Umbrella Liability Coverage Meaning: What It Really Does for Your Business

Your primary business insurance has limits. When a lawsuit or claim exceeds those limits, you’re exposed to serious financial risk.

Umbrella liability coverage meaning is straightforward: it’s extra protection that kicks in when your standard policies max out. We at Grimes Insurance Agency help business owners understand how this coverage works and why it matters for protecting what you’ve built.

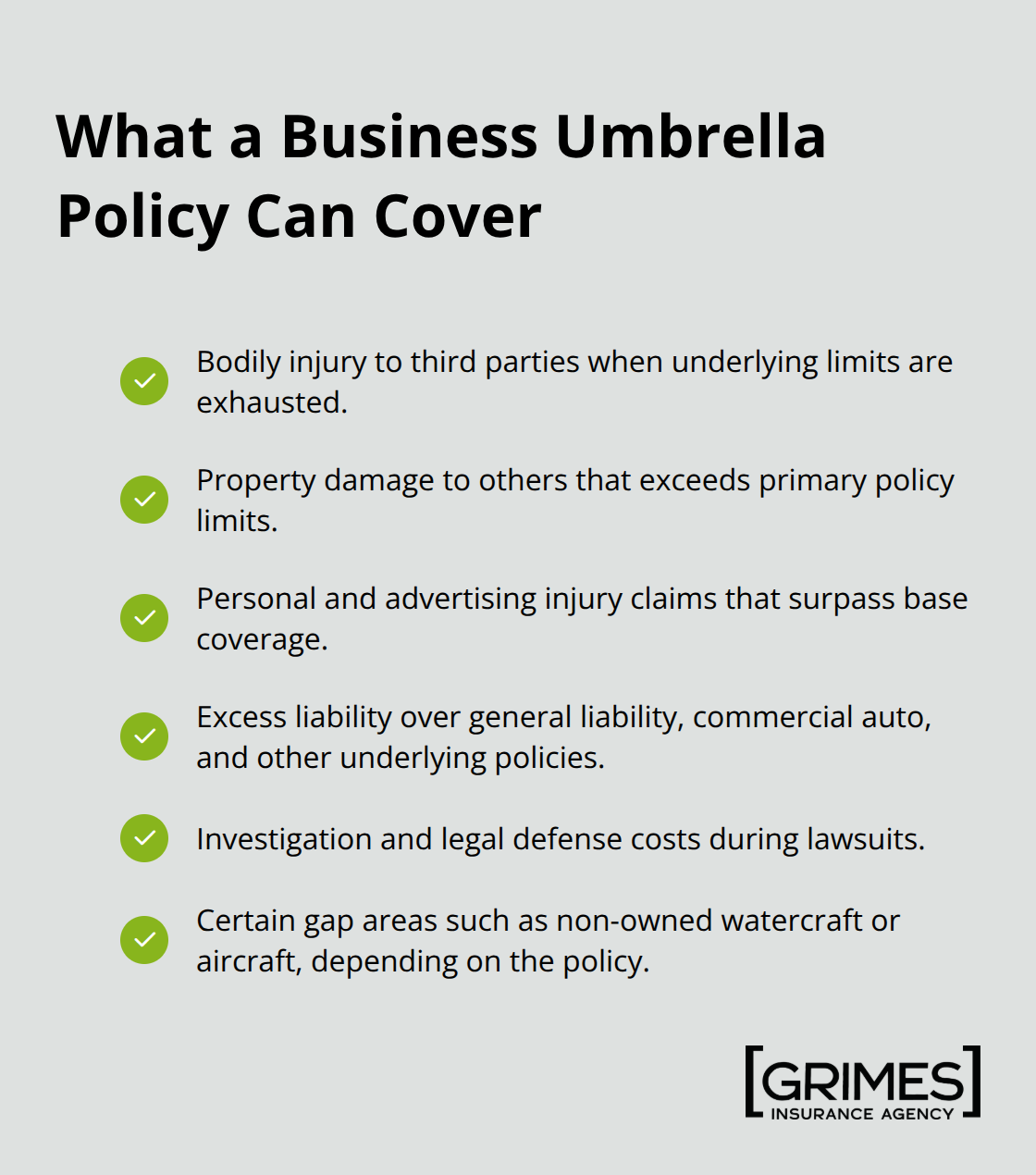

What Your Umbrella Policy Actually Covers

Umbrella liability coverage sits on top of your existing policies and activates only after those primary policies reach their limits. This matters because a single lawsuit can easily exceed what your general liability, commercial auto, or other standard policies provide. When that happens, your business absorbs the excess cost directly, which can devastate your assets and operations.

Umbrella policies cover the same types of claims as your underlying policies: bodily injury, property damage, personal injuries, and advertising injuries. If a customer is injured on your property and wins a $2.5 million judgment while your general liability maxes out at $1 million, your umbrella steps in to cover that remaining $1.5 million. According to the Insurance Information Institute, the average product liability award reaches $7.1 million, which underscores why this extra layer of protection matters for most businesses.

Where Your Umbrella Actually Kicks In

Your umbrella only responds after your primary policies are exhausted on a per-occurrence basis. If you carry a $1 million general liability policy and face a $2 million claim, your GL policy pays the first $1 million and your umbrella covers the additional $1 million. The umbrella also covers investigation and defense costs if a claim goes to court, which can run into hundreds of thousands of dollars before a settlement or verdict is reached. One critical distinction: umbrella coverage does not create new protections beyond what your underlying policies already cover. If your general liability excludes certain activities, your umbrella will not cover those same activities either. However, umbrella policies can fill specific gaps that your primary policies leave open, such as non-owned watercraft, non-owned aircraft, and certain advertising liabilities that standard GL policies often exclude.

What Umbrella Does Not Cover

Umbrella coverage explicitly does not protect professional liability or malpractice claims. If you run a consulting firm, accounting practice, or medical office, raising your umbrella limits will not increase protection for professional errors. You need separate professional liability insurance for that exposure. Umbrella also does not cover physical damage to your own vehicles or property-it only covers third-party liability. A $5 million umbrella policy will not pay to repair your company truck if it’s damaged in an accident; your commercial auto physical damage coverage handles that. Understanding these boundaries prevents you from thinking you have coverage you actually do not have.

How Much Coverage You Actually Need

The right umbrella limit depends on your industry, business size, and asset exposure. Restaurants, retail stores, event venues, and contractors on high-liability projects face greater exposure and typically need higher limits. Your net worth, annual revenue, and the frequency of customer contact all influence how much protection makes sense. Most small businesses carry about $2 million per occurrence and $4 million aggregate on underlying policies before adding umbrella coverage. From there, you can add $1 million to $10 million in umbrella protection, depending on your risk profile. The cost remains reasonable-commercial umbrella insurance typically runs about $40 per month for each additional $1 million of coverage, making it an affordable way to protect what you’ve built.

When Umbrella Coverage Stops a Lawsuit from Destroying Your Business

A slip-and-fall on your retail floor sends a customer to surgery. The medical bills alone reach $400,000, but the plaintiff’s attorney demands $1.8 million for pain and suffering, lost wages, and permanent disability. Your general liability policy caps out at $1 million. Without umbrella coverage, you’re personally liable for that remaining $800,000-money that comes directly from your business assets, your home equity, or forced asset sales.

This scenario plays out regularly in American courts. According to Thomson Reuters data, the average product liability award reaches nearly $6.4 million, yet most small businesses carry general liability limits between $1 million and $2 million. The gap between what you’re covered for and what juries award creates real financial exposure. Umbrella liability steps in precisely when these gaps matter most.

How Umbrella Covers the Gaps That Destroy Unprepared Businesses

A contractor works on a commercial renovation and accidentally damages the building’s electrical system, causing a fire that spreads to adjacent properties. The total property damage claim reaches $3.2 million. The contractor’s commercial general liability maxes out at $2 million, leaving a $1.2 million shortfall. An umbrella policy with $5 million in coverage absorbs that excess without forcing the contractor into bankruptcy or asset liquidation.

Defense costs alone-expert witnesses, depositions, attorneys’ fees-often exceed $200,000 before a case settles. Your umbrella covers these investigation and defense expenses, which means your business cash flow stays intact while the claim gets resolved.

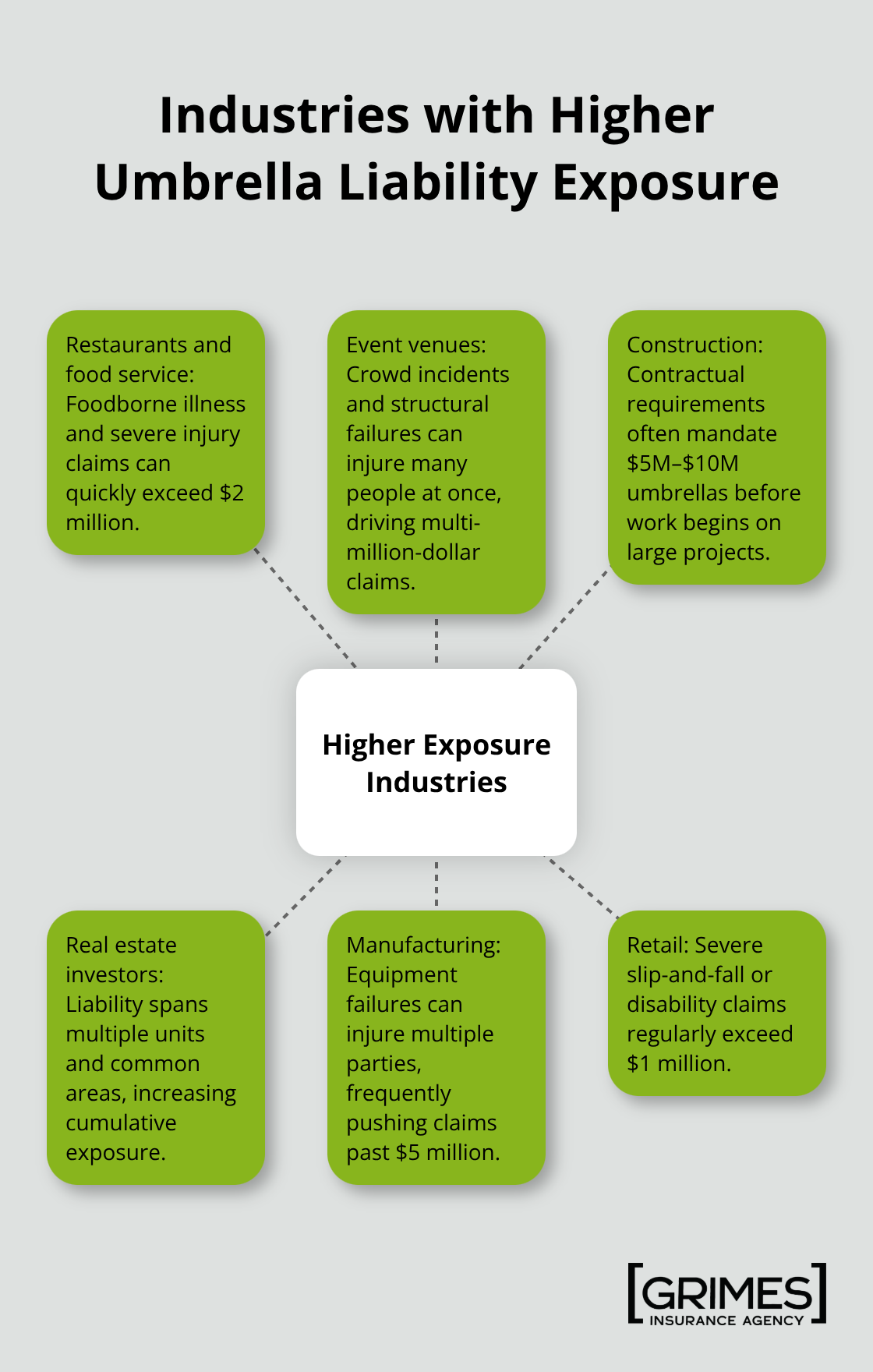

Why Your Industry Determines Your Real Exposure

Restaurants face exposure that retail stores don’t. A customer suffers severe food poisoning that triggers a lawsuit claiming permanent digestive damage and lost earning capacity. The settlement reaches $2.5 million. Restaurants typically carry $1 million to $2 million in general liability, creating immediate vulnerability.

Event venues that host concerts or festivals face crowd-related injuries. A structural failure or crowd crush incident injures dozens of people simultaneously, pushing claims well into the millions. Construction firms working on large commercial projects often face contractual requirements from property owners demanding $5 million or $10 million in umbrella coverage before work begins. These aren’t optional protections-they’re contractual necessities.

Where Umbrella Protection Matters Most Across Industries

Real estate investors renting multiple properties encounter liability across all their units. A tenant’s guest suffers injury in a common area, and the injury claim exceeds your per-property coverage limits. Manufacturing operations use machinery that can malfunction and cause injury. A single equipment failure injures multiple workers or third parties and generates claims exceeding $5 million easily.

The cost of umbrella coverage-roughly $40 per month per additional $1 million-becomes negligible when you understand what a single major claim costs your business. Most businesses that skip umbrella coverage don’t face claims for years, then get hit with one lawsuit that wipes out a decade of profits or forces asset sales they never anticipated.

Understanding your specific industry risk is only the first step. The next critical decision involves calculating exactly how much umbrella coverage your business actually needs to match your assets, revenue, and operational exposure.

How Much Coverage Your Business Actually Needs

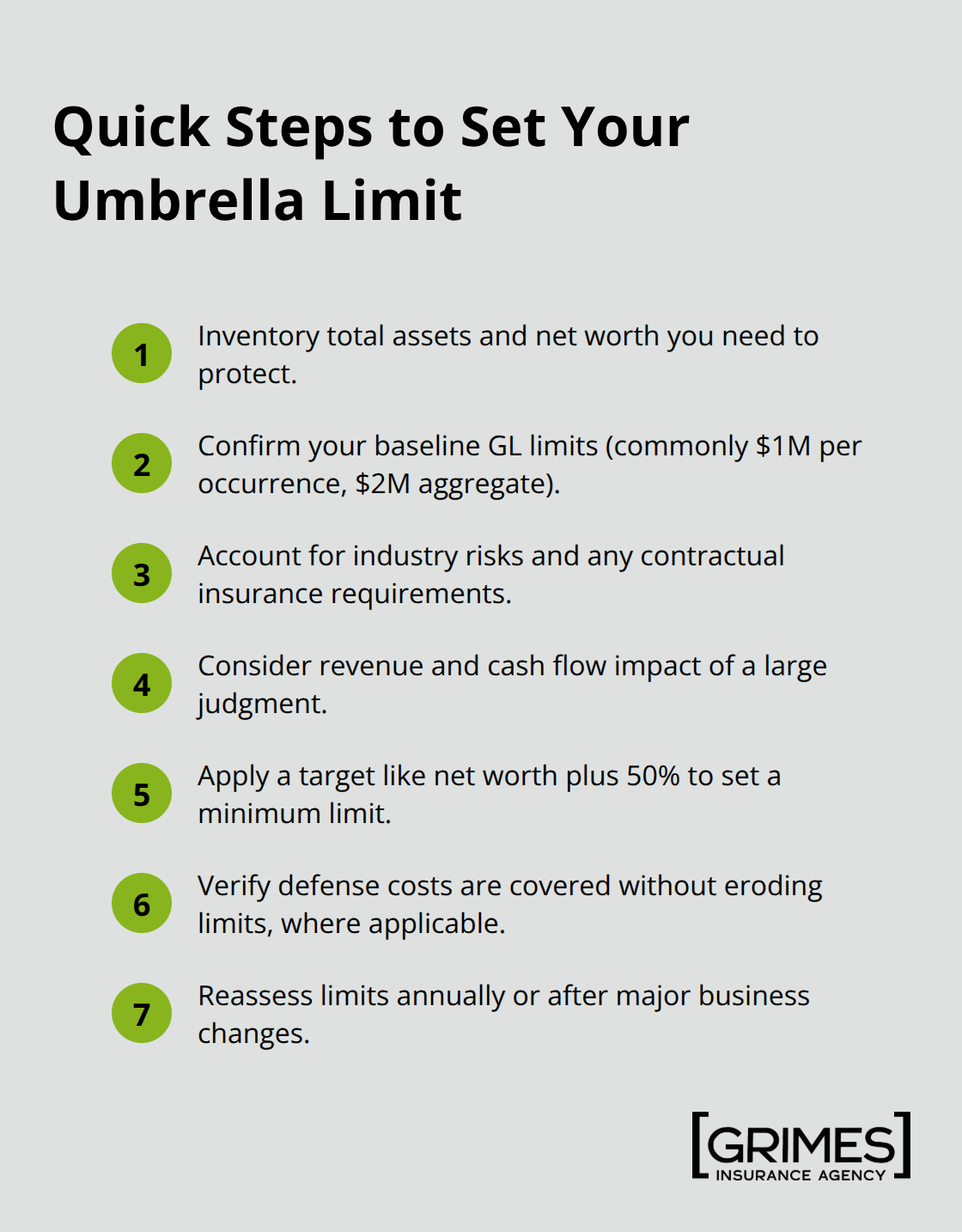

Your industry determines your baseline exposure, and your assets determine your ceiling. A restaurant operator with $500,000 in net worth faces different umbrella needs than a commercial contractor with $5 million in equipment and real estate holdings. Start by identifying what you actually stand to lose if a major lawsuit hits. Your net worth-buildings, equipment, savings, investment accounts-represents the financial target a plaintiff’s attorney will pursue after your primary policies max out. Most businesses underestimate this number significantly.

A $2 million net worth business carrying only $1 million in general liability and no umbrella coverage leaves $1 million completely exposed to a single slip-and-fall or product liability claim. Most small business owners choose general liability coverage limits of $1 million per occurrence and $2 million aggregate for each policy period. From that baseline, you can add $1 million to $10 million in umbrella limits depending on your specific situation. The math matters here: a $5 million umbrella typically costs about $375 to $525 per year, while a $10 million policy runs roughly $2,200 to $2,500 annually. That works out to roughly $40 per month for each additional $1 million of coverage.

Your Industry’s Claims History Shapes Your Coverage Needs

Restaurants and food service operations face product liability exposure that most business owners ignore until a foodborne illness claim arrives. A customer hospitalized for severe food poisoning can generate settlement demands exceeding $2 million when permanent digestive damage is claimed. Event venues hosting crowds face concentrated injury risk-a structural failure or crowd incident injures multiple people simultaneously, multiplying liability exposure instantly.

Construction firms working commercial projects face contractual requirements from property owners demanding $5 million to $10 million in umbrella coverage before a shovel touches ground. These aren’t optional recommendations; they’re lease and contract prerequisites. Real estate investors with multiple rental properties need umbrella coverage that reflects cumulative exposure across all units. A single injury in a common area or tenant space can trigger claims exceeding per-property coverage limits.

Manufacturing operations using industrial equipment face machinery malfunction exposure that generates claims in the millions. Manufacturing injury claims involving multiple workers or permanent disability frequently exceed $5 million. Retail operations encounter slip-and-fall exposure and customer injury claims that regularly exceed $1 million when serious injury or permanent disability is involved.

Assets and Revenue Determine Your Real Exposure Level

A business with $10 million in annual revenue and $3 million in assets should carry substantially more umbrella coverage than a business with $1 million in revenue and $500,000 in assets. Your gross annual revenue represents earning potential that a judgment could claim through wage garnishment or forced business asset sales. A $3 million judgment against a $1 million revenue business essentially forces liquidation. A $3 million judgment against a $10 million revenue business is serious but potentially manageable.

Your tangible assets-real estate, equipment, vehicles, inventory-represent the direct target of asset recovery. A contractor with $2 million in owned equipment and $1 million in real estate owns $3 million worth of seizeable assets. That contractor needs umbrella coverage that protects that $3 million minimum. Try aligning your umbrella limit with your total net worth plus 50 percent.

A business with $2 million in net worth should carry $3 million in umbrella coverage minimum. A business with $5 million in net worth should carry $7.5 million minimum. This approach prevents a catastrophic claim from forcing asset liquidation or bankruptcy.

Claims History and Risk Profile Affect Your Rates

Your claims history influences what carriers will offer and at what price. A business with zero claims over five years qualifies for better rates than a business with two claims in the same period. If you operate in a high-risk industry (construction, food service, events), your umbrella costs increase compared to lower-risk operations like professional services or office-based businesses. Carriers assess your specific operational exposure, not just industry averages, when pricing umbrella coverage.

Final Thoughts

Umbrella liability coverage meaning comes down to one reality: it protects your business when standard policies fail. Average product liability awards reach nearly $6.4 million according to Thomson Reuters data, yet most small businesses carry general liability limits between $1 million and $2 million. That gap represents real money that comes directly from your pocket if a major claim hits, making umbrella protection an affordable safeguard (a $5 million umbrella policy costs roughly $375 to $525 annually).

Start evaluating your coverage gaps today by identifying your industry’s typical claim exposure, your total net worth and business assets, and any contractual requirements from clients or landlords for higher liability limits. Most businesses should carry umbrella coverage equal to at least their total net worth, with higher-risk industries like restaurants, construction, and event venues needing substantially more protection. An independent insurance agent understands your specific business operations and matches you with carriers offering the right limits at competitive rates.

We at Grimes Insurance Agency have helped business owners across Lubbock find the right coverage combinations that actually protect what they’ve built. Contact us today to review your current coverage and identify whether umbrella liability protection fits your business needs. A single conversation could prevent a catastrophic claim from destroying years of hard work.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation