Business Insurance Coverage for Startups: What You Need to Know

Starting a business means juggling countless decisions, and insurance often gets pushed to the back of the pile. The truth is, the wrong coverage-or worse, no coverage-can wipe out your startup faster than a bad quarter.

At Grimes Insurance Agency, we’ve seen firsthand how business insurance coverage for startups separates those who survive setbacks from those who don’t. This guide walks you through the coverage types you actually need, the gaps most startups miss, and how to pick a provider that gets your business.

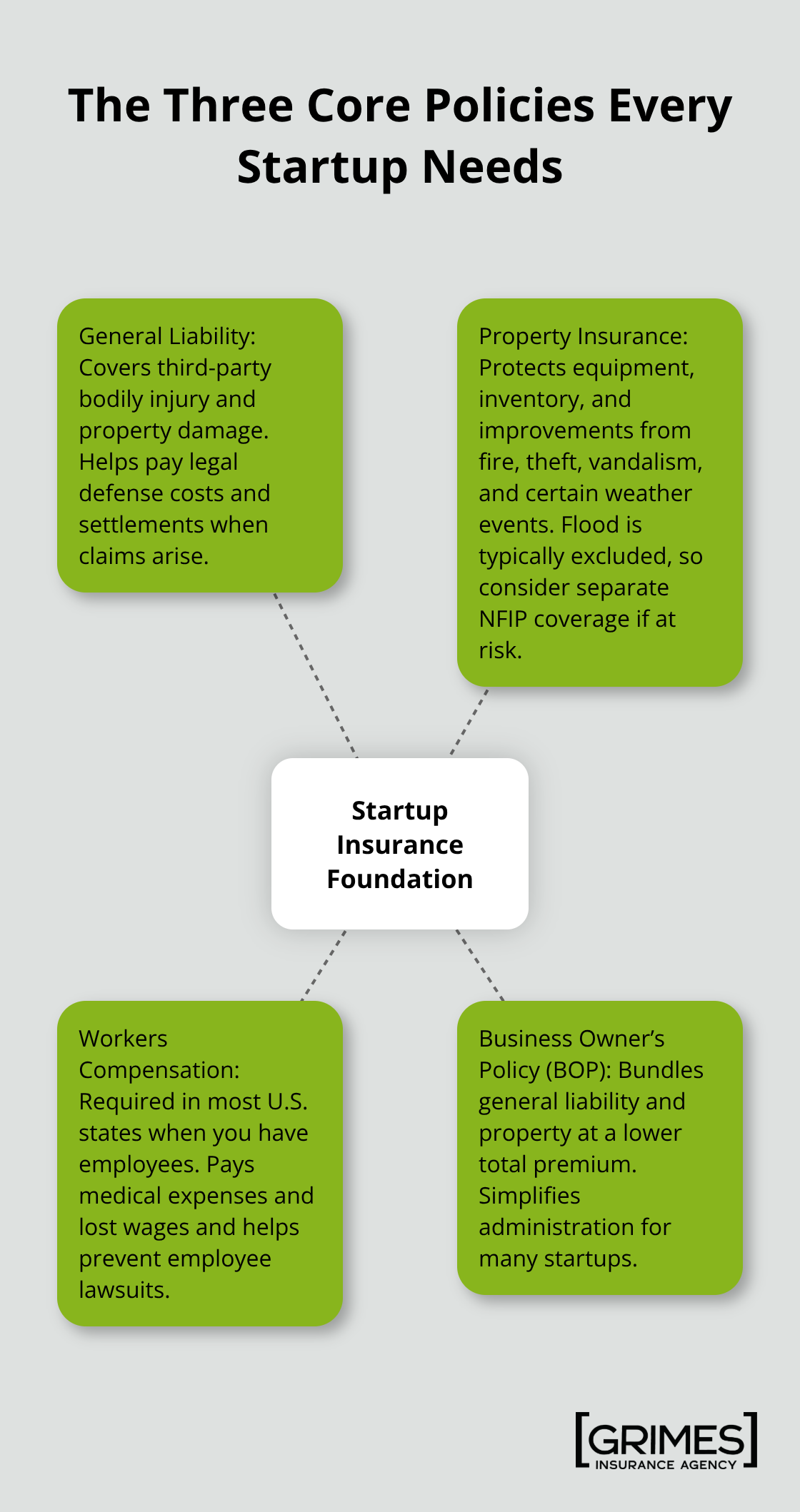

The Three Core Policies Every Startup Needs

General liability insurance sits at the foundation of startup protection, and it’s non-negotiable. This coverage protects your business when a client or third party claims you caused them bodily injury or property damage. A visitor trips in your office and breaks their arm, or your product causes financial harm to a customer-general liability covers the legal costs and settlements. Most startups underestimate how often these situations arise. The reality is that general liability claims happen across every industry, from software companies to service providers. You need minimum coverage limits between $1 million and $2 million per occurrence, with aggregate limits of $2 million to $3 million. This isn’t excessive; it reflects actual claim costs in today’s market.

Property Insurance Protects What You’ve Built

Property insurance covers the physical assets your startup depends on: office equipment, inventory, furniture, and leasehold improvements. Fire, theft, vandalism, and weather damage all fall under a standard property policy. Many startups operate from leased spaces, and landlords almost always require proof of property coverage before you sign a lease. If your startup manufactures products, stores inventory, or maintains expensive equipment, property insurance isn’t optional-it’s the difference between recovering from a disaster and closing your doors. Standard property policies typically exclude flood damage, which means you need separate flood insurance if your location sits in a flood zone or even moderately elevated flood risk. The National Flood Insurance Program covers flood losses and costs roughly $500 to $2,000 annually depending on risk level, a small price compared to uninsured flood damage that can total tens of thousands of dollars.

Workers Compensation Covers Your Team

If your startup has employees, workers compensation insurance is legally required in virtually every state. This coverage pays for medical expenses and lost wages when an employee gets injured on the job. California’s Department of Industrial Relations enforces strict compliance, and penalties for operating without coverage include fines up to $10,000 per uninsured employee, plus potential criminal charges. The cost depends on your industry classification and payroll size. A small tech startup with five employees might pay $800 to $1,500 annually, while a startup in construction or manufacturing faces higher premiums due to greater injury risk. The real value appears when an actual injury happens: workers compensation prevents lawsuits from employees and protects your startup’s finances during recovery periods.

Why These Three Policies Form Your Foundation

These three policies work together to shield your startup from the most common financial threats. General liability handles third-party claims, property insurance protects your physical assets, and workers compensation covers your team. Most startups can bundle these coverages into a Business Owner’s Policy (BOP), which combines general liability and property coverage at a lower cost than separate policies. This approach simplifies administration and reduces your overall premium. However, your specific industry and business model may demand additional protections beyond this foundation. The gaps most startups overlook often prove far more expensive than the premiums they try to save.

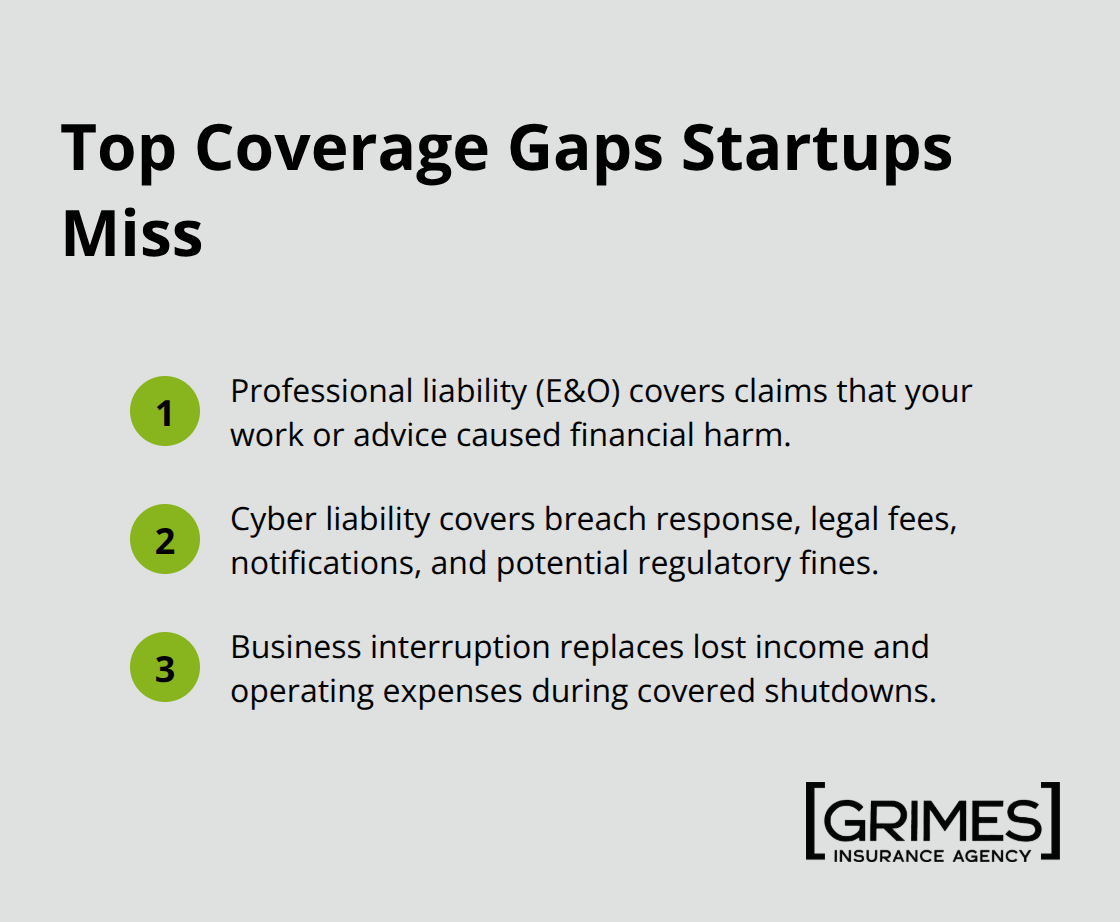

What Coverage Gaps Actually Cost Startups

Most startups operate with incomplete protection because they focus only on the three core policies and ignore everything else. This approach creates serious financial exposure in areas where claims hit hardest. Your industry determines which gaps matter most, but three gaps appear consistently across nearly every startup we encounter.

Industry-Specific Liability Gaps Leave You Exposed

The first gap involves underestimating liability exposure specific to your industry. A software startup faces completely different liability risks than a consulting firm or a product manufacturer, yet many founders grab a standard general liability policy without considering industry-specific claims. Tech startups encounter claims around software failures, IP disputes, and service delivery failures that standard general liability doesn’t adequately cover.

Professional liability insurance, also called Errors and Omissions coverage, protects against claims that your work or advice caused a client financial harm. If you’re a consultant, designer, engineer, or software developer, professional liability becomes as essential as general liability itself. Skipping this coverage means a single client lawsuit could create substantial legal costs, even if you ultimately win the case.

Cyber Liability and Data Security Breaches

The second critical gap involves cyber liability and data security. The Cybersecurity and Infrastructure Security Agency notes that cyber threats target organizations of all sizes, including startups, and even a single incident can create significant financial strain for companies still raising capital. If your startup handles customer data, payment information, or proprietary client files, you operate in constant breach risk.

Standard business policies exclude data breach costs entirely. Cyber liability insurance covers breach response expenses, legal fees, notification costs to affected customers, and potential regulatory fines. The Federal Trade Commission emphasizes data security as a foundational business practice, and costs from a single breach typically range from $10,000 to $100,000 depending on customer count and data sensitivity.

Many startups discover this gap only after a breach occurs, at which point the damage spreads across customer relationships and investor confidence.

Business Interruption Coverage Protects Your Cash Flow

The third gap involves business interruption coverage, which protects your income and operating expenses when a covered event forces you to temporarily close. A fire, natural disaster, or extended equipment failure could halt operations for weeks or months. During that shutdown, your rent, payroll, and vendor payments continue regardless of whether revenue arrives.

Business interruption insurance reimburses these ongoing costs, typically covering 30 to 90 days of lost income and operating expenses. Startups with high fixed costs or heavy supplier dependence benefit most from this protection, as a two-month closure without coverage could eliminate months of cash reserves. These three gaps represent the most common blind spots we see, but your specific business model may reveal additional exposures that demand attention before they become expensive problems.

Picking an Insurance Partner That Understands Your Startup

Selecting an insurance provider matters far more than most founders realize. The wrong carrier leaves you with gaps you don’t discover until a claim arrives, while the right partner proactively identifies exposures before they become problems. Start by requesting quotes from at least three carriers, but don’t treat this as a simple price comparison. A quote that looks cheap often comes with higher deductibles, lower coverage limits, or exclusions that create the exact gaps you’re trying to avoid.

When you evaluate quotes, verify that each carrier proposes identical coverage limits and deductibles across all three policies. This forces apples-to-apples comparison and reveals where carriers differ on actual protection. Many startups fixate on monthly premium and miss that a $50 difference in premium might come with a $10,000 difference in coverage limits or a critical exclusion buried in policy language.

Demand that each carrier provides a detailed coverage summary, not just a price sheet. Ask specifically whether cyber liability, professional liability, or business interruption coverage is included or available as add-ons, since these determine whether you’re actually protected against the gaps we discussed.

Experience with Startup-Stage Companies Matters

Insurance carriers vary dramatically in how they approach startup businesses. Some carriers treat startups as loss leaders and provide minimal support, while others specialize in early-stage companies and understand the unique cash flow constraints and rapid growth patterns that define startup operations. An independent insurance agency with access to multiple carriers can match your startup to insurers that actively support early-stage businesses rather than viewing them as problems.

Ask your prospective carriers directly: How many startups do you insure in my industry? What’s your average policy size? Do you offer online quotes or require phone calls? Carriers that invest in startup-friendly processes typically provide faster quotes and more flexibility on coverage customization. Request references from founders in your industry who use each carrier. A five-minute call with another founder reveals whether claims get processed quickly, whether customer service actually answers the phone, and whether the carrier stands behind coverage when problems arise.

Tech startups particularly need carriers that understand cyber risk and data security, not generalist carriers that treat cyber as an afterthought. Construction startups need carriers experienced with equipment and contractor liability. Your industry determines which carrier experience matters most.

Claims Support Determines Real-World Value

The true test of an insurance carrier arrives the moment you file a claim. A carrier with excellent customer service during the sales process can become unresponsive once your money is paid. Investigate each carrier’s claims process before you purchase: Do they offer 24/7 claims reporting? Can you file claims online or through a mobile app? How long does it typically take to receive a claims decision?

Check AM Best ratings to verify financial stability, prioritizing carriers with A- ratings or higher. A startup cannot afford to discover mid-claim that your insurer lacks financial reserves to pay claims. Ask your prospective carriers for their average claims processing time and request specific examples of how they’ve handled claims similar to yours. Some carriers assign a dedicated claims adjuster to each policy, while others rotate between adjusters, which affects consistency and relationship continuity. Request a sample Certificate of Insurance to verify the format matches what your clients, landlords, and investors will demand. Cheap insurance that creates headaches during claims destroys more value than higher premiums that provide smooth, fast resolution when problems occur.

Final Thoughts

Business insurance coverage for startups forms the financial foundation that lets you take calculated risks without betting your entire company on a single bad event. The three core policies-general liability, property insurance, and workers compensation-establish your baseline protection, but the gaps we discussed often prove far more expensive than the premiums you’ll pay to fill them. Professional liability, cyber liability, and business interruption coverage aren’t luxuries for larger companies; they’re practical shields against the specific threats your startup actually faces.

Getting properly covered starts with honest assessment of your industry’s unique risks. A software startup’s exposure looks nothing like a consulting firm’s, and your insurance should reflect that reality. Request quotes from multiple carriers, but evaluate them on coverage quality and claims support, not just price. The cheapest premium means nothing if it comes with exclusions that leave you exposed exactly where you need protection most.

An independent insurance agent transforms this process from overwhelming to manageable, as they access multiple carriers and understand which insurers actually specialize in startups rather than treating them as afterthoughts. They identify gaps you might miss, explain policy language in plain terms, and contact Grimes Insurance Agency to discuss your coverage needs and receive a customized quote that reflects your specific risks.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation