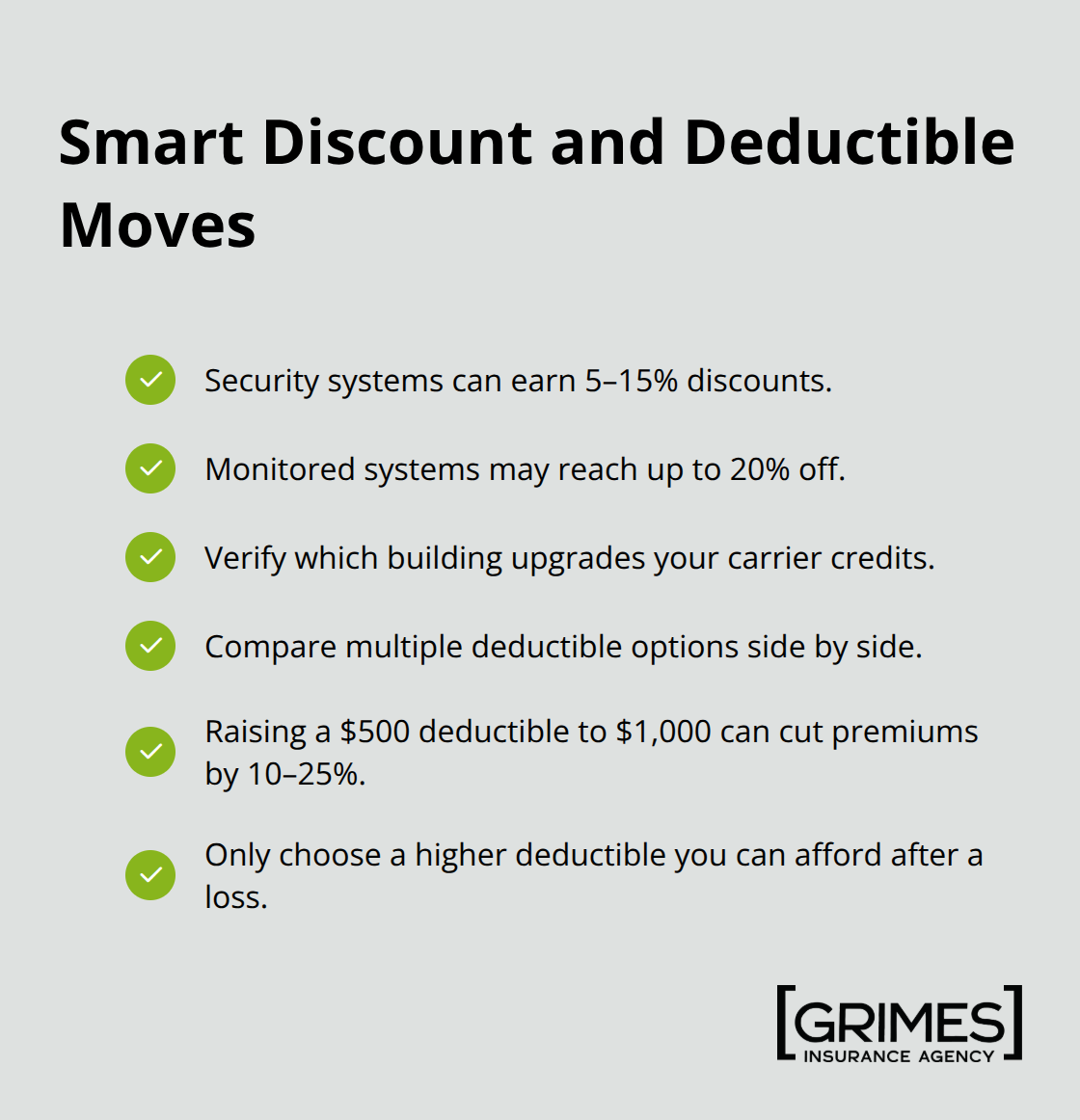

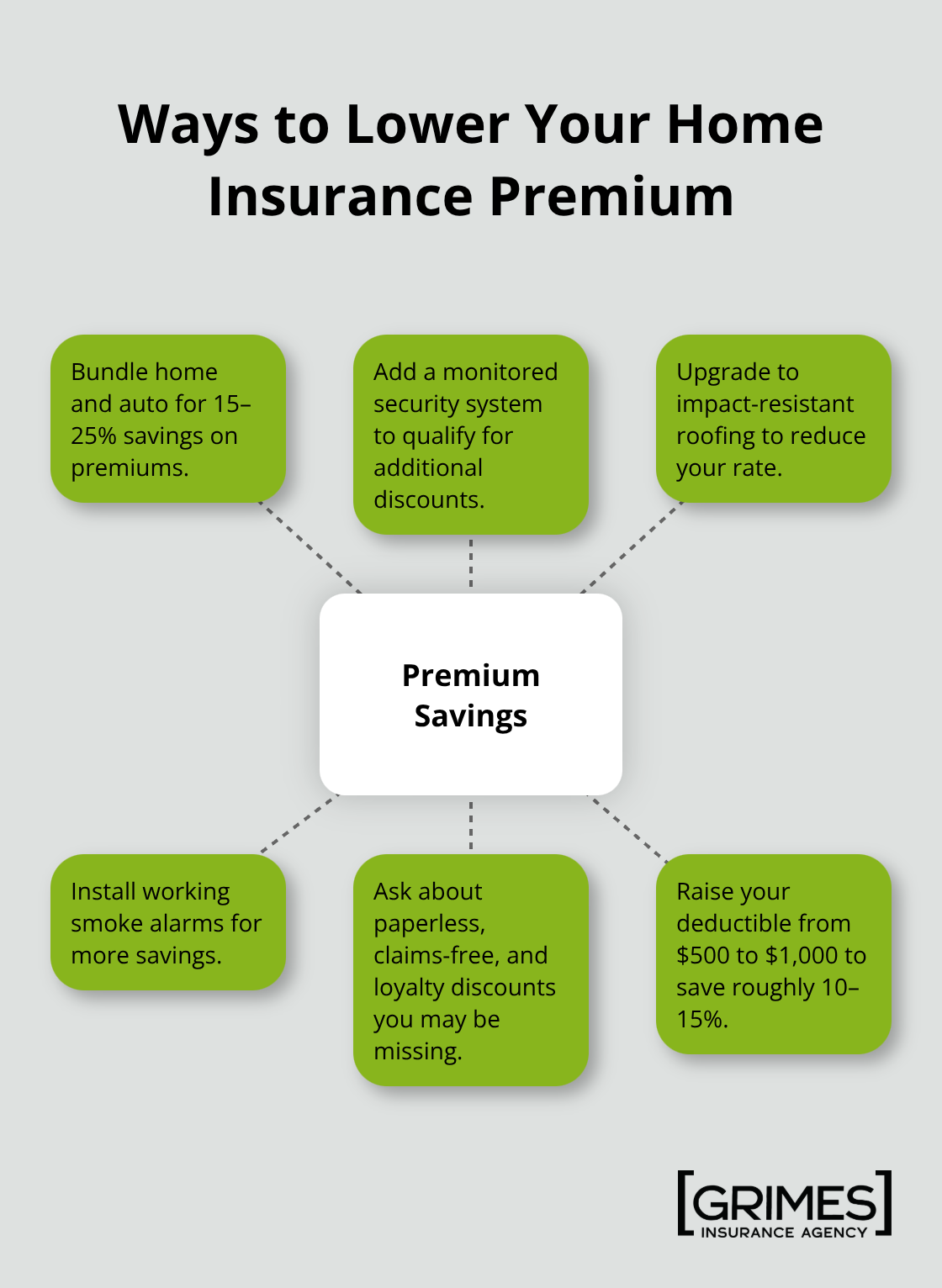

Bundling home and auto insurance often yields 15 to 25 percent savings on premiums. Adding a security system, upgrading to impact-resistant roofing, or installing working smoke alarms can each reduce your rate further. Yet homeowners routinely carry standalone policies and miss these savings entirely. Some insurers offer paperless billing discounts, claims-free discounts, or loyalty discounts that disappear if you never ask.

Your deductible choice also affects your bottom line dramatically. Jumping from $500 to $1,000 can lower your premium 10 to 15 percent, money you keep unless you file a claim. Set that deductible at a level you can genuinely afford out of pocket. This approach prevents financial strain while capturing premium savings that compound year after year.

Final Thoughts

Home insurance basics come down to three critical decisions: covering your structure at replacement cost, protecting your belongings at their true value, and setting liability limits high enough to shield your assets. The data shows that nearly 98 percent of claims involve property damage, yet many homeowners carry dwelling limits below what they actually need to rebuild. Liability claims happen less frequently but average $31,690 per incident, so that $100,000 limit most policies start with disappears instantly in serious lawsuits.

Pull your current policy today and verify three things: your dwelling limit matches your home’s actual replacement cost, your personal belongings coverage reflects what you truly own, and your liability limit sits at $300,000 minimum. Schedule endorsements for high-value items like jewelry or art, calculate whether bundling home and auto insurance saves money, and confirm you’re capturing every available discount. Set your deductible at an amount you can afford out of pocket without financial strain.

We at Grimes Insurance Agency understand that navigating home insurance feels overwhelming, which is why our team accesses multiple carriers to shop your policy against dozens of options and match your protection needs with competitive rates. Whether you’re buying your first home, updating coverage after renovations, or simply want a second opinion on your current policy, contact Grimes Insurance Agency to review your coverage and ensure your home and assets receive the protection they deserve.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

We often come across advertisements urging us to bundle our insurance policies together, promising savings and convenience. But what lies behind this recommendation, and is it truly a better option for your insurance needs? Let’s dive into the benefits of bundling and explore whether it’s the right choice for you.

We often come across advertisements urging us to bundle our insurance policies together, promising savings and convenience. But what lies behind this recommendation, and is it truly a better option for your insurance needs? Let’s dive into the benefits of bundling and explore whether it’s the right choice for you.

As summer approaches, many of you are eagerly preparing to take your boats out on the water or perhaps even considering purchasing a new one. When it comes to insuring your boat, it’s important to prioritize having the right coverage rather than simply opting for the least expensive policy. While boating season offers incredible fun and excitement, being on the water also comes with certain risks. As you shop for boat insurance, make sure your policy includes three specific coverages, which are sometimes optional but highly recommended:

As summer approaches, many of you are eagerly preparing to take your boats out on the water or perhaps even considering purchasing a new one. When it comes to insuring your boat, it’s important to prioritize having the right coverage rather than simply opting for the least expensive policy. While boating season offers incredible fun and excitement, being on the water also comes with certain risks. As you shop for boat insurance, make sure your policy includes three specific coverages, which are sometimes optional but highly recommended: