Navigating the Home Insurance Claims Process in 2025: A Step-by-Step Guide

Filing a home insurance claim can feel overwhelming, especially when you’re dealing with damage to your property. We at Grimes Insurance Agency know that understanding each step of the process makes a real difference in getting the settlement you deserve.

This guide walks you through navigating the home insurance claims process in 2025, from reviewing your policy to negotiating with adjusters. You’ll learn exactly what to do when damage happens.

What’s Actually Covered in Your Home Insurance Policy

Read Your Policy Before You Need It

Your home insurance policy is a contract with specific boundaries about what it covers and what it doesn’t. Most homeowners avoid reading their policies until they file a claim, which is exactly when confusion hits hardest. You should review your policy document before damage occurs so you understand what protection you actually have. Start by locating your declarations page, which lists your coverage limits for dwelling, personal property, liability, and additional living expenses. Your dwelling coverage pays to repair or rebuild your home’s structure, while personal property coverage handles your belongings. Homeowners are underinsured for rebuilding their homes, meaning many people discover their coverage limits fall short when they need them most.

Know Your Coverage Limits and Deductibles

Check your deductible amount, which is what you pay out of pocket before insurance kicks in. A higher deductible lowers your premium, but it also means you’ll pay more when damage happens. If your home is worth $400,000, your dwelling coverage should reflect that current replacement cost, not the price you paid ten years ago. You also need to understand whether you have replacement cost coverage, which pays to replace damaged items with new ones, or actual cash value coverage, which deducts depreciation. Replacement cost coverage costs more but pays significantly better when you file a claim.

Identify What Your Policy Excludes

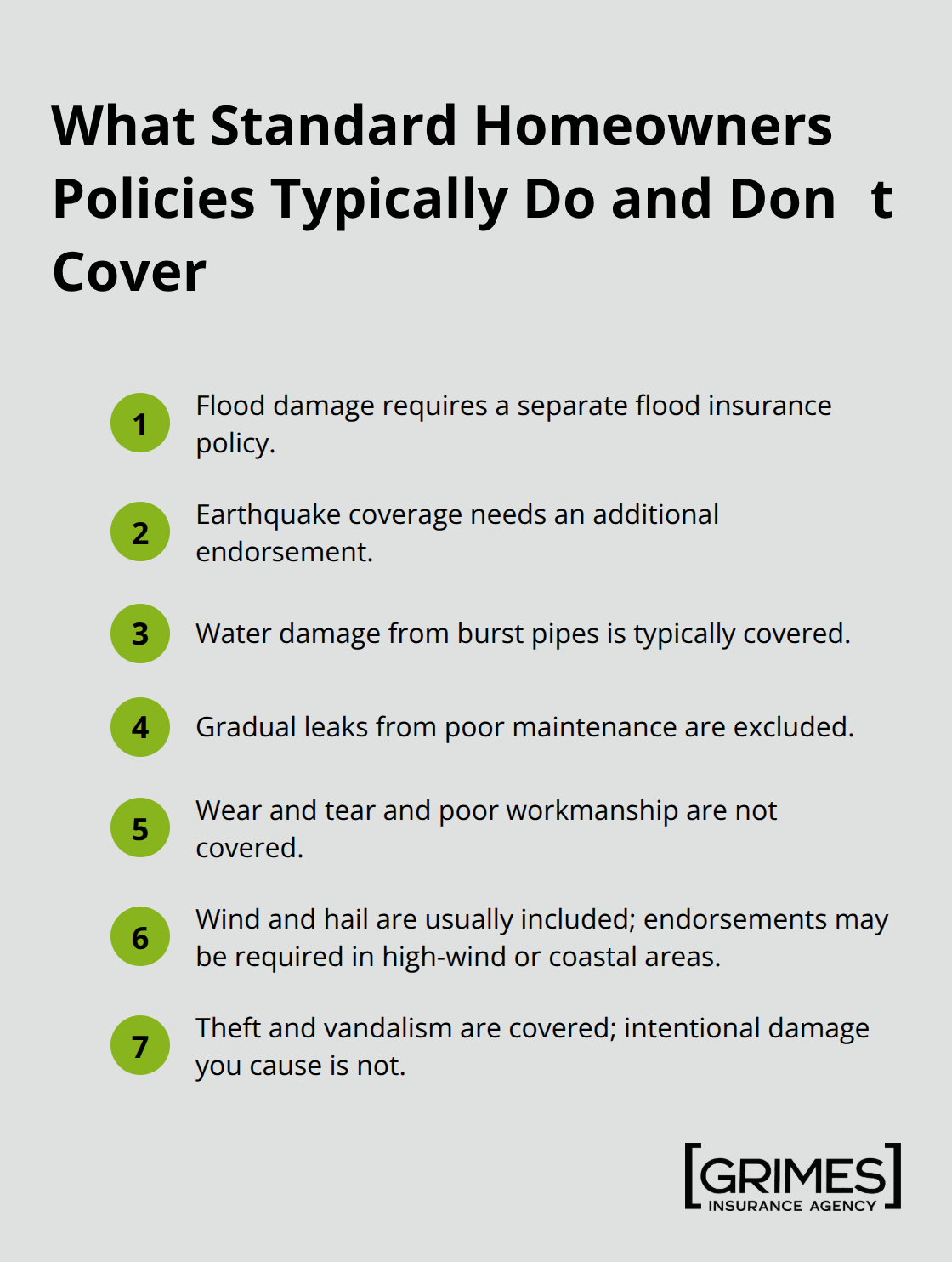

Standard homeowners insurance doesn’t cover flood damage, which requires a separate flood insurance policy through the National Flood Insurance Program or private carriers. Earthquake coverage is also excluded and requires an additional endorsement. Water damage from burst pipes is typically covered, but gradual leaks from poor maintenance are not.

Damage from lack of maintenance, poor workmanship, or normal wear and tear falls outside coverage. Wind and hail damage is usually included in standard policies, but some insurers in coastal or high-wind areas offer wind coverage as an optional endorsement (check with your agent about your specific location). Theft and vandalism are covered under most policies, but intentional damage you cause yourself is not.

Understand Business and Special Coverage Gaps

If you operate a business from your home, business property and liability aren’t covered under a standard homeowners policy. You’ll need a separate business policy to protect that income and equipment. These gaps matter because they determine what happens when disaster strikes. Contact your agent to clarify any coverage gaps before damage occurs, because waiting until after an incident leaves you vulnerable to claim denials. Once you understand exactly what your policy covers, you’re ready to take the next critical step: knowing how to document and report damage properly.

How to Document and Report Damage the Right Way

Photograph and Video Everything Immediately

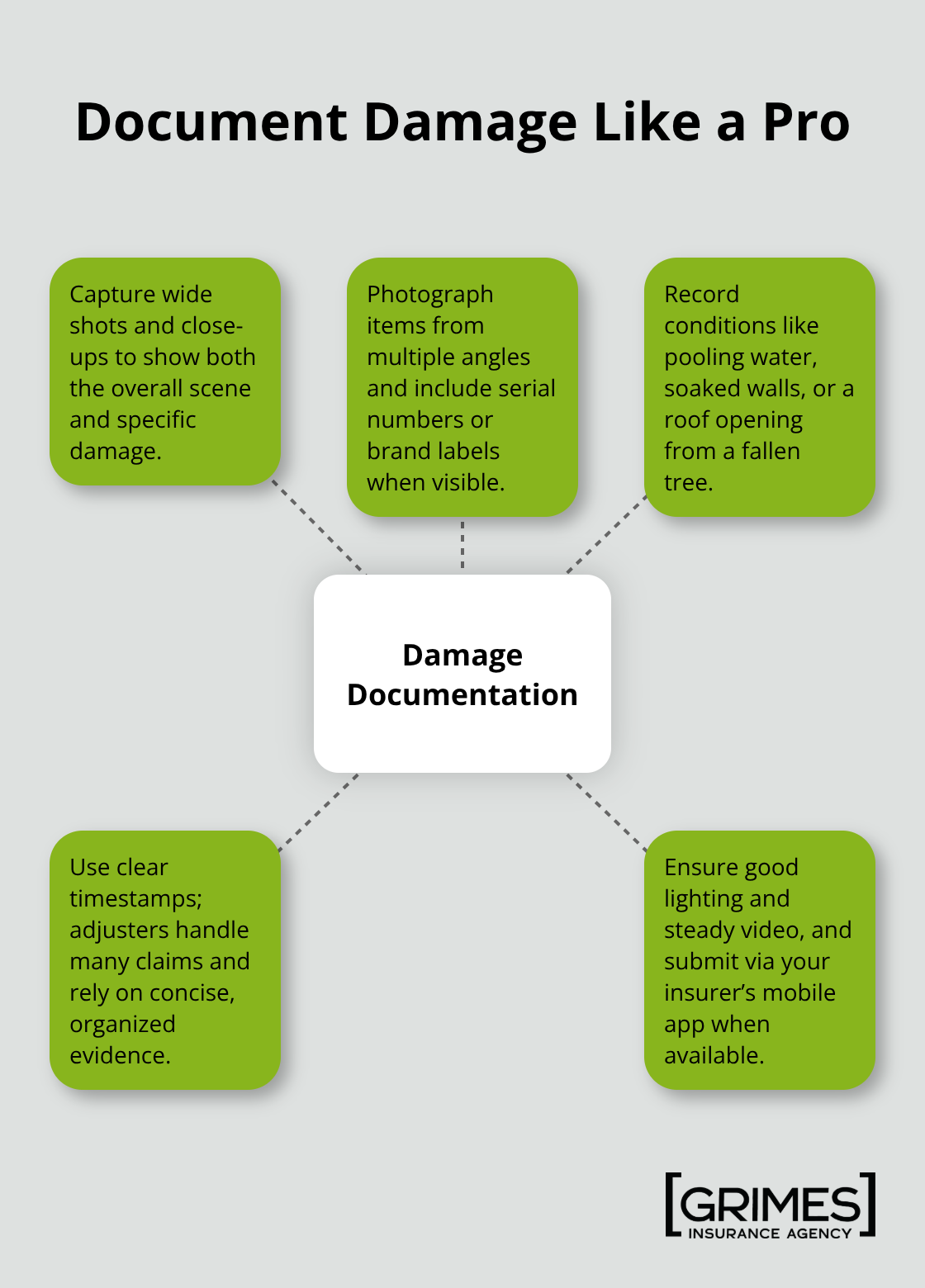

You must photograph and video damage immediately, before you touch anything or start cleanup. Take wide shots that show the overall damage, then close-ups of specific areas where you can see the destruction clearly. Photograph damaged items from multiple angles and include shots of serial numbers or brand labels when visible. If pipes burst, capture water pooling on floors or soaking into walls. If a tree crashes through your roof, photograph the hole, the tree, and the surrounding area. Insurance adjusters receive thousands of claims yearly, and clear documentation with timestamps helps them process yours faster. Phone videos work just fine, but you need adequate lighting and steady hands to hold your device. Many adjusters now accept photos and videos submitted through mobile apps, which speeds up the initial assessment phase considerably.

Report the Damage Within 24 to 48 hours

You should contact your insurance company within 24 to 48 hours of discovering damage, not days later. The Insurance Information Institute recommends reporting promptly to prevent coverage complications and start the claims process immediately. When you call, have your policy number ready and describe what happened, where the damage occurred, and when you discovered it. Provide specific details like the cause of damage (storm, fire, theft), the date and time it occurred, and whether anyone was injured. You should not speculate about the cause or guess at repair costs. Stick to facts you observed directly.

Explain Temporary Repairs You’ve Made

The representative will ask if you have made temporary repairs to prevent further damage, which most policies actually require. If a pipe burst and water is still running, you should turn off the water immediately. This temporary repair protects your home and does not harm your claim. The adjuster will want to see your documentation before settlement, so you should organize those photos and videos by room or damage type to make their job straightforward. Your clear reporting and organized evidence set the stage for what happens next: the adjuster’s assessment of your claim and the path toward fair compensation.

Working with Adjusters and Getting Fair Settlements

Prepare Your Documentation Before the Adjuster Arrives

An adjuster will inspect your property and estimate repair costs, but this estimate isn’t final and isn’t always accurate. Organize your documentation by room and damage type before the adjuster arrives. Create a simple spreadsheet listing each damaged item, its replacement cost, and the photo evidence you have. Include receipts, credit card statements, or online purchase confirmations for high-value items like electronics, furniture, or appliances. The adjuster will spend 30 minutes to two hours at your property, so having everything ready prevents important damage from being overlooked.

Understand What Happens During the Inspection

Take notes during the inspection, including what the adjuster photographs, measures, and comments about. Ask the adjuster to explain their methodology for calculating repair costs and which items they’re including or excluding. Most adjusters work on commission based on claim volume, not claim accuracy, which means some rush through inspections without catching everything. If your home has structural damage, foundation issues, or hidden water damage behind walls, the adjuster’s initial walkthrough often misses these problems. Request a detailed written estimate before they leave your property, not days later via email.

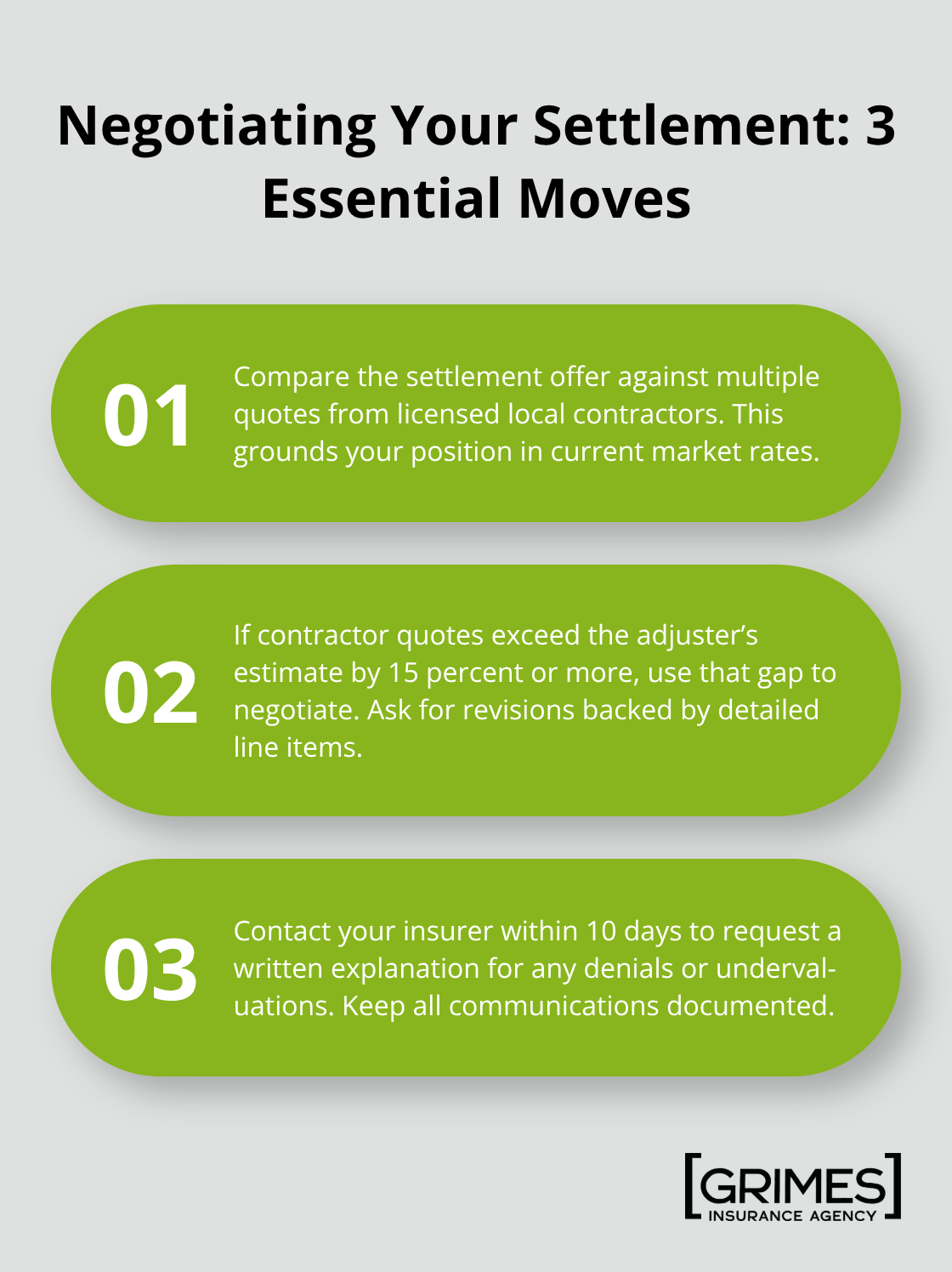

Compare the Settlement Against Local Contractor Quotes

When the settlement offer arrives, compare it against quotes you’ve obtained from local contractors. If repair quotes from licensed contractors in your area exceed the adjuster’s estimate by 15 percent or more, that’s grounds for negotiation. Contact your insurance company within 10 days of receiving the settlement offer and request a detailed explanation for any items they denied or undervalued.

Negotiate Disputed Items or File a Complaint

If you disagree with specific line items, provide your contractor quotes and explain why the adjuster’s estimate is unrealistic for your local market. Some insurers will send a second adjuster to reassess, while others will work with you on specific disputed items. If the insurer refuses to budge and you believe the settlement is genuinely unfair, file a complaint with the Texas Department of Licensing and Regulation, which oversees insurance practices in Texas. This formal complaint often prompts insurers to reconsider their position because regulatory scrutiny is expensive. Alternatively, you can hire an independent adjuster or public adjuster to advocate on your behalf, though they typically charge 5 to 10 percent of any additional settlement they recover (this cost is worth it when the gap between the insurer’s offer and actual repair costs is substantial).

Final Thoughts

Filing a home insurance claim doesn’t have to derail your life. The key to navigating the home insurance claims process in 2025 is preparation before damage happens and organization when it does. Review your policy now, understand your coverage limits and exclusions, and keep your documentation organized. When damage occurs, photograph everything immediately, report it within 24 to 48 hours, and gather contractor quotes before accepting any settlement offer.

Don’t accept the first adjuster estimate as final, especially if local contractors quote significantly higher repair costs. Compare their numbers against your documentation and negotiate disputed items with confidence. After your claim resolves, review what happened and whether your coverage still matches your home’s current value (rebuilding costs have increased substantially, and your policy limits from five years ago may no longer reflect what it actually costs to repair or rebuild your home today).

We at Grimes Insurance Agency understand that navigating home insurance claims can be frustrating, which is why we’re here to help before and after damage strikes. Our team works with multiple carriers to find coverage that actually protects what matters to you, and we can walk you through your options and answer questions about what your policy covers. Contact Grimes Insurance Agency today to make sure you’re protected for whatever comes next.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation