Flood Insurance Coverage Options in 2025: What Homeowners Need to Know

Flooding has become one of the most expensive natural disasters for homeowners, with the National Flood Insurance Program paying out over $3 billion annually in claims. Most homeowners don’t realize their standard insurance policy leaves them completely unprotected against flood damage.

At Grimes Insurance Agency, we help homeowners understand the flood insurance coverage options available in 2025 so they can make informed decisions about protecting their properties. This guide walks you through your choices and how to pick the right coverage for your situation.

Why Your Standard Homeowners Policy Won’t Protect You From Floods

The Coverage Gap That Leaves Homeowners Vulnerable

Flooding costs American homeowners billions annually, yet most people believe their standard homeowners insurance covers this damage. It doesn’t. Your homeowners policy explicitly excludes flood damage, whether the water comes from heavy rainfall, overflowing rivers, storm surge, or saturated ground. According to FEMA, standard homeowners policies, condo policies, and renters insurance universally exclude flood losses. This means a one-inch flood in your home can cause up to $25,000 in damage with zero coverage from your existing policy.

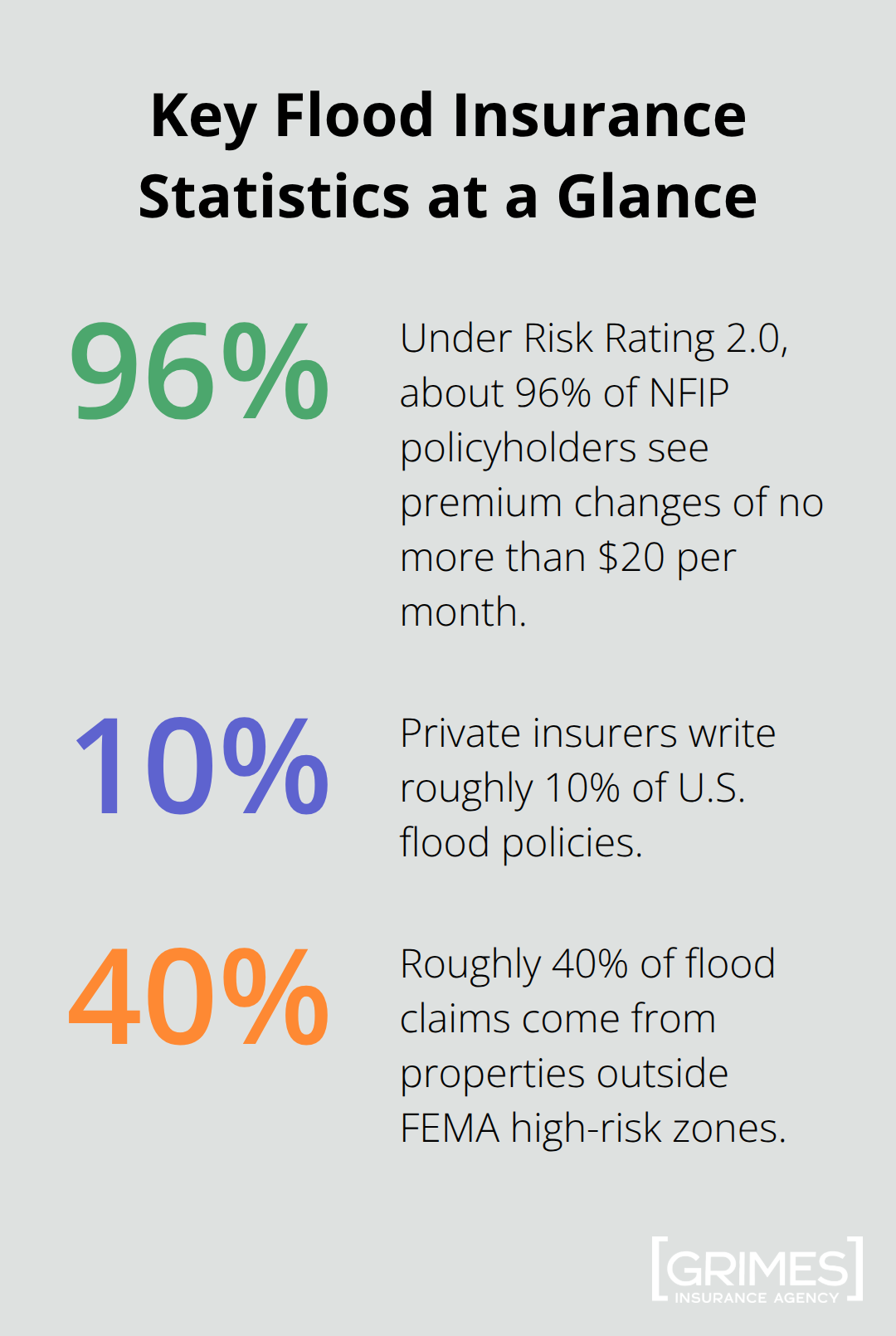

The gap is massive: less than 4% of U.S. households have flood insurance, yet more than 24 million properties face flooding risk over the next 30 years according to First Street Foundation. Even properties outside high-risk flood zones experience damage regularly. Roughly 40% of flood claims come from properties outside FEMA high-risk zones, which means your risk extends far beyond what most people assume.

Who Must Buy Flood Insurance and Who Should

If you have a federally backed mortgage in a high-risk zone, your lender requires flood insurance. If you don’t have a mortgage or live in a moderate-risk area, flood insurance remains optional, but that doesn’t mean you’re safe. Climate patterns intensify rainfall events and expand flood risk nationwide. Since 1996, 99% of U.S. counties have experienced flooding according to the Insurance Information Institute. The question isn’t whether flooding could happen to you, but when.

Two Paths to Flood Protection

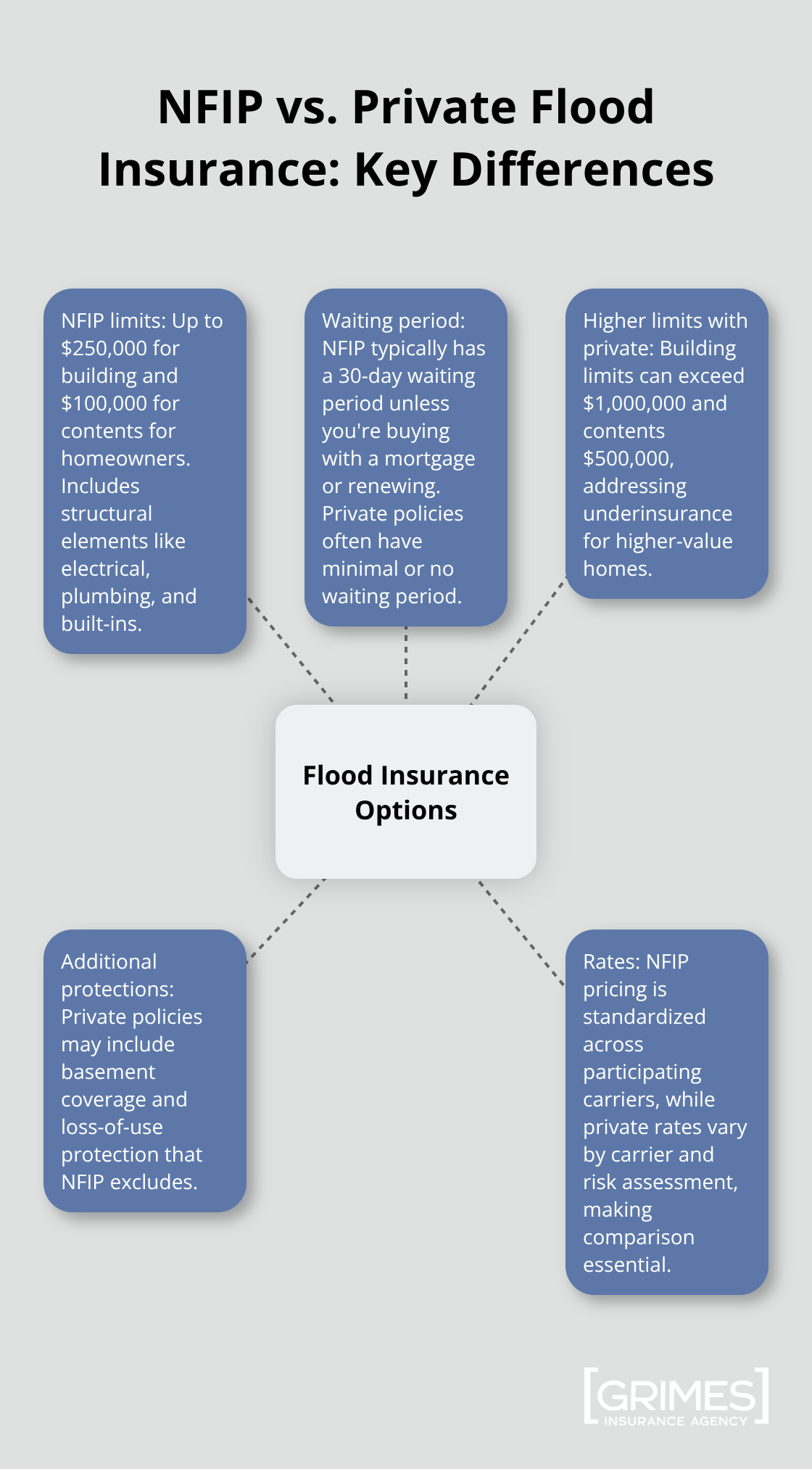

Two primary paths exist for flood protection: the National Flood Insurance Program or private flood insurance. The NFIP operates in all states and covers buildings up to $250,000 and contents up to $100,000 for homeowners. Coverage begins 30 days after purchase, though this waiting period doesn’t apply if you’re buying with a mortgage or renewing an existing policy.

Private flood insurance, now written by roughly 10% of the U.S. market, offers higher limits often exceeding $1,000,000 for building coverage and $500,000 for contents, with options like basement coverage and loss-of-use protection that NFIP excludes.

NFIP rates remain consistent across all carriers since more than 48 insurance companies partner with the program using identical pricing, so shopping around for lower NFIP rates wastes time. With private insurance, rates vary significantly by carrier, making comparison essential.

Understanding Flood Insurance Costs

Typical flood insurance costs range from $50 to $75 monthly in moderate areas, though high-risk coastal zones can exceed $1,000 annually. Your actual premium depends on distance to water, property elevation, construction type and age, coverage limits selected, deductible amount, and replacement cost. These factors determine whether NFIP or private coverage makes more financial sense for your situation. The next section explores each option in detail so you can evaluate which path aligns with your home’s specific risk profile and your budget constraints.

NFIP vs. Private Flood Insurance: Understanding Your Options

What the National Flood Insurance Program Covers

The National Flood Insurance Program protects buildings up to $250,000 and personal belongings up to $100,000 for homeowners, with structural protection that includes electrical systems, plumbing, furnaces, water heaters, built-in appliances, carpeting, and detached garages. FEMA data shows NFIP policies cost roughly $786 annually on average, though your actual premium depends on property-specific factors like elevation, flood frequency, proximity to water sources, and first-floor height under Risk Rating 2.0 pricing. About 96% of policyholders experience premium changes of no more than $20 monthly under this system, making costs relatively predictable.

The program requires your local community to participate and imposes a mandatory 30-day waiting period before coverage activates, except when you buy with a mortgage or renew an existing policy. NFIP policies do not cover basement contents, decks, swimming pools, vehicles, or additional living expenses if you’re displaced, which creates significant gaps for many homeowners.

How Private Flood Insurance Differs

Private flood insurance operates differently and often makes financial sense for your situation. Private carriers write roughly 10% of U.S. flood policies and frequently offer building limits exceeding $1,000,000 and contents coverage above $500,000, with options for basement protection and loss-of-use coverage that NFIP excludes entirely. In high-risk areas like Charleston’s AE flood zones, NFIP premiums can reach $3,000 annually or exceed $21,000 in very dangerous zones, while private quotes commonly range from $800 to $1,500 or even lower depending on your specific risk profile.

Private insurers typically have little to no waiting period and may provide faster claims processing thanks to newer technology, though NFIP has been improving its speed. Private policies often include endorsements like increased cost of compliance coverage to help you meet new building codes after a loss, adding value beyond basic protection.

The Critical Difference: Rates and Availability

Private rates vary significantly by carrier and risk assessment, making comparison essential-you absolutely should obtain quotes from at least three private providers alongside an NFIP quote before deciding. However, private flood insurance availability varies by state and risk level, and some high-risk zones may not qualify for private coverage, whereas NFIP operates nationwide and accepts all flood zones.

Since NFIP rates remain consistent across all carriers (more than 48 insurance companies partner with the program using identical pricing), shopping around for lower NFIP rates wastes your time. With private insurance, rates differ substantially between carriers, so comparison shopping directly impacts your bottom line.

Making Your Decision

Your choice between NFIP and private coverage depends on your home’s risk profile, budget, and coverage needs. High-risk coastal properties often find private insurance more affordable, while moderate-risk inland homes may benefit from NFIP’s stability and nationwide availability. The next section walks you through assessing your specific flood risk and understanding the coverage limits that match your home’s value and your financial situation.

Picking the Right Coverage for Your Home

Assess Your Flood Risk Beyond FEMA Maps

Start with your flood risk zone, but don’t stop there. FEMA flood maps provide a baseline, yet they miss inland flooding and rainfall-driven risks that affect properties outside designated high-risk areas. Use FloodSmart.gov to check your zone and obtain an initial rate estimate, then cross-reference with FloodFactor, which assigns a risk score from 1 to 10 based on flood frequency and severity specific to your property. Realtor.com and CoreLogic Flood Risk Report offer additional perspectives on your actual exposure.

Your FEMA zone classification doesn’t tell the complete story. If your home sits within a mile of a river, stream, or coastal area, or if your property experienced flooding since 2015, treat your risk as higher than maps suggest.

Gather your elevation certificate (required for new construction and helpful for rate quotes) and your home’s replacement cost estimate before obtaining quotes. These documents allow you to compare apples to apples between NFIP and private carriers.

Calculate Your True Coverage Needs

NFIP caps building coverage at $250,000 and contents at $100,000 for homeowners, with basement contents excluded entirely. If your home’s replacement cost exceeds $250,000, NFIP leaves you significantly underinsured. Private policies commonly offer $1,000,000 building limits and $500,000 contents coverage, plus basement protection.

Calculate your home’s actual replacement cost through a professional appraisal, not your purchase price or current market value-these differ substantially. High-value items like original artwork face $2,500 limits under NFIP, so if you own significant collections, private endorsements become essential.

Your deductible choice directly impacts your monthly premium. NFIP and private carriers typically offer deductibles from $1,000 to $25,000. A higher deductible reduces premiums but requires accessible savings to cover your portion during a claim. Most homeowners benefit from $5,000 deductibles unless cash reserves are extremely limited. Obtain quotes with multiple deductible options to see the actual dollar difference-sometimes the premium savings don’t justify the increased out-of-pocket risk.

Compare Multiple Quotes Systematically

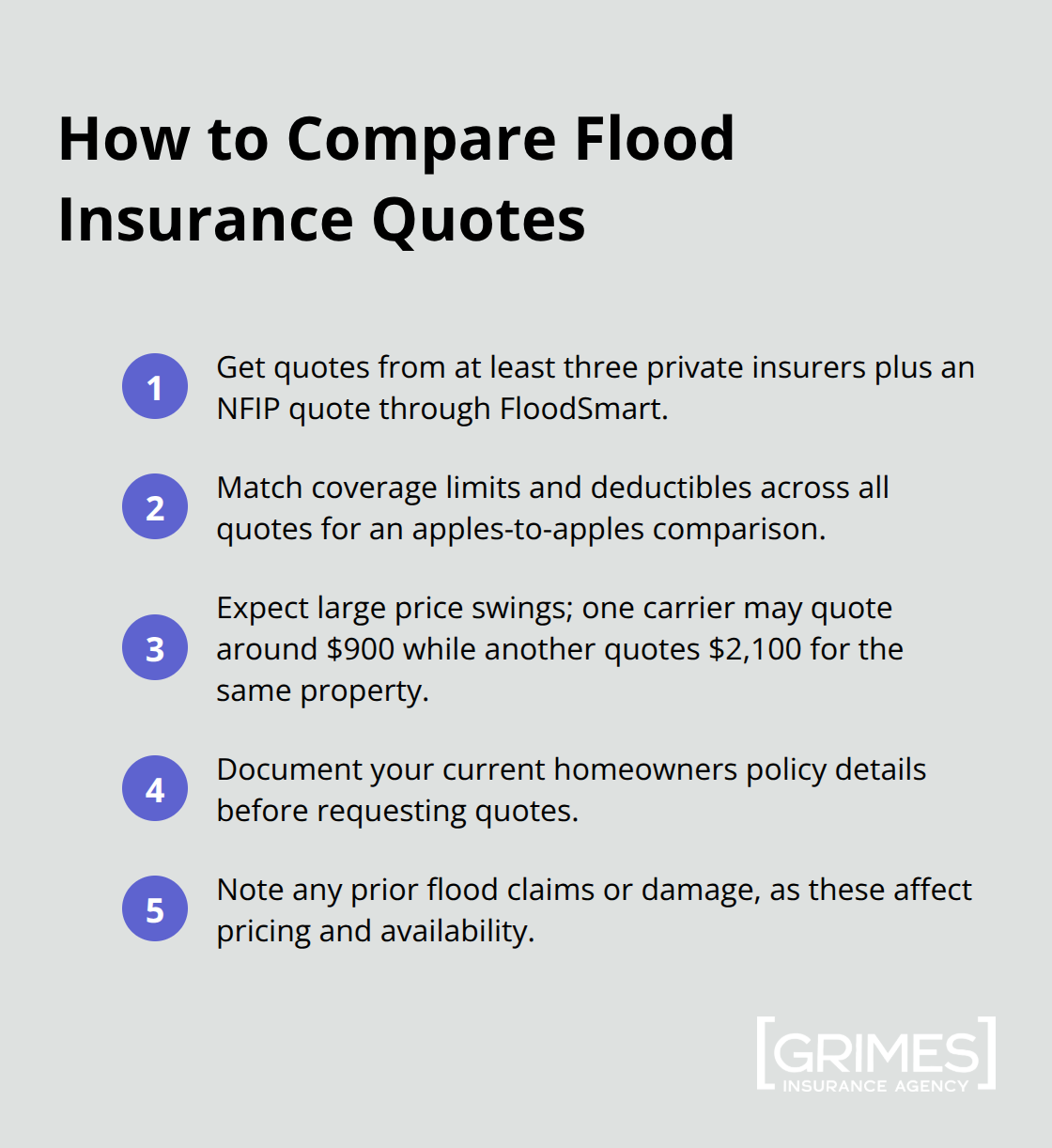

Contact at least three private insurers alongside an NFIP quote through FloodSmart. Compare identical coverage limits and deductibles across all quotes, not just premiums. Private rates vary dramatically by carrier and risk assessment methodology, so one company might quote $900 annually while another charges $2,100 for the same property. This variation makes comparison non-negotiable.

Document your current homeowners policy details and any prior flood claims or damage, as these influence pricing and availability.

Work With an Agent Who Represents Multiple Carriers

A licensed insurance agent who understands your specific property and can access multiple carriers dramatically improves your options and pricing. When speaking with any agent, ask directly whether they represent multiple private flood insurers or only NFIP. Some agents work exclusively with NFIP, which limits your access to private alternatives that might save thousands annually.

Provide your agent with your elevation certificate, property photos showing distance to water sources, and details about any past flood events within your neighborhood. These concrete details produce more accurate quotes than general address information.

Verify Coverage Activation and Lender Requirements

Confirm your lender’s requirements before purchasing-some mortgage servicers have specific approval requirements for private policies, and knowing this upfront prevents coverage gaps. Once you’ve selected a policy, verify the effective date matches your needs. NFIP imposes a 30-day waiting period unless you’re buying with a mortgage or renewing, but private policies typically have minimal or no waiting period. If you’re closing on a home purchase, private flood insurance often activates immediately, protecting you from day one.

Final Thoughts

Flood insurance coverage options in 2025 break down into two distinct paths: the National Flood Insurance Program and private flood insurance. NFIP provides nationwide availability with standardized coverage up to $250,000 for buildings and $100,000 for contents, costing roughly $786 annually on average, while private insurers offer higher limits exceeding $1,000,000 for buildings and $500,000 for contents, with faster claims processing and additional protections like basement coverage that NFIP excludes. Your choice depends entirely on your home’s specific risk profile, replacement cost, and budget constraints.

Your standard homeowners policy leaves you completely unprotected against flood damage-one inch of floodwater causes up to $25,000 in damage according to FEMA, yet fewer than 4% of American households carry flood insurance despite more than 24 million properties facing flooding risk over the next 30 years. Start by assessing your actual flood risk using FloodSmart.gov, FloodFactor, and local flood maps, then gather your elevation certificate and home replacement cost estimate. Obtain quotes from at least three private carriers alongside an NFIP quote through FloodSmart, comparing identical coverage limits and deductibles across all options, since private rates vary dramatically between carriers.

We at Grimes Insurance Agency help homeowners navigate flood insurance coverage options in 2025 with access to multiple carriers and personalized guidance based on your property’s unique characteristics. Our team understands that flood risk extends far beyond FEMA maps and that your coverage needs depend on factors like elevation, proximity to water, and replacement cost. Contact us today to discuss your flood insurance needs and protect what matters most.