Commercial Property Insurance Tips: Smart Ways to Guard Your Assets

Your commercial property is likely your biggest business investment. Yet many business owners carry inadequate coverage or miss critical protection gaps that could cost them thousands.

We at Grimes Insurance Agency help business owners understand commercial property insurance tips that actually protect their assets. This guide walks you through coverage types, common policy gaps, and how to build a protection plan that fits your business.

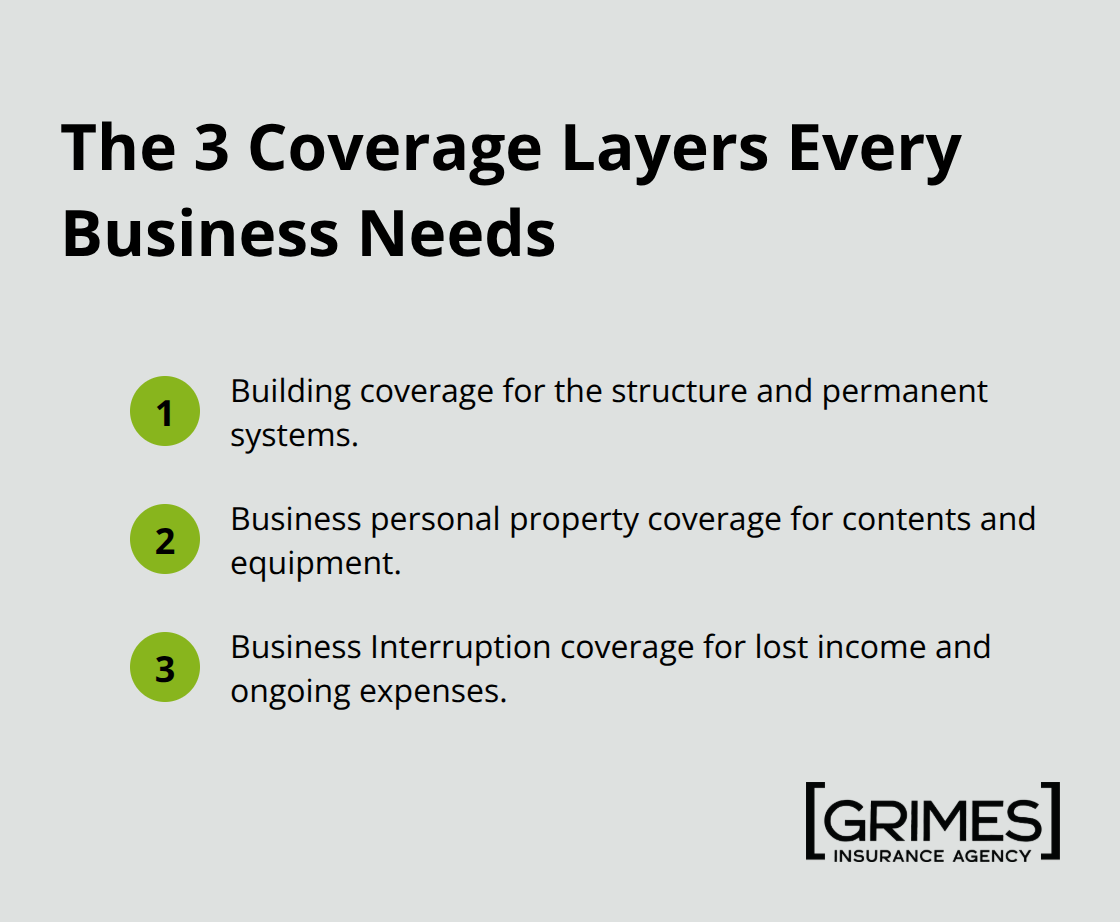

What Three Coverage Types Should Your Business Actually Have

Your building sits empty after a fire, but your rent and payroll don’t stop coming. Your inventory floods, yet you still owe suppliers for stock you can no longer sell. These scenarios play out constantly because business owners misunderstand what commercial property insurance actually covers. Building protection alone leaves your operations vulnerable. Most businesses need three distinct coverage layers working together: protection for the physical structure itself, coverage for everything inside it, and income protection when disaster forces you to close temporarily.

The Building and Its Permanent Systems

Your building coverage protects the structure and anything permanently attached to it-the roof, walls, electrical wiring, plumbing, HVAC systems, and built-in fixtures. This is non-negotiable if you own the property. The coverage pays to repair or rebuild these elements after a covered loss. You need to know your building’s replacement cost, not its market value. These are completely different numbers. A building worth $500,000 on the real estate market might cost $750,000 to rebuild at current construction prices. If you have a $500,000 building but only insure it for $350,000 and a fire causes $400,000 in damage, coinsurance penalties can reduce your payout dramatically. You must obtain a professional property appraisal to establish accurate replacement costs. Do this when you first obtain coverage, after major renovations, and every 3 to 5 years as construction costs change.

Protecting What’s Inside

Business personal property coverage protects everything that isn’t permanently attached: furniture, computers, inventory, equipment, machinery, and supplies. This coverage travels with your business if you move. Many owners assume their building policy covers these items-it doesn’t. This is where real losses happen. A restaurant loses $50,000 in kitchen equipment and inventory in a fire. A retail store’s entire stock vanishes in a flood. A contractor’s tools worth $100,000 sit stolen from a job site. Without adequate personal property coverage, you absorb these costs yourself. Replacement Cost Value coverage is the only sensible choice here. It pays what it costs to replace items new at today’s prices. Actual Cash Value coverage subtracts depreciation, leaving you short when you need to rebuild. Track what you own through a detailed inventory with photos and purchase receipts. Update this list annually or whenever you add significant equipment or inventory. Equipment and tools require special attention if your business operates off-site. Inland Marine coverage extends protection to property away from your main location-tools at job sites, equipment in transit, or inventory stored elsewhere. This isn’t optional for contractors or service businesses.

Income Protection When Operations Stop

Loss of income insurance, called Business Interruption coverage, pays your lost profits and ongoing operating expenses when a covered disaster forces you to close temporarily. This is the coverage most business owners overlook, yet it’s often the most financially devastating loss they face. When a severe storm damages your building and you’re closed for three months, your revenue disappears but your rent, utilities, insurance, and employee salaries don’t. Business Interruption coverage pays these continuing expenses plus lost profits, typically for up to 12 months. Extra Expense coverage works alongside it, paying the additional costs you incur to minimize downtime-renting temporary space, expedited repairs, or equipment rental. For a manufacturing business closed for four months, this coverage could mean the difference between survival and bankruptcy. Calculate your daily operating expenses and monthly profit to determine appropriate limits. Most businesses significantly underestimate these numbers. The premium for Business Interruption coverage is modest compared to its protection value, typically 5 to 15% of your property premium depending on your business type and closure risk.

Identifying Your Coverage Gaps

Now that you understand what these three layers cover, the next step involves assessing which gaps exist in your current policy. Many business owners carry policies that protect the building but leave personal property and income unprotected. Others have adequate building and contents coverage but no Business Interruption protection. The only way to know where you stand is to review your actual policy documents and compare them against your real business assets and operating expenses.

Where Coverage Actually Falls Short

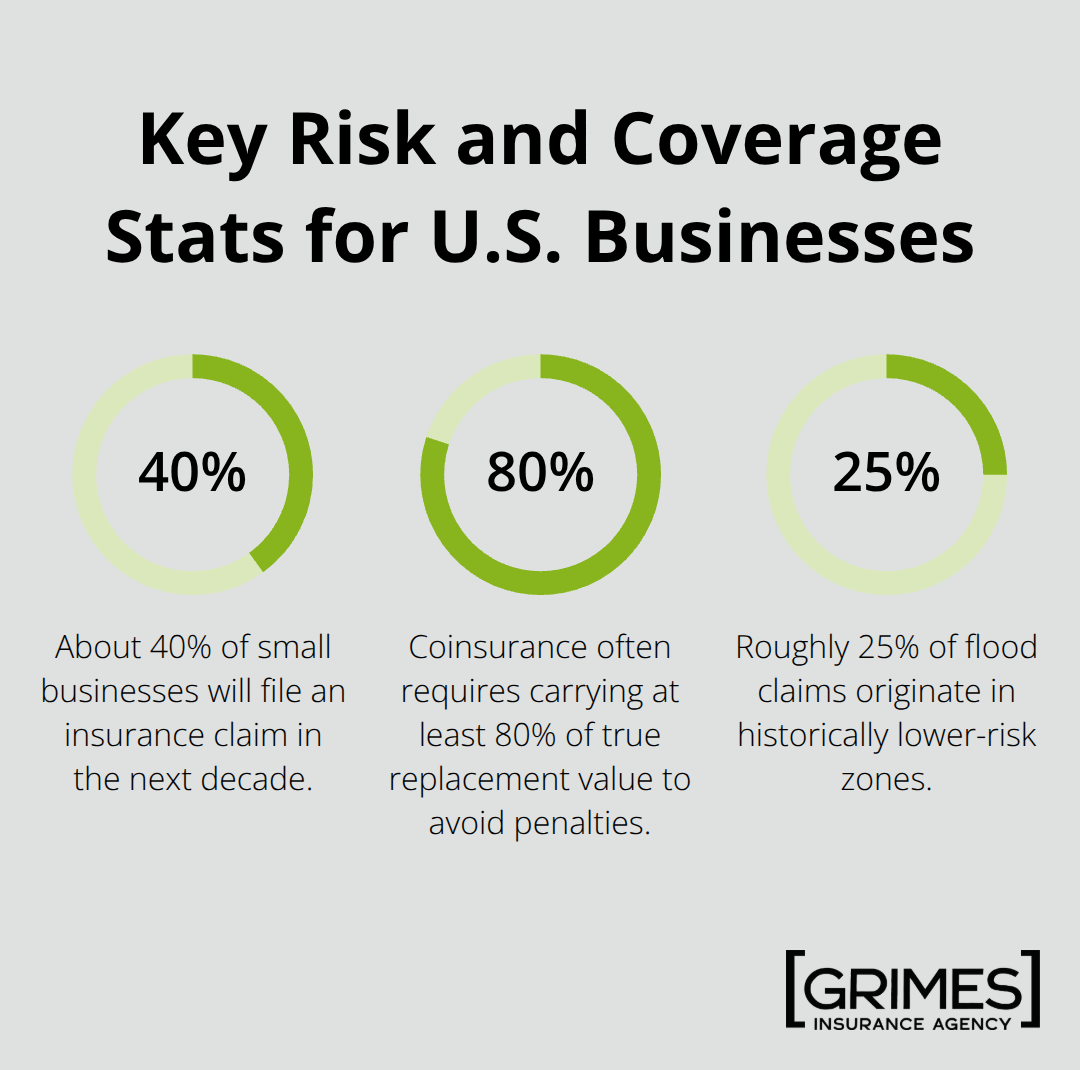

Most business owners discover their coverage gaps only after a loss occurs. A client files a claim expecting full reimbursement, only to learn their policy limits fall far short of actual damage costs. The problem stems from three distinct failures in how policies are purchased and maintained. First, business owners underestimate what their assets actually cost to replace. Second, they ignore standard policy exclusions that leave major disaster types completely unprotected. Third, they assume their general property coverage extends to equipment and inventory that require specialized protection. These gaps aren’t accidental oversights-they’re the direct result of policies purchased without proper asset valuation or professional risk assessment. About 40% of small businesses will file an insurance claim in the next decade, and most of those filing claims discover they’re significantly underinsured. The financial consequences are severe: when your building reconstruction cost is $800,000 and your coinsurance is 80%, you need at least $640,000 in coverage to avoid penalties that can reduce your payout significantly.

The Replacement Cost Trap

The underinsurance problem starts with replacement cost confusion. You might know your building’s market value but have no idea what it costs to rebuild at current prices. Construction costs in 2025 remain elevated, and many owners base coverage limits on valuations from five or ten years ago. When you file a claim, the insurer calculates your coinsurance penalty based on whether you carried 80% to 100% of true replacement value-and most businesses fail this test. A professional property appraisal establishes what your building actually costs to rebuild, not what it sells for on the real estate market. These numbers diverge significantly. Conduct this appraisal when you first obtain coverage, after major renovations, and every three to five years as construction costs shift.

Natural Disasters Leave You Exposed

Natural disasters create a second gap: floods, earthquakes, and earth movement are almost universally excluded from standard commercial policies. NOAA reported that 2024 produced 24 weather and climate disasters causing losses exceeding $1 billion each, with severe storms alone driving over $30 billion in U.S. insurance claims. Yet most business owners carry no separate flood coverage whatsoever. Coastal and riverfront properties face particularly acute risk, with about 25% of flood claims originating in historically lower-risk zones. Obtain separate flood insurance through the National Flood Insurance Program or private providers. This protection isn’t optional if your property sits in any flood-prone area-and many properties face risk that owners never anticipated.

Equipment and Inventory Gaps Go Unnoticed

Equipment and inventory gaps represent the third major failure. Contractors store $80,000 in tools off-site with no Inland Marine coverage. Retailers stock inventory that isn’t properly valued on their personal property endorsement. Manufacturers assume their equipment coverage extends to tools and machinery stored at job sites. These assumptions cost businesses thousands in unprotected losses annually. Document all equipment and inventory with current replacement costs, then verify these values appear on your actual policy documents. Inland Marine coverage specifically protects property away from your main location-tools at job sites, equipment in transit, or inventory stored elsewhere. Without this endorsement, your off-site assets sit completely unprotected.

Taking Action on What You’ve Learned

Your next step involves moving beyond understanding these gaps and actually assessing your own coverage. This requires pulling your current policy documents and comparing them against your real business assets, operating expenses, and disaster exposures. The following chapter walks you through how to conduct this assessment with professional guidance and build a protection plan that actually fits your business.

Building Your Asset Inventory and Setting Real Coverage Limits

Start with what you actually own. Pull out every invoice, receipt, and equipment list from the past five years. Document your building’s square footage, construction materials, age, and systems. List every piece of equipment, machinery, furniture, and inventory with its purchase date and cost. Take photos of everything. This isn’t busywork-it’s the foundation that prevents massive coverage gaps. Many businesses underestimate their property values by more than 30%, leaving significant coverage gaps. When you underestimate replacement costs, your coinsurance penalties eliminate thousands in coverage you thought you had. A manufacturing facility with $2 million in actual replacement value but only $1.4 million in coverage faces a coinsurance penalty that could reduce a $500,000 claim to $350,000. The gap costs money you’ll never recover.

Get Your Building Appraised Professionally

For your building specifically, obtain a professional property appraisal from a licensed appraiser who understands replacement cost valuation, not just market value. Construction costs in 2025 remain elevated compared to pre-2020 levels, making old appraisals dangerously inaccurate. Schedule this appraisal when you first obtain coverage, after any major renovations or system upgrades, and every three to five years as construction material and labor costs shift. Your appraiser should provide separate values for the building structure, electrical systems, plumbing, HVAC, and any specialized equipment permanently installed. Use these specific numbers when purchasing coverage, not round estimates.

Document Personal Property and Equipment Values

For personal property and equipment, create detailed spreadsheets organized by category: furniture and fixtures, computers and technology, machinery, tools, inventory, and signage. Include purchase dates, original costs, and current replacement values. Equipment depreciates, but your insurance should pay replacement cost value, not what the used item would fetch. A five-year-old commercial oven doesn’t cost less to replace just because it’s older-you still pay full price for a new one. Verify that your policy documents specifically list coverage limits for each category and that these limits match your actual values. Many policies contain generic limits that fall far short of reality.

Protect Off-Site Assets and Equipment

If you operate off-site-contractors with job sites, service businesses with equipment in vehicles, retailers with satellite locations-ensure your Inland Marine coverage explicitly covers these locations and asset types with adequate limits. Off-site assets sit completely unprotected without this endorsement. Review your Business Interruption coverage limits by calculating your actual monthly operating expenses including rent, utilities, payroll, insurance, and loan payments, then add your average monthly profit. Most businesses discover they’ve insured only 60% of their true exposure. The premium difference between insuring $30,000 monthly and $50,000 monthly in business interruption is minimal, typically $200 to $400 annually, yet the protection gap could bankrupt you after a major loss.

Work with an Insurance Professional for Detailed Assessment

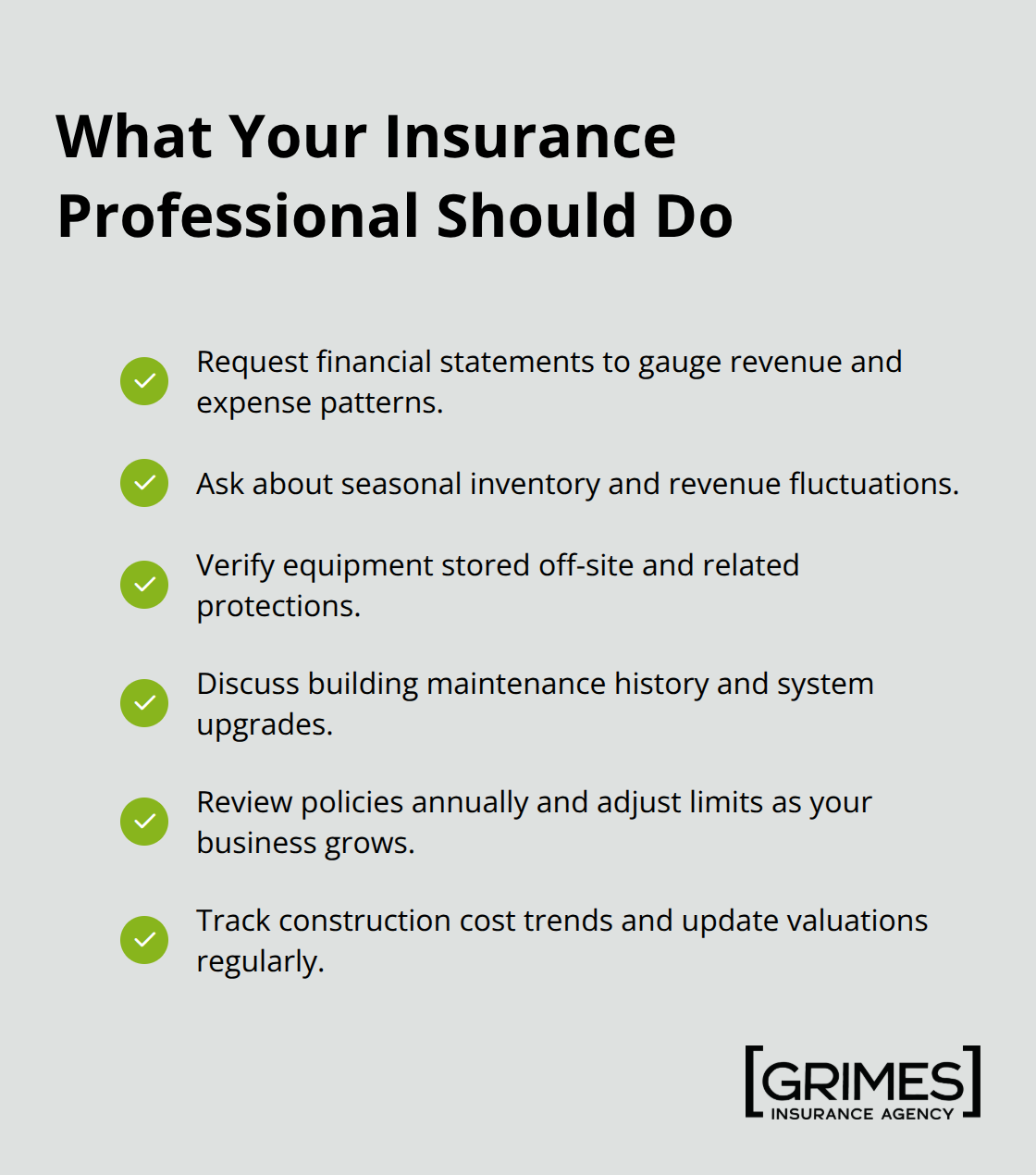

Once you’ve documented everything, work with an insurance professional who asks detailed questions about your operations rather than simply processing an application. A broker or agent should request your financial statements, ask about seasonal fluctuations in inventory or revenue, inquire about equipment stored off-site, and discuss your building’s maintenance history. They should also review your current policy annually and adjust limits upward as your business grows or construction costs increase. This ongoing relationship prevents the common mistake of purchasing coverage once and never updating it, leaving you increasingly underinsured year after year.

Final Thoughts

Your commercial property represents years of investment and hard work. Protecting it requires more than a standard policy purchased years ago and forgotten. The commercial property insurance tips covered throughout this guide point to one clear reality: most business owners leave themselves dangerously exposed through underinsurance, unaddressed exclusions, and coverage gaps that only surface after a loss occurs. About 40% of small businesses will file an insurance claim within the next decade, and when that claim arrives, you’ll discover whether your coverage actually protects your assets or leaves you absorbing massive losses yourself.

Pull your current policy documents and compare them against the three coverage layers discussed here: building protection, personal property coverage, and business interruption insurance. Conduct a professional property appraisal to establish accurate replacement costs. Document everything you own with photos and current values, calculate your true monthly operating expenses and lost profit exposure, and verify that your Inland Marine coverage protects off-site equipment and inventory. The difference between proper coverage and gaps often amounts to thousands of dollars in unrecovered losses.

We at Grimes Insurance Agency understand that commercial property protection requires more than processing applications. Our team conducts detailed assessments of your actual business operations, equipment, inventory, and income exposure to help you build protection plans that fit your specific risks rather than generic policies that leave gaps. Contact Grimes Insurance Agency to schedule a comprehensive coverage review and ensure your assets receive the protection they deserve.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation