Home Insurance Coverage for Natural Disasters: Are You Fully Protected?

Your homeowner’s insurance likely covers wind, hail, and fire damage. But most policies have significant gaps when it comes to natural disasters.

At Grimes Insurance Agency, we’ve seen too many homeowners discover they’re underprotected when disaster strikes. The difference between adequate home insurance coverage for natural disasters and a policy full of holes can cost you thousands.

What Your Standard Home Insurance Actually Covers

Wind and Hail Protection in Your Policy

Standard homeowners policies cover wind and hail damage as core perils. Most insurers will pay for roof damage, broken windows, and structural harm caused by high winds or severe hail storms. Your coverage limit matters enormously here-if your home suffers $50,000 in wind damage but your policy caps dwelling coverage at $300,000, you remain protected. But if your home requires $500,000 to rebuild, that same $50,000 loss represents only partial protection.

Named-Storm Deductibles Change the Game

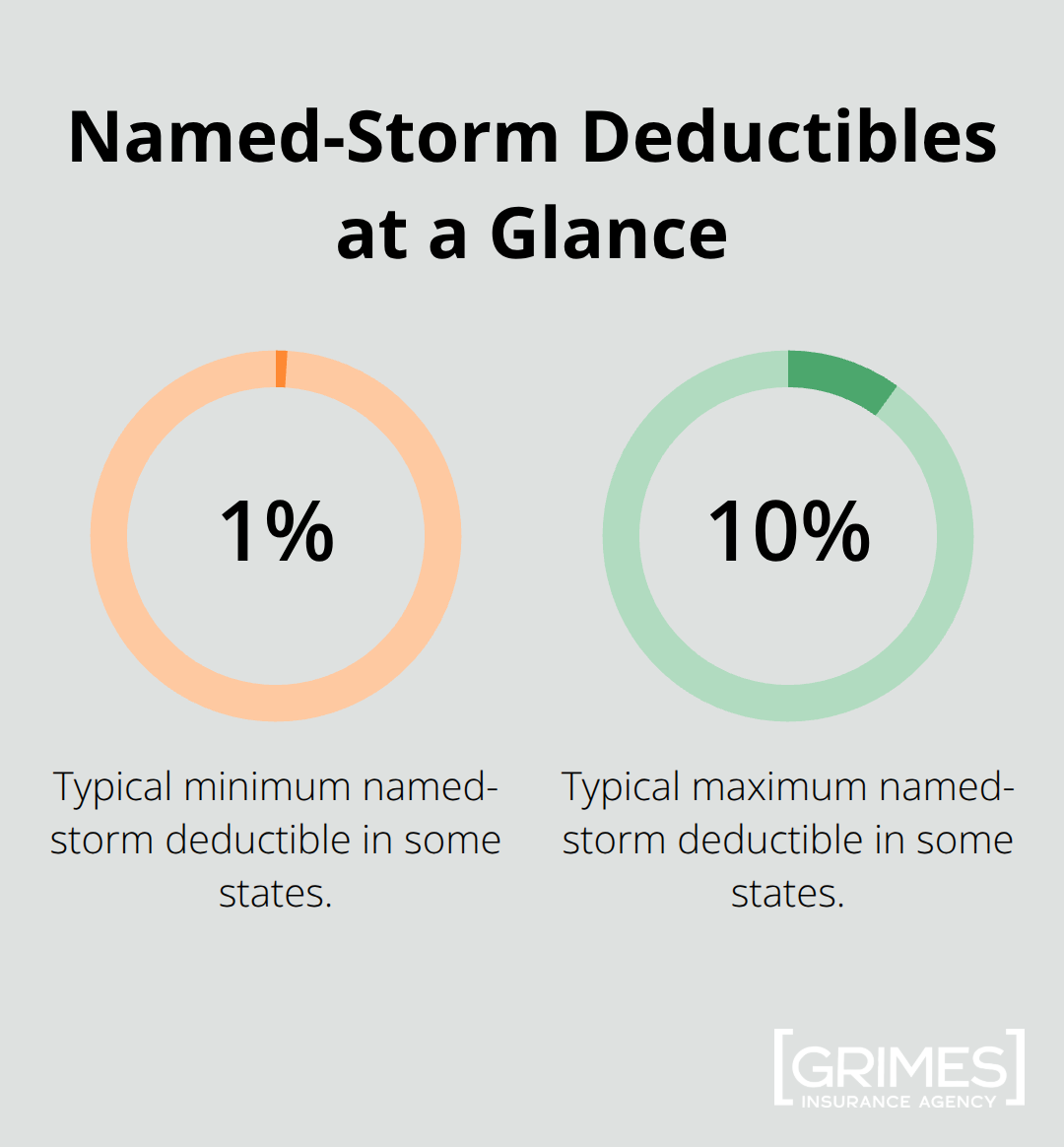

Named-storm deductibles exist in 19 states and the District of Columbia, and this matters significantly if you live in a hurricane-prone area. These deductibles typically range from 1% to 10% of your insured home value or a fixed dollar amount, meaning a $400,000 home in Florida might trigger a $4,000 deductible when a named hurricane hits-substantially higher than your regular $500 deductible. Insurers restrict coverage within one to two days of a hurricane, so you cannot add or increase coverage right before a storm arrives. This timing restriction forces homeowners to plan ahead rather than react at the last moment.

Fire, Smoke, and Lightning Coverage

Fire and smoke damage fall under standard coverage, protecting you against structural damage and contents destroyed by flames or smoke infiltration. Lightning strikes and resulting electrical damage are typically covered too, though the damage pathway matters. Direct lightning damage to your home receives coverage, but damage to appliances or electronics caused by a power surge during a lightning event may fall outside standard coverage unless you’ve added an endorsement. Understanding this distinction prevents costly surprises when electrical equipment fails after a storm.

The Real Cost of Underinsurance

Review your current policy limits immediately against your home’s actual rebuilding cost, not its market value including land. If your policy hasn’t been updated in two or three years, your coverage limits almost certainly fall short of current replacement costs. This gap between what you think you’re covered for and what you actually need to rebuild creates serious financial exposure.

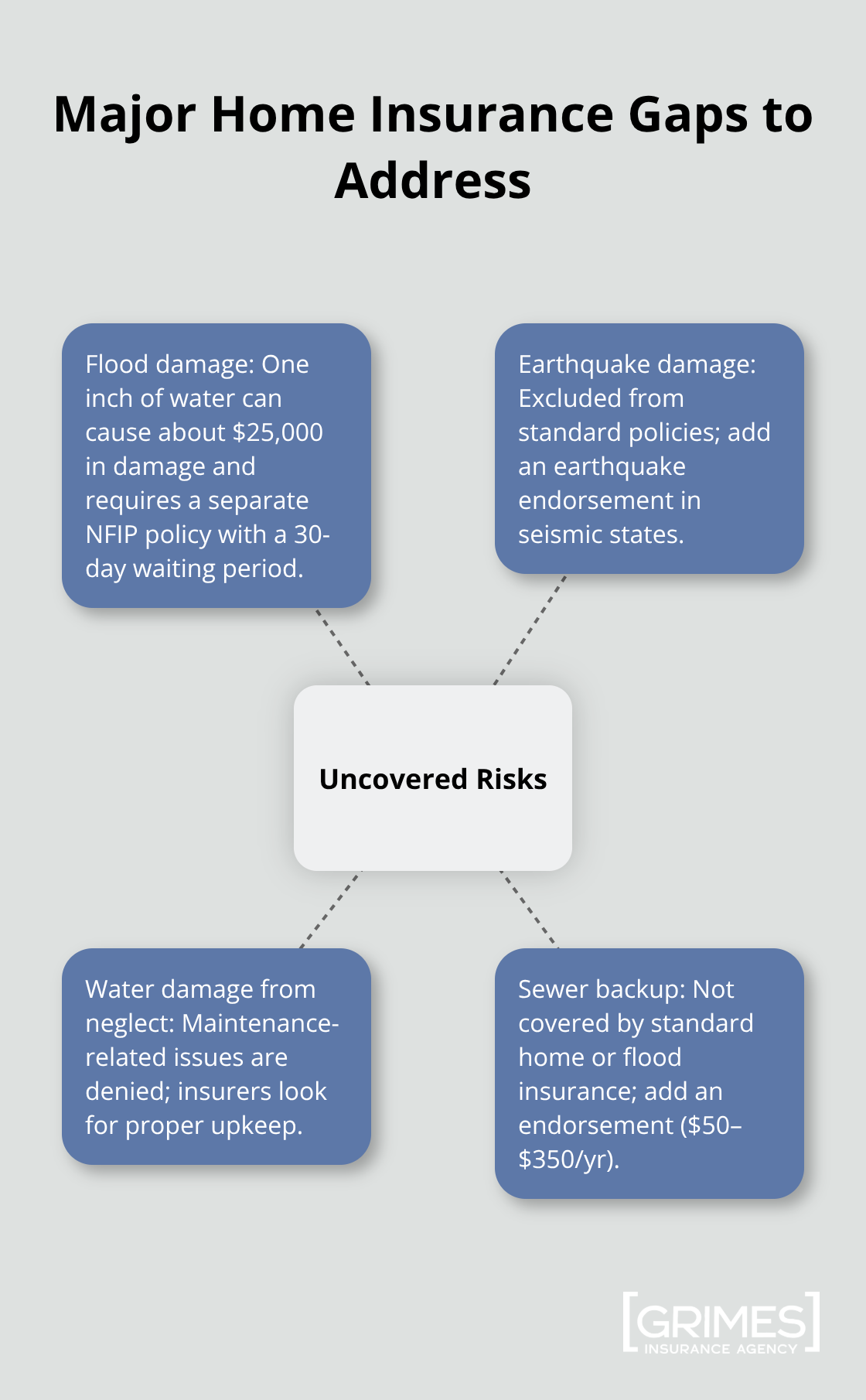

The gaps in standard coverage become apparent only when you examine what happens after a disaster strikes. Flood damage and earthquake damage and water damage from poor maintenance all fall outside standard policies-and these exclusions affect far more homeowners than most realize.

What Your Policy Leaves Unprotected

Flood Damage: The Costliest Gap

Flood damage stands as the most expensive gap in standard homeowners insurance, yet most people don’t realize they lack this coverage until water enters their home. One inch of water causes approximately $25,000 in damage according to FEMA data, making this exclusion potentially catastrophic. The National Flood Insurance Program administers flood coverage through FEMA, and you must purchase a separate policy if you have a mortgage in a high-risk flood zone. You can obtain flood insurance through the National Flood Insurance Program or private insurers, but the coverage includes a 30-day waiting period before activation. This waiting period prevents you from purchasing flood protection days before a hurricane arrives-you need to act well in advance of storm season. The NFIP serves about 4.7 million policyholders with nearly $1.3 trillion in total coverage across approximately 22,600 participating communities nationwide.

Earthquake Coverage Gaps

Earthquake damage receives exclusion from standard policies in most states, creating another major protection gap. If you live in a seismic zone, you must purchase a separate earthquake endorsement, yet many homeowners remain unaware this coverage even exists. This gap affects homeowners in California, Washington, Oregon, and other regions with significant seismic activity, leaving them exposed to potentially devastating losses without additional protection.

Water Damage from Neglect

Water damage from poor maintenance or lack of upkeep receives no coverage whatsoever, and insurers actively deny claims when they determine negligence caused the damage. A leaky roof ignored for two years, rotting wood from deferred maintenance, or mold growth from delayed repairs all fall outside your protection. This distinction matters enormously because it shifts responsibility directly to you-your insurer will investigate whether you maintained your property adequately before approving any claim related to water intrusion.

Sewer Backup: A Hidden Threat

Sewer backup damage, another common exclusion, costs homeowners thousands when their sewer line backs up into the basement during heavy rain. Standard flood insurance does not cover sewer backup either, forcing you to purchase a separate endorsement costing between $50 and $350 annually depending on coverage limits. You typically bear responsibility for sewer lines from your home to the city system, making this coverage particularly important for older homes with aging pipes.

These specific exclusions transform your approach to home protection because they reveal exactly where your policy fails. The next step involves examining your current coverage details and identifying which gaps pose the greatest risk to your financial security.

How to Assess Your Coverage and Fill the Gaps

Review Your Policy Documents Today

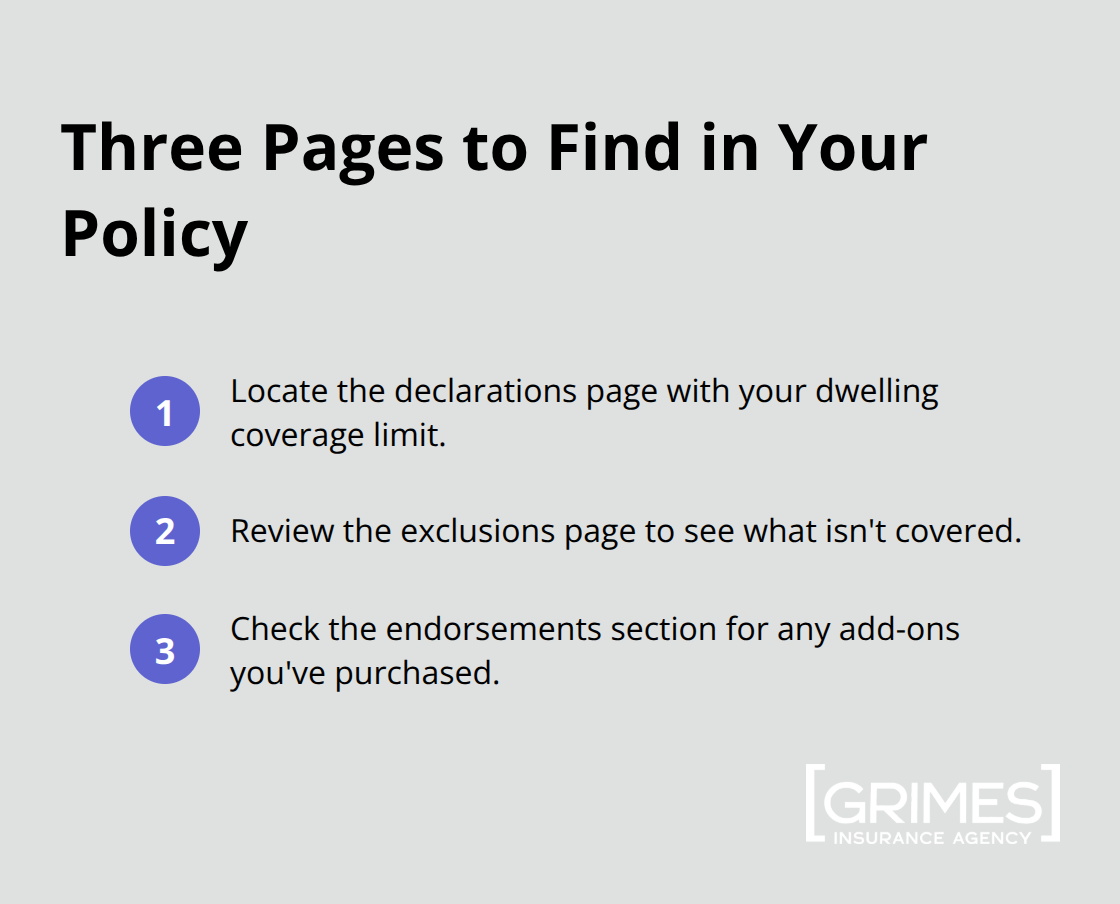

Pull out your actual homeowners policy document-not the summary or marketing materials, but the full policy itself. Most homeowners keep this in a drawer or file and never read it again after purchase. Open it and locate three specific sections: the declarations page showing your dwelling coverage limit, the exclusions page listing what isn’t covered, and the endorsements section showing any add-ons you’ve purchased. Your dwelling coverage limit must reflect what it would actually cost to rebuild your home today, not what it cost five years ago.

Check Your Dwelling Limits Against Current Costs

Construction costs have climbed significantly since 2020. Real premiums have risen approximately 20 percent between 2020–2023 alone. If your policy shows a dwelling limit below $400,000 and you live in an area where rebuilding costs exceed $200 per square foot, your coverage falls short of what you actually need. Named-storm deductibles also matter enormously-if you live in Florida, Georgia, Louisiana, or other hurricane-prone states, this deductible could cost you $2,000 to $10,000 out of pocket when a hurricane strikes. Look specifically for whether you have flood coverage listed; if the word flood does not appear anywhere on your endorsements page, you have zero flood protection regardless of what your standard policy says.

Identify Your Location-Specific Gaps

Compare what your policy actually covers against the disasters that threaten your specific location. If you live anywhere in a flood zone-and many homeowners discover they’re in flood zones only after buying a home-you need separate flood insurance through the National Flood Insurance Program, which operates in approximately 22,600 participating communities. Contact NFIP at 877-336-2627 or use their online quote tool to get pricing; most policies activate after a 30-day waiting period, so waiting until hurricane season arrives means you cannot obtain coverage. If you live in California, Washington, Oregon, or other seismic regions, earthquake coverage costs between $100 and $500 annually depending on your home’s value and location-this is optional coverage that your standard policy explicitly excludes.

Add Specialized Policies for High-Risk Events

Sewer backup protection costs $50 to $350 per year and requires you to call your current insurer and ask specifically whether this endorsement is available; many insurers offer it, but you must request it by name. Calculate the financial risk each gap poses: a basement flood could cost $25,000 in damage according to FEMA data, an earthquake could cause $50,000 or more in structural damage, and a sewer backup during heavy rain could easily exceed $10,000 in cleanup and restoration. Once you understand your actual exposure, you can make informed decisions about which additional policies justify the annual cost. Contact your insurance agent or shop with multiple insurers to compare pricing on these specialized coverages, because rates vary substantially based on your specific risk profile and the insurer’s appetite for that particular peril.

Final Thoughts

Your home represents your largest financial asset, yet most homeowners carry insurance policies that leave them dangerously exposed when natural disasters strike. The gaps we’ve outlined-flood damage, earthquakes, sewer backups, and water damage from maintenance issues-affect real families every year, often resulting in losses exceeding $25,000 or more. Standard homeowners policies simply don’t address these vulnerabilities, which means the protection you think you have likely falls short of what you actually need.

Pull your policy documents this week and compare your dwelling limits against current rebuilding costs in your area. If you live in a flood zone, contact the National Flood Insurance Program at 877-336-2627 to obtain a quote before hurricane season arrives, since the 30-day waiting period means timing matters enormously. If you’re in an earthquake-prone region, request earthquake endorsement pricing from your current insurer, and ask specifically about sewer backup coverage, which costs between $50 and $350 annually and protects against one of the most common and expensive water-related claims.

Your location determines which gaps pose the greatest financial risk to your household (a homeowner in Florida faces different natural disaster threats than someone in California or the Pacific Northwest). We at Grimes Insurance Agency work with multiple carriers to find the right combination of policies and pricing for your home insurance coverage for natural disasters. Visit us at https://grimesinsurance.com to discuss your coverage gaps with an agent who understands your local risks and can help you build a comprehensive protection strategy.