Key Factors in Commercial Property Insurance: What to Look For

Commercial property insurance protects your business assets, but choosing the right coverage requires understanding several key factors. Many business owners overlook critical details that could leave them underinsured or paying for unnecessary protection.

At Grimes Insurance Agency, we’ve seen firsthand how the right decisions during the selection process make a real difference. This guide walks you through what matters most when protecting your commercial property.

What Coverage Do You Actually Need?

Property coverage and liability coverage serve completely different purposes, and confusing them is one of the biggest mistakes we see business owners make. Property coverage protects your building structure, equipment, inventory, and furniture from perils like fire, theft, wind, and vandalism. Liability coverage protects you when someone gets injured on your property or when your operations damage someone else’s property.

A Hartford study found that a Business Owner’s Policy bundles property and general liability together and has helped over 1.5 million small business owners avoid gaps between these two protections. The distinction matters because a fire that destroys your equipment is a property claim, while a customer who slips on your wet floor and sues you is a liability claim. Many owners assume one policy covers both and end up with dangerous gaps.

How Much Property Coverage You Truly Need

Most business owners underestimate what their building and contents are actually worth. You need replacement cost coverage, not actual cash value, because material and labor costs have skyrocketed. The U.S. Bureau of Labor Statistics reported that inflation hit a 40-year high in mid-2022 and remained elevated, meaning reconstruction costs today far exceed what older appraisals suggest.

If your building is worth $500,000 but you only insure it for $350,000, you will absorb the difference when disaster strikes. Calculate your building value by considering the cost to rebuild from scratch with modern materials and current construction standards, not what you paid for it years ago. Include every piece of equipment, machinery, tools, and inventory in your count.

Many owners skip this step and discover during a claim that they are thousands of dollars short. The gap between underinsurance and actual replacement costs (driven by inflation and material availability) can devastate a business that thought it had adequate protection.

Business Interruption Insurance Stops the Bleeding

When a covered loss forces you to close temporarily, your expenses do not pause. You still owe salaries, rent, loan payments, property taxes, and utilities while generating zero revenue. Business interruption insurance will pay for the business’s lost income and other expenses while it’s non-operational.

This coverage is especially critical if you operate a retail storefront, restaurant, or any business where foot traffic directly drives income. Without it, a two-week closure from a kitchen fire can bankrupt a restaurant even if the property damage itself is insured. The policy typically covers the time needed for repairs plus a reasonable period to restore customer operations back to normal levels.

Why Location and Risk Profile Matter Next

Your building’s location, age, and the type of business you operate all influence what coverage you actually need and what you will pay for it. Understanding these factors helps you make informed decisions about coverage limits and additional protections before you face a loss.

What Really Drives Your Insurance Rates

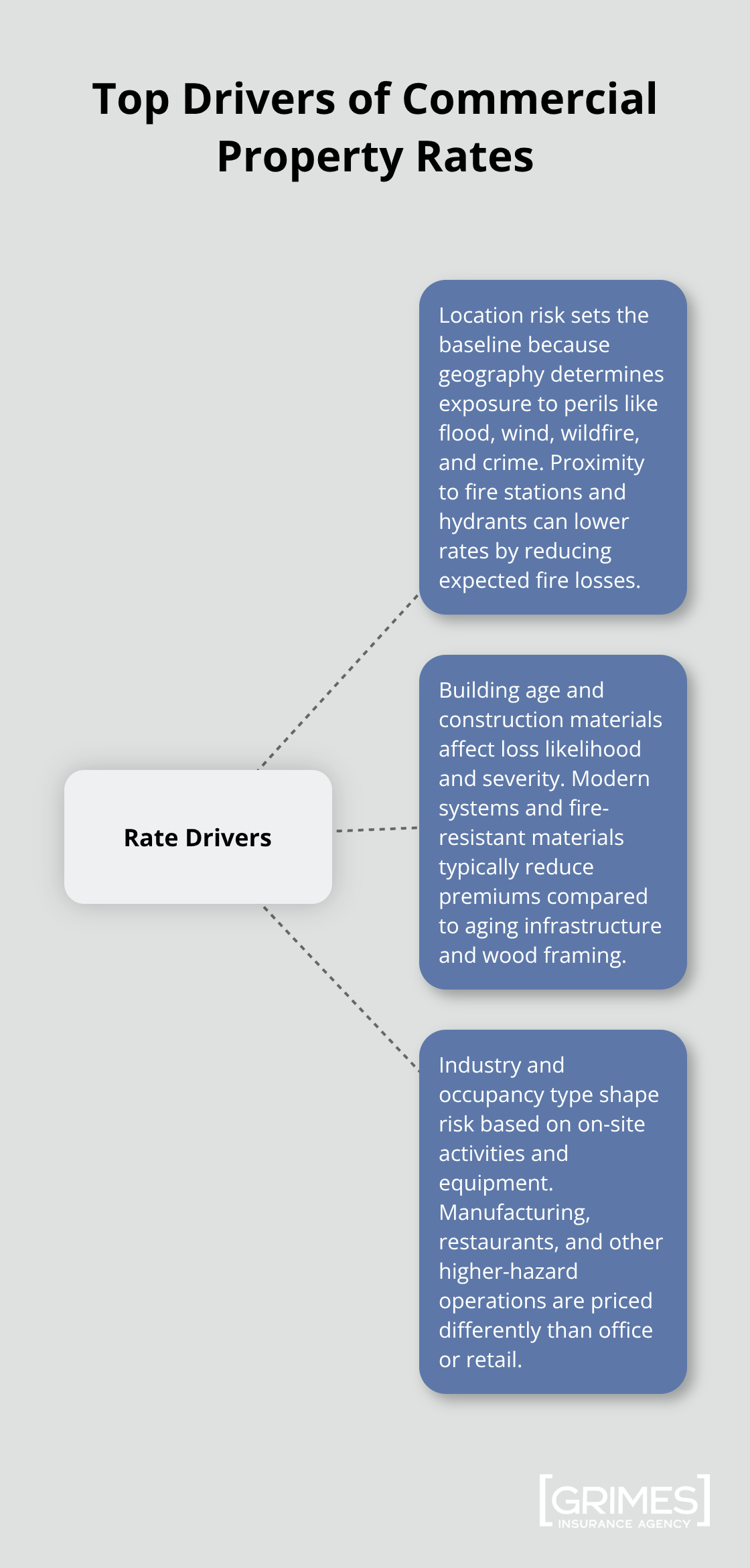

Location Creates Your Rate Foundation

Your insurance premium is not arbitrary, and understanding what insurers actually measure separates smart business owners from those who overpay or underpay. Location risk sits at the top of the rate calculation because geography determines your exposure to specific perils. A building in a flood-prone area near the coast will pay substantially more than an identical property fifty miles inland, even if both are equally well-maintained. Proximity to fire stations and hydrants directly lowers premiums because faster emergency response reduces fire damage severity. Properties in high-crime neighborhoods face higher theft and vandalism risk, which shows up immediately in your quote.

You cannot change your location, but understanding how it affects your rate helps you evaluate whether additional protections like flood insurance make financial sense for your situation.

Building Age and Construction Materials Control What You Pay

Building age and construction materials is the second major rate driver, and here you have more control. Older structures typically carry higher premiums because outdated electrical systems, aging plumbing, and weaker structural integrity create genuine risk. A ten-year-old building with modern fire-resistant materials and updated safety systems will cost less to insure than an older property.

The good news is that upgrading key systems actually reduces your premium. If you own an older property, investing in electrical rewiring, plumbing modernization, or installing sprinkler systems and fire alarms pays for itself through lower insurance costs over time. Construction materials matter too because concrete and steel structures cost less to insure than wood-frame buildings.

Your Industry Classification Shapes Risk Assessment

Your industry classification and what actually happens inside your building rounds out the rate picture. A manufacturing facility with heavy machinery creates different risk than an office space, and a restaurant with commercial cooking equipment faces different hazards than a retail boutique. Occupancy type directly influences premium because insurers price based on the specific activities and equipment your business uses.

If you operate a higher-risk business, you cannot avoid the premium increase, but you can control how well you mitigate those risks through proper maintenance, safety equipment, and documented protocols. The steps you take to manage risk within your industry will determine whether you pay top dollar or negotiate better rates at renewal time.

Common Mistakes That Leave Businesses Dangerously Exposed

Underestimating Property Value Costs You Thousands

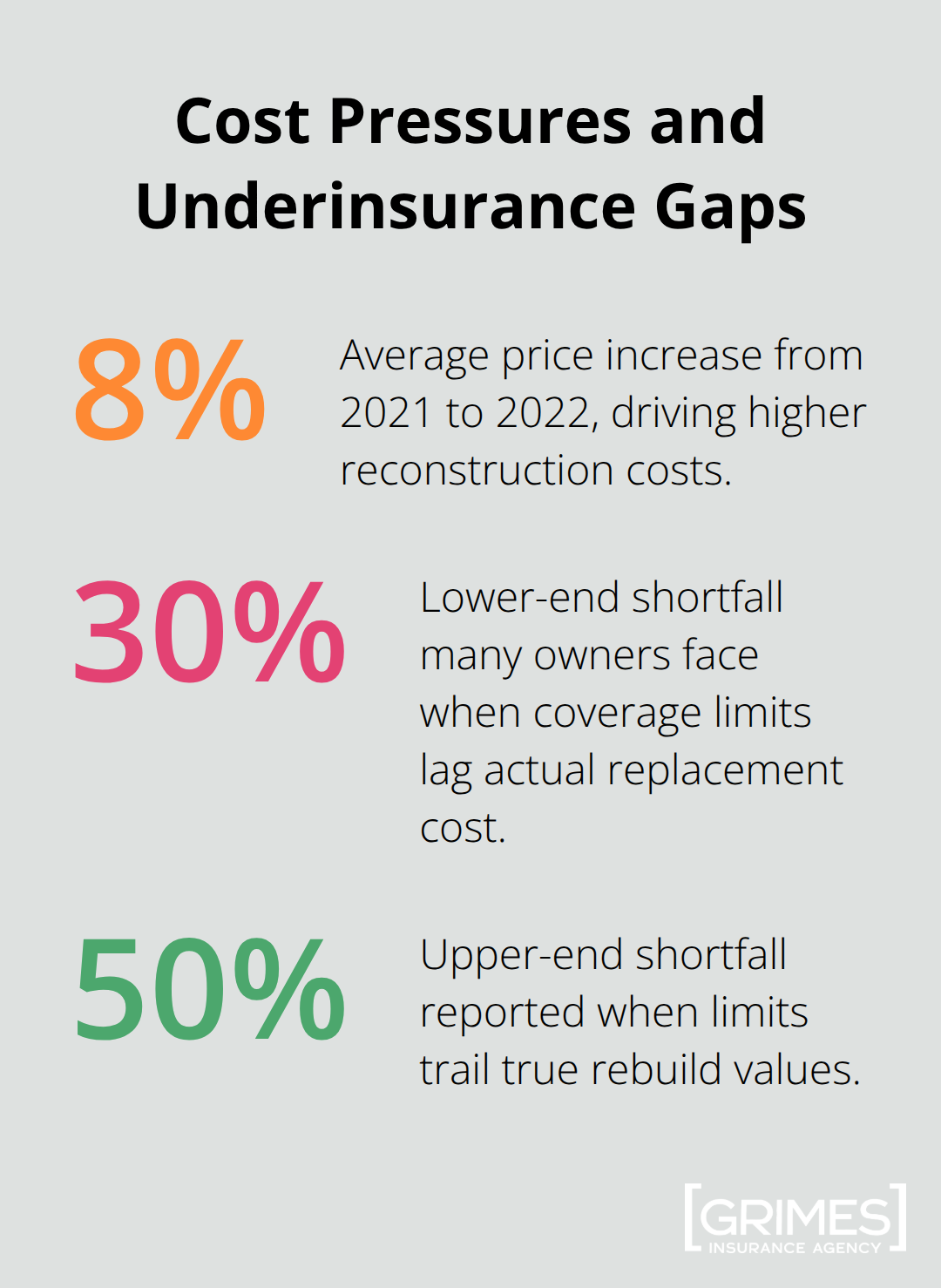

Most business owners make the same critical errors when selecting commercial property insurance, and these mistakes compound over time. The first mistake is catastrophic underestimating property value. You cannot simply add up what you paid for your building and equipment years ago and call that your coverage limit. Material costs have exploded, and prices rose by an average of 8.0 percent from 2021 to 2022.

A manufacturing facility that cost $800,000 to build in 2015 now costs $1.2 million to reconstruct with current labor and materials. When you insure that same facility for $800,000 today, you absorb the $400,000 gap yourself during a total loss. Business owners discover during claims that their coverage limits fall 30 to 50 percent below actual replacement costs.

The fix is straightforward but requires action. Get a current appraisal of your building structure separate from land value. Price out your equipment and inventory with today’s vendor quotes, not historical purchase receipts. Add 15 percent cushion for cost overruns and inflation that occurs during reconstruction. Update this calculation annually because replacement costs keep rising.

Overlooking Specialized Coverages Creates Hidden Gaps

The second mistake is overlooking specialized coverages that protect against risks outside standard property policies. Equipment breakdown insurance covers the cost of repairing or replacing machinery when electrical or mechanical failure occurs, and it includes coverage for spoiled inventory and lost revenue during downtime. A restaurant owner with a failed walk-in cooler faces thousands in spoiled food and lost business while repairs take weeks, yet many standard policies skip this protection entirely.

Accounts receivable insurance covers losses when payment records are destroyed in a fire or flood, protecting your ability to collect from customers and maintain cash flow. Inland marine insurance protects tools and equipment in transit or at job sites, critical for contractors and service businesses. A single oversight with specialized coverage can cost more than the annual premium savings you thought you gained.

Treating Your Policy as Static Leaves You Exposed

The third mistake is treating your insurance policy as a static document that never needs attention. Business changes require coverage adjustments. You expanded your inventory, added expensive equipment, opened a second location, or changed your primary business activity. Your policy from three years ago no longer matches your actual risk profile.

Most policies should be reviewed during renewal conversations with your agent, and major business changes warrant immediate policy reviews. The cost of reviewing coverage takes an afternoon; the cost of discovering gaps during a claim takes years to recover from.

Final Thoughts

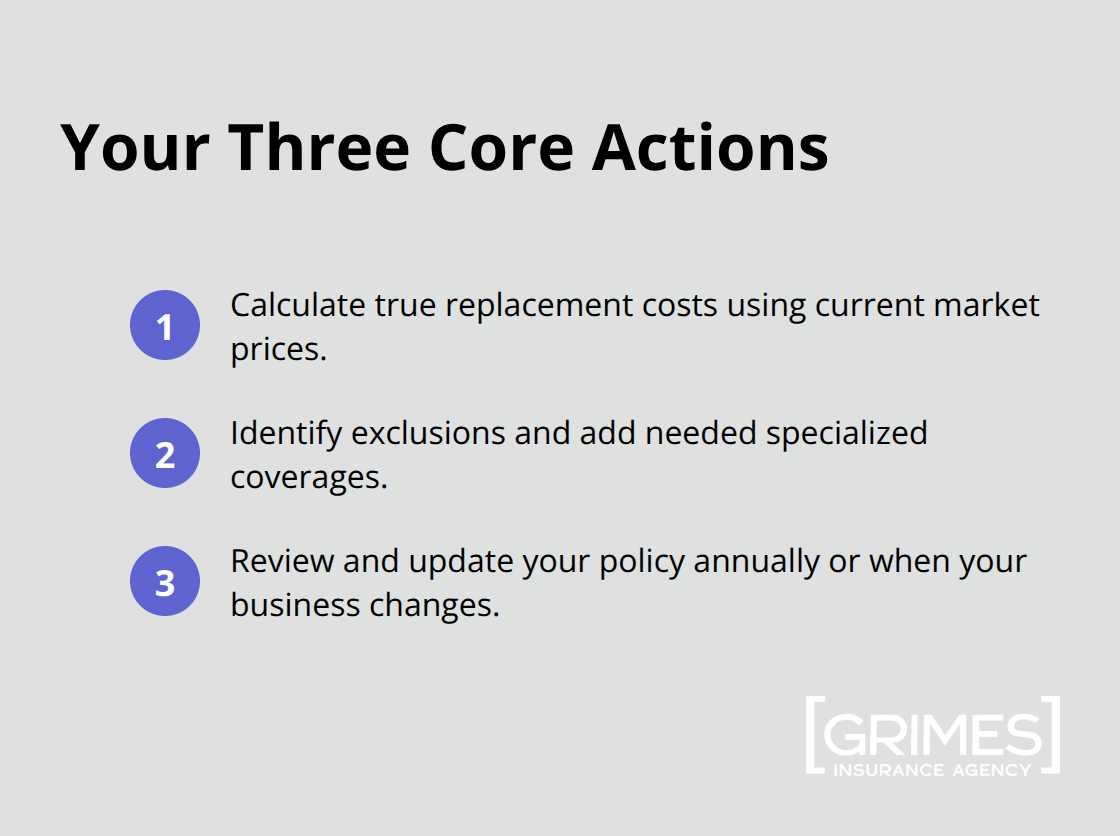

Selecting adequate commercial property insurance comes down to three core actions. First, calculate your actual replacement costs using current market prices, not historical purchase receipts. Second, identify gaps in your coverage by reviewing what standard policies exclude, then add specialized protections like equipment breakdown or accounts receivable insurance.

Third, commit to annual policy reviews whenever your business changes or your asset values shift.

The key factors in commercial property insurance-location, building age, business type, and coverage limits-all demand your attention during the selection process. Getting these right protects your business from catastrophic financial loss. Getting them wrong leaves you exposed to thousands in uninsured damages or paying for protections you do not need.

Working with an insurance professional who understands commercial property makes this process faster and more accurate. Contact Grimes Insurance Agency to discuss your commercial property insurance needs and ensure your coverage matches your actual risk.