Understanding Commercial Property Risks in 2026: What Every Investor Should Know

Commercial property investing comes with real financial exposure. Interest rates, tenant vacancies, and climate risks are reshaping the landscape in 2026.

At Grimes Insurance Agency, we help investors understand commercial property risks and build protection strategies that actually work. This guide covers the market threats you face, the insurance solutions available, and the practical steps to safeguard your assets.

What’s Really Driving Commercial Property Risk in 2026

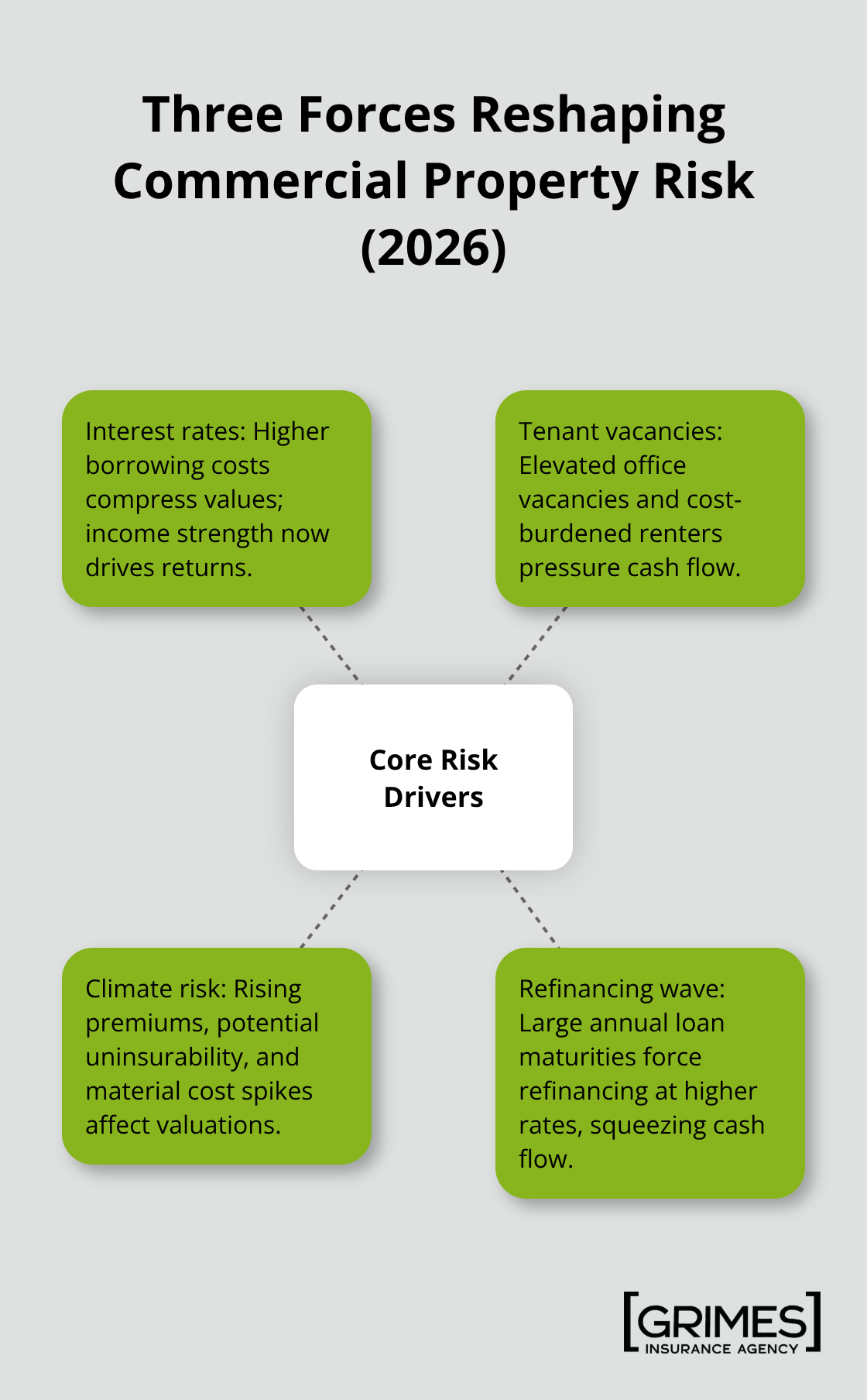

Interest Rates Compress Property Values

The federal funds rate sitting around 3.64% as of December 2025 has fundamentally changed the economics of commercial real estate investing. Higher borrowing costs directly compress property values because investors now demand stronger income streams to justify their capital. According to JPMorgan Chase’s Commercial Real Estate Outlook 2026, cap rate compression has ended, meaning future returns depend almost entirely on strong income performance rather than financial engineering or appreciation. This shift is brutal for investors who counted on rising valuations to offset weak operational performance. Properties that generate solid net operating income hold their value; those that don’t face downward pressure.

The Counselors of Real Estate warns that over 950 billion dollars in loan maturities hit annually through 2027, which means thousands of commercial property owners face refinancing at rates significantly higher than their original terms. If you own a property with a loan maturing in 2026 or 2027, refinancing costs could consume 20 to 40 percent of your annual cash flow depending on how much rates have moved since you originated the debt.

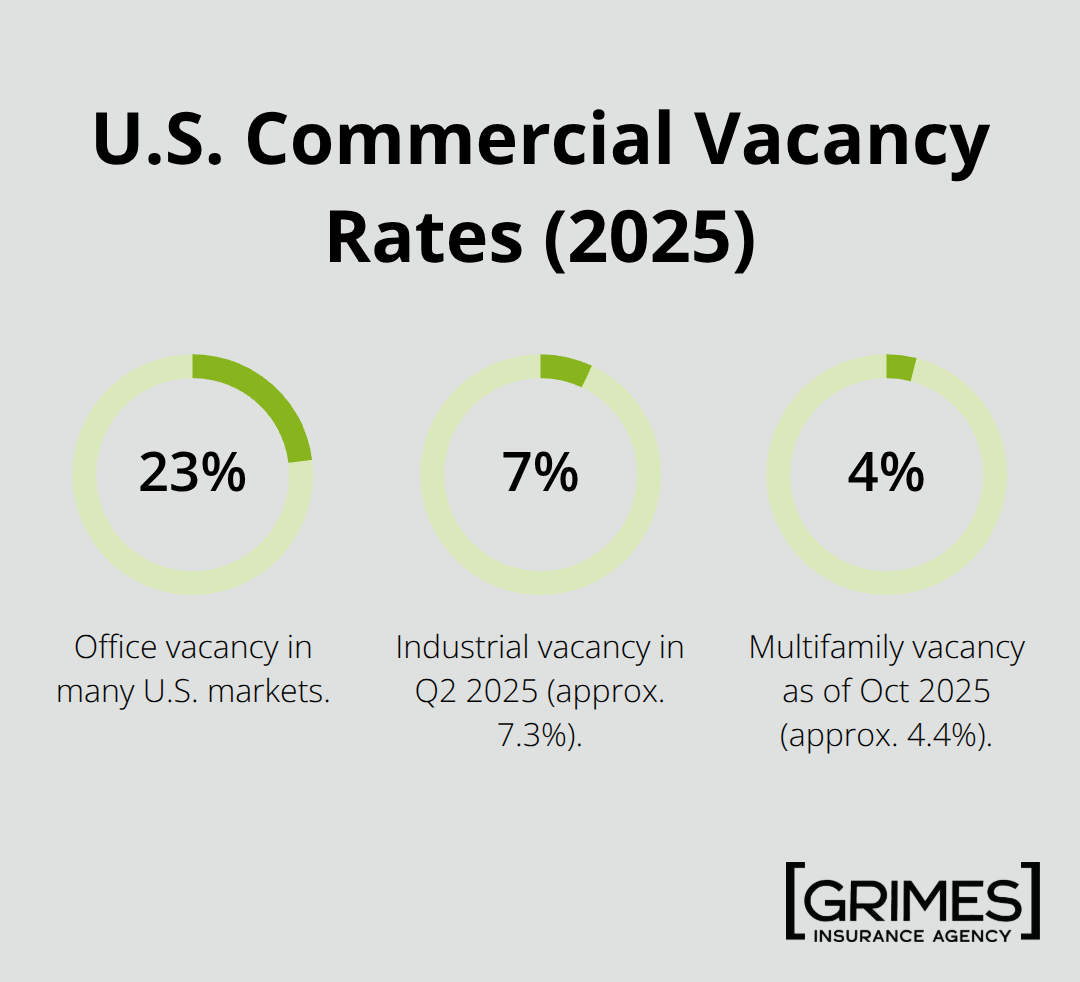

Tenant Vacancies Rise Across Markets

Tenant vacancies are rising across most property types, and this is where economic uncertainty hits hardest. Office vacancy hovers around 23 percent in many markets as remote work persists, but industrial space remains tight at approximately 7.3 percent vacancy in Q2 2025, according to market data. Multifamily vacancy sits around 4.4 percent as of October 2025, but affordability pressures mean renters are cost-burdened, making them more likely to default or move when circumstances change. The National Low Income Housing Coalition reports that over 22 million renter households are cost-burdened, which creates systemic fragility in your tenant base.

Climate Risk Moves From Theory to Reality

Climate risk has moved from theoretical to concrete. Building material costs have already risen 50 percent for steel, aluminum, and copper due to tariffs, and reciprocal rates on other materials could further damage project economics according to JPMorgan analysis. Properties in flood zones, hurricane corridors, and wildfire-prone areas face higher insurance premiums, potential uninsurability in extreme cases, and reduced resale appeal. Investors who ignore climate exposure are essentially betting against insurance markets and property valuations in the regions most affected by severe weather.

The smartest investors conduct continuous risk assessments that account for infrastructure, climate, financial, and operational risks to guide buy and sell decisions. This means stress-testing your portfolio around refinancing scenarios, calculating what happens if your tenants face economic pressure, and honestly assessing whether your properties can weather the physical impacts of climate change in their specific locations. Understanding these three risk drivers sets the foundation for selecting the right insurance protections and coverage strategies.

What Insurance Actually Protects Your Commercial Property

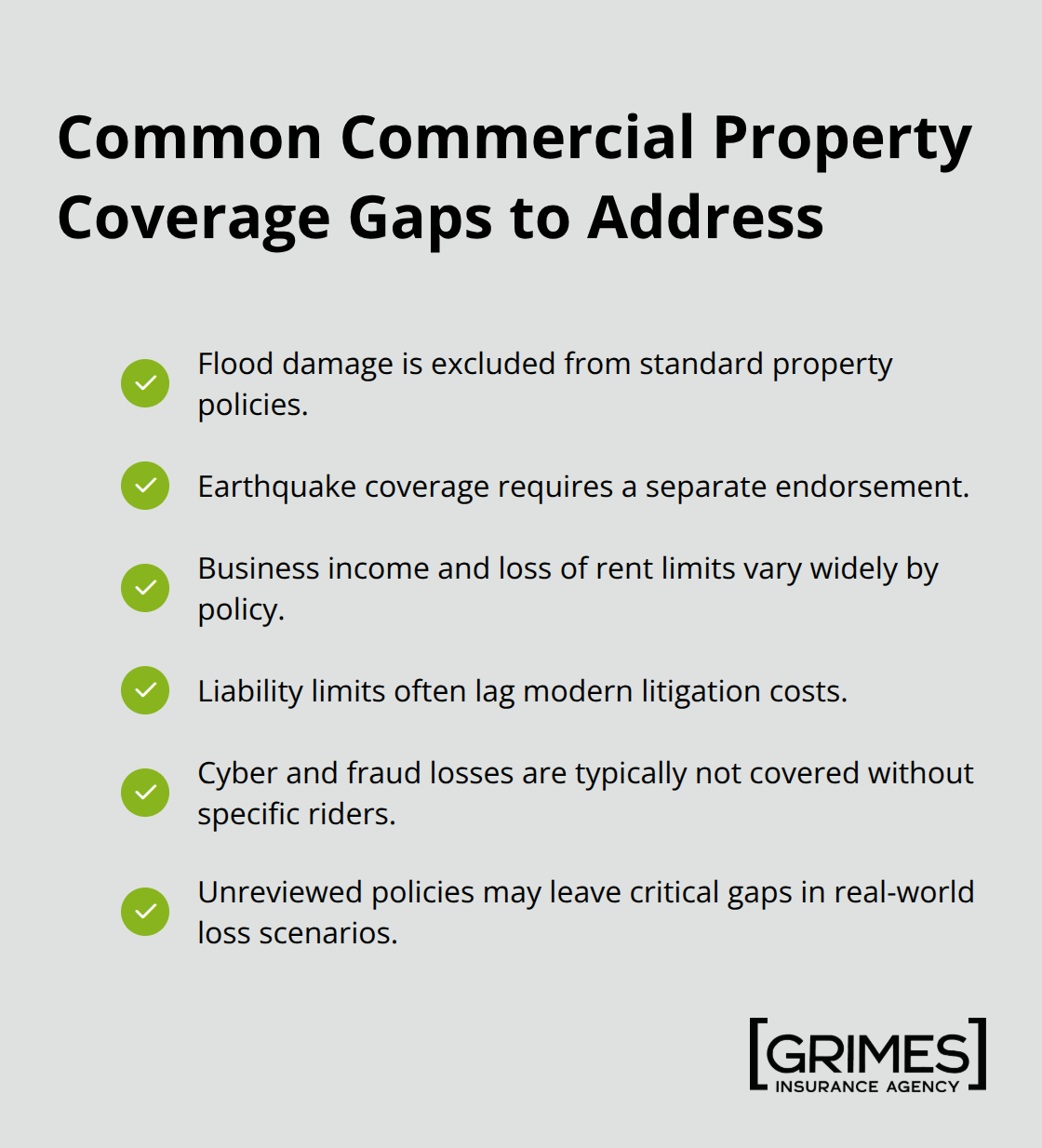

The Coverage Gap That Costs Investors Money

Most commercial property investors carry standard coverage and assume they’re protected. They’re not. The gap between what policies actually cover and what investors think they cover is where financial disasters happen. Standard commercial property insurance covers the building structure and basic contents against named perils like fire, wind, and theft. But it typically excludes flood damage entirely, which is catastrophic given that flood losses now account for a significant portion of commercial property claims in vulnerable areas. Earthquake coverage requires a separate endorsement. Loss of income protection varies wildly between policies. Liability coverage limits often fall short of modern litigation costs. The 2025 AFP Payments Fraud and Control Survey found that 79 percent of organizations faced attempted or actual payment fraud, yet most commercial property policies don’t cover cyber-related losses or fraud unless specifically added.

Your property might be fully insured for fire but completely exposed to flood, cyber liability, or business interruption coverage.

Identify Your Actual Exposure

Assessing your actual insurance needs requires brutally honest answers about your specific exposure. If your property sits in a high-risk flood zone, standard coverage is worthless-you need separate flood insurance, period. If you own multifamily or retail with significant tenant operations, business interruption coverage should cover your lost rent for at least six months based on current vacancy trends and tenant cost-burden data. If you refinance in 2026, your lender will require updated valuations and appraisals, which should trigger a full insurance review because property values shift and coverage limits often lag behind.

Work With an Independent Agent

Independent agents have access to multiple carriers and can layer specialized coverage that captive agents cannot offer. They can benchmark your rates against actual market comparables rather than accepting the first quote. When you work with an independent agent, you gain someone invested in protecting your long-term interests because your retention matters to their business, not just the initial commission. The agent should ask detailed questions about your property condition, tenant profile, location risks, and financial capacity to absorb losses. If an agent doesn’t ask these questions, find a different agent.

Improve Your Rates Through Risk Management

Rates improve when coverage is properly structured because insurers reward disciplined risk management with better pricing. Properties with documented maintenance records, security systems, and clear loss prevention protocols attract lower premiums from carriers who trust the underlying risk is genuinely lower. This connection between operational discipline and insurance costs means that the steps you take to protect your property also protect your bottom line. As you strengthen your risk profile, your insurance costs decline-and your property becomes more attractive to future buyers or refinancing lenders. The next section covers the specific risk management strategies that reduce both your exposure and your insurance premiums.

How to Reduce Your Risk and Lower Insurance Costs

Document Your Property Condition and Maintenance

Insurers price risk based on asset condition, so properties with documented inspections and preventive maintenance cost less to insure than identical properties with deferred maintenance. Start with a professional property condition assessment that identifies structural deficiencies, mechanical system age, roof condition, and deferred maintenance items. This assessment becomes your baseline for future comparisons.

Schedule inspections every quarter minimum, more frequently if your property exceeds 30 years old or sits in harsh climates. Document everything: roof inspections, HVAC servicing, plumbing checks, electrical panel reviews. This documentation proves to insurers that you actively manage risk rather than react to emergencies. Properties with documented maintenance histories see insurance rate reductions because the underlying risk is genuinely lower. The discipline also reduces actual losses because you catch problems before they become catastrophic claims.

Spread Investments Across Multiple Regions

Geographic concentration amplifies your exposure to rate volatility, tenant shocks, and local economic downturns. If you own five properties and four sit in the same metropolitan area, a single recession or local industry collapse can devastate your entire portfolio simultaneously. Spreading investments across different regions, different property types, and different tenant industries creates genuine diversification that protects you when one market weakens.

Industrial logistics properties in Texas perform differently than multifamily assets in Florida or retail centers in Colorado. When you own properties in geographically separated markets with different tenant bases, a downturn in one region doesn’t cascade through your entire portfolio. This diversification also improves your refinancing position because lenders view geographically dispersed portfolios as lower-risk, which translates to better loan terms and stronger cash flow protection.

Strengthen Security and Loss Prevention

Security systems and loss prevention measures deserve the same rigor as your maintenance protocols. Install monitored alarm systems, implement access controls that limit entry to authorized personnel, maintain clear sightlines around the property perimeter, and establish documented procedures for tenant screening and eviction protocols. Properties with active security systems (particularly those monitored 24/7 by professional services) attract lower premiums from most carriers because theft, vandalism, and liability losses decrease measurably.

Document your loss prevention efforts and share them with your insurance agent annually because rate reviews based on improved security can unlock better pricing. The connection is direct: stronger operational discipline produces lower claims frequency, which produces lower insurance costs, which protects your cash flow in an environment where refinancing costs already consume 20 to 40 percent of annual cash flow for properties maturing in 2026 or 2027.

Final Thoughts

Understanding commercial property risks in 2026 requires you to face three hard truths: interest rates have permanently shifted property economics, tenant cost-burden data exposes your cash flow to real pressure, and climate risk demands immediate attention in your underwriting. The federal funds rate around 3.64 percent means refinancing costs will consume 20 to 40 percent of your annual income if your loans mature in 2026 or 2027, while over 22 million renter households struggle financially, which translates directly into higher default risk across multifamily and retail properties. Climate-driven insurance costs and material price increases have moved from future concerns to present-day budget items that affect your bottom line today.

Insurance coverage protects your capital when these risks materialize, but only if your policies match your actual exposure. Standard commercial property insurance leaves dangerous gaps: flood coverage is excluded entirely, business interruption limits often fall short of realistic loss scenarios, and cyber liability protection is missing from most policies (the 2025 AFP Payments Fraud and Control Survey documented that 79 percent of organizations faced attempted or actual payment fraud). Identifying your actual exposure requires detailed conversations about your specific property location, tenant profile, and financial capacity to absorb losses without triggering a financial crisis.

We at Grimes Insurance Agency have spent over 75 years helping commercial property investors build protection strategies that actually work. Contact us to review your current coverage gaps and identify the insurance structure that protects your investments against the real risks you face in 2026.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation