Flood Insurance Benefits for Texas Homeowners: Why You Should Consider It

Texas homeowners face a harsh reality: standard insurance policies don’t cover flood damage, leaving families vulnerable to devastating financial losses. Flooding is the costliest natural disaster in the United States, and Texas experiences it regularly through hurricanes and heavy rainfall.

At Grimes Insurance Agency, we believe flood insurance benefits for Texas homeowners go far beyond basic protection. This coverage shields your property, your belongings, and your financial stability when water damage strikes.

Why Your Homeowners Policy Won’t Protect You From Floods

Standard homeowners insurance policies contain explicit exclusions for flood damage, and this gap leaves Texas families exposed to catastrophic financial loss. Water damage from external flooding falls outside these policies, regardless of your premium level or coverage limits. Homeowners often assume their comprehensive coverage includes all water-related damage, only to discover during a claim that flood damage remains unprotected. This misunderstanding has cost thousands of Texas families hundreds of thousands of dollars in repairs after storms and heavy rainfall events.

The Real Cost of Flooding in Texas

Flooding ranks as the costliest natural disaster in the United States, causing an average of $54 billion in annual damage according to FEMA data. Texas faces particular vulnerability because the state sits in multiple flood corridors, from coastal regions prone to hurricane surge to inland Flash Flood Alley across Central and North Texas. In 2023 alone, Texas experienced multiple severe flooding events that displaced families and destroyed homes.

Even a single inch of floodwater causes $25,000 or more in damage to a home, and most properties lack the coverage to address these costs. When homeowners file claims expecting their standard policy to cover flood damage, they learn too late that they remain personally liable for every dollar of recovery. This financial shock forces families to deplete savings, take loans, or abandon their homes entirely.

Why Insurance Companies Exclude Flood Coverage

Insurance companies exclude flood coverage from standard homeowners policies because flood risk is geographically concentrated, highly predictable, and extremely expensive to cover. This economic reality led Congress to establish the National Flood Insurance Program, a government-backed solution designed specifically for flood protection.

Relying on federal disaster assistance cannot substitute for insurance. Disaster aid typically comes as a loan that homeowners must repay, and it rarely covers full reconstruction costs. The federal government has no obligation to provide assistance, and homeowners who receive aid often spend years paying back what they received.

What Your Homeowners Policy Actually Covers

Your homeowners policy protects against fire, theft, and weather events like hail and wind. Water entering your home from external sources (flooding, storm surge, or heavy rainfall) falls into an entirely different category that requires separate protection. This distinction means your standard policy leaves a critical gap in your financial security when water damage strikes your property.

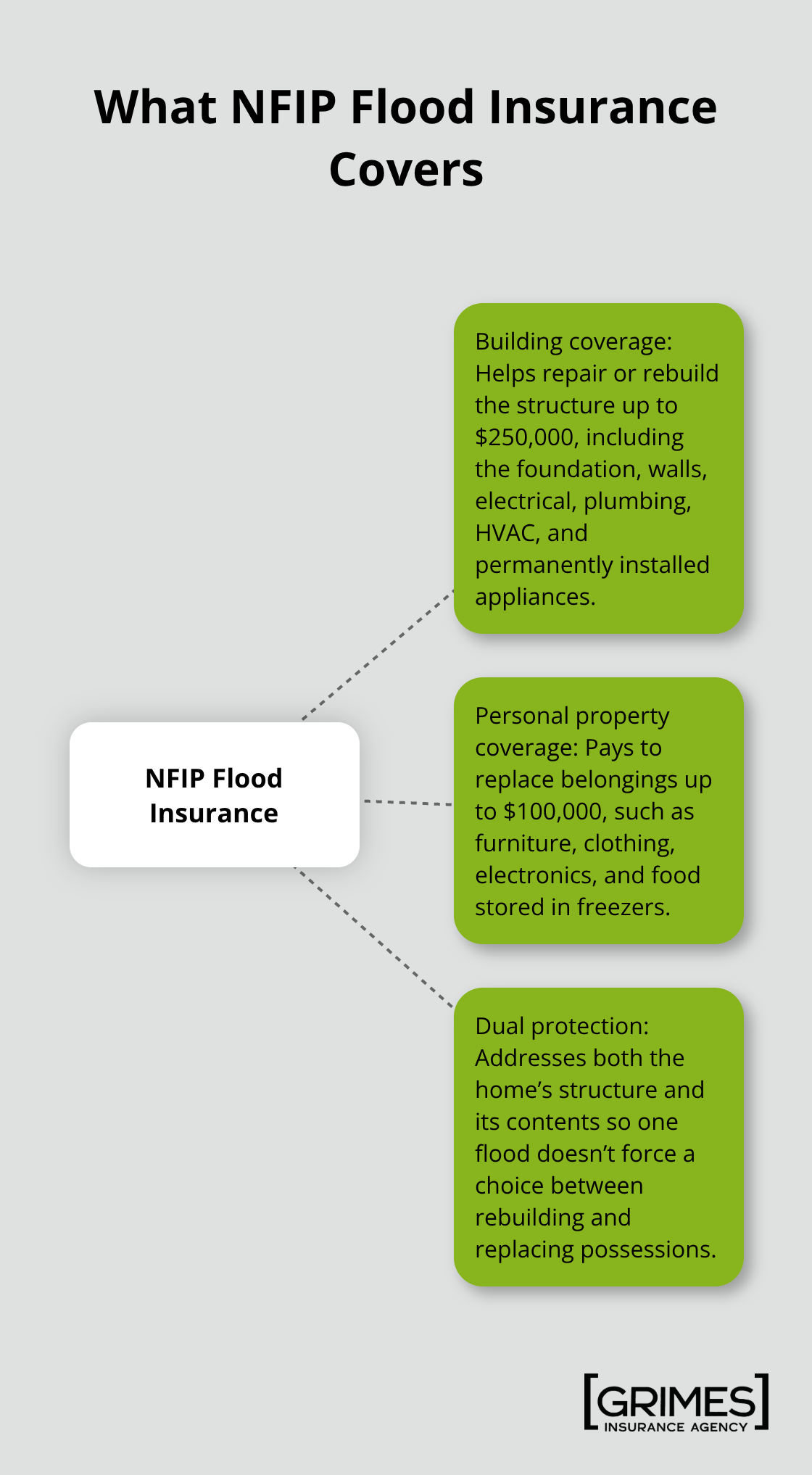

What Flood Insurance Actually Covers

Flood insurance from the National Flood Insurance Program covers two distinct categories of loss that your standard homeowners policy completely excludes. Building coverage protects the structure itself up to $250,000 for single-family homes, including foundations, walls, electrical systems, plumbing, HVAC equipment, and permanently installed appliances. Personal property coverage extends up to $100,000 for your belongings like furniture, clothing, electronics, and food in freezers. This dual protection addresses both the physical structure and the contents inside it, so a single flood event won’t force you to choose between rebuilding your home or replacing your possessions.

The Math Behind Flood Damage Costs

Most Texas homes experience significant water penetration during major flood events, with a typical basement flood reaching five feet and multiplying damage exponentially. Without flood insurance, homeowners absorb these costs entirely through savings, loans, or selling assets. With coverage in place, your policy pays for repairs and replacements according to your chosen limits, protecting your financial foundation when water strikes. The average Texas homeowner pays between $700 and $1,200 annually for NFIP flood insurance in low-to-moderate risk areas, yet a single flood event can cost ten to fifty times that amount in uninsured losses.

Avoiding the Underinsurance Trap

Many homeowners purchase flood insurance with inadequate limits, assuming their $250,000 building coverage will suffice without calculating their actual replacement costs. A home worth $450,000 on the real estate market might require $350,000 or more to fully rebuild after a flood, leaving a $100,000 gap that the homeowner must cover personally. Calculate your home’s full replacement cost, not its market value, when determining flood coverage limits. If your replacement cost exceeds the NFIP maximum, private flood insurance options provide higher limits and additional protections. Update your coverage annually and adjust it after renovations to maintain adequate protection as your home’s value changes.

Coverage Gaps That Catch Homeowners Off Guard

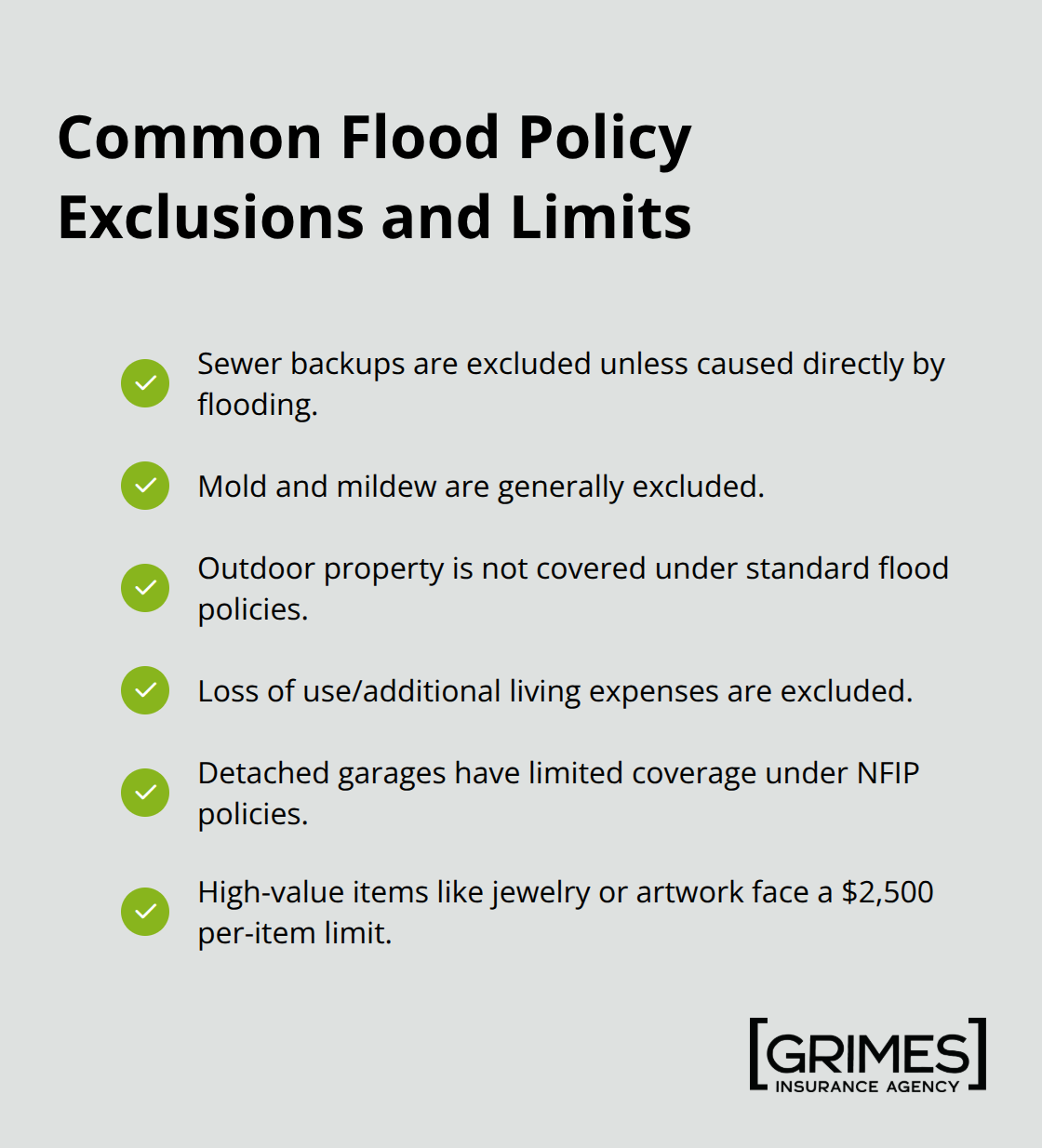

Flood policies contain specific exclusions that homeowners often overlook when purchasing coverage. Sewer backups, mold and mildew, outdoor property, and loss of use fall outside standard flood insurance protection (unless the sewer backup results directly from flooding). Detached garages receive limited coverage under NFIP policies, and valuables like jewelry or artwork face per-item limits of $2,500.

Understanding these exclusions prevents the shock of discovering your claim won’t cover certain damages after a flood strikes your property.

Planning Ahead for Maximum Protection

Most flood policies include a 30-day waiting period before coverage becomes active, which means purchasing insurance during storm season often arrives too late. Homeowners who wait until heavy rain threatens their area cannot activate coverage immediately when they need it most. Elevation certificates and your property’s flood history directly affect your premiums, so reviewing these factors before purchasing coverage helps you understand your actual costs. Properties built above the Base Flood Elevation or those with flood mitigation measures in place qualify for reduced premiums, making improvements to your home’s flood resistance financially worthwhile.

Your flood coverage decisions today determine whether you recover quickly or face years of financial hardship after the next major storm. Understanding what your policy covers and what it excludes allows you to make informed choices about your protection level and budget.

Getting Flood Insurance in Texas

Start by checking your property’s flood zone on the FEMA Flood Map Service Center at no cost. Enter your address and review whether you fall into a high-risk zone (SFHA), moderate-risk area, or low-risk zone. This step matters because your zone determines whether your lender requires flood insurance and influences your premium significantly.

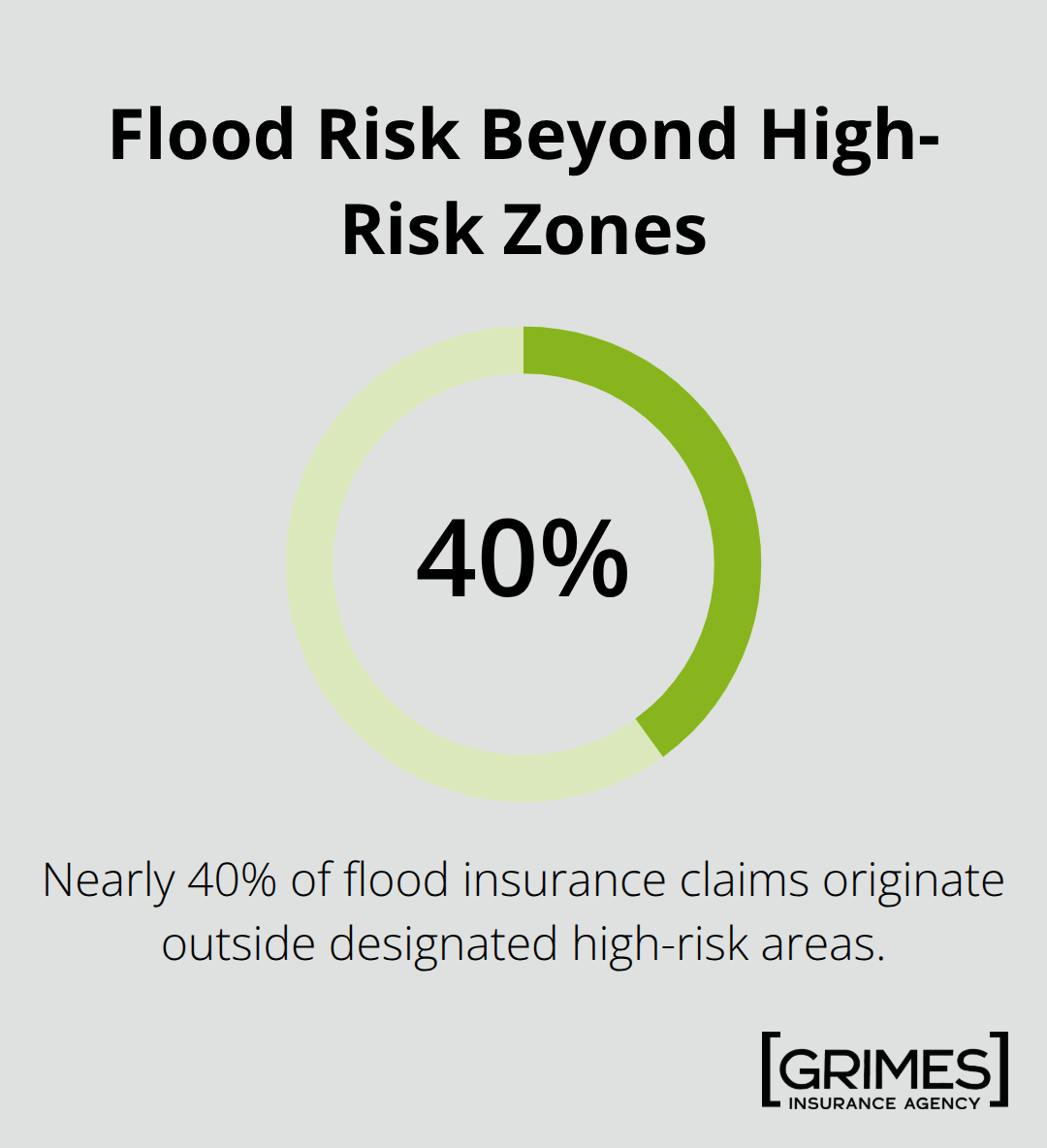

Properties in high-risk zones face mandatory flood insurance if you have a mortgage, but nearly 40 percent of flood claims originate outside these designated high-risk areas, so moderate and low-risk property owners should treat flood coverage as essential rather than optional.

After identifying your zone, contact your current homeowners insurance agent to request flood insurance quotes. Most major insurers participate in the National Flood Insurance Program and can bind coverage within days. If your agent cannot provide flood quotes, call 877-336-2627 for assistance locating a participating agent. Request quotes from multiple carriers rather than accepting the first option available. Premiums vary considerably between NFIP policies and private flood insurers, with NFIP coverage in low-to-moderate risk areas typically ranging from $700 to $1,200 annually according to industry data, while private policies may offer different pricing structures and higher limits. Your elevation relative to the Base Flood Elevation, proximity to waterways, foundation type, and construction materials all influence your final premium, so obtaining three to five quotes reveals the true cost range for your specific property.

Understanding Premium Factors and Cost Reduction

An elevation certificate shows your home’s elevation compared to the Base Flood Elevation and directly impacts your premium. Homes built above the Base Flood Elevation qualify for substantially lower rates, sometimes reducing annual costs by 30 percent or more. If you have not obtained an elevation certificate, request one from a surveyor before comparing quotes because this document often produces significant savings. Flood mitigation improvements like proper grading, elevated utilities, flood vents, or improved drainage systems can reduce your premiums even without raising your home’s elevation. These physical improvements cost between $1,000 and $5,000 in most cases but can lower annual insurance costs by 10 to 15 percent, meaning the investment pays for itself within five to ten years.

Calculating Your Coverage Needs

When comparing coverage limits, calculate your home’s full replacement cost rather than its market value. A $500,000 home on the real estate market may cost $350,000 to rebuild after flood damage, or it may cost $400,000 depending on foundation type and local labor costs. Underestimating replacement cost leaves you personally responsible for the gap between your coverage limit and actual reconstruction expenses. Document your home’s contents through photos and receipts to support personal property claims if flooding damages your belongings.

Timing Your Purchase and Maintaining Coverage

The 30-day waiting period built into flood policies creates urgency around timing your purchase. Policies become effective 30 days after you complete the application, which means waiting until June to purchase coverage before hurricane season leaves you unprotected until July. Purchase flood insurance well before severe weather threatens your area, ideally during spring for summer and fall storm seasons. Review your coverage annually and adjust limits after home renovations or major improvements. A kitchen renovation adding $50,000 in value requires a corresponding increase in your flood insurance limits to maintain adequate protection.

Final Thoughts

Flood insurance benefits for Texas homeowners protect your home’s structure, your personal belongings, and your financial stability when water damage strikes. Without coverage, a single flood event costs tens of thousands of dollars in uninsured losses, depleting savings and forcing difficult choices about your family’s future. Nearly 40 percent of flood insurance claims originate outside high-risk zones, meaning moderate and low-risk properties experience significant flooding regularly.

Check your property’s flood zone on the FEMA Flood Map Service Center, then contact an insurance agent to obtain quotes from multiple carriers. Compare coverage limits, understand your replacement costs, and explore your flood insurance options well before storm season arrives. The 30-day waiting period means waiting until heavy rain threatens your area leaves you unprotected when you need coverage most.

We at Grimes Insurance Agency understand the specific flood risks Texas homeowners face and provide access to multiple carriers so you receive the best protection and pricing for your situation. Our team specializes in comprehensive coverage options and can help you navigate flood insurance requirements, compare NFIP and private policies, and tailor protection to your actual risk and budget. Contact us today to safeguard what matters most to your family.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation