Exploring the Top Home Insurance Providers in Lubbock: What You Need to Know

Finding the right home insurance in Lubbock means understanding your options. We at Grimes Insurance Agency know that the top home insurance providers in Lubbock each offer different coverage levels and pricing structures.

This guide walks you through what matters most when comparing policies. You’ll learn how to evaluate coverage types, assess your home’s specific needs, and make a decision that protects your property without overpaying.

Top Home Insurance Providers in Lubbock

Lubbock homeowners face higher-than-average premiums compared to the rest of Texas. For a $300,000 dwelling, you’ll pay roughly $4,121 per year, or about $343 per month, according to rate data from Bankrate using Quadrant Information Services. This is about 6% above the Texas average of $3,899 annually, driven by the area’s exposure to hail, tornadoes, and wind. Understanding which carriers operate in Lubbock and what they actually charge matters far more than generic national rankings.

State Farm, Farmers, and Chubb Lead the Lubbock Market

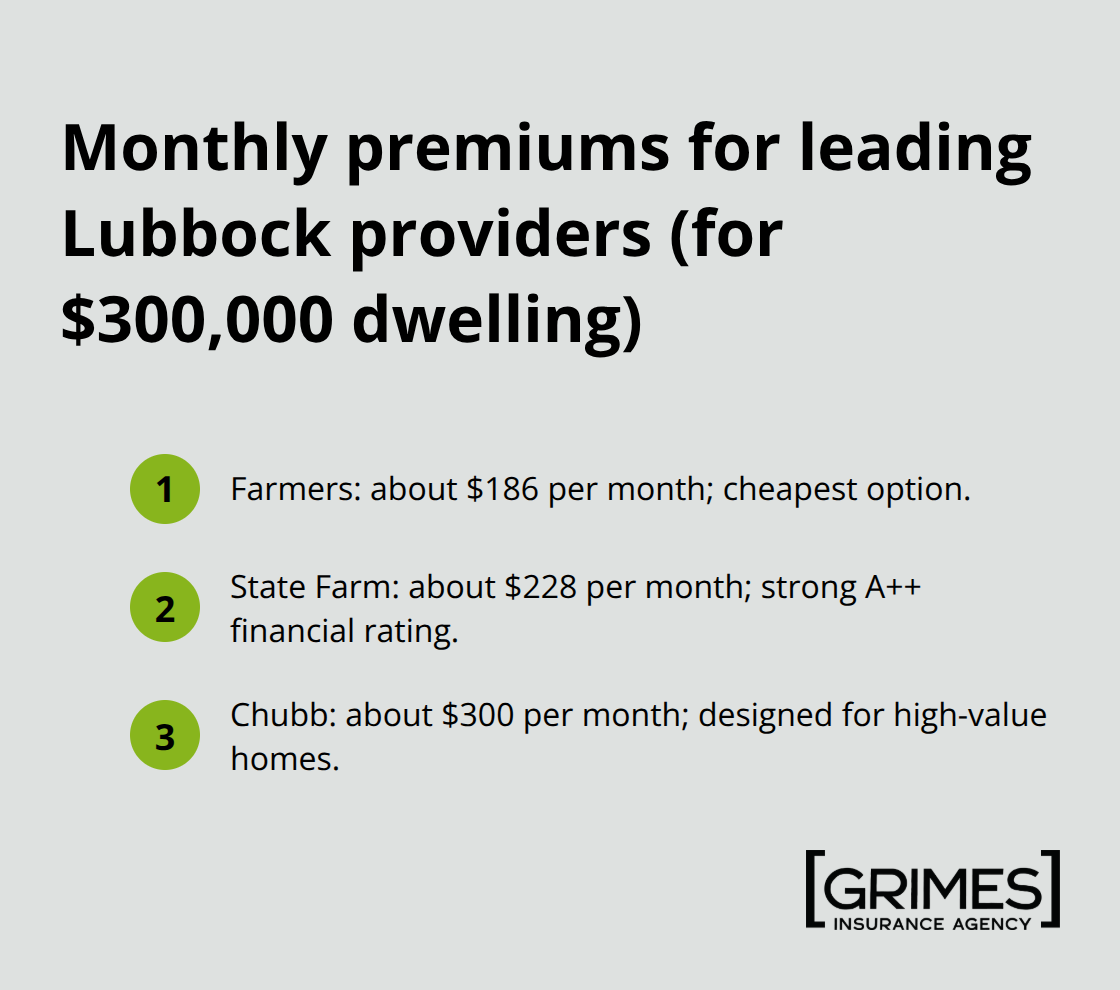

State Farm, Farmers, and Chubb dominate the Lubbock market, each with distinct pricing and coverage strengths. State Farm charges roughly $228 per month for a $300,000 dwelling in Lubbock and carries an AM Best A++ financial stability rating, making it solid for homeowners who prioritize reliability and local agent access. Farmers offers the cheapest option at around $186 per month for the same coverage, though you’ll need to verify their wind and hail deductible structure since those often sit separately in storm-prone areas like Lubbock.

Chubb targets high-value homes with extended replacement cost and private flood insurance options, running about $300 per month for $300,000 coverage but offering superior service ratings through J.D. Power.

Other National Carriers Worth Considering

According to Insurify’s analysis of 180+ insurers, several other carriers serve Lubbock effectively. USAA serves military members with replacement-cost coverage and A++ ratings, while Nationwide emphasizes bundling discounts and broad endorsements if you combine home and auto policies. Armed Forces offers the absolute lowest premiums in Texas at around $2,240 annually for a $300,000 dwelling, though availability and coverage options in Lubbock vary. These carriers represent practical starting points for Lubbock residents seeking competitive quotes tailored to the region’s specific weather risks.

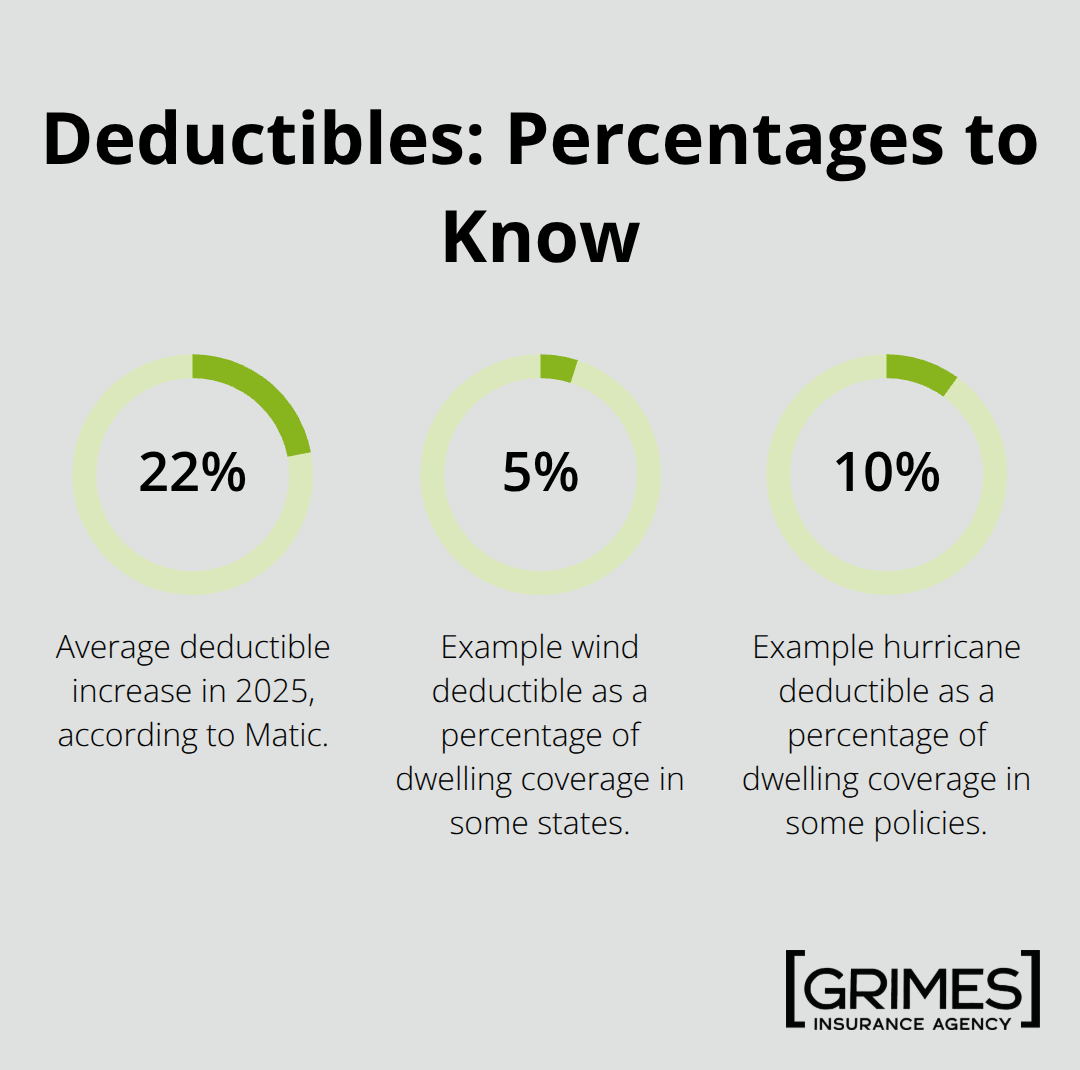

Wind and Hail Deductibles Create Hidden Costs

Standard homeowners policies in Lubbock have a critical gap that catches people off guard. Wind and hail deductibles operate separately from your main deductible, sometimes running 2% to 5% of your dwelling’s value, meaning you could face a $6,000 to $15,000 deductible for a hail claim on a $300,000 home. Bankrate’s analysis of common Texas home insurance problems identified these separate deductibles as a frequent source of claim disputes and inadequate payouts.

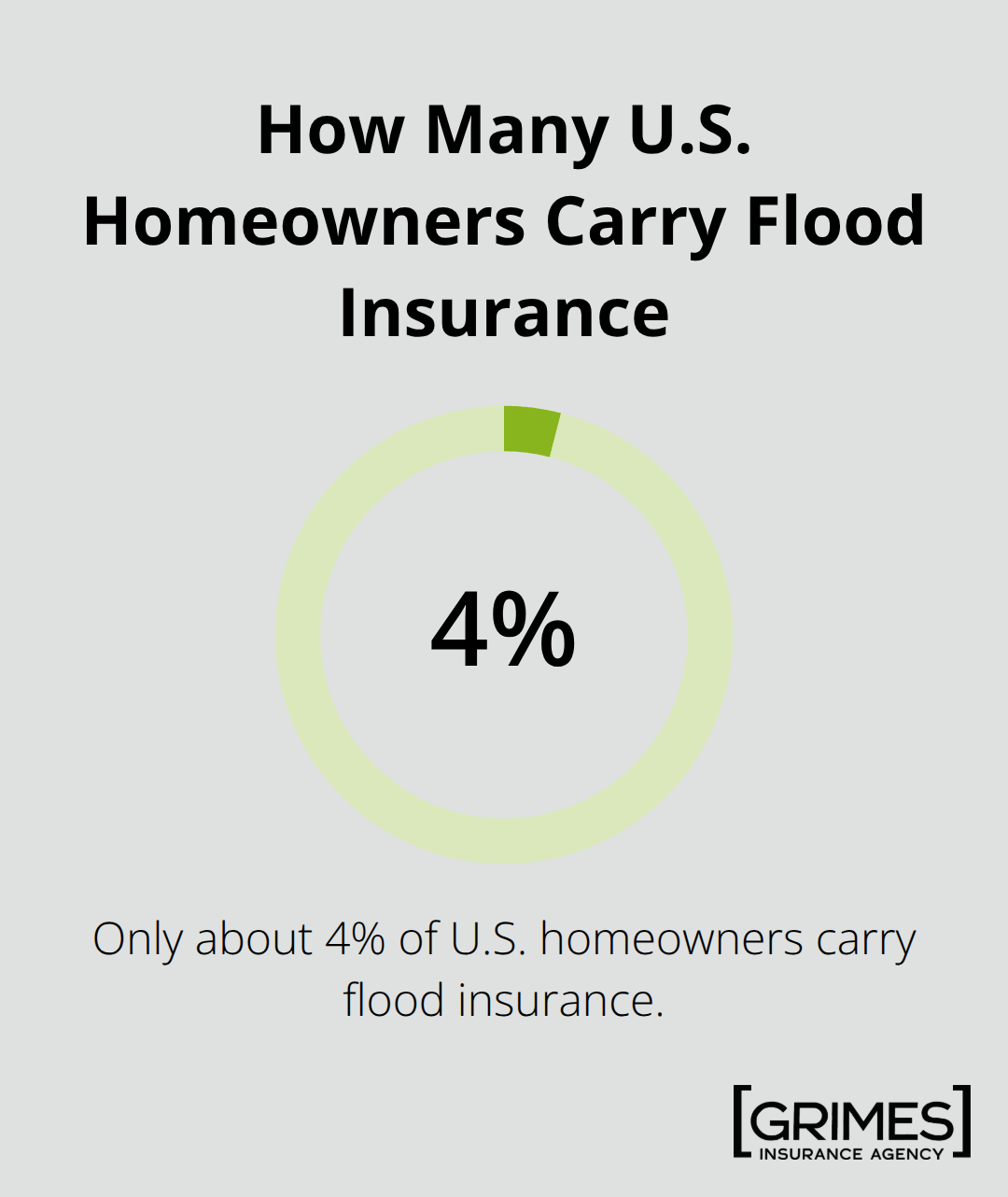

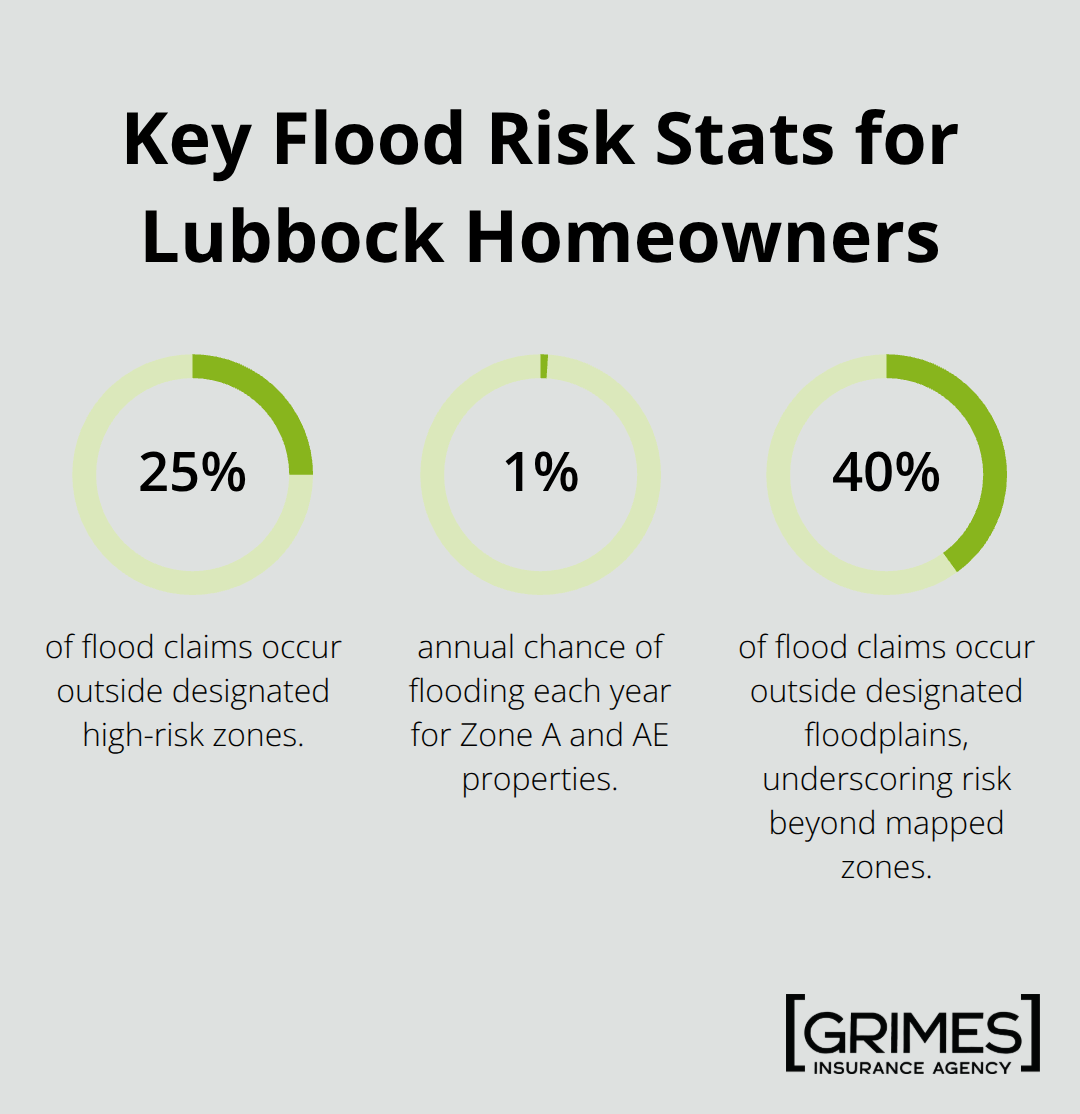

Flood Coverage Requires a Separate Policy

Flood coverage is almost never included in a standard HO-3 policy, and you’ll need standalone flood insurance through the National Flood Insurance Program or private carriers. A typical policy includes 20% to 30% of your dwelling limit for additional living expenses if you’re displaced by a covered loss, but that can fall short in Lubbock’s high rebuild-cost environment. When comparing quotes, explicitly ask each carrier about wind and hail deductibles, flood exclusions, and how replacement cost applies to older structures, since many homes in Lubbock were built in the 1980s and earlier. These questions reveal which carriers actually understand Lubbock’s unique risks and which ones treat your home like any other property in a low-risk market.

What Matters Most When Selecting a Home Insurance Provider

Claims Processing Speed Determines Real-World Value

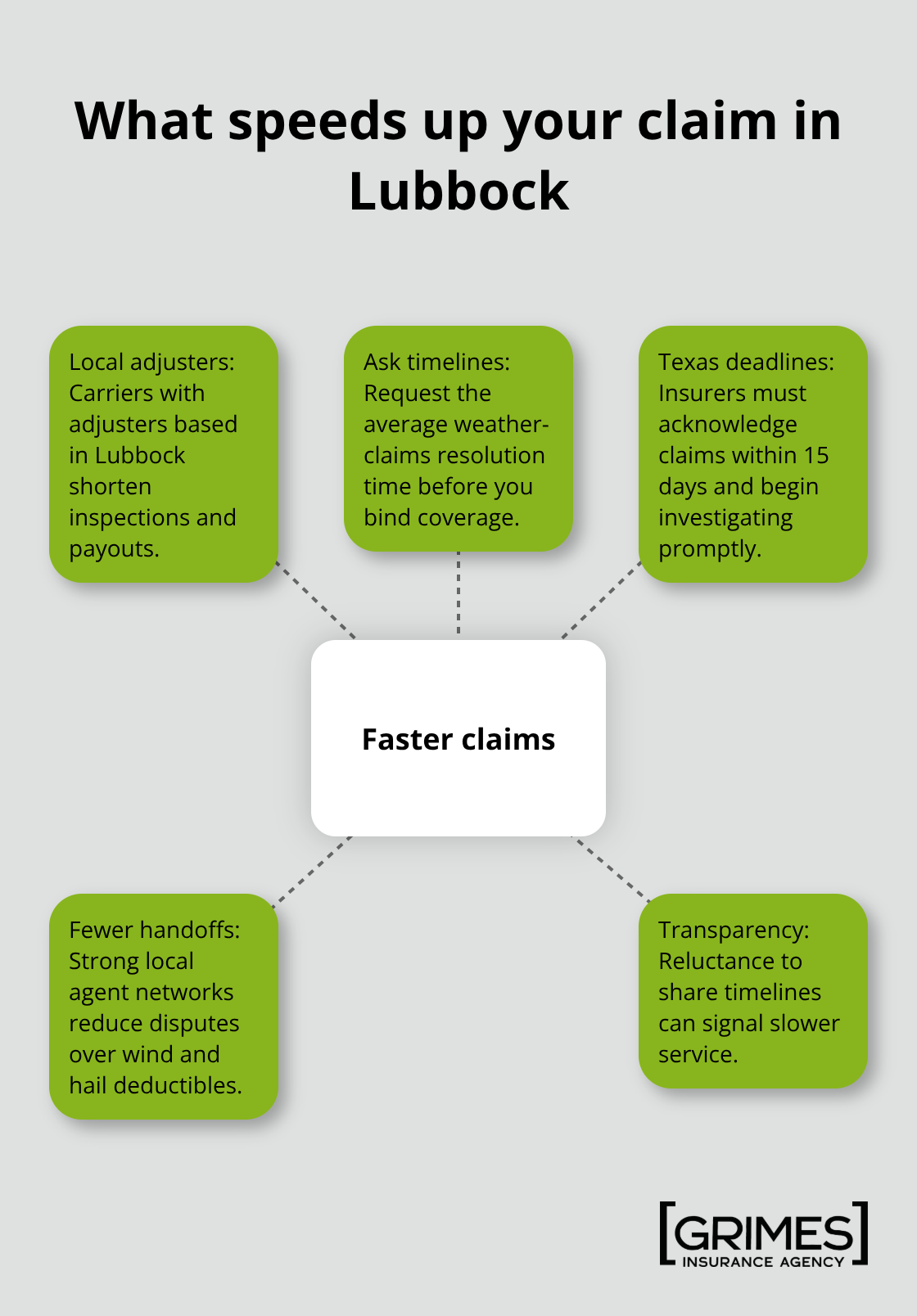

Claims processing speed separates adequate insurers from exceptional ones, and this matters more in Lubbock than anywhere else. When hail or wind damage strikes your $300,000 home, you don’t want to wait weeks for an adjuster or months for a payout. State Farm’s extensive local agent network in Lubbock means faster claim routing and face-to-face communication, which according to J.D. Power satisfaction data translates to fewer disputes over wind and hail deductible calculations. Farmers, while cheaper at $186 per month for a $300,000 dwelling, operates through fewer local touchpoints, potentially slowing claims in urgent situations. Chubb’s private flood insurance option and extended replacement cost coverage appeal to homeowners with high-value properties, but their claims process works through specialized adjusters rather than neighborhood-based agents.

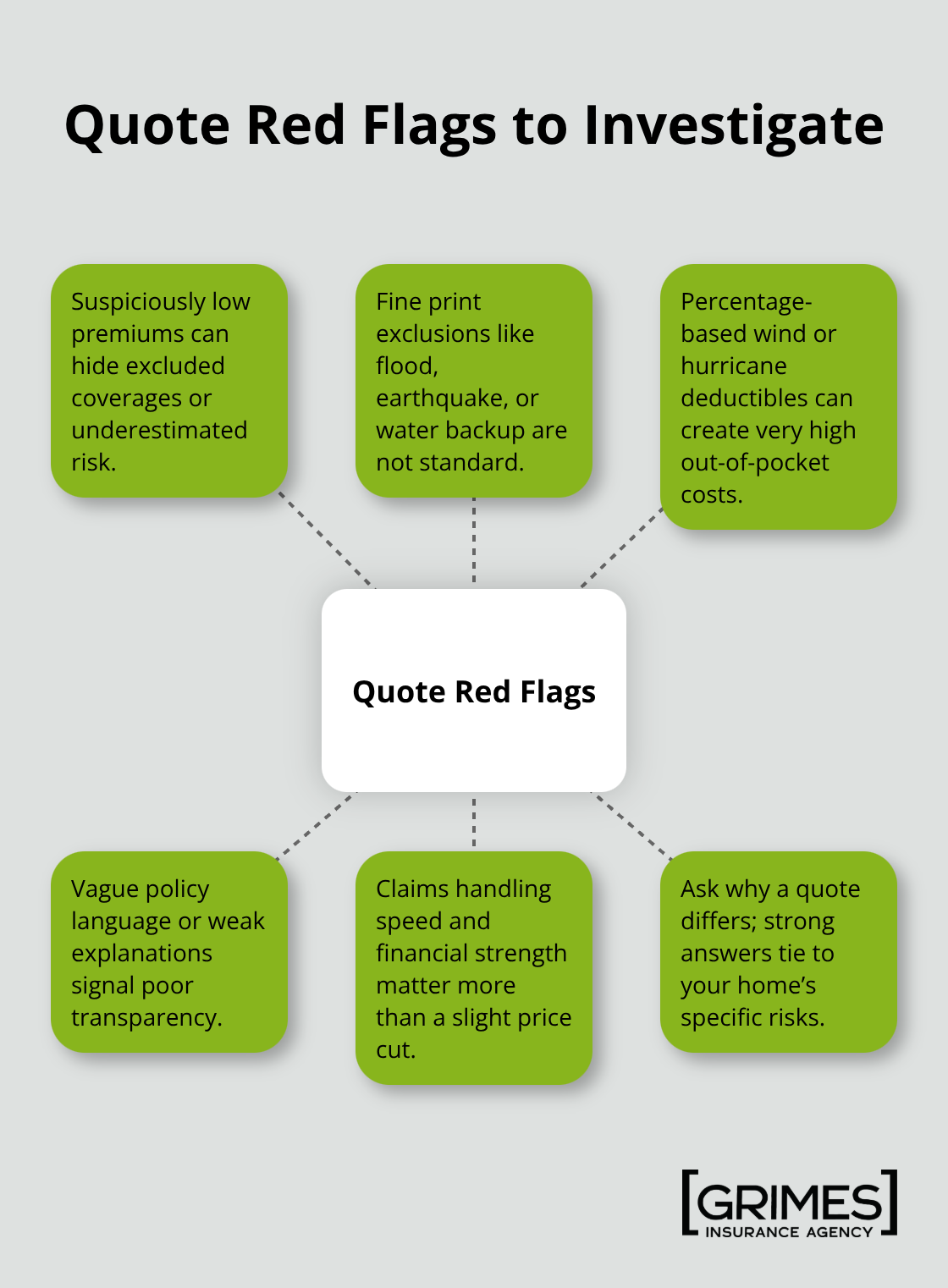

Verify whether your carrier maintains local claims adjusters in Lubbock before you commit to a policy. Contact the company directly and ask their average claim resolution time for weather-related losses, not general statistics. Under Texas law, claims processing speed requires insurers to acknowledge your claim within 15 days of notification and begin investigating immediately. Most carriers won’t volunteer additional details about their timeline, which itself tells you something about their transparency.

Financial Strength Ratings Protect You During Regional Disasters

Financial strength ratings matter more than premium price when disaster hits. AM Best A++ ratings from State Farm and USAA guarantee they’ll pay claims even during catastrophic regional losses, whereas lower-rated carriers sometimes delay or deny payouts after major events. Lubbock’s tornado history and hail exposure mean you need an insurer with rock-solid reserves. An independent agency accesses multiple carriers simultaneously and can compare not just monthly costs but also each carrier’s specific claims procedures, local representation, and financial stability ratings in a single conversation. This approach eliminates the legwork of calling five insurers separately and asking identical questions about wind deductible structures, flood exclusions, and replacement cost definitions.

You’ll pay roughly $228 per month with State Farm or $186 with Farmers, but the difference in claims experience could mean $5,000 or more when you actually need the coverage. The cheapest option rarely delivers the fastest payout when your roof sustains hail damage or wind tears off your siding.

Local Market Knowledge Reveals Hidden Coverage Gaps

Carriers that understand Lubbock’s specific weather patterns ask better questions during the quote process. They probe whether your roof has impact-resistant shingles, whether your home sits in a flood-prone area, and whether you’ve upgraded your electrical system-details that directly affect your actual risk and your actual premium. National carriers that treat Lubbock like any other Texas city often miss these nuances, leaving you underinsured or overpaying for coverage you don’t need. An independent agency with deep roots in West Texas knows which carriers offer the best wind and hail deductible structures for Lubbock properties and which ones impose unnecessary restrictions on older homes built in the 1980s.

This local expertise becomes invaluable when you file a claim and discover that your carrier interprets replacement cost differently than you do, or that your wind deductible applies to damage you thought was covered under your standard deductible. The agent who understands Lubbock’s construction standards and weather history can advocate for you during disputes and steer you toward carriers known for fair claim settlements in your area.

Choosing Your Home Insurance Without Overpaying

Calculate Your Home’s True Replacement Cost

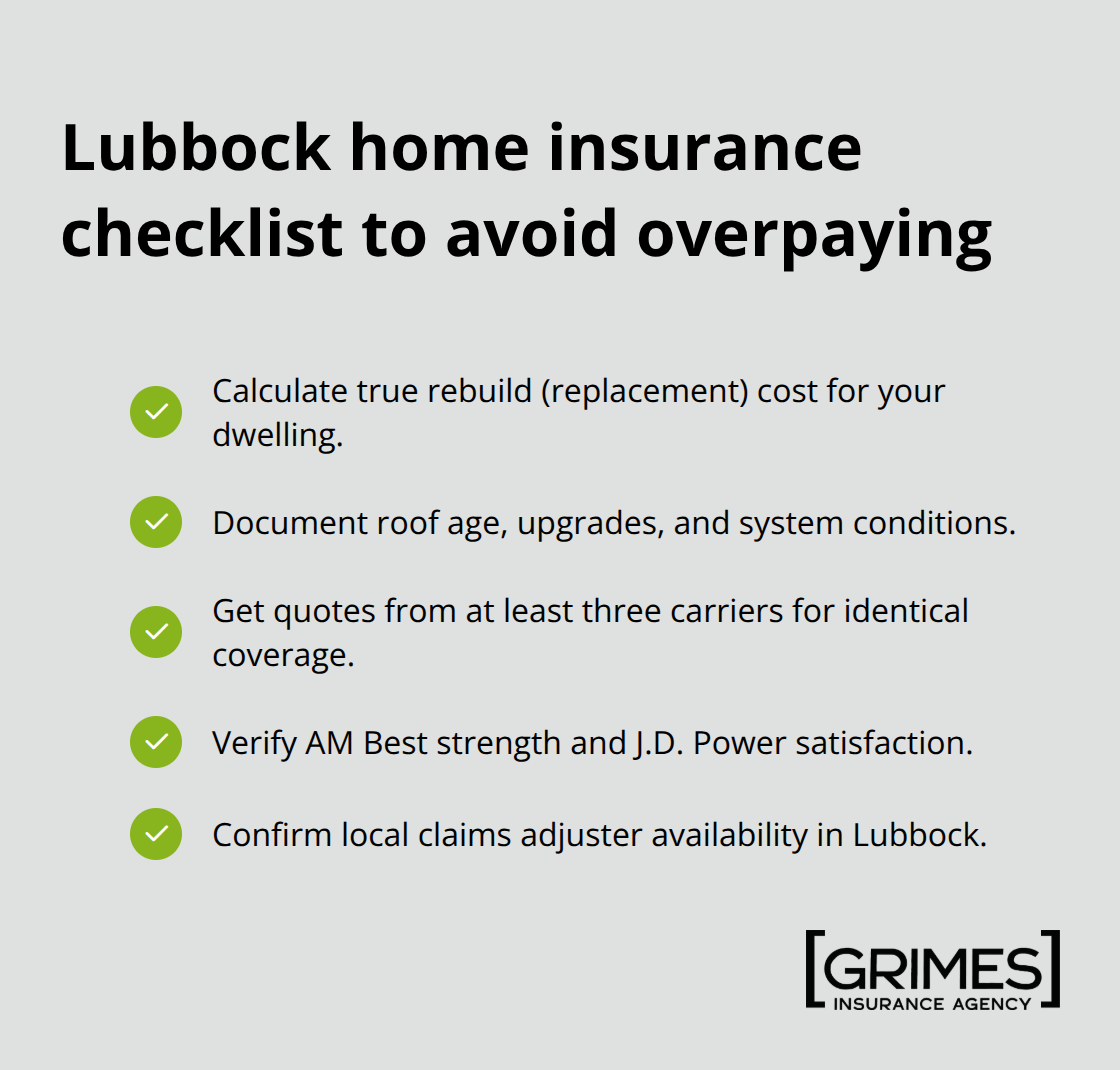

Start with your home’s actual replacement cost, not its market value. A $300,000 home in Lubbock might cost $350,000 to rebuild after a total loss because of elevated labor and material costs in West Texas. Contact local contractors and ask what they’d charge to rebuild your specific home from the ground up, then use that figure as your dwelling coverage amount. This step prevents you from underinsuring your property and facing a shortfall when you file a claim.

Identify Your Home’s Specific Vulnerabilities

Document your home’s age, roof condition, electrical system type, and whether you’ve upgraded plumbing or HVAC systems, since carriers ask about these details during quotes and honest answers prevent claim denials later. Homes built before 1990 in Lubbock often lack impact-resistant shingles, making them targets for higher wind and hail deductibles. If your roof is older than 15 years, carriers will either charge more or impose steeper deductibles.

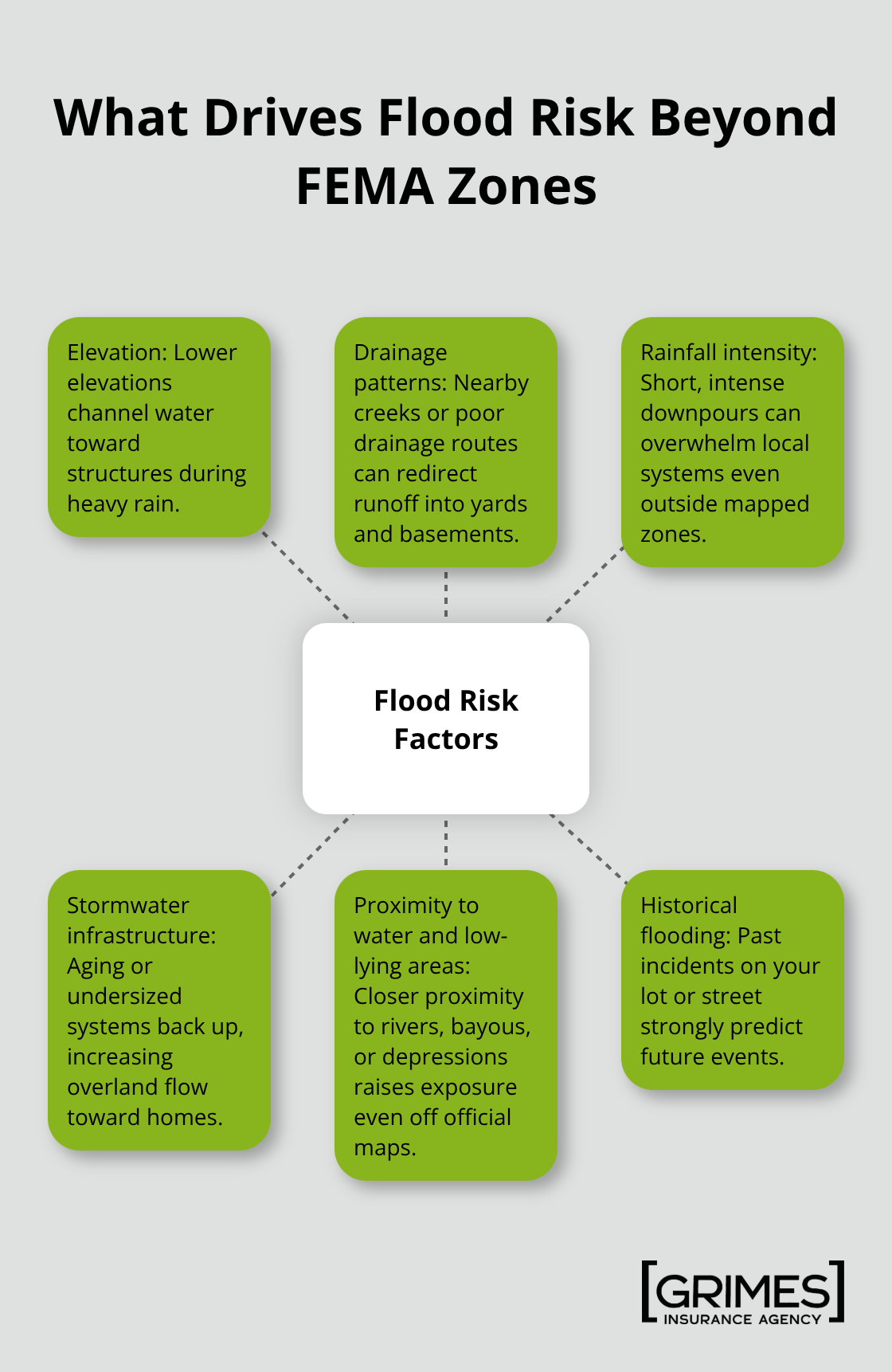

Flood risk matters enormously in Lubbock despite the city’s location away from major waterways. Check the FEMA flood maps for your specific address, then contact your mortgage lender to confirm whether flood insurance is required. Even if it’s not required, standing water from heavy rainfall or overflowing storm drains can cause thousands in damage that standard policies won’t cover.

Request Quotes From Multiple Carriers

Request quotes from at least three different carriers rather than relying on online comparison tools that often omit local options. Call State Farm, Farmers, and Chubb directly with your home details, then contact an independent agency that accesses multiple carriers simultaneously. Compare the actual monthly premiums for identical coverage levels-State Farm typically runs $228 monthly for $300,000 dwelling coverage in Lubbock while Farmers sits around $186, but ask specifically about wind and hail deductible structures since those vary dramatically between carriers.

Verify Financial Strength and Claims Performance

Don’t choose based on price alone. Check AM Best ratings for financial strength and J.D. Power customer satisfaction scores to verify that the cheapest option won’t disappear when you file a claim. Read recent customer reviews on Google and the National Association of Insurance Commissioners complaint database to see whether claims get paid quickly or disputed endlessly. Lubbock residents report that claims involving wind damage take anywhere from two weeks to three months depending on the carrier, so ask each insurer for their specific average claims timeline before committing.

Confirm Local Claims Adjuster Availability

Verify that your chosen carrier maintains local claims adjusters in Lubbock. If adjusters operate from Amarillo or Dallas, expect delays during major weather events when multiple claims flood in simultaneously. This local presence (or lack thereof) directly affects how quickly you receive payment after hail or wind damage strikes your home.

Final Thoughts

Selecting home insurance in Lubbock requires balancing coverage that protects your home, claims processing that works when you need it, and pricing that fits your budget. State Farm delivers reliability and local agent access with AM Best A++ ratings, Farmers undercuts competitors on monthly premiums at around $186 per month for a $300,000 dwelling, and Chubb serves high-value properties with extended replacement cost options. The top home insurance providers in Lubbock each excel in different areas, which is why comparing quotes across multiple carriers matters far more than picking a name you recognize.

An independent agency eliminates the guesswork by accessing multiple carriers simultaneously, so you receive competing quotes with identical coverage levels in a single conversation rather than calling insurers separately. This approach reveals which carriers offer the best wind and hail deductible structures for your home’s age and condition, which ones maintain local claims adjusters in Lubbock, and which ones impose unnecessary restrictions on older properties. An independent agent understands Lubbock’s unique weather risks, construction standards, and carrier quirks better than any national call center.

Contact Grimes Insurance Agency and provide your home’s details: age, square footage, roof condition, and replacement cost estimate. Request quotes from at least three carriers with identical dwelling coverage amounts and deductibles so you can compare apples to apples, then ask each carrier about wind and hail deductibles, flood exclusions, and their average claims timeline for weather-related losses. Choose based on the complete picture, not just the lowest monthly premium.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

Spring is the perfect time to dive into a deep cleaning session for your home. Instead of overwhelming yourself with an extensive checklist, let’s focus on five key things to keep in mind when tackling your spring cleaning tasks.

Spring is the perfect time to dive into a deep cleaning session for your home. Instead of overwhelming yourself with an extensive checklist, let’s focus on five key things to keep in mind when tackling your spring cleaning tasks.