Business Interruption Insurance Explained in 2026: What You Need to Know

A single day without operations can cost your business thousands of dollars. Equipment failures, natural disasters, and supply chain disruptions happen more often than you’d think, and most business owners aren’t prepared for the financial fallout.

Business interruption insurance explained for 2026 shows you how to protect your revenue when unexpected events force you to shut down. At Grimes Insurance Agency, we help business owners understand this coverage so they can make informed decisions about their protection.

What Business Interruption Insurance Actually Covers

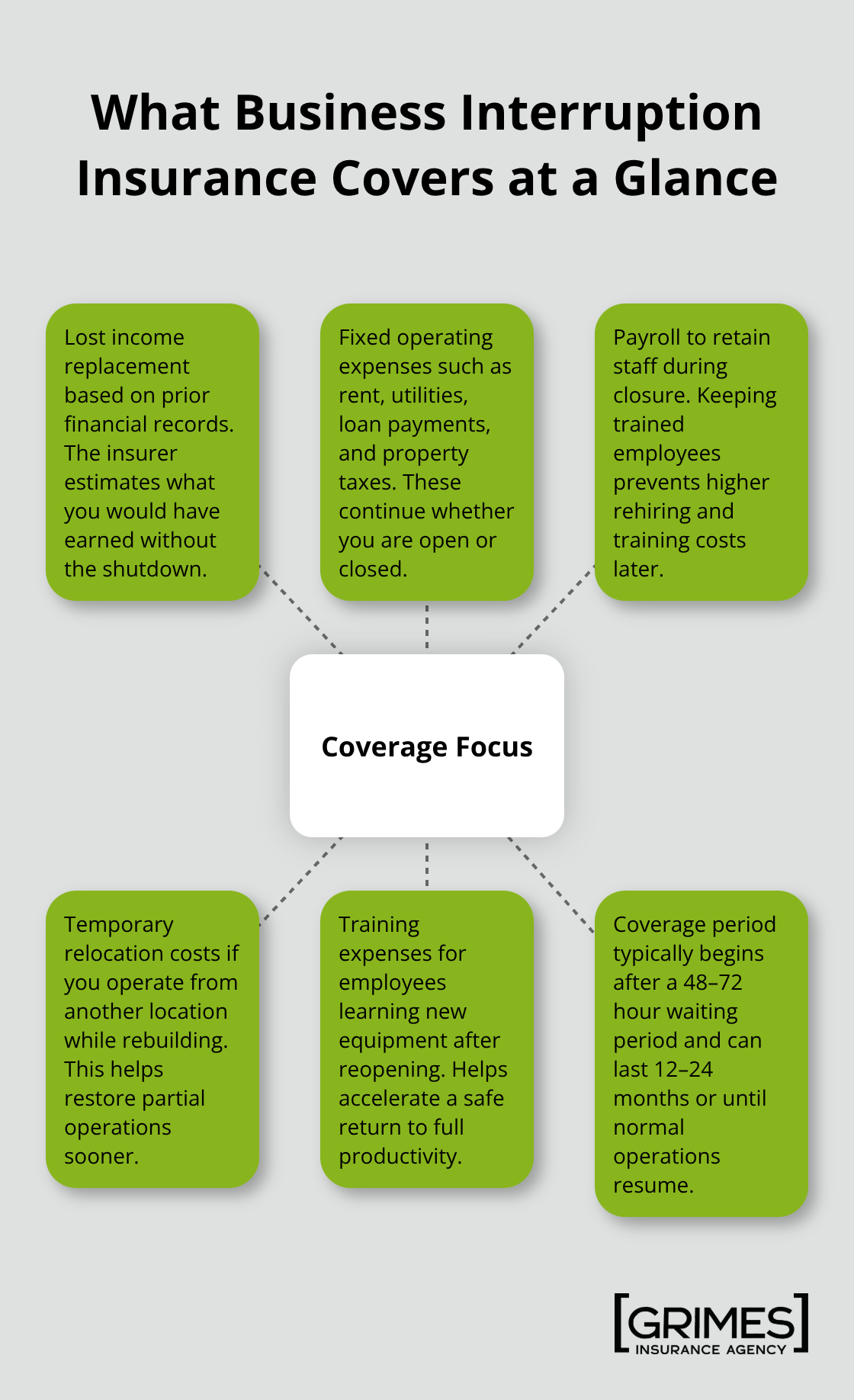

Business interruption insurance replaces the income your business loses when a covered event forces you to shut down temporarily. This isn’t property insurance-it doesn’t fix your building or replace your equipment. Instead, it covers the money you stop earning while you recover. If a fire damages your retail location and you need three months to reopen, business interruption insurance covers the sales revenue you would have made during those three months, plus your ongoing operating costs like rent, utilities, loan payments, and employee wages. The Allianz Risk Barometer 2026 ranked business interruption and supply chain disruption as the number three global risk, which shows how critical this protection has become for operations worldwide.

Understanding What Gets Covered During Shutdown

Most business interruption policies cover lost income based on your prior financial records-the insurer looks at what you earned before the loss to calculate what you’re owed. Fixed expenses continue whether you’re open or closed. Your mortgage doesn’t disappear, your loan payments don’t stop, and your property taxes still come due. A solid policy covers all of these. You can also recover wages you pay to retain staff during the closure, which matters because losing trained employees costs far more than temporary payroll.

Temporary relocation costs apply if you operate from another location while rebuilding, and training expenses for employees who learn new equipment after reopening typically fall under coverage. The coverage period starts after a waiting period of 48 to 72 hours and continues until you return to normal operations or hit your policy limit, which commonly ranges from 12 to 24 months of coverage.

Why Waiting Periods Impact Your Cash Flow

The 72-hour waiting period isn’t arbitrary-it excludes minor disruptions and keeps premiums reasonable. However, this delay directly impacts your cash flow during recovery, so factor this into your planning. Most business owners underestimate how long recovery actually takes, which leaves them exposed when disruption strikes. You need to estimate realistically how long your specific business would need to reopen and what your daily operating costs actually are.

Coverage Limits Determine Your Out-of-Pocket Risk

Your coverage limit is equally important because if your losses exceed that limit, you pay the difference out of pocket. If you choose a coverage limit that pays for six months of lost income but your recovery takes nine months, you’re responsible for the final three months of losses. This is why calculating your coverage amount correctly matters-you must account for both recovery time and actual operating expenses. Underestimating either figure leaves you dangerously exposed when disruption happens.

Understanding these coverage details positions you to make the right choice for your business. The next step involves assessing your specific vulnerability to interruptions and determining what coverage limits actually protect your operation.

Why Business Interruption Insurance Matters Now

Disruptions Have Become Mainstream Threats

Operational disruptions strike businesses constantly, not as rare events. The Allianz Risk Barometer 2026 ranked business interruption and supply chain disruption as the number three global risk, a position that reflects what business owners face today. Supply chain problems alone affected approximately 2.7 trillion dollars of merchandise in 2025-roughly 20 percent of global imports-according to Allianz Trade data. When your supply chain breaks, your business stops earning money immediately. Verisk Maplecroft reports that global conflict zones have nearly doubled since 2021 to 6.6 million square kilometers, with armed fighting areas up almost 90 percent over five years.

This geopolitical instability directly threatens the suppliers and logistics networks most businesses depend on.

Cyber Attacks and System Failures Stop Operations Cold

Cyber incidents rank as the top global risk for 2026, and when hackers shut down your systems, you cannot operate. A majority of respondents surveyed by Allianz-51 percent-view global supply chain paralysis due to geopolitical conflict as a plausible scenario within five years. These aren’t edge cases anymore. They represent mainstream business risks that demand protection.

The Hidden Cost of Downtime Extends Beyond Lost Revenue

The financial damage from downtime hits faster and harder than most business owners expect. A single day without operations costs your business thousands in lost revenue, but the real damage extends far beyond that first day. Your fixed costs keep mounting regardless of whether you generate income. Rent, loan payments, utilities, and employee salaries continue whether you operate or not. If your recovery takes three months, you face three months of these expenses with zero revenue to offset them.

Coverage Limits Determine Your Financial Survival

The coverage limit you choose determines whether you survive this gap or face catastrophic out-of-pocket costs. If your limit covers only six months of losses but your recovery takes nine months, you absorb the final three months entirely. This is why the waiting period matters to your cash flow planning and why underestimating recovery time exposes you to significant financial risk. Businesses that operate without this protection often discover during recovery that their savings evaporate within weeks, forcing permanent closure despite having a viable business model before the disruption occurred.

Understanding these financial realities shapes how you assess your specific vulnerability to interruptions and what coverage limits actually protect your operation.

Choosing Business Interruption Coverage That Actually Protects You

Calculate Your Daily Operating Costs First

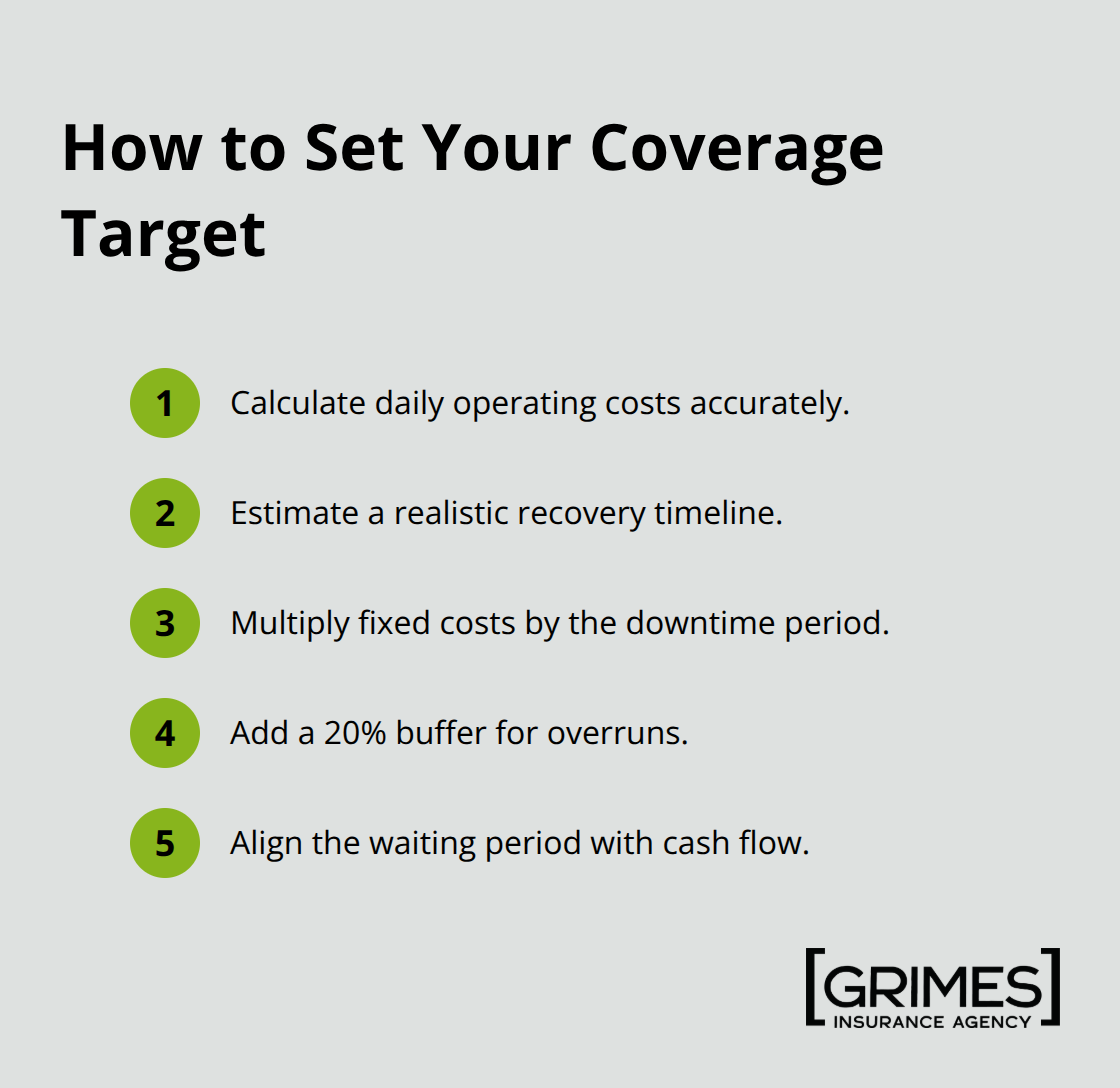

Start with your daily operating costs, not your revenue-most business owners confuse these two numbers and end up underinsured. Your daily operating costs include rent or mortgage, utilities, loan payments, insurance premiums, property taxes, and employee wages. Add these up and multiply by 365 to get your annual fixed expenses. This number matters because business interruption insurance covers these costs during shutdown, not your gross revenue. If your annual fixed expenses total $200,000, you need coverage that reflects this reality.

Determine Your Realistic Recovery Timeline

Next, establish your realistic recovery timeline. A manufacturing facility with specialized equipment might need six months to fully reopen, while a service business operating from a small office might recover in two weeks. Talk to your vendors about equipment replacement timelines, consult your landlord about building repair expectations, and ask your industry peers about their actual recovery experiences. This conversation reveals whether your current thinking about recovery time is optimistic or grounded in reality.

Calculate Your Coverage Target

Once you know your fixed costs and recovery timeline, multiply them together. If your annual fixed costs are $200,000 and recovery takes six months, you need $100,000 in coverage minimum. However, add 20 percent to this figure as a buffer because recovery almost always takes longer than expected, and unexpected expenses emerge during shutdown. This means your coverage target becomes $120,000.

Select Your Waiting Period Based on Cash Flow

The waiting period you select directly impacts your premium cost and your cash flow strategy. A 48-hour waiting period costs more than a 72-hour waiting period, but it means you receive benefits sooner during recovery. If your business operates on tight cash flow margins, the 48-hour option protects you better because those first three days of shutdown hit hardest. Conversely, if you maintain three months of operating capital in reserve, the 72-hour waiting period is acceptable and saves you money on premiums.

Work with an Independent Agent to Review Policy Language

An independent insurance agent can access multiple insurers and compare coverage options specific to your business type and industry risks. They understand that a restaurant faces different interruption risks than a manufacturing plant or a professional services firm. Tell your agent about your specific vulnerabilities-if you depend heavily on a single supplier, mention this because some policies offer supply chain coverage extensions. If you operate in an area prone to specific natural disasters like hurricanes or wildfires, your agent needs this information to select appropriate coverage. If your business relies on staff you cannot easily replace, coverage that includes payroll continuation becomes essential.

Your agent should also review your commercial property policy to confirm business interruption coverage integrates properly with it. Many business owners discover gaps between their property policy and their interruption coverage because they never had this conversation. The policy language matters more than the carrier name. Ask your agent to explain exactly what triggers coverage in your policy. Does it require direct physical loss to your building, or does it cover losses from utility outages caused by damage elsewhere? Some policies exclude losses from government-mandated closures unrelated to property damage, which became relevant during recent public health situations. Understanding these exclusions prevents shock when you file a claim. Request a sample claim form from your agent and ask how they would handle a claim for your specific business scenario. This conversation reveals whether your agent truly understands your operation and whether the policy actually covers what you think it covers.

Final Thoughts

Business interruption insurance explained for 2026 comes down to one reality: your business cannot survive extended downtime without financial protection. The disruptions covered throughout this guide happen regularly, and when they strike, your fixed costs continue accumulating while revenue stops completely. The coverage you choose today determines whether your business survives or collapses when interruption happens.

Calculate your actual daily operating costs, determine your realistic recovery timeline, and select coverage limits that reflect both numbers plus a safety buffer. Your waiting period choice should match your cash flow situation, not just your budget. Most importantly, review your policy language with someone who understands your specific business risks, and request a sample claim form to walk through your specific business scenario with your agent.

Contact Grimes Insurance Agency today to discuss your business interruption coverage and protect what you have built. We access multiple carriers to ensure you receive the best protection and pricing for your situation. This conversation takes an hour and prevents catastrophic gaps in your protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation