Understanding Home Insurance Policies in 2026: Your Essential Guide

Home insurance protects one of your biggest investments, yet many homeowners don’t fully understand what their policies actually cover. Premiums have climbed significantly in 2026, making it more important than ever to know exactly what you’re paying for.

We at Grimes Insurance Agency created this guide to help you navigate understanding home insurance policies in 2026. Whether you’re shopping for new coverage or reviewing your current policy, you’ll find the facts and practical steps you need to make confident decisions.

What’s Covered in Your Home Insurance Policy

Dwelling Coverage Protects Your Home’s Structure

Your standard homeowners policy covers three major areas, but most homeowners misunderstand the specific limits and exclusions that apply to each. Dwelling coverage protects the structure itself-walls, roof, foundation, and permanently attached systems like electrical and plumbing. The Insurance Information Institute confirms that replacement cost coverage for the dwelling is standard in 2026 policies, meaning repairs cover actual rebuild costs rather than market value. This distinction matters enormously. If your home would cost $450,000 to rebuild today but you only carry $300,000 in dwelling coverage, you’ll absorb the gap out of pocket after a covered loss.

Construction costs continue climbing, so verify your dwelling limit reflects current rebuilding expenses, not the price you paid years ago. Many insurers now automatically adjust dwelling coverage annually through inflation guards, but confirm your provider includes this feature.

Personal Property Coverage Has Real Limits

Personal property coverage typically sits at 50-70% of your dwelling limit, protecting furniture, appliances, clothing, and other belongings inside your home. Here’s where most homeowners get it wrong: standard policies pay actual cash value for personal property unless you add a replacement cost endorsement. That means a five-year-old television worth $800 new might only net you $300 in a claim.

If you own jewelry, fine art, or collectibles, these items hit sublimits-often just $1,500 to $2,500 total-regardless of actual value. The Insurance Information Institute recommends scheduling high-value items with appraisals to avoid catastrophic underinsurance.

Liability and Medical Payments Protect You Financially

Liability coverage is coverage beyond the liability limits on your existing policies. Standard limits range from $100,000 to $300,000 according to the Insurance Information Institute, but with home values and legal judgments rising, many financial advisors now suggest considering umbrella policies that add $1 million or more in protection for relatively low cost.

Medical payments coverage-typically $1,000 to $5,000-pays for minor injuries to guests without requiring fault, helping you avoid small claims that could spike your rates. Understanding these three coverage areas sets the foundation for making smart choices about your specific needs and the deductibles that affect your premium.

How Home Insurance Costs Have Changed in 2026

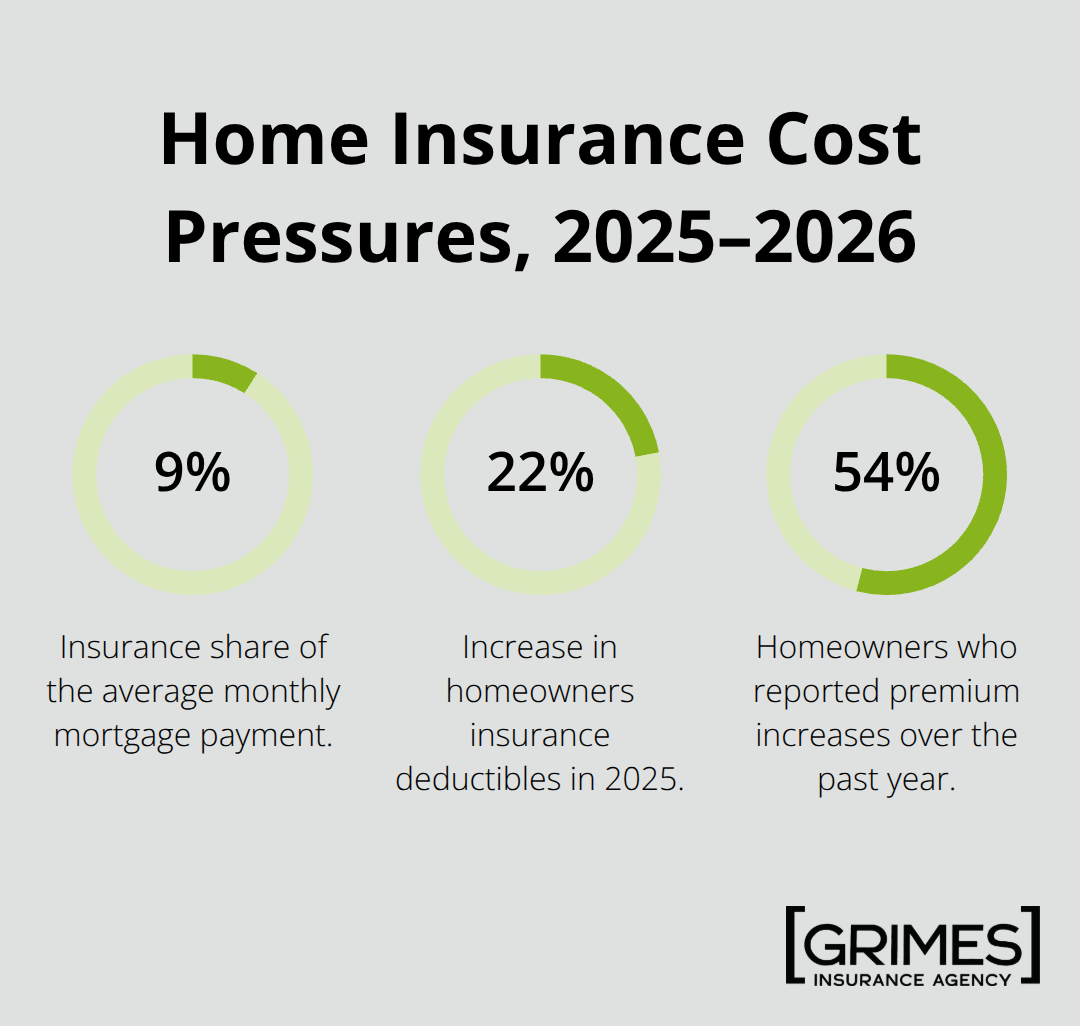

The average cost for a new homeowners policy reached approximately $1,950 in late 2025, up 8.5% year over year according to Matic’s analysis of nearly 9 million quoted properties. While this marks a slowdown from the double-digit increases homeowners faced between 2022 and 2024, the reality remains stark: insurance now consumes about 9% of your monthly mortgage payment, the highest share on record. This isn’t temporary. The 8.5% annual increase still far exceeds the pre-2022 norm of 3-5% yearly growth, meaning your insurance costs are rising faster than inflation.

Construction and repair expenses continue climbing, and insurers pass these costs directly to policyholders. Deductibles jumped 22% in 2025 alone, shifting more financial responsibility onto homeowners while helping carriers lower ongoing premiums. About 54% of homeowners reported premium increases over the past year according to Harris Poll research, making this a widespread affordability crisis rather than an isolated problem.

Roof Age Now Determines Your Price

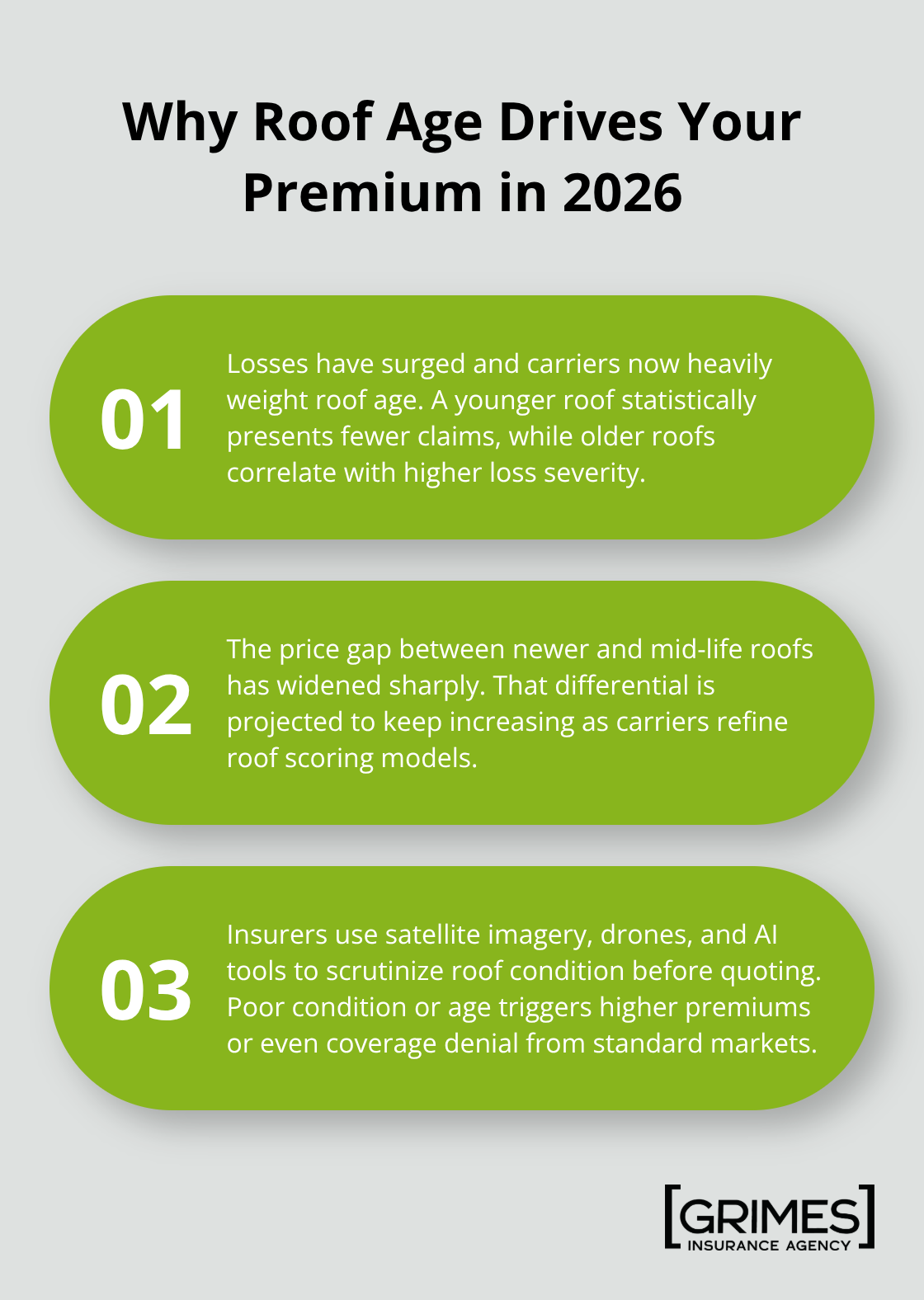

Roof condition has become the single biggest pricing factor in 2026 underwriting. U.S. roof claims reached nearly $31 billion in 2024, roughly 30% higher than 2022 levels, and insurers have responded with dramatically widened price gaps between newer and older roofs.

A roof under five years old versus one that is 11-15 years old now carries a $155 annual premium difference, up from just $49 in 2022. This gap will likely widen further in 2026. Carriers now deploy satellite imagery, drones, and AI-driven tools to assess roof condition before quoting your policy. If your roof approaches ten years old, expect substantially higher premiums or potential coverage denial from standard carriers. A roof replacement before shopping for new coverage can save thousands over your policy’s lifetime. Alternatively, if replacement isn’t feasible, you may end up in the Excess & Surplus market, where policies cost significantly more and offer fewer protections.

Where You Live Matters More Than Ever

Regional pricing diverged sharply in 2025, with some states experiencing dramatic increases. Georgia saw premiums jump 28.4%, Colorado 25.7%, New York 23%, and Texas 20.5%. Colorado homeowners faced new-policy premiums roughly $666 higher than 2024 levels alone. These aren’t minor adjustments; they represent fundamental shifts in carrier appetite for risk in specific geographies. Climate exposure drives this variation. Areas with higher exposure to hurricanes, wildfires, and severe convective storms face the steepest increases. The 2025 severe convective storm season generated approximately $42 billion in losses, cementing these storms as the top peril for insurers. If you live in a high-risk state, standard carriers may have already exited your market or tightened underwriting so severely that coverage becomes difficult to obtain. The Excess & Surplus market now accounts for roughly 16% of policies nationwide, up from under 2% in 2023, primarily because homeowners in high-risk areas have nowhere else to turn.

How Insurers Now Price Your Risk

Carriers have shifted from broad underwriting to property-specific assessment. Satellite imagery, drones, and AI-driven tools now evaluate your exact risk profile before you receive a quote. Localized weather risk data and catastrophe modeling inform pricing decisions that reflect your specific location and property conditions. This precision means two homes on the same street can carry vastly different premiums based on subtle differences in exposure, construction, or maintenance. Lenders reported experiencing home insurance issues (frequently or somewhat frequently) over the last year according to Matic’s survey, affecting loan approvals and terms. Understanding how insurers assess your property helps you anticipate pricing and identify areas where improvements can lower your costs. The next section explores how to evaluate your specific coverage needs and compare quotes effectively across carriers using this new pricing landscape.

How to Build Coverage That Matches Your Actual Risk

Calculate Your Home’s True Rebuild Cost

Selecting the right homeowners policy requires matching coverage limits to your specific property and financial situation, not chasing the lowest premium. Start with your home’s actual rebuild cost, not its market value. A home purchased for $350,000 might cost $450,000 to rebuild today due to inflation in construction materials and labor. Contact three local contractors or use your county assessor’s cost data to estimate replacement expenses accurately. Your dwelling coverage must reflect this figure. According to NerdWallet analysis, dwelling coverage is the biggest cost driver in your premium, and underinsurance creates catastrophic gaps. A homeowner with a $300,000 dwelling limit on a $450,000 rebuild faces a $150,000 out-of-pocket loss after a total loss claim.

Assess Your Personal Property and High-Value Items

Next, assess your personal property realistically. If you own high-value items like jewelry, art, or collectibles, these require separate scheduling with appraisals rather than relying on standard sublimits. The Insurance Information Institute confirms that jewelry typically maxes out at $1,500 to $2,500 in standard policies regardless of actual value. Scheduling these items protects you from devastating underinsurance on your most valuable possessions. Without proper scheduling, a $10,000 jewelry collection receives only $2,500 in a claim, leaving you with a $7,500 loss.

Evaluate Your Liability Exposure and Umbrella Options

For liability, evaluate your assets and household composition. A family with children and a swimming pool faces higher exposure than a single adult. Standard limits of $100,000 to $300,000 may leave you vulnerable if a serious injury occurs on your property. Consider an umbrella policy adding $1 million in protection for roughly $150 to $300 annually, far cheaper than defending a major lawsuit without adequate coverage. This additional layer protects your home equity and future earnings from catastrophic liability claims.

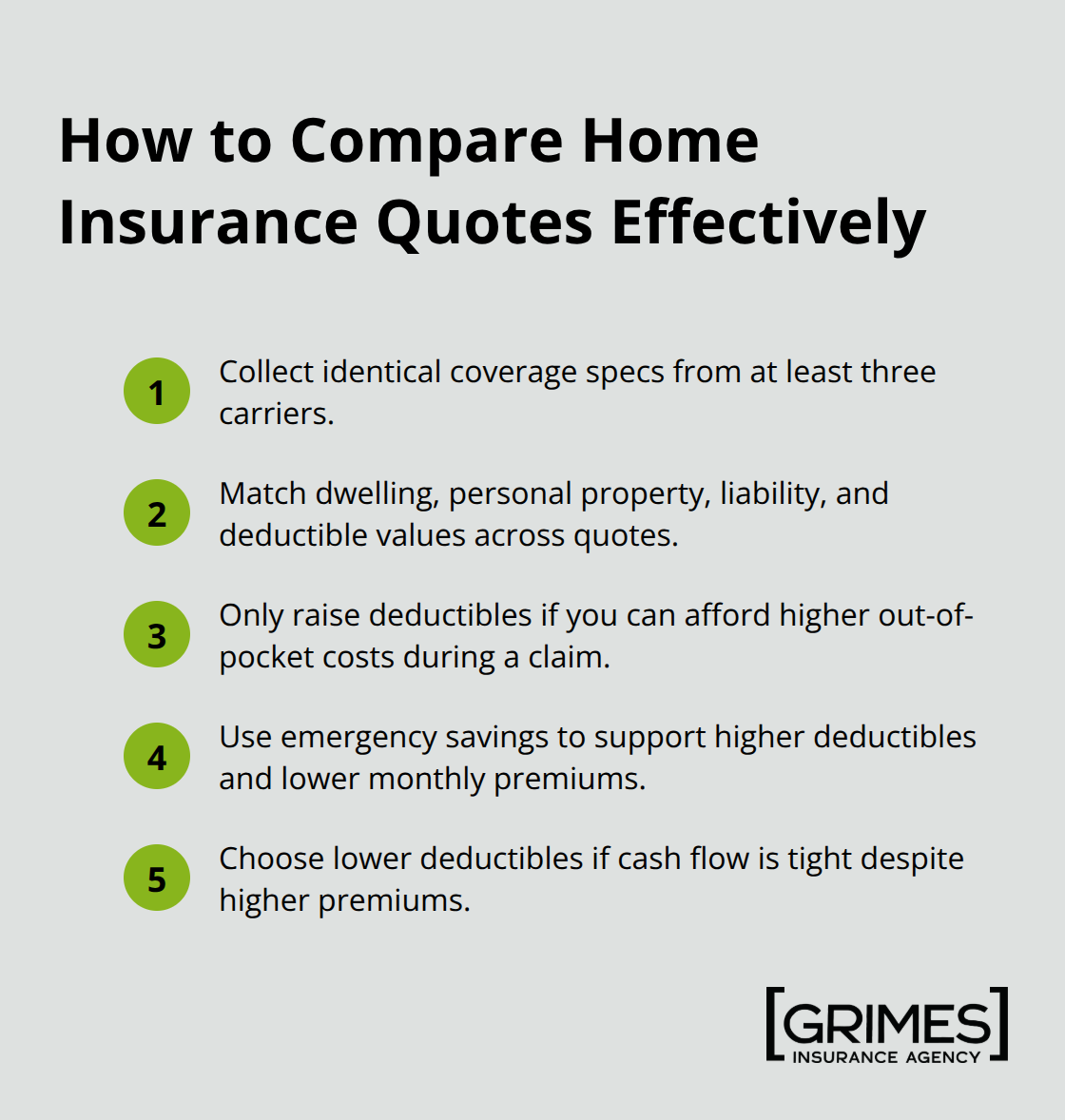

Compare Quotes with Identical Coverage Specifications

Comparing quotes requires gathering identical coverage specifications from at least three carriers before evaluating price. Request quotes with the same dwelling limit, personal property coverage, liability limit, and deductible from each insurer. NerdWallet data shows that raising your deductible from $1,000 to $2,500 saves approximately 9% on average premiums, but this tradeoff only makes sense if you can afford the higher out-of-pocket cost during a claim. Homeowners with solid emergency savings should try higher deductibles to lower monthly costs. Conversely, those living paycheck-to-paycheck need lower deductibles despite higher premiums.

Verify Coverage Details and Lender Requirements

Ask each carrier for itemized breakdowns showing exactly what is covered, excluded, and any sublimits that apply. Some policies include replacement cost for personal property while others pay only actual cash value; this difference can mean recovering $800 for a damaged television versus $300. Verify whether the policy includes automatic inflation adjustment on your dwelling coverage and confirm the claims process timeline. Ensure your policy meets your mortgage lender’s minimum requirements, typically $100,000 liability and a mortgagee clause. After comparing quotes with identical coverage, you can evaluate price differences confidently. A $200 annual premium difference across identical coverage represents genuine savings, but a $200 difference on different coverage levels tells you nothing about value.

Final Thoughts

Understanding home insurance policies in 2026 requires matching your coverage to actual rebuild costs, not purchase prices from years ago. Start by calculating your home’s true rebuild cost using contractor estimates or county assessor data, then schedule high-value items like jewelry or art with appraisals to avoid catastrophic underinsurance. Assess your liability exposure honestly and gather quotes from at least three carriers using identical coverage specifications so you can compare actual value rather than just price tags.

Your current policy deserves annual review because construction costs shift, your home ages, and carrier appetite for risk changes. Check whether your dwelling coverage reflects current rebuild expenses, confirm your personal property limits match your belongings, and verify that your liability limits protect your assets adequately. If your roof approaches ten years old, expect higher premiums or potential denial from standard carriers-this reality shapes your shopping strategy significantly.

We at Grimes Insurance Agency understand that navigating home insurance feels overwhelming, especially when premiums rise faster than your income. Our team has served Lubbock, Texas and surrounding communities with honest guidance and access to multiple carriers for over 75 years. Contact Grimes Insurance Agency to review your current coverage or shop for new protection, and let us help you build confidence in your home insurance decisions.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation