Understanding Why Auto Insurance Rates Go Up

The auto insurance industry has experienced a consistent increase in premiums, which may have caught the attention of many individuals. While our agency represents several top insurance companies in the country and can provide quotes from multiple sources, it is important to understand the reasons behind this upward trend in premiums.

The auto insurance industry has experienced a consistent increase in premiums, which may have caught the attention of many individuals. While our agency represents several top insurance companies in the country and can provide quotes from multiple sources, it is important to understand the reasons behind this upward trend in premiums.

Several factors contribute to the rising premiums:

- Expensive Repairs: The market is flooded with new cars that are costly to repair. Advanced technology and sophisticated features in modern vehicles make replacement parts more expensive than ever before.

- Technological Advances: The intricate technology integrated into today’s vehicles comes with a higher price tag for replacement. Repairing or replacing these advanced systems can significantly impact insurance costs.

- Distracted Driving: Distraction behind the wheel has become a major concern. Approximately one out of every four car crashes involves cell phone use. Such accidents lead to increased claims and higher premiums.

- Rising Medical Costs: The complexity of the health insurance industry has caused medical payments associated with car accidents to skyrocket. The increasing cost of healthcare translates into higher insurance premiums.

- Growing Claims Severity: The severity of claims, i.e., the amount paid out, is on the rise. This can be attributed to a combination of factors such as expensive repairs, medical costs, and higher compensation expectations.

- Escalating Labor Costs: The cost of labor has increased significantly over time. When repairs are necessary, the expenses incurred for skilled labor contribute to higher insurance premiums.

- Parts Delays: Manufacturing and labor shortages can cause delays in obtaining necessary parts for repairs. Such delays can prolong the time a vehicle spends in the repair shop, driving up costs and subsequently impacting premiums.

While these factors are beyond an individual’s control, there are measures you can take to manage your insurance costs effectively:

- Review Your Coverage: Regularly assess your insurance coverage to ensure it aligns with your current needs and circumstances. Adjustments can be made to optimize your coverage and potentially lower your premiums.

- Explore Discounts: Check for any available discounts with your current insurance carrier. You may be eligible for various discounts that can help reduce your premium.

- Bundle Your Coverage: Consider bundling your insurance policies, such as home, auto, and specialty insurance, with a single carrier. Bundling often results in discounts, ultimately saving you money.

If you have specific inquiries about your auto insurance coverage, we strongly encourage you to reach out to our agency. As an independent insurance agent, we can thoroughly review your coverage and determine whether your current carrier remains the best option for your situation. We are here to assist you in obtaining the most suitable coverage at competitive rates.

What Is Rental Property Insurance?

What Is Rental Property Insurance?

What Is Insurance Bundling?

What Is Insurance Bundling? Our children hold a special place in our hearts, and as parents, their well-being and safety become our utmost priority. However, it’s important to recognize that as they grow and explore the world, their actions can have implications that extend beyond their immediate surroundings.

Our children hold a special place in our hearts, and as parents, their well-being and safety become our utmost priority. However, it’s important to recognize that as they grow and explore the world, their actions can have implications that extend beyond their immediate surroundings. Are Solar Panels Covered by Home Insurance?

Are Solar Panels Covered by Home Insurance?

When it comes to finding the right insurance policy, working with a local insurance agent can offer numerous benefits tailored to your specific needs. While instant quotes may seem enticing in our fast-paced society, they often fall short in providing the best rates and coverage. Here are six ways in which a local insurance agent can assist you:

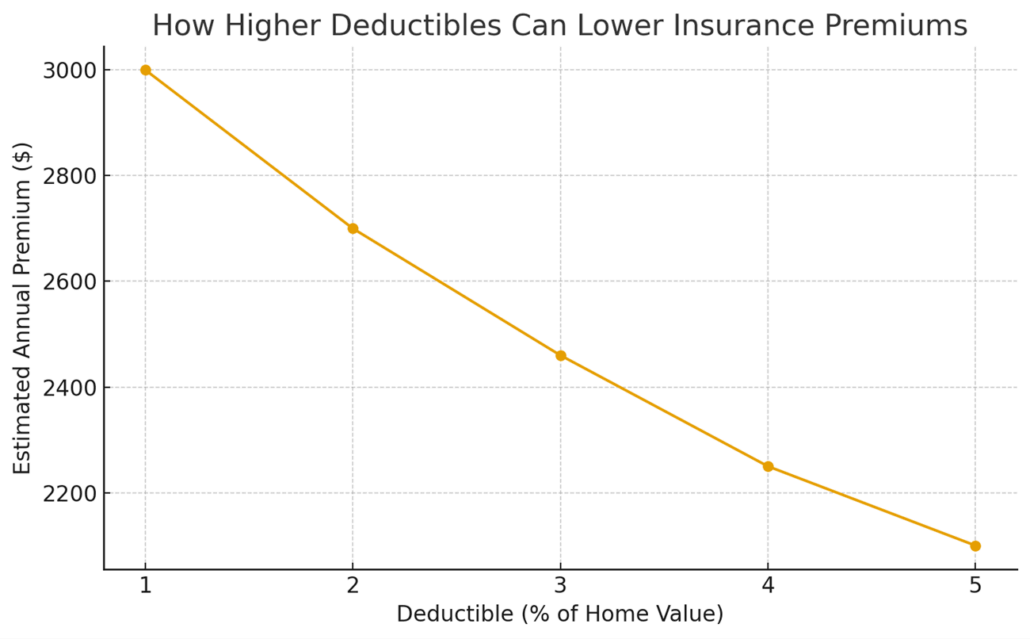

When it comes to finding the right insurance policy, working with a local insurance agent can offer numerous benefits tailored to your specific needs. While instant quotes may seem enticing in our fast-paced society, they often fall short in providing the best rates and coverage. Here are six ways in which a local insurance agent can assist you: re you looking for ways to lower your insurance premiums without sacrificing protection? You’re not alone. In today’s world, the cost of insurance—whether it’s home, auto, commercial, or health insurance—has gone up dramatically. Families and business owners are asking the same question: “How can I save money on my insurance?”

re you looking for ways to lower your insurance premiums without sacrificing protection? You’re not alone. In today’s world, the cost of insurance—whether it’s home, auto, commercial, or health insurance—has gone up dramatically. Families and business owners are asking the same question: “How can I save money on my insurance?”

Planning a wedding or a special event requires a tremendous amount of time, effort, and attention to detail. From creating the guest list to selecting vendors and deciding on the perfect menu, there are countless considerations involved in making your dream wedding or event a reality.

Planning a wedding or a special event requires a tremendous amount of time, effort, and attention to detail. From creating the guest list to selecting vendors and deciding on the perfect menu, there are countless considerations involved in making your dream wedding or event a reality.