Commercial Property Insurance for Real Estate Investors: Safeguarding Your Investments

Real estate investors face constant threats to their portfolios. From natural disasters to tenant lawsuits, one unexpected event can wipe out years of profit.

Commercial property insurance for real estate investors isn’t optional-it’s the foundation of smart investing. We at Grimes Insurance Agency help investors like you understand what coverage actually protects your assets and what gaps could cost you thousands.

What Commercial Property Insurance Actually Protects

Commercial property insurance covers the building structure itself, interior equipment, inventory, fixtures, and outdoor assets like signage and fencing. For real estate investors, this means protection against fire, theft, vandalism, wind damage, and lightning strikes. However, standard policies vary significantly in what they cover. A basic form policy protects against common perils like fire and theft, while a broad form adds water damage and falling objects. A special form covers all non-excluded perils, which is substantially more comprehensive but also more expensive.

Many investors assume flood damage is covered and discover too late that it isn’t. The National Flood Insurance Program (administered by FEMA) handles flood coverage separately, and you must purchase it independently if your property sits in a flood zone. Similarly, earthquake insurance requires a separate rider in states prone to seismic activity. Standard policies also exclude wear and tear, neglect, and pollution-related damage, so read your policy documents carefully to identify gaps.

Building and Contents Coverage

Real estate investors often focus only on building coverage but overlook contents insurance, which protects equipment, tools, furniture, and fixtures inside the property. This matters significantly if you own specialized equipment or maintain on-site storage. Contents insurance covers items your tenants depend on for operations, and you remain responsible for protecting those assets.

Income Protection During Disruptions

Business interruption insurance, also called loss of income coverage, allows businesses to pay fixed expenses, including costs incurred while operating at an offsite location, while the property is closed for repairs. If a fire damages a retail tenant’s space and repairs take three months, business interruption coverage replaces the rent you would have collected. A Business Owner’s Policy bundles property, liability, and business income coverage into one streamlined package, often saving 10 to 15 percent on premiums compared to purchasing policies separately.

Understanding Your Premium Costs

Small businesses typically pay between $1,000 and $3,000 annually for commercial property insurance, roughly $83 to $250 monthly depending on location, property age, construction type, and occupancy. Properties in Florida, California, and Texas cost substantially more due to hurricane, wildfire, and tornado exposure. Replacement cost coverage pays the full amount to rebuild or replace damaged items at current prices, while actual cash value policies pay depreciated amounts. Replacement cost costs more upfront but protects your investment far better.

Your choice between these coverage types directly affects both your premiums and your financial recovery after a loss. Understanding which perils your policy covers and which gaps exist sets the stage for selecting the right coverage limits and additional protections your specific properties need.

What Threatens Your Real Estate Portfolio

Natural Disasters Strike Fixed Locations Hard

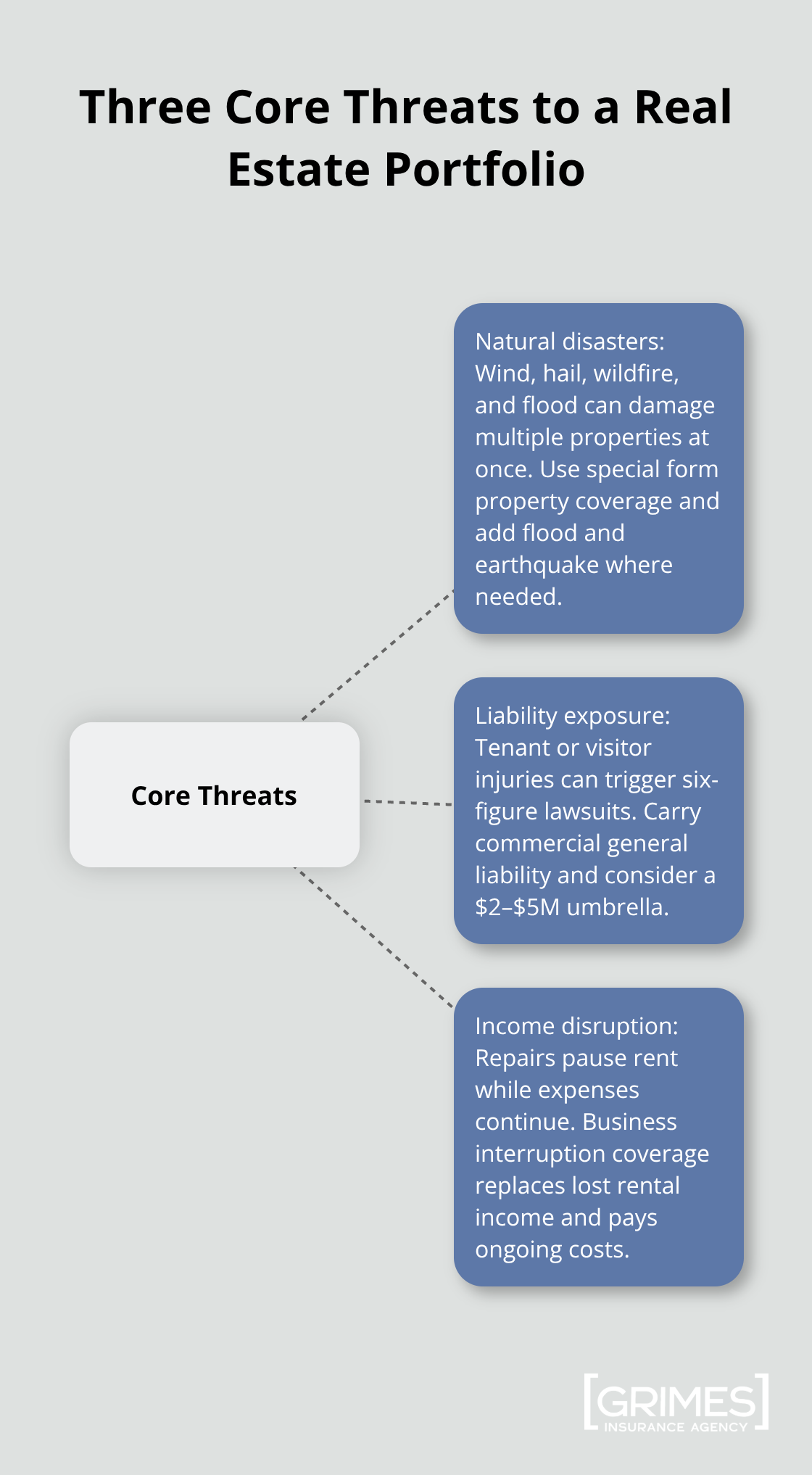

Natural disasters hit real estate investors harder than most business owners because your properties sit in fixed locations you cannot relocate. Hurricane damage in Florida doesn’t just destroy one building-it can wipe out an entire portfolio concentrated in coastal areas. The Insurance Information Institute reports that hurricanes cause an average of $7.2 billion in insured losses annually across the United States, with Florida accounting for a significant portion. If your properties lack wind coverage or sit outside the NFIP flood program, a single hurricane season could exceed your liquid reserves.

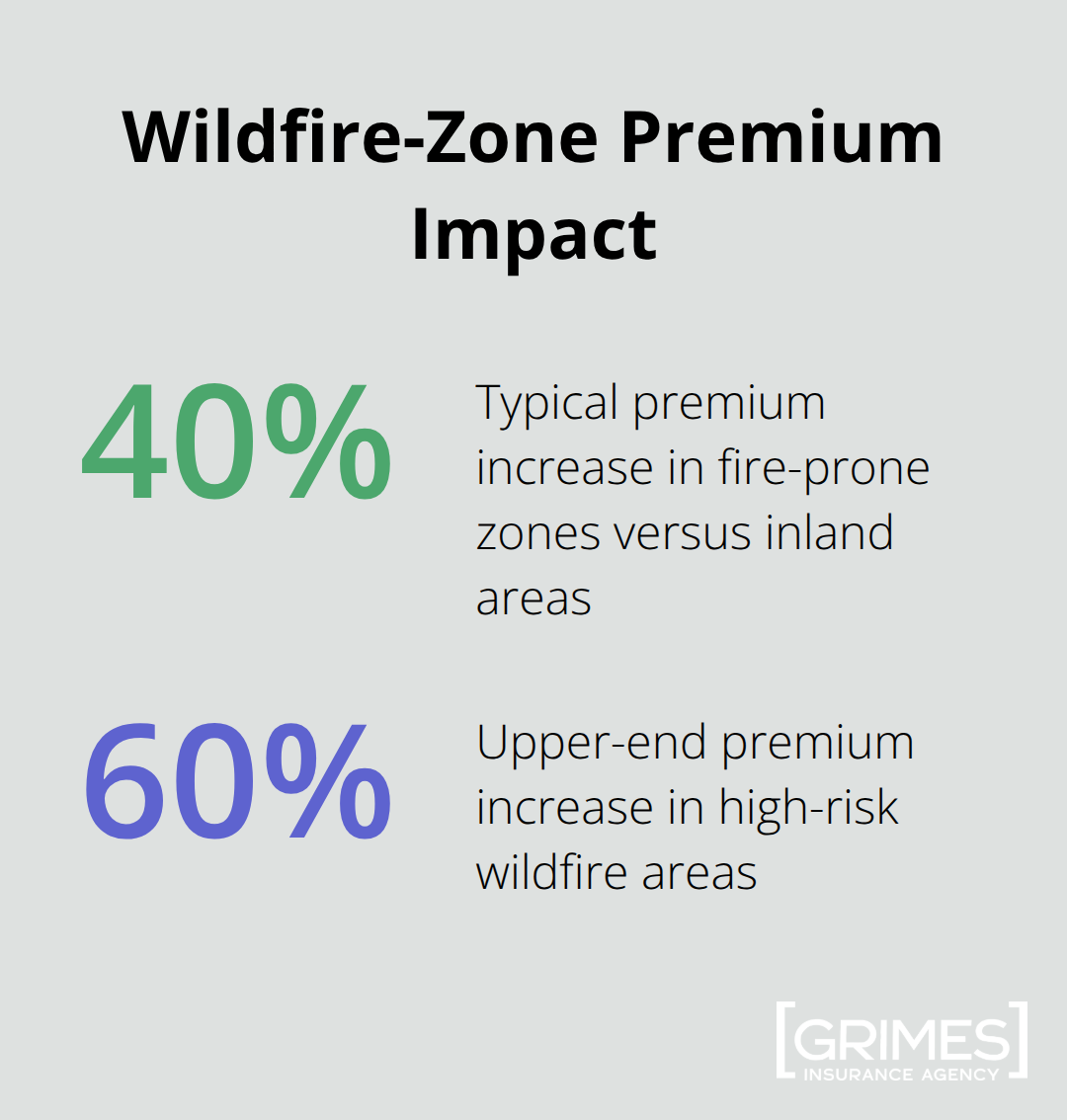

Wildfires in California and Texas present similar threats. Properties in fire-prone zones face premiums that climb 40 to 60 percent higher than inland properties, yet many investors skip adequate coverage to save money-a decision that costs far more when flames arrive. Hail damage to roofs happens faster than most investors expect. A single hailstorm in Texas can damage hundreds of properties within hours, leaving repair queues that stretch months and causing temporary vacancy losses.

Taking Action on Location-Specific Risks

Brutal honesty about your location’s specific risks separates successful investors from those who face catastrophic losses. If your property sits within a flood zone, you must purchase separate flood insurance regardless of cost. If it sits in a wildfire corridor or tornado alley, upgrade to a special form policy that covers all non-excluded perils rather than relying on basic coverage.

Liability Claims Drain Portfolios Quickly

Liability claims from tenants and third parties represent a different category of threat that many real estate investors underestimate. A tenant slips on a wet floor in a common area and sues for $200,000 in medical bills plus lost wages-your liability coverage must respond quickly or your personal assets face seizure. A visitor trips on a broken step and claims permanent disability, demanding $500,000 in damages. These scenarios happen constantly.

Commercial general liability insurance covers bodily injury and property damage claims arising from accidents on your property, and the coverage limits matter tremendously. Most small commercial properties carry $1 million limits, but a serious injury claim can exceed that threshold within weeks. Investors carrying multiple properties should consider umbrella coverage that extends $2 to $5 million of additional protection across the entire portfolio at a fraction of the cost of raising individual policy limits.

Rental Income Stops While Expenses Continue

Loss of rental income during property downtime cuts deeper than most investors realize because your expenses don’t stop when tenants cannot occupy the space. Property taxes, mortgage payments, insurance premiums, and maintenance costs continue whether the building generates revenue or not. A fire that closes a retail tenant’s space for four months doesn’t just eliminate that month’s rent-it eliminates four months of rent while your fixed costs continue uninterrupted.

Business interruption coverage reimburses lost rent and covers your ongoing operating expenses during the repair period, making it non-negotiable for investors whose cash flow depends on consistent monthly rental income. Without this coverage, you absorb the entire financial impact yourself. These three threat categories-natural disasters, liability exposure, and income disruption-demand different coverage solutions that work together to protect your portfolio.

How to Choose the Right Commercial Property Insurance

Calculate your property’s replacement value, not its market value. Market value and replacement cost diverge significantly, especially in hot real estate markets where land appreciation outpaces construction costs. A property worth $500,000 on the market might cost $650,000 to rebuild from scratch due to current labor and material expenses. Contact three local contractors and request rebuild estimates for each property you own. This single step prevents the catastrophic mistake of underinsuring by $100,000 or more.

Inventory everything inside the building that your tenants depend on for operations. Equipment, HVAC systems, electrical infrastructure, and specialized fixtures all require coverage. A retail space with custom shelving and point-of-sale systems costs far more to replace than a bare warehouse. Document these items with photos and purchase receipts because insurers will request proof during claims. Your contents coverage limits should reflect this actual inventory value, not a rough estimate.

Location Risk Drives Pricing More Than You Expect

Location risk determines pricing more aggressively than most investors expect, so obtain quotes from at least five different carriers rather than accepting the first offer. Geographic proximity to fire stations and police departments can lower premiums by 10 to 15 percent according to industry standards, while properties in high-crime areas or flood zones face substantially higher costs. Request quotes using identical property details to compare apples-to-apples pricing.

Ask each carrier specifically what perils their basic form excludes and what endorsements would add flood, earthquake, or equipment breakdown coverage. One carrier’s $1,200 annual premium might jump to $2,100 with flood coverage included, while another carrier quotes $1,400 with flood already bundled. These differences matter enormously over a five or ten-year investment horizon. Many investors make the mistake of shopping price alone without examining coverage limits and exclusions, then face massive gaps when claims arise.

Compare replacement cost versus actual cash value options for each quote because this choice impacts both your premium and your recovery. Replacement cost coverage provides more protection than actual cash value coverage, though it can also be more expensive because it costs the insurance company more.

Adjust Deductibles to Control Your Costs

Higher deductibles reduce premiums more dramatically than most investors realize. Moving from a $500 deductible to $2,500 typically lowers your annual premium by 15 to 25 percent, saving $150 to $750 yearly on a $1,000 to $3,000 annual policy. Over a ten-year holding period, that compounds to $1,500 to $7,500 in premium savings. The math only works if you can absorb a $2,500 loss from operating reserves without derailing your business.

Conservative investors comfortable with higher out-of-pocket costs should choose $2,500 or $5,000 deductibles. Aggressive investors who need predictable claims costs should stay at $1,000. Your cash position, not industry norms, should drive this decision.

Work With an Independent Broker for Better Coverage

An independent insurance broker who represents multiple carriers provides advantages that captive agents cannot match. Captive agents represent one company and cannot show you competing quotes, forcing you to shop multiple carriers independently. Independent brokers access ten to twenty carriers simultaneously, exposing pricing variations you would never discover alone.

Ask potential brokers whether they specialize in real estate investor coverage and request references from other property investors they represent. A broker unfamiliar with commercial real estate investing will miss coverage gaps specific to rental properties, like loss-of-rent protection and tenant-damage liability. Interview brokers about their claims handling process because premium price means nothing if the carrier delays payments or disputes coverage when you file a claim.

Request the broker’s contact information for three clients who filed claims in the past two years and ask those clients directly whether the broker responded promptly and advocated effectively during the claims process.

Final Thoughts

Commercial property insurance for real estate investors protects far more than buildings and equipment-it protects your cash flow, your personal assets, and your ability to weather financial storms that destroy unprepared investors. When a fire closes a tenant’s space for three months, business interruption coverage replaces the income you would have lost. When a visitor sues for injuries sustained on your property, liability coverage defends you without depleting your reserves.

The path forward requires three concrete actions. First, calculate your actual replacement costs by contacting local contractors rather than guessing based on market value. Second, obtain quotes from at least five carriers using identical property details so you can compare coverage and pricing accurately (this exposes pricing variations you would never discover alone).

We at Grimes Insurance Agency understand that real estate investors need coverage tailored to rental properties, not generic commercial policies designed for retail shops or offices. Work with an independent insurance broker who specializes in real estate investor coverage and can access multiple carriers simultaneously to ensure your properties receive the protection they deserve.