Understanding Business Insurance Requirements in Texas: A Comprehensive Guide

Running a business in Texas means navigating specific insurance requirements that protect your company from real financial risk. Whether you operate a small retail shop, manage construction crews, or own rental properties, the coverage you need varies significantly based on your industry and operations.

We at Grimes Insurance Agency help Texas business owners understand exactly what insurance they need and why. This guide breaks down the mandatory coverage, industry-specific requirements, and how to find the right protection for your situation.

What Business Liability Coverage Do You Actually Need in Texas

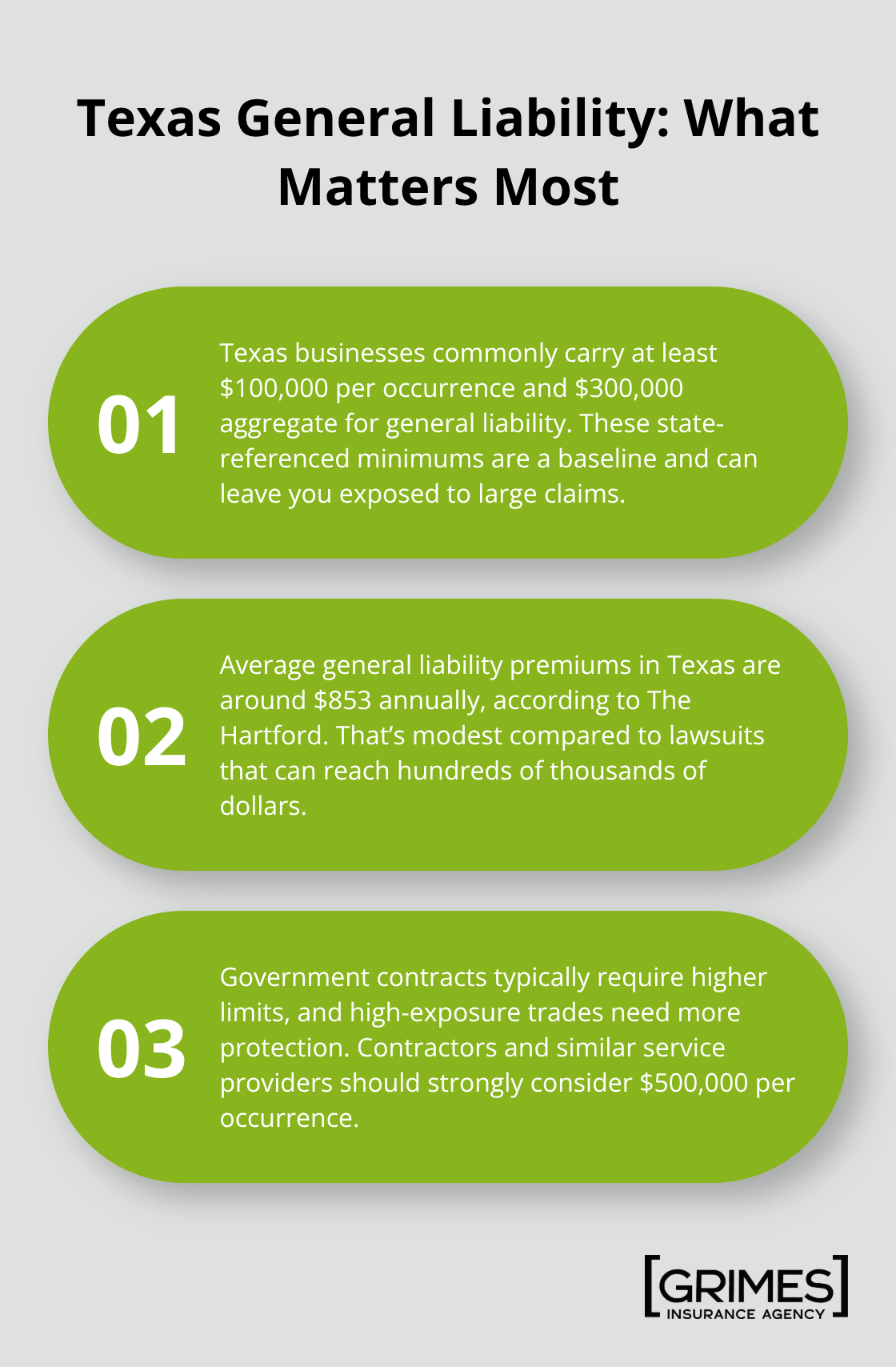

General liability insurance protects your business when someone claims you caused them bodily injury or property damage. In Texas, the minimum coverage most businesses should carry is $100,000 per occurrence and $300,000 aggregate per year, according to the Texas State Fire Marshal’s Office requirements. However, minimum coverage often leaves you dangerously exposed. The Hartford reports that average general liability premiums in Texas run around $853 annually, which is reasonable insurance against lawsuits that could cost hundreds of thousands. If you contract with government entities in Texas, you’ll face mandatory requirements that typically demand higher limits. Construction companies, contractors, and service providers face the highest exposure and should seriously consider $500,000 per occurrence coverage minimum. A single injury claim can bankrupt a small operation, and Texas courts award substantial damages.

Workers Compensation Separates Required From Optional

Texas doesn’t mandate workers compensation for most businesses, which confuses many owners into skipping it entirely. This is a dangerous mistake. If you contract with any government entity, workers compensation becomes mandatory. If you have even one employee and want to operate responsibly, you need coverage. The average annual workers compensation premium in Texas runs about $714, or roughly $59 monthly according to The Hartford. That’s cheap protection against claims that could exceed six figures. The Texas Department of Insurance administers the Division of Workers Compensation, which handles disputes and claims. If an injured worker contests their claim, you contact the Division at 800-252-7031 or 512-804-4100. The Division also offers safety consultations to help reduce workplace injuries and associated costs. Operating without workers compensation exposes you to personal liability when an employee gets hurt.

Your Physical Assets Need Direct Protection

Commercial property insurance covers buildings, tools, equipment, and inventory your business owns or leases. This coverage isn’t optional if you have a mortgage on your building, as lenders require it. The Hartford data shows Business Owner’s Policies, which bundle property and liability coverage, average $2,072 annually in Texas. Property insurance becomes especially critical if you store valuable equipment or inventory. A fire, theft, or weather event can instantly destroy your ability to operate. Texas experiences significant hail and wind damage annually, making property coverage essential rather than theoretical. If you lease your space, your landlord’s insurance doesn’t cover your equipment or inventory, leaving you completely exposed. You should review your current property policy limits carefully because underinsuring creates a false sense of security that evaporates the moment you file a claim.

Coverage Gaps Vary by Your Business Type

Your industry determines which liability exposures matter most. Contractors face different risks than retailers, and retailers face different risks than property investors. The coverage that protects a construction company won’t adequately protect a service business. Understanding your specific industry risks helps you avoid paying for unnecessary coverage while ensuring you don’t leave critical gaps. The next section walks through industry-specific requirements so you can identify exactly what your business type demands.

Industry-Specific Insurance Needs in Texas

Construction and Contractor Coverage

Construction contractors operate under completely different risk profiles than retail shops, and property investors face exposure that service businesses never encounter. Your industry determines which insurance gaps will destroy your business if left uncovered. Contractors face liability exposure from equipment operation, employee injuries on job sites, and property damage claims that routinely exceed $100,000 per incident.

The Texas State Fire Marshal’s Office requires contractors to carry at least $100,000 per occurrence and $300,000 aggregate for general liability, but this baseline leaves you exposed. Construction crews working on government contracts must carry workers compensation insurance, making it mandatory rather than optional. Equipment coverage matters enormously because a single piece of heavy machinery costs $50,000 to $200,000, and theft or damage creates immediate cash flow problems.

Contractors should also carry commercial bonds to protect projects and clients. Higher limits make sense given the nature of construction work and the severity of potential claims.

Retail and Service Business Requirements

Retail and service businesses face entirely different risks centered on customer interactions and premises liability. A customer slipping in your store, getting injured by your product, or claiming negligent service can trigger lawsuits that general liability insurance handles. Retail operations averaging $2,072 annually for Business Owner’s Policies gain bundled property and liability protection, covering both the physical storefront and inventory simultaneously.

Service businesses like plumbers, electricians, and HVAC contractors need professional liability coverage beyond general liability because mistakes in your work directly harm customers and their property. This coverage protects against claims that your work caused damage or failed to meet standards. Service providers should verify that their policies cover the specific work they perform and the geographic areas where they operate.

Real Estate and Investment Property Insurance

Real estate investors and property managers operate under the strictest insurance requirements because mortgage lenders demand specific coverage levels. Commercial property insurance protecting rental buildings, apartment complexes, and investment properties becomes non-negotiable when you carry a loan. Lenders typically require coverage equal to the replacement cost of the building, not just the mortgage balance.

Landlords also need liability coverage because tenant injuries on your property create legal exposure, and you remain responsible for maintaining safe premises. Rental property investors should verify that their commercial property policies cover liability for tenant-caused damage and include loss of rents coverage, which replaces income during repairs after a covered loss. Each business type requires honest assessment of its actual exposures rather than generic coverage that leaves critical gaps. Understanding your specific industry risks helps you avoid paying for unnecessary coverage while ensuring you don’t leave critical gaps unprotected. The next section walks through how to evaluate carriers and agents so you can find the right protection at the right price.

Finding the Right Insurance Carrier and Agent for Your Texas Business

Compare Carriers Beyond Price Alone

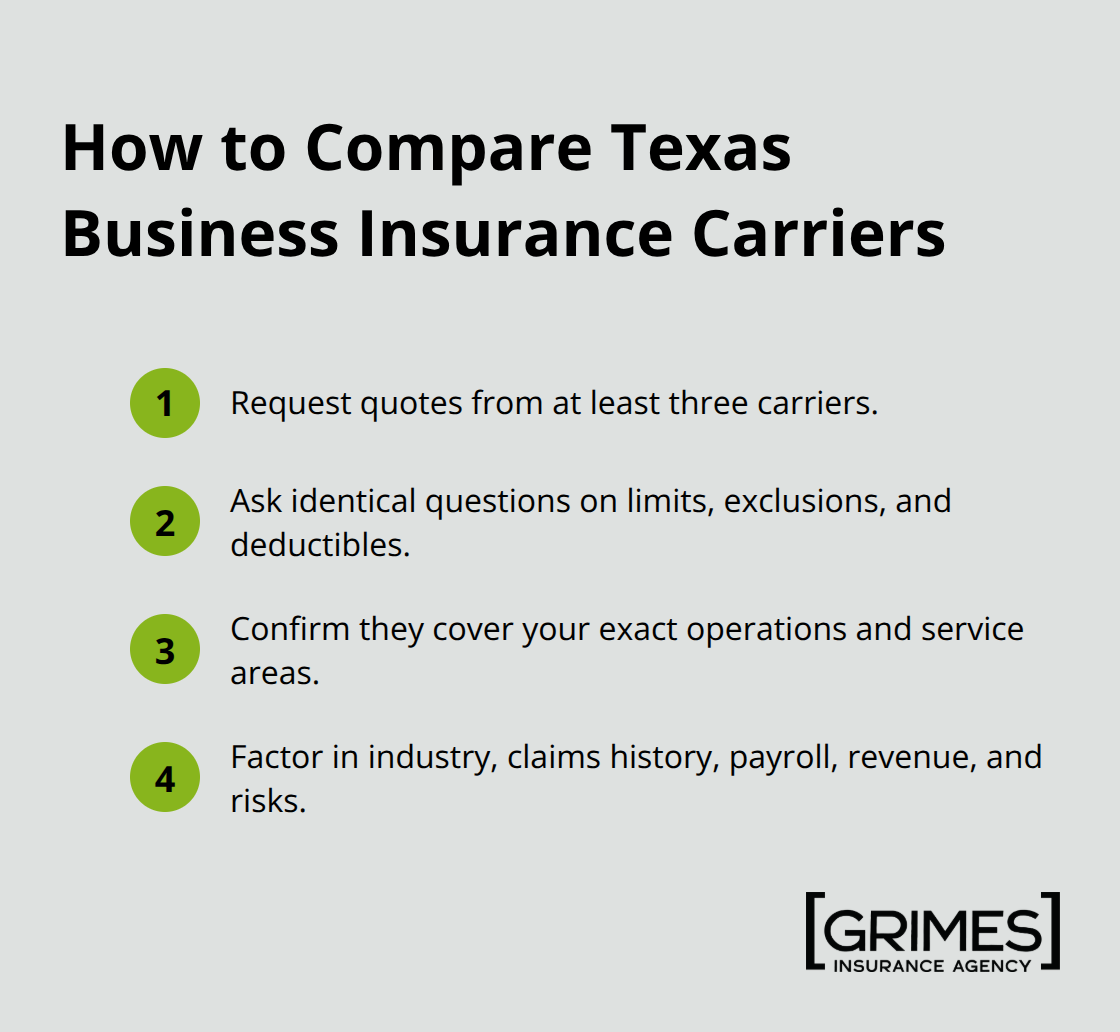

Comparing insurance carriers requires moving beyond premium quotes and examining what each company actually covers and how they handle claims. No single insurer excels at covering every business type equally well. A carrier that offers excellent rates for retail operations might be expensive or restrictive for contractors, and vice versa. When you request quotes, ask each carrier the same detailed questions about coverage limits, exclusions, deductibles, and whether they cover your specific operations.

When you compare insurance carriers, request quotes from at least three carriers before making a decision, and don’t automatically choose the lowest price. Your actual quote depends entirely on your industry, claims history, payroll, revenue, and the specific risks your business faces.

Evaluate Claims Handling and Service Quality

A carrier offering $500 annual savings might exclude coverage you desperately need or deny claims more frequently than competitors. Ask potential carriers about their claims process, average claim processing time, and whether they assign a dedicated agent or adjuster to your account. Some carriers process claims within days while others take weeks, which matters enormously when your business cannot operate while waiting for payment.

Understanding how a carrier treats policyholders during claims reveals far more than marketing materials ever will. Contact their customer service line with a test question and note how quickly they respond. Check online reviews from other Texas business owners to see whether customers praise or criticize their claims experience. A slightly higher premium often pays for itself through faster claim resolution and fewer disputes.

Work with Independent Agents for Better Access

Independent agents have access to multiple carriers and understand how different insurers rate specific business types, giving you advantages that direct online quotes cannot match. When you work with an independent agent, you gain someone who advocates for your interests rather than pushing a single company’s products. Agents know which carriers specialize in construction, which ones excel at retail coverage, and which ones offer the best rates for your specific situation.

The Texas Department of Insurance maintains licensing records for all agents, so verify that your agent holds an active Texas license before signing anything. Ask your agent directly how they’re compensated because understanding whether they earn higher commissions from certain carriers helps you evaluate their recommendations. Most independent agents earn standard commissions from all carriers, but some arrangements create conflicts of interest worth understanding upfront.

Verify Agent Expertise and Recommendations

Your agent should explain exactly which coverages you need and why, using your specific business operations to justify recommendations rather than offering generic packages. An agent who listens to your operations and asks detailed questions about your risks demonstrates genuine expertise. An agent who immediately quotes a standard package without asking questions signals that they prioritize speed over accuracy.

Ask your agent about their experience with businesses like yours. How many contractors, retailers, or property investors do they represent? What common coverage gaps have they identified in your industry? Agents with deep experience in your sector spot risks that generalists miss entirely. They also know which carriers offer the best pricing for your specific business type, saving you money through informed placement rather than guesswork.

Schedule Regular Policy Reviews

Once you select a carrier and policy, schedule a review meeting with your agent annually because your business changes, new risks emerge, and coverage gaps appear over time. Expansion into new service areas, hiring additional employees, or purchasing new equipment all affect your insurance needs. A policy that protected you adequately last year might leave you exposed this year. Annual reviews catch these changes before they create uninsured losses that devastate your business.

Final Thoughts

Understanding business insurance requirements in Texas protects your company from financial devastation when claims arise. The coverage you need depends entirely on your industry, operations, and the specific risks your business faces daily. Comprehensive coverage planning means honestly assessing your actual risks rather than accepting generic packages that leave critical gaps.

Your business changes constantly, and your insurance should change with it. Annual reviews with your agent catch gaps before they become expensive problems. A policy that protects your building might not cover your equipment, and coverage that handles customer injuries might exclude professional liability for your work.

Contact Grimes Insurance Agency today to discuss your business insurance needs and receive quotes from carriers that specialize in your business type. We access multiple carriers to find coverage that matches your specific business type and budget. Protecting what you’ve built requires the right coverage at the right price, and that starts with honest assessment of your actual risks.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation