How to Save on Business Insurance Costs: Smart Strategies for Texas Entrepreneurs

Business insurance is one of the largest expenses Texas entrepreneurs face, yet most business owners overpay without realizing it. We at Grimes Insurance Agency work with business owners every day who discover they’re carrying redundant coverage or missing out on available discounts.

The good news is that how to save on business insurance costs doesn’t require cutting corners on protection. With the right strategy and guidance, you can reduce premiums while maintaining the coverage your business actually needs.

What’s Actually Costing You Money in Your Business Insurance

Most Texas business owners haven’t reviewed their insurance policies in years, which means they’re almost certainly overpaying. A Dallas café paid for two separate general liability policies because coverage got duplicated when the owner switched agencies. A San Antonio contractor carried commercial property insurance on equipment he’d sold three years prior. These aren’t edge cases-they’re the norm.

Start by gathering every insurance document you have and listing each policy type, coverage limit, deductible, and annual premium. You’ll likely find that some coverages overlap or that limits don’t match your actual business needs. If you’re paying for a two million dollar general liability aggregate but your lease only requires one million, you’re throwing money away each month. Texas small businesses typically spend about four thousand dollars annually on insurance premiums, but the actual amount varies wildly based on what you’re actually carrying versus what you actually need.

Spot the redundancies that drain your budget

When you review your policies side by side, look specifically for duplicate coverages. If you have a business owners policy that includes general liability and commercial property, and you also carry a standalone commercial property policy, you’re paying twice for the same protection. Workers’ compensation is another area where businesses overpay without knowing it.

In Texas, workers’ comp costs range from fifty cents to fifty dollars per one hundred dollars of payroll depending on your industry risk level, so misclassifying your business or carrying coverage you don’t legally need adds up fast. A Houston salon cut its general liability premium by ten percent by reducing coverage limits to match what state regulations actually required rather than what the previous agent recommended.

Use your claims history to negotiate better rates

Your claims history directly impacts what you pay going forward. Review the last three to five years of claims. If you haven’t filed a claim in that time, mention it when getting quotes-a clean loss history qualifies you for better rates. Conversely, if you’ve had multiple claims, investing in safety programs and risk management now can lower your premiums in the future by demonstrating to insurers that you’re reducing exposure.

The next step involves taking action on what you’ve learned. Once you identify where you’re overpaying and understand your actual risk profile, you can implement strategies that meaningfully reduce your costs without sacrificing the protection your business needs.

How to Cut Your Premium Without Cutting Coverage

Bundle Policies for Immediate Savings

Bundling policies remains the fastest way to lower what you pay each month. A Business Owner’s Policy protects you from liability claims and lawsuits while safeguarding your buildings and equipment into one package. Rather than spreading coverage across multiple insurers, consolidating with one carrier signals stability to underwriters and qualifies you for multi-policy discounts. A Dallas café that bundled its general liability and commercial property policies saved roughly eighteen percent annually, which freed up cash for other business priorities.

When you shop for quotes, always request pricing for a bundled package alongside individual policies so you can see the actual savings. The catch is verifying that a BOP covers your essential risks-some exclude professional liability or commercial auto, which means you’d still need separate policies for those coverages. Ask your agent explicitly what’s included and what gaps remain before committing.

Raise Deductibles Strategically

Raising deductibles works when you have cash reserves to cover a claim. Increasing a commercial property deductible from one thousand to twenty-five hundred dollars typically saves about three hundred dollars annually on premiums. The math is straightforward: insurers charge less because you absorb more risk upfront. However, only raise deductibles on coverages where a claim won’t devastate your business.

Construction firms and retailers with significant inventory should keep property deductibles lower since a fire or theft could mean substantial out-of-pocket costs. Workers’ compensation deductibles work differently than property deductibles-raising them saves less and creates administrative headaches, so this strategy works best for general liability and commercial property only.

Invest in Safety Programs That Lower Claims

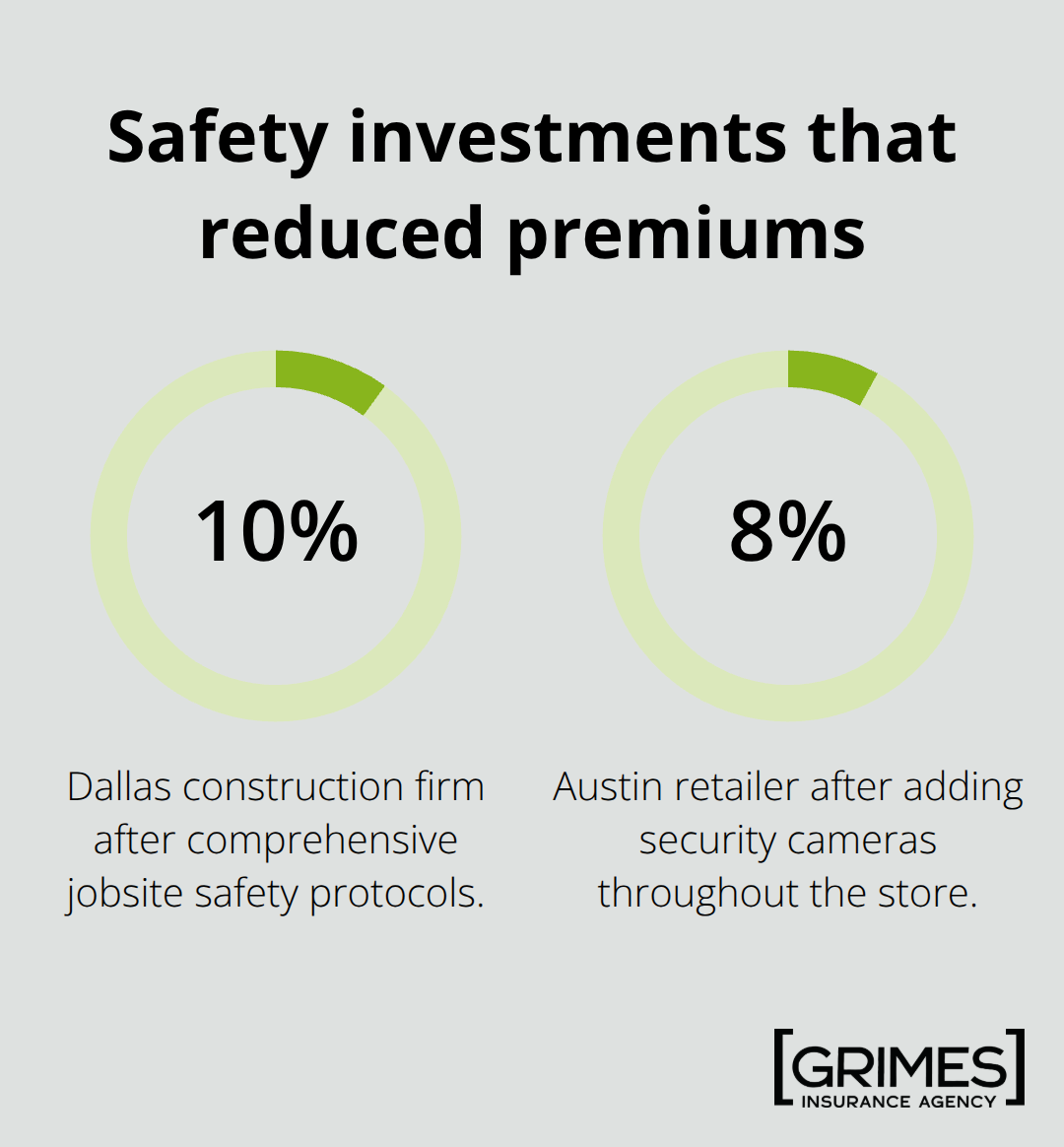

Implementing formal safety programs and loss prevention measures directly reduces what insurers charge because you lower claim frequency. A Dallas construction firm cut its general liability premium by ten percent after installing comprehensive jobsite safety protocols, while an Austin retailer saved eight percent by adding security cameras throughout the store. These investments signal to underwriters that you take preventing losses seriously.

Document your safety efforts through written policies, employee training records, and maintenance logs-insurers want evidence that risk management is systematic, not accidental. The most effective approach combines all three strategies: bundle your core coverages, adjust deductibles strategically based on your cash position, and implement measurable loss prevention programs that you can demonstrate to insurers during renewal. With these fundamentals in place, the next step involves finding an agent who can access multiple carriers and negotiate rates tailored to your specific business profile.

Why Independent Agents Access Better Rates Than Online Quotes

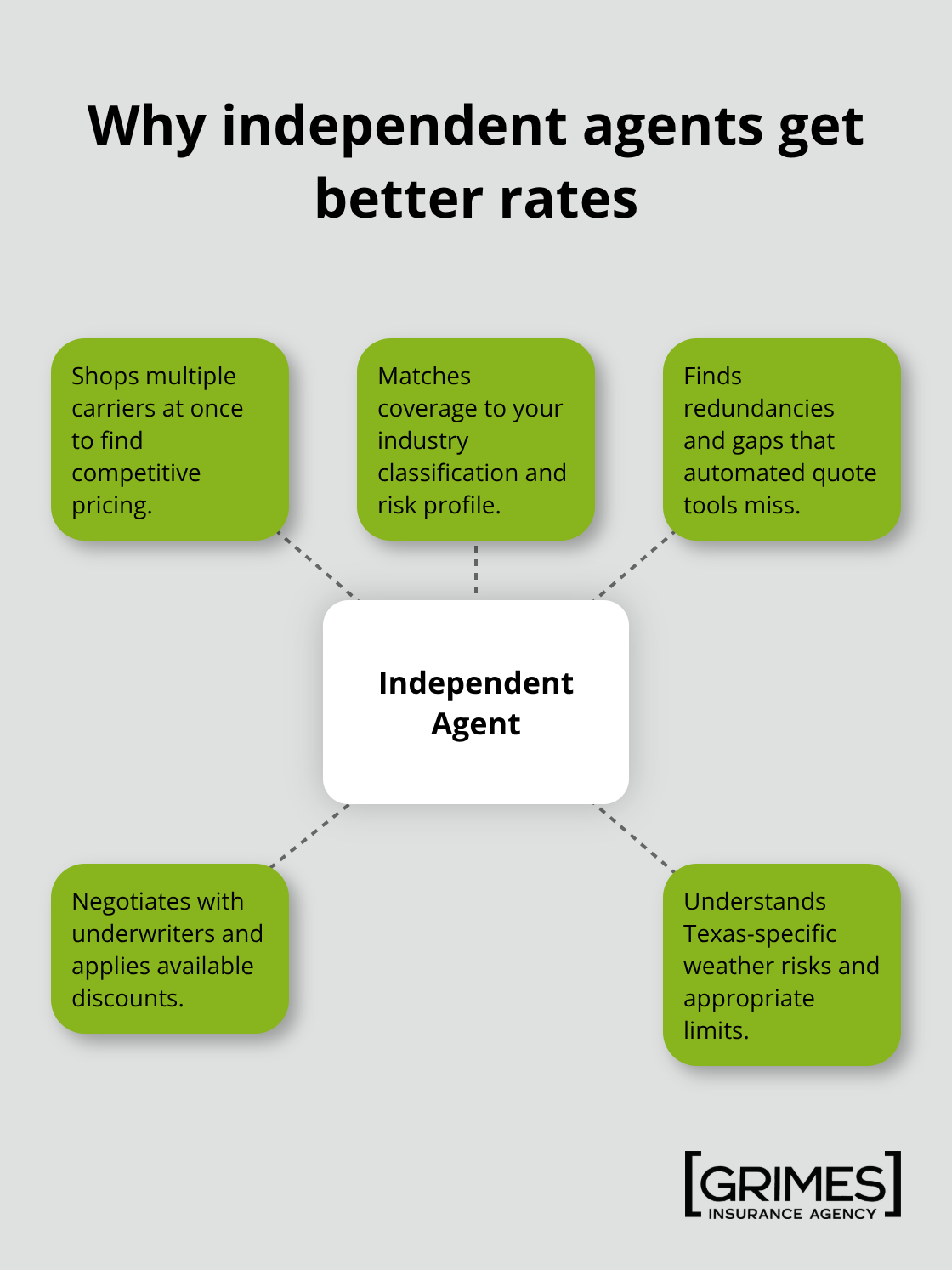

When you compare quotes online or contact a major insurer directly, you see pricing from one company using their underwriting criteria and risk classifications. An independent insurance agent operates differently. Independent agents represent multiple carriers, which means they shop your exact business profile across dozens of insurers simultaneously rather than limiting you to whatever one company decides to charge. A Plano manufacturer who switched from a direct insurer to an independent agent saw a fifteen percent savings on identical coverage by accessing carriers that better suited the company’s specific risk profile.

This matters because insurers price businesses differently based on factors like your industry classification, loss history, and credit score. Misclassify your business or miss a discount you qualify for, and you overpay without knowing better rates exist.

How Independent Agents Identify Hidden Savings

An independent agent conducts a formal risk assessment of your operation and identifies which carriers compete most aggressively for your type of business. They negotiate on your behalf in ways that online quote tools cannot. These tools only show you what they’re programmed to sell, not what actually protects your business. An independent agent catches redundancies and gaps that automated systems miss entirely. A Galveston restaurant saved ten percent on business interruption coverage after an agent tailored the policy to account for the restaurant’s actual seasonal revenue patterns rather than applying a generic formula. Texas businesses face specific risks from hurricanes, hail, and severe weather, which means your coverage limits and deductibles should reflect those exposures and your cash reserves, not some national standard.

The Ongoing Value of an Agent Partnership

An agent reviews your policies annually, adjusts coverage as your business grows or changes, and alerts you when new discounts become available or when competitors offer better rates. A Houston tech startup reduced its annual premium by eighteen percent after an agent identified that the company had purchased redundant professional liability coverage when the existing policy already included the necessary protection. This ongoing partnership costs nothing extra because independent agents earn commission from insurers, not from you. Shop around with at least three independent agents to compare not just pricing but the quality of their recommendations and responsiveness to your questions.

Final Thoughts

Reducing your business insurance costs comes down to three actions: understanding what you currently pay, implementing strategies that lower premiums without sacrificing protection, and partnering with someone who can access better rates than you’d find alone. Texas business owners who save the most money aren’t cutting corners on coverage-they’re eliminating waste and working with agents who represent multiple carriers. A Houston salon saved ten percent, a Dallas café saved eighteen percent, and a Plano manufacturer saved fifteen percent when they took a systematic approach to how to save on business insurance costs.

Your claims history matters more than you might think, and a clean loss history qualifies you for better rates. Raising deductibles on coverages where you have cash reserves typically saves three hundred dollars annually on commercial property alone, while bundling general liability and commercial property into a Business Owner’s Policy saves roughly fifteen to twenty-five percent compared to separate policies. Annual policy reviews catch gaps and redundancies that you’d miss on your own, and an agent negotiates with carriers on your behalf while alerting you when better rates become available.

We at Grimes Insurance Agency represent multiple carriers, which means we can shop your business profile across dozens of insurers to find rates tailored to your specific risk profile and industry. Contact us today for a free policy review and competitive quotes that reflect what your business actually needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation