Home Insurance Basics for Homeowners: A Comprehensive Overview

Homeownership comes with real financial responsibility, and home insurance is the foundation of protecting your investment. At Grimes Insurance Agency, we’ve helped countless homeowners understand the home insurance basics they need to make confident decisions.

This guide walks you through what coverage actually protects you, what factors shape your rates, and how to pick a policy that fits your situation.

What Your Home Insurance Actually Protects

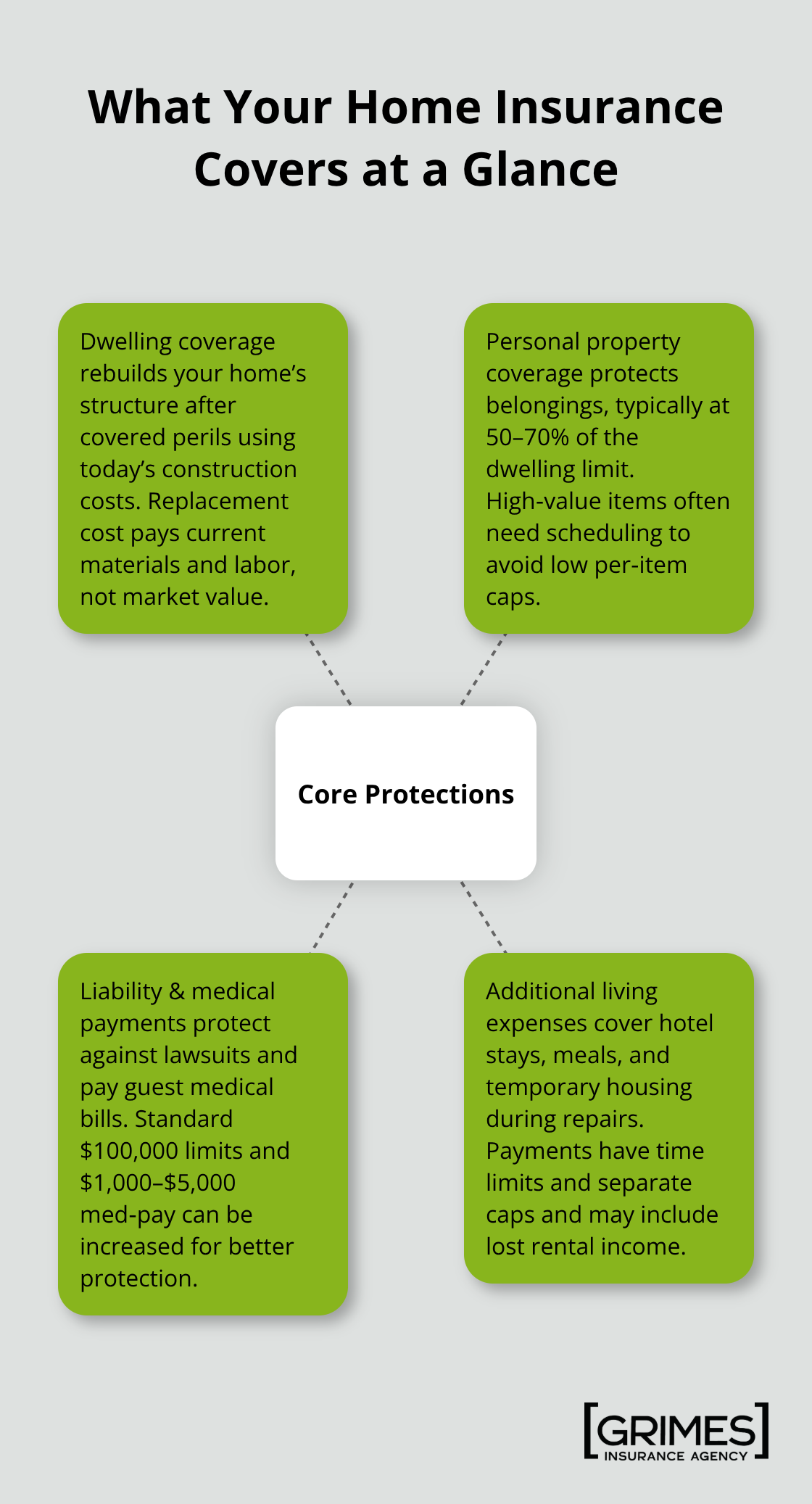

Your homeowners policy typically covers four core protections, and understanding exactly what each one does prevents costly coverage gaps. Dwelling coverage rebuilds your home’s structure after fire, wind, hail, or lightning damage-but the amount matters far more than most homeowners realize. You need enough to rebuild at today’s construction costs, not your home’s market value, since land isn’t covered and rebuilding expenses have climbed significantly. According to the Insurance Information Institute, replacement cost coverage pays what it actually costs to rebuild using current materials and labor rates, which differs sharply from what your home would sell for.

Wind and hail cause roughly 42.5% of homeowners insurance losses, while water damage and freezing account for 22.6%, so your dwelling limit should reflect these real rebuilding expenses in your area. Personal property coverage typically sits at 50–70% of your dwelling limit and protects your belongings if they’re stolen or destroyed, though this standard percentage often falls short for households with valuable items.

High-Value Items Need Extra Protection

High-value items like jewelry, art, antiques, and collectibles hit coverage caps-usually around $500 per item-unless you add a scheduled personal property endorsement with appraisals to document true worth. Off-site coverage for items taken outside your home frequently caps at roughly 10% of your personal property limit, so items stolen while traveling may receive less protection than you’d expect. This gap means you should obtain appraisals for expensive possessions and insure them with a rider that reflects their appraised value.

Liability and Medical Coverage Work Differently

Liability protection covers lawsuits when someone is injured on your property or you accidentally damage someone else’s property, and the standard $100,000 limit often proves insufficient for meaningful asset protection. No-fault medical coverage pays a guest’s medical bills immediately if they’re injured in your home, typically ranging from $1,000 to $5,000, regardless of who caused the accident. This coverage excludes your own family members and pets, so it only helps visitors.

Additional Living Expenses and Temporary Housing

Additional living expenses, sometimes called loss of use, covers hotel stays, meals, and temporary housing while your home is being repaired or rebuilt after a covered loss, but these payments have time limits and separate caps from your rebuild funds. If you rent out part of your home while displaced, this coverage may also pay lost rental income you would have collected. The data from the Insurance Information Institute shows wind and hail claims average around $88,170 per incident, while water damage averages $15,400, illustrating why adequate dwelling coverage directly prevents financial disaster.

Separate Policies for Flood and Earthquake

Flood and earthquake damage aren’t included in standard policies-you’ll need separate flood insurance through the National Flood Insurance Program or private carriers, and earthquake coverage is available through separate endorsements. Water backup coverage, which protects against sewer or drain backups, costs between $50 and $250 annually and covers a different peril than flood insurance. Most mortgage lenders require proof of active homeowners insurance and may specify minimum coverage amounts, so keeping your policy current and notifying your lender of changes protects your loan status.

Now that you understand what your policy covers, the next critical factor-your rates-depends heavily on where you live and how insurers assess your specific risk profile.

Factors That Affect Your Home Insurance Rates

Location Creates the Largest Premium Gap

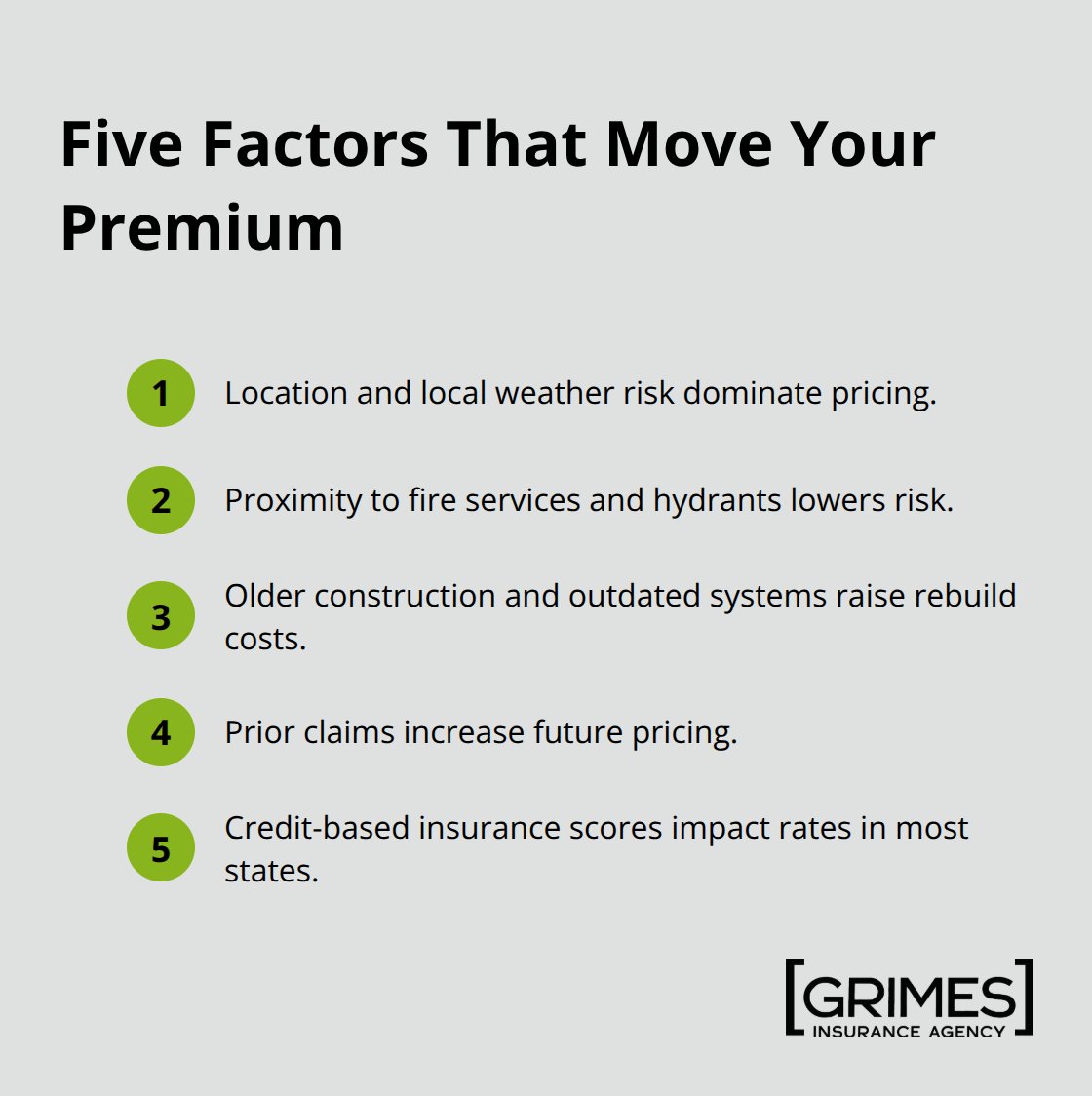

Your location is the single most powerful factor controlling your premium, and it’s not negotiable. If you live in Florida, you’ll pay roughly $2,677 annually on average according to the National Association of Insurance Commissioners, while Oregon homeowners average around $893-a difference driven almost entirely by weather exposure and loss frequency in your specific area. Coastal regions face hurricane risk, areas prone to hail experience higher wind-and-hail claims, and states with frequent winter storms see elevated water damage losses.

Your proximity to fire departments and hydrants directly lowers premiums because insurers view these as concrete risk reducers. Before you buy a home, factor insurance cost into your decision-location-based premium differences in homeowners insurance can persist for decades. The Insurance Research Council found Florida homeowners spend about 4.07% of their income on homeowners insurance, the least affordable state in the nation, while Utah residents spend just 0.96%, revealing how geography creates real financial hardship for some and manageable costs for others.

Home Age and Construction Type Shape Your Rate

Home age and construction type matter almost as much as location because older homes cost more to rebuild and typically lack modern safety systems. A 1970s home with original wiring and outdated plumbing will command higher premiums than an identical 2015 home with updated electrical systems and modern building code compliance. Upgrading to impact-resistant roofing, storm shutters, or obtaining an IBHS Fortified Home certification can reduce your premium substantially-ask your insurer specifically what retrofit qualifies for discounts rather than assuming all upgrades help.

Claims History and Credit Score Predict Future Risk

Your claims history and credit score function as a permanent record that insurers use to predict future losses. One homeowners insurance claim typically raises premiums, and multiple claims within five years can make coverage difficult to obtain at any price. Credit scores matter in most states because insurers link payment behavior to claim likelihood, so paying bills on time and maintaining low credit card balances directly reduces your rates.

If your credit score improves, request a rate review from your insurer rather than waiting for renewal, since loyalty discounts kick in after 3–5 years with the same carrier and reach roughly 10% after six years or more. The national average premium sits around $1,569 annually, but your actual rate reflects your specific combination of location risk, home characteristics, and personal history-comparing quotes from multiple carriers remains the only way to see how each factor prices your individual situation.

Understanding what drives your rates helps you identify which factors you can control and which ones shape your baseline cost. The next step involves taking that knowledge and using it to select a policy that actually matches your needs rather than settling for whatever your current insurer offers.

How to Choose the Right Home Insurance Policy

Calculate Your Dwelling Coverage Accurately

Selecting home insurance requires moving past price alone and getting specific about what you actually own and what could realistically happen to your home. Most homeowners either over-insure and waste money or under-insure and face catastrophic gaps when disaster strikes. Calculate your dwelling coverage based on current rebuilding costs in your area, not your home’s market value-the National Association of Home Builders reports an average of $162 per square foot based on surveys of builders across the country. Contact local contractors or use online rebuild cost calculators to get a realistic number, then add 10–20% as a buffer for code upgrades required during reconstruction.

Document Your Personal Property and High-Value Items

For personal property, the standard 50–70% of dwelling coverage often falls short if you own valuable items. Create a detailed home inventory with photos, serial numbers, and receipts for everything from electronics to furniture. About 47% of homeowners maintain an inventory according to Munich Re’s 2023 consumer survey, and that preparation cuts claim processing time dramatically while preventing disputes over item values.

If you own jewelry, art, collectibles, or antiques worth more than a few thousand dollars, calculate their total value separately-these items hit the standard $500-per-item cap unless you add scheduled personal property endorsements with appraisals. Liability coverage at $100,000 is barely adequate if someone is seriously injured on your property, and legal costs alone can exceed that limit; consider raising liability to $300,000 or $500,000, especially if you have a pool, trampoline, or rental property exposure. An umbrella policy covering $1 million costs surprisingly little-typically $150–$300 annually-and provides critical protection beyond your homeowners policy limits.

Compare Quotes from Multiple Carriers

Get quotes from at least three different carriers because premiums for identical coverage vary wildly by insurer. State Farm dominates the market with an 18.2% share according to 2024 NAIC data, but that size doesn’t guarantee the best price for your specific situation-Allstate, USAA, Liberty Mutual, and regional carriers often undercut the largest players. Ask each insurer about bundling discounts for combining home and auto, but don’t assume bundling saves money; compare quotes from different carriers for each line separately.

Identify Discounts and Deductible Strategies

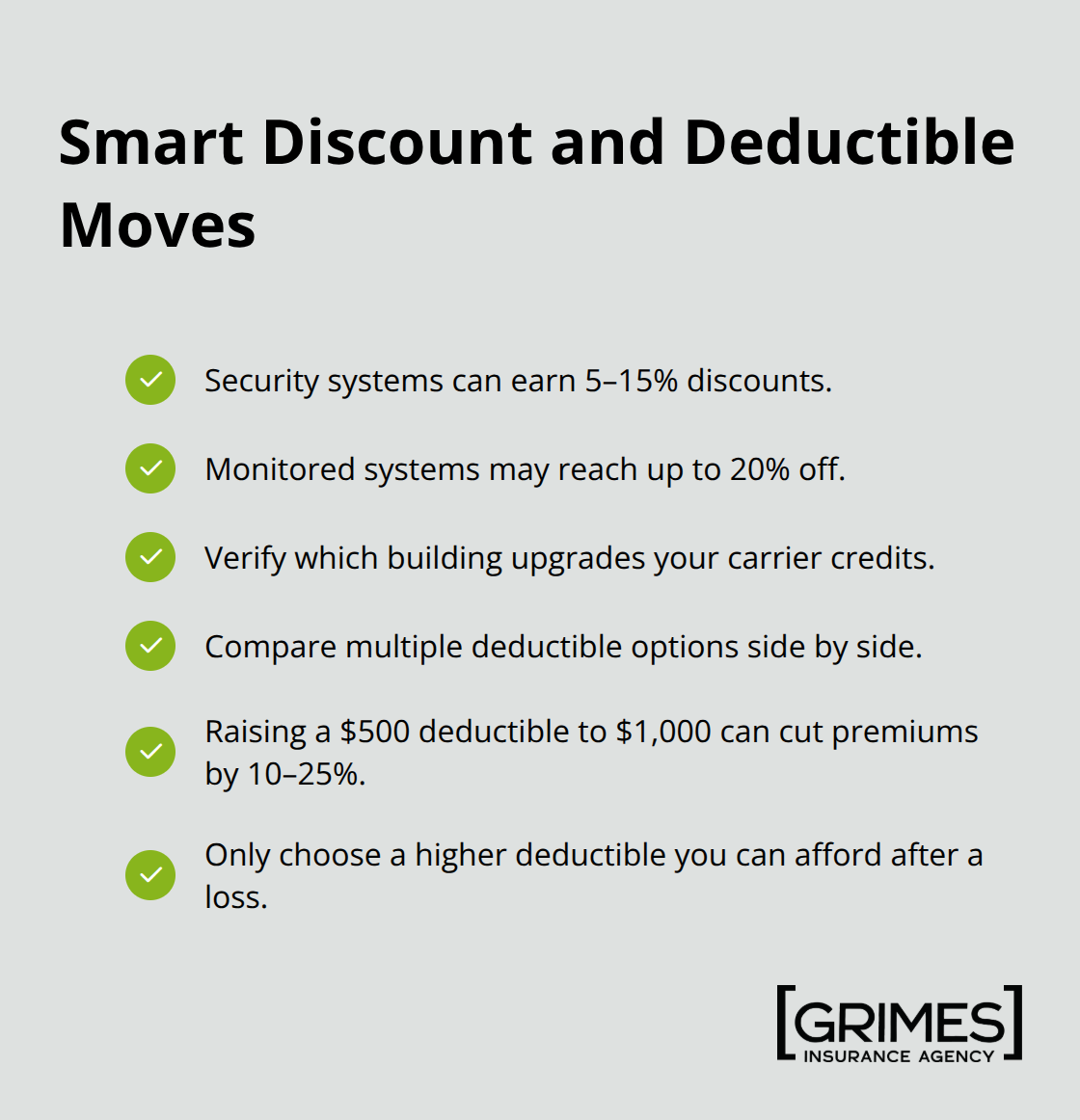

Some insurers offer 5–15% discounts for security systems, and monitored systems can yield discounts up to 20%, so factor in installation costs against long-term savings. Building upgrades like impact-resistant roofing or storm shutters qualify for discounts at many carriers, but not all insurers recognize the same improvements-ask specifically what retrofit earns a credit rather than assuming. Request quotes with multiple deductible options because raising your deductible from $500 to $1,000 typically reduces premiums by 10–25%, and that tradeoff makes sense only if you can actually afford the higher out-of-pocket amount after a loss.

Verify Coverage Details and Exclusions

When comparing policies, verify that replacement cost valuation applies to your personal property rather than actual cash value, which factors in depreciation and pays far less for older items. Check each policy’s exclusions carefully because water backup coverage, earthquake protection, and flood insurance require separate endorsements or standalone policies-standard coverage excludes these, and discovering that gap after a loss is financially devastating. The Insurance Information Institute notes that wind and hail claims average $88,170 per incident, water damage averages $15,400, and fire averages $14,747, so gaps in coverage directly translate to uninsured losses that come straight from your pocket.

Final Thoughts

Home insurance basics for homeowners come down to three decisions: buying enough dwelling coverage to rebuild at current costs, protecting your personal property with accurate limits, and selecting liability protection that matches your actual risk. Wind and hail claims average $88,170 per incident while water damage averages $15,400, so underestimating coverage creates real financial exposure that hits your savings account directly. About 5.3% of insured homes file a claim annually, which means the odds favor you experiencing a loss at some point during your ownership.

Gather quotes from at least three carriers and compare them using identical coverage amounts rather than stopping at price alone. Verify that each policy covers flood and earthquake separately, confirm replacement cost valuation applies to your personal property, and check whether your deductible fits your budget. If you own high-value items, calculate whether scheduled personal property endorsements make sense, and consider raising liability to $300,000 or $500,000 instead of accepting the standard $100,000 limit.

We at Grimes Insurance Agency in Lubbock, Texas work with multiple carriers to find coverage that fits your specific situation rather than pushing one company’s products. Contact Grimes Insurance Agency to discuss your home insurance needs and receive quotes that reflect your actual protection requirements.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation