Understanding Commercial Property Insurance Coverage Limits: What You Should Know

Many business owners underestimate how much coverage they actually need. Getting your commercial property insurance coverage limits wrong can leave you exposed to significant financial losses when disaster strikes.

At Grimes Insurance Agency, we’ve seen firsthand how the right coverage limits make all the difference. This guide walks you through what you need to know to protect your business properly.

Understanding Coverage Limits and How They Work

Coverage limits are the maximum dollar amount your insurance company will pay for a covered loss. A $500,000 building limit means your insurer pays up to $500,000 if your building burns down. A $100,000 business personal property limit means they pay up to $100,000 if your equipment, inventory, and fixtures are destroyed. If your actual loss exceeds the limit, you pay the difference out of your own pocket. This isn’t theoretical-it’s a hard financial ceiling.

Many business owners discover this the hard way after a loss, when they realize their $300,000 limit doesn’t cover their $450,000 in actual damage. That $150,000 gap comes directly from your business account.

How Coinsurance Penalties Reduce Your Payout

Coverage limits interact with other policy features that most owners overlook. Coinsurance clauses help ensure you carry enough coverage to protect your possessions in case of a loss. They require you to insure your property for a minimum percentage of its total value-typically 80%, 90%, or even 100%. If you don’t meet this requirement, the insurance company applies a penalty to your payout.

The number 100% seems to be not appropriate for this chart. Please use a different chart type.

For example, if your building is worth $1 million and your policy has an 80% coinsurance requirement, you must carry at least $800,000 in coverage. If you only carry $600,000 and suffer a $50,000 loss with a $1,000 deductible, your actual payout drops to approximately $36,750 instead of the expected $49,000. The math is straightforward: (coverage carried ÷ coverage required) × (loss minus deductible) = your actual payout. The insurer applies this penalty because they want you to carry adequate coverage that reflects the true value of what you’re protecting.

Reconstruction Cost Versus Market Value

The critical mistake we see repeatedly is basing coverage limits on market value rather than reconstruction cost. Your building’s market value and what it actually costs to rebuild are two completely different numbers. A 5,000-square-foot warehouse in Lubbock might have a market value of $400,000 but a reconstruction cost of $600,000 when you factor in current labor rates, materials, code upgrades, and the time to rebuild. If you insure based on market value alone, you’re automatically underinsured.

Start with a professional property valuation that specifically calculates reconstruction cost using today’s material and labor prices, not depreciated values. This matters enormously because inflation continuously pushes reconstruction costs upward. If you last reviewed your coverage limits three years ago, your actual rebuilding costs have likely increased 15–20% or more depending on your property type and location.

Business Interruption Limits Require Separate Calculation

Business interruption coverage, sometimes called business income coverage, has its own separate limits that operate independently from your property limits. This coverage replaces lost income and covers operating expenses during the period your business is shut down due to a covered event. The limit should be based on your average monthly revenue plus your monthly operating expenses multiplied by the realistic number of months it would take to resume operations.

If your business generates $50,000 in monthly revenue with $30,000 in monthly operating expenses, and you estimate three months to rebuild and reopen, your business interruption limit should be at least $240,000 (($50,000 + $30,000) × 3 months). Setting this limit too low creates a false sense of protection. You might think you’re covered, but when the claim comes, you discover the limit only covers 30 days of losses when your actual recovery takes 90 days. That gap becomes real cash you must find to keep the business operating while rebuilding.

The right coverage limits protect your business from these gaps. Understanding how to set them properly requires looking at your specific property, income, and recovery timeline-which is exactly what we’ll examine in the next section on assessing your actual needs.

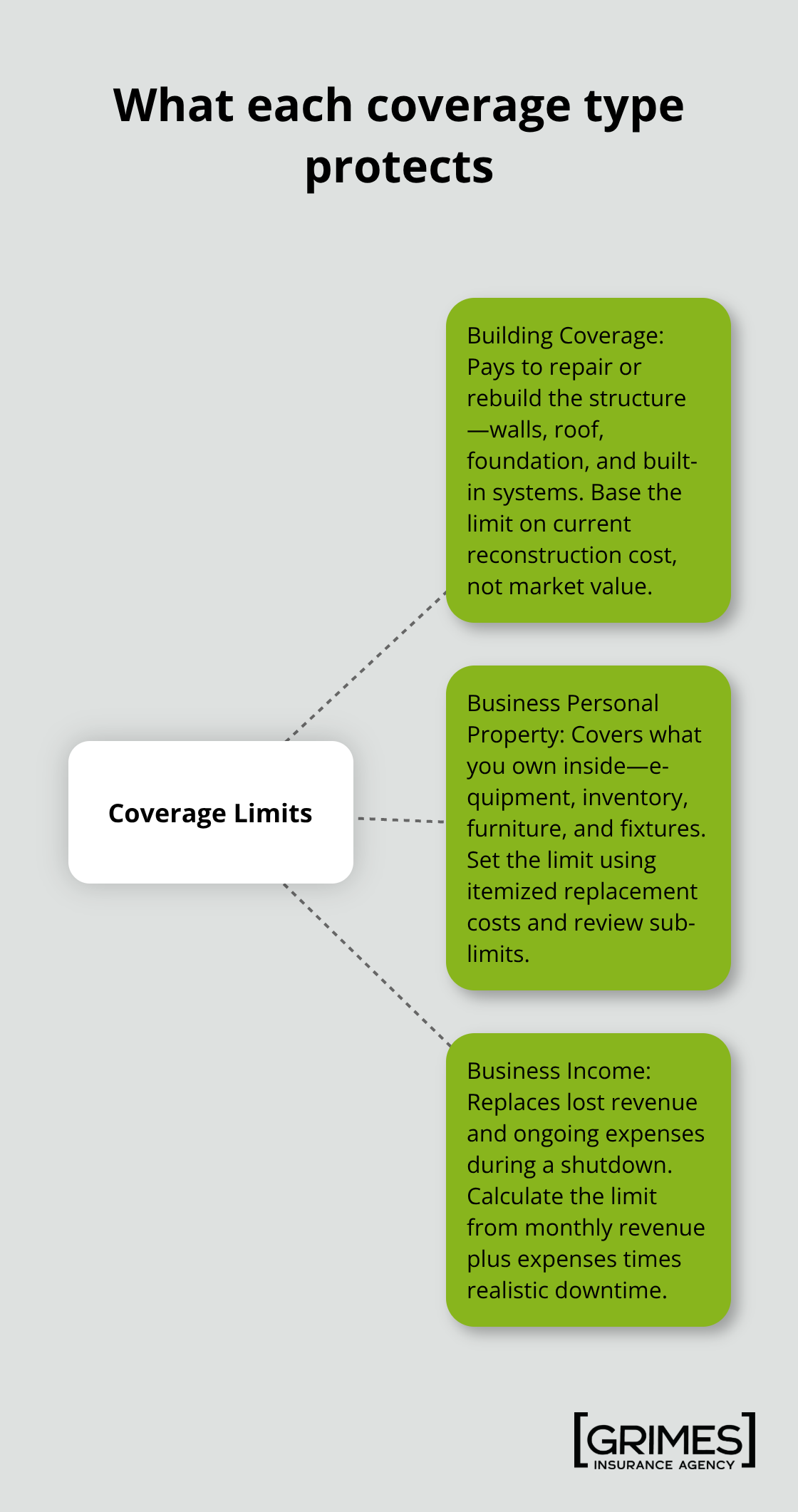

The Three Coverage Types That Matter Most

Your commercial property insurance policy typically separates coverage into distinct categories, each with its own limit, and understanding what each one covers prevents costly gaps when you file a claim. Building coverage protects the structure itself-walls, roof, foundation, built-in systems-while business personal property coverage protects what’s inside: equipment, inventory, furniture, and fixtures you own. These two limits operate independently, meaning a $500,000 building limit and a $150,000 personal property limit don’t combine into a single pool. If your building sustains $300,000 in damage and your contents sustain $100,000 in damage, the building limit covers the first, and the personal property limit covers the second.

Most owners set one limit high and assume the other is adequate without actually calculating what they need.

Building Coverage Requires Accurate Reconstruction Costs

Your building limit should reflect the full reconstruction cost valuation for commercial property insurance of the structure today, not what it cost to build ten years ago or what a real estate appraiser says it’s worth on the market. A 10,000-square-foot manufacturing facility in Lubbock might appraise at $800,000 but cost $1.2 million to rebuild because reconstruction includes code compliance upgrades, modern materials, and current labor rates substantially higher than depreciated valuations suggest. Owners dramatically underestimate reconstruction costs. If your policy requires 80% coinsurance coverage and you’ve insured based on market value rather than reconstruction cost, you trigger a penalty on every claim. Obtain a professional property valuation that specifically calculates reconstruction cost using current material and labor prices in your region, not a standard appraisal that emphasizes market value.

Personal Property and Equipment Need Itemized Assessment

Business personal property limits should account for everything you own inside the building: machinery, tools, computers, shelving, inventory, furniture, and specialized equipment. Most owners set this limit as an afterthought, choosing a round number like $100,000 without actually calculating what they’d need to replace. Your equipment list should include purchase prices and current replacement costs for high-value items. If you own a $75,000 industrial printer, a $45,000 HVAC system, $30,000 in inventory, and $20,000 in general equipment and furniture, you need at least $170,000 in personal property coverage-not $100,000. Sub-limits within your policy can also cap coverage for specific items like computers (often capped at $2,500 each) or theft (sometimes limited to 10% of the personal property limit), so review your policy documents carefully to identify these restrictions.

Business Income Coverage Requires Monthly Expense Analysis

Business interruption or business income coverage operates on a completely separate limit from your property coverage and reimburses lost revenue and ongoing expenses during a shutdown. Calculate this limit by adding your average monthly revenue to your average monthly operating expenses, then multiply by the realistic number of months needed to resume operations. A restaurant generating $60,000 in monthly revenue with $35,000 in monthly operating expenses that estimates four months to rebuild needs at least $380,000 in business income coverage (($60,000 + $35,000) × 4). Most owners set this limit at six months of revenue alone, forgetting that expenses continue during shutdown-rent, utilities, loan payments, and salaries for key staff. The actual number of months to resume operations varies by damage severity and your industry; a simple retail space might reopen in two months while a manufacturing facility could take six months or longer.

Sub-Limits and Special Coverage Restrictions

Your policy likely contains sub-limits that cap payouts for specific perils or items even when your overall limit is higher. A policy with a $1 million building limit might carry only a $100,000 sub-limit for flood damage, meaning you’d pay $900,000 out of pocket if flooding causes $1 million in damage. High-value items like specialized equipment, art, or antiques may require scheduling (listing them separately on your policy) to receive full coverage rather than relying on blanket limits. Water damage, mold, theft, and debris removal often carry their own sub-limits that fall well below your main coverage amount. Review your policy documents to identify these restrictions and determine whether endorsements or additional coverage would close gaps in your protection.

The limits you set across these three categories form the financial foundation of your business protection. Getting them right requires honest assessment of your property value, income, and recovery timeline-which means moving beyond guesswork to actual calculations based on your specific situation.

Setting Your Coverage Limits to Match Your Actual Needs

Create a Detailed Property Inventory

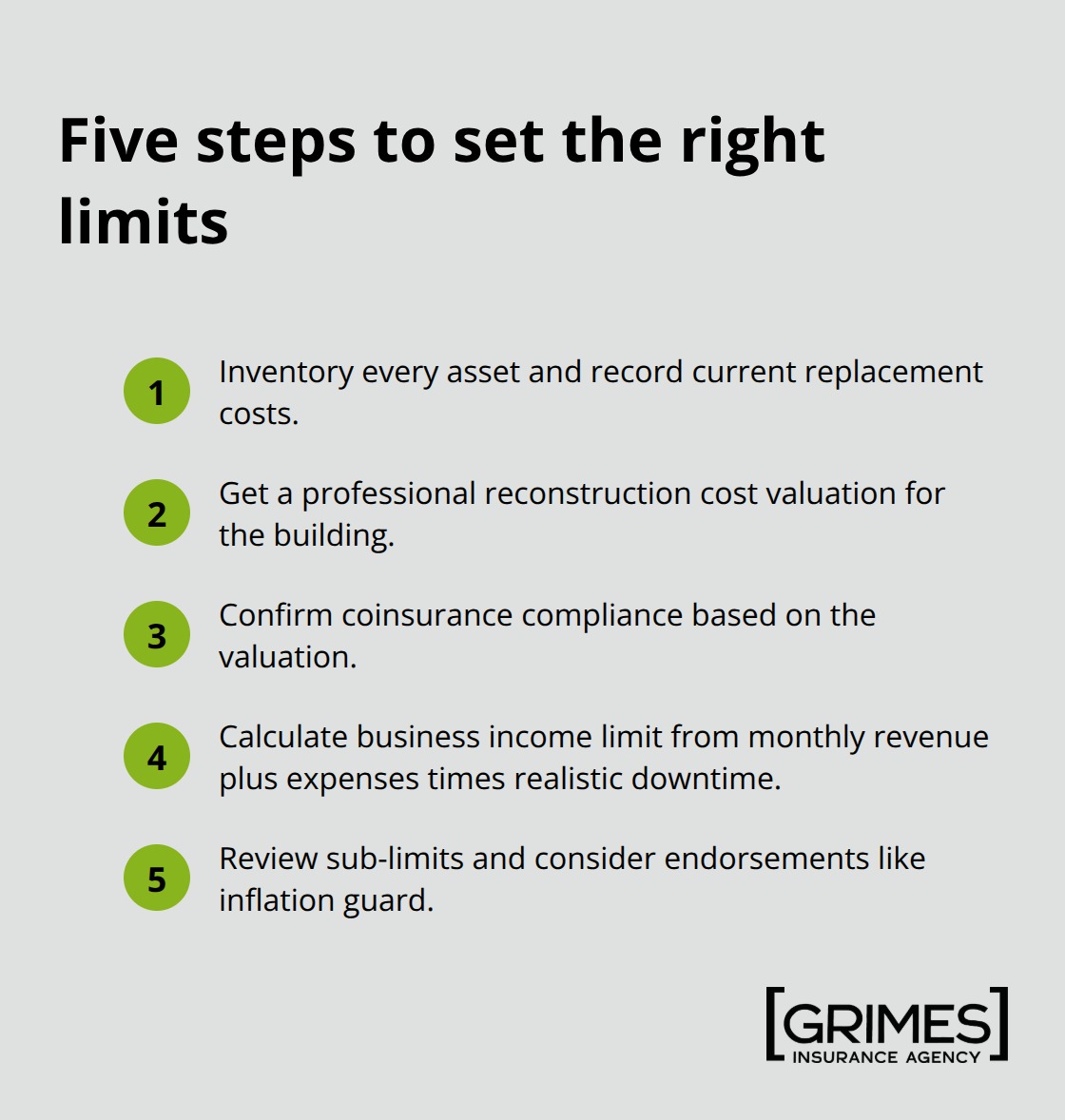

Start with a property inventory that goes beyond rough estimates. Walk through your building and document every asset that would need replacement: machinery, equipment, computers, furniture, inventory, and fixtures. For high-value items exceeding $5,000, photograph them and record purchase prices and current replacement costs. This process reveals what many owners discover-their mental estimate of total equipment value was off by 30% or more. A manufacturing facility owner might think they have $80,000 in machinery when the actual replacement cost is $120,000. Once you have this detailed list, multiply the total replacement cost by 1.15 to account for inflation and unexpected items you’ll encounter during rebuilding. This number becomes your business personal property limit.

Obtain a Professional Reconstruction Cost Valuation

For your building coverage, obtain a professional reconstruction cost valuation specific to commercial property-not a real estate appraisal. A real estate appraiser estimates market value; you need a property valuator who calculates what it actually costs to rebuild using current material and labor rates in your region. Reconstruction costs have increased significantly in recent years due to labor availability and material pricing changes. Your building limit should match this reconstruction cost valuation, then verify you’re meeting your policy’s coinsurance requirement (typically 80%, 90%, or 100%) by multiplying the reconstruction cost by the required percentage. If your building reconstruction cost is $800,000 and your coinsurance is 80%, you need at least $640,000 in coverage-not the $500,000 you might have thought was adequate.

Calculate Your Monthly Operating Loss

Business income coverage requires calculating your actual monthly loss if operations shut down completely. Add your average monthly revenue to your total monthly operating expenses (rent, utilities, loan payments, payroll, insurance premiums, and other fixed costs that continue during closure). Most business owners underestimate these expenses-they focus on revenue and forget that rent and loan payments don’t pause while you rebuild. Multiply this monthly total by the realistic number of months your business would be closed. A retail shop might reopen in two months; a manufacturing facility could take six months or longer depending on damage severity and equipment availability.

A restaurant generating $70,000 monthly revenue with $40,000 in monthly operating expenses needs at least $330,000 in business income coverage if recovery takes three months (($70,000 + $40,000) × 3 = $330,000). Setting this limit below your calculated number creates a false sense of security-you think you’re protected, then face a coverage gap during the actual claim.

Work with an Insurance Professional to Verify Coverage

Once you’ve calculated these numbers, professional guidance becomes essential. An insurance professional reviews your calculations, identifies coverage gaps you’ve overlooked (like sub-limits for specific perils), and ensures your policy structure actually matches your risk profile. They also discuss whether endorsements like inflation guard protection make sense for your situation-this automatically adjusts your limits annually to keep pace with rising costs, preventing the slow creep of underinsurance. The cost of professional guidance is negligible compared to discovering after a loss that your limits were inadequate. An insurance professional can also help you understand whether your current policy structure protects your specific assets and operations or whether adjustments would strengthen your protection.

Final Thoughts

Getting your commercial property insurance coverage limits right protects your business from financial devastation when disaster strikes. Base your building limit on reconstruction cost using current material and labor rates, not market value or outdated appraisals. Calculate your business personal property limit by inventorying everything you own and adding 15% for inflation and unexpected replacement costs. Set your business income limit by adding monthly revenue to monthly operating expenses, then multiplying by realistic recovery months.

Professional guidance transforms these calculations into actionable protection that actually works when you need it. An insurance professional identifies coverage gaps you’d miss on your own, explains how coinsurance penalties work in your specific policy, and recommends endorsements like inflation guard protection that prevent slow creep of underinsurance over time. They also review sub-limits that cap payouts for specific perils, ensuring you understand where your protection ends and your out-of-pocket exposure begins.

Schedule a comprehensive policy review with an insurance professional who understands commercial property insurance coverage limits and your industry. Bring your property inventory, recent financial statements showing monthly revenue and expenses, and your current policy documents. We at Grimes Insurance Agency have over 75 years of experience helping business owners in Lubbock and beyond set appropriate coverage limits that actually protect what they’ve built, and our team accesses multiple carriers to find the best protection and pricing for your specific needs. Contact us today to review whether your current limits match your actual exposure, or visit Grimes Insurance Agency to get started.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation