Flood Insurance for Homeowners: A Quick Guide

Floods cause more damage to American homes than any other natural disaster, yet most homeowners don’t realize their standard insurance won’t cover it. We at Grimes Insurance Agency see this gap in protection firsthand, and it’s why flood insurance for homeowners matters so much.

The good news is that getting protected doesn’t have to be complicated. This guide walks you through what flood insurance covers, how much it costs, and exactly how to buy it.

Why Your Homeowners Insurance Won’t Cover Flood Damage

The Critical Difference Between Water Damage and Flood Damage

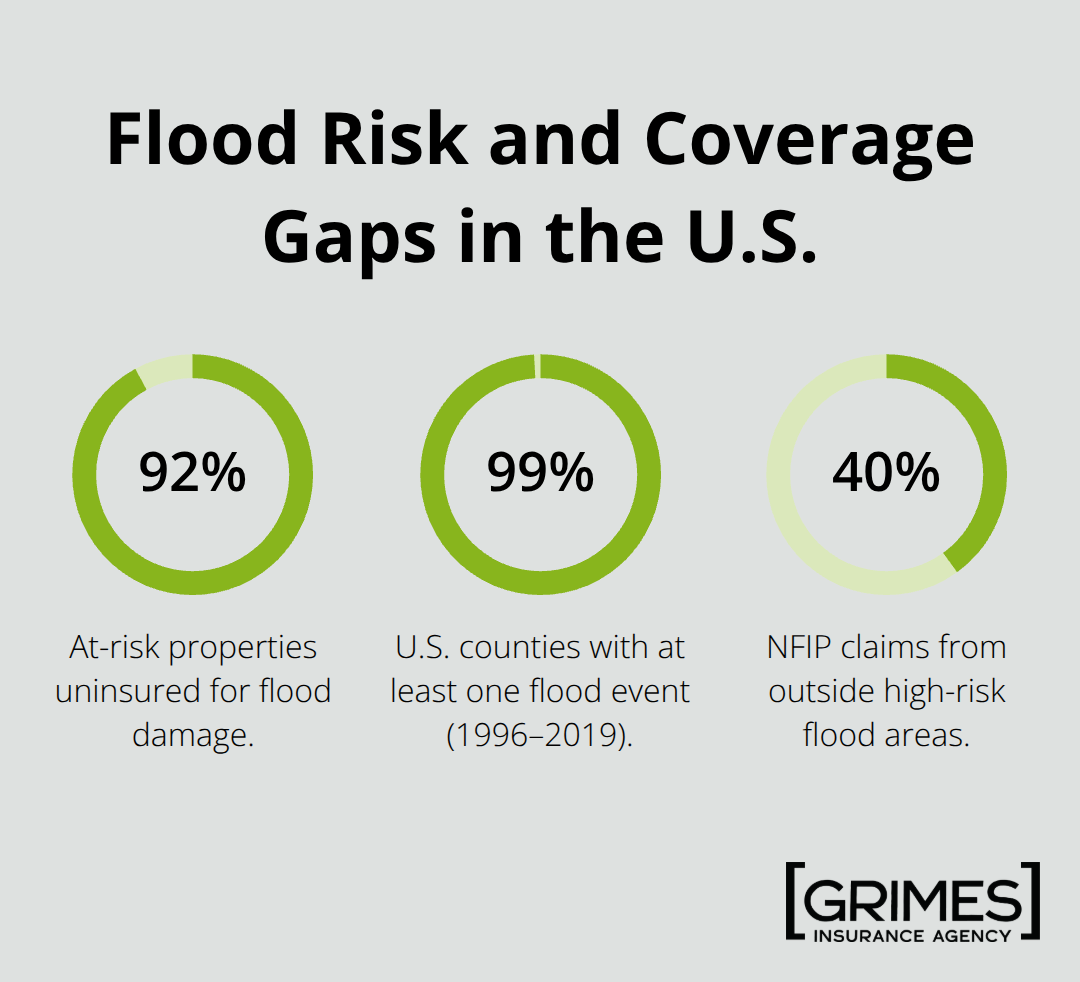

Water damage from a burst pipe, backed-up toilet, or leaking roof gets covered by your standard homeowners policy. Flood damage does not. This distinction matters enormously because flooding is the leading natural disaster in the United States, yet about 92% of at-risk properties remain uninsured for it. Insurance companies define a flood as an excess of water on normally dry land that affects two or more acres or two or more properties.

When water from heavy rain, overflowing rivers, storm surge, or inadequate drainage systems inundates your neighborhood, that’s a flood. When water backs up through your plumbing system because of a clogged pipe, that’s not.

Why Insurance Companies Exclude Flood Coverage

Insurance companies exclude flood coverage from standard homeowners policies because floods are catastrophic events that affect entire communities at once. A single house fire might destroy one property. A major flood can devastate hundreds of homes simultaneously. The financial exposure is simply too large for traditional homeowners insurers to absorb. That’s why Congress created the National Flood Insurance Program in 1968, establishing a separate system where the federal government and private insurers share the risk.

The Real Cost of Flood Damage

The numbers reveal why this gap in coverage exists and why you need to address it now. According to FEMA data, the average flood insurance claim payout between 2016 and 2022 exceeded $66,000. Between 1996 and 2019, 99% of U.S. counties experienced at least one flood event, meaning flood risk is genuinely widespread, not confined to designated flood zones. About 40% of NFIP claims come from properties outside high-risk flood areas, which shows that flooding happens in neighborhoods most people consider safe.

The Congressional Budget Office reports that roughly 9% of U.S. homes will experience at least one flood event of one foot or more in the next 30 years. Climate change is intensifying this threat, with rising ocean temperatures and more frequent extreme weather events creating conditions for heavier rainfall and more severe storms. The World Meteorological Organization and NOAA both document these trends. If your home floods without insurance, you cover the full cost of repairs, replacement, and temporary housing out of pocket. Standard homeowners insurance will not help, leaving thousands of homeowners financially devastated every year.

Understanding this protection gap is the first step toward securing your home. The next section explains exactly what flood insurance covers and what it leaves out.

What Flood Insurance Actually Covers

Building and Contents Coverage Limits

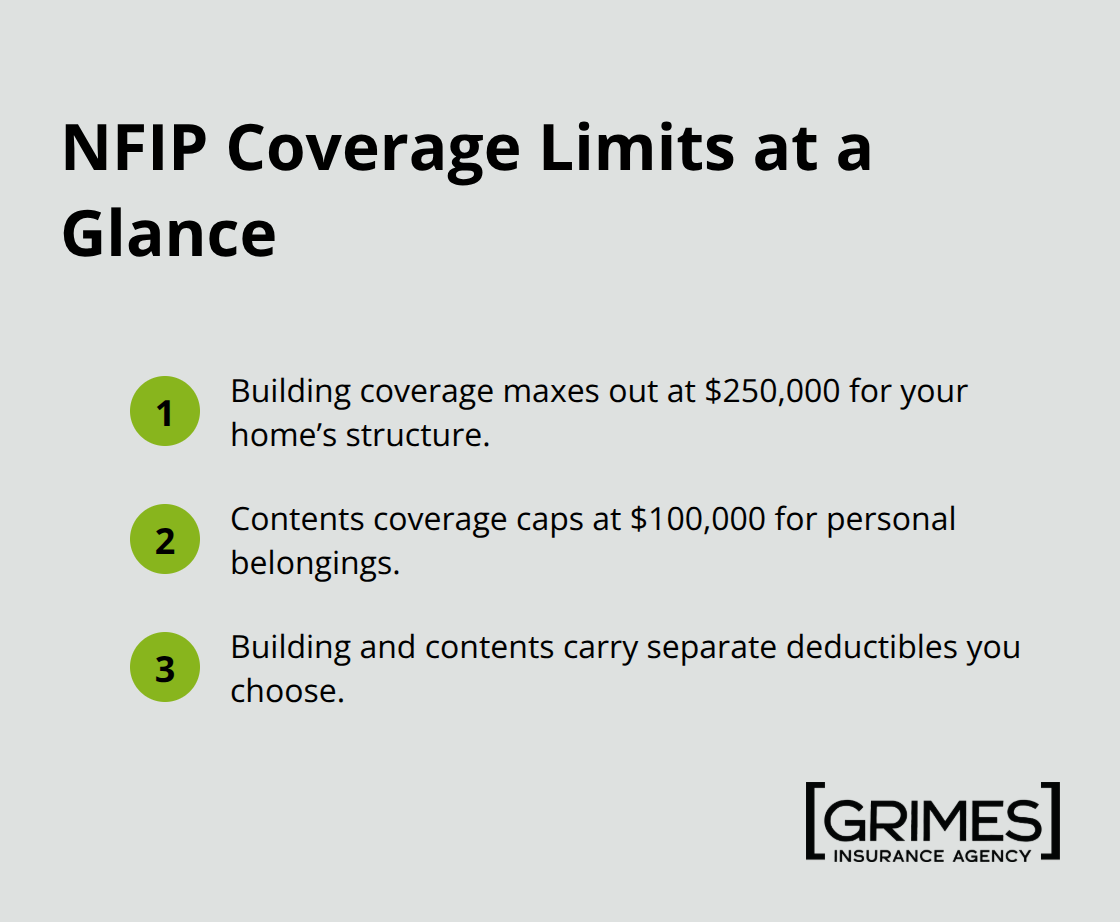

National Flood Insurance Program policies protect your home’s structure and belongings in two separate coverage categories, each with distinct limits and deductibles. Building coverage pays for damage to the structure itself, including electrical systems, plumbing, furnaces, water heaters, refrigerators, built-in appliances, carpeting, cabinets, and blinds. For homeowners, building coverage maxes out at $250,000 according to NFIP guidelines. Contents coverage handles your personal belongings like clothing, furniture, electronics, curtains, washers and dryers, and portable air conditioners, capped at $100,000 for homeowners. You purchase these separately and maintain separate deductibles for each, meaning you could have a $1,000 deductible on your building coverage and a different amount on contents.

Why Separate Deductibles Matter

This separation matters because you might want to prioritize protecting your home’s structure over possessions, or vice versa depending on your situation. Your deductible choices directly affect your monthly premium and out-of-pocket costs when you file a claim. Higher deductibles lower your premium but increase what you pay when flood damage occurs. Lower deductibles raise your premium but reduce your financial burden after a flood strikes.

What NFIP Explicitly Excludes

NFIP policies do not cover currency, precious metals, stock certificates, vehicles, property outside your building like landscaping and decks, temporary housing costs, or business interruption losses. Sewer backups receive coverage only if flooding directly caused the backup, not if a clogged pipe created the problem. Moisture or mold damage that you could have prevented also falls outside coverage. This matters significantly because the average NFIP claim between 2016 and 2022 topped $66,000, yet many homeowners discover their actual losses exceed policy limits once disaster strikes.

Coverage Gaps and Private Insurance Options

If your home’s replacement value exceeds $250,000 for the structure, standard NFIP coverage leaves you substantially underinsured. Private flood insurers exist to address this gap-they offer higher limits and different coverage structures, sometimes reaching $500,000 or more for building coverage. Under Risk Rating 2.0, which FEMA implemented around 2023, premiums now reflect individual replacement costs and specific flood risk rather than zone-based rates. This change makes accurate coverage amounts even more critical to your financial recovery after a flood. Understanding what your policy covers and where gaps exist helps you decide whether NFIP protection alone suffices or whether private flood insurance makes sense for your property. The next section walks you through how much flood insurance actually costs and what factors affect your premium.

Getting Flood Insurance and What to Budget

Understanding Your NFIP Options

The National Flood Insurance Program handles roughly 4.7 million policyholders nationwide and provides nearly $1.3 trillion in flood coverage, making it the dominant option for most homeowners. NFIP policies are available through more than 47 private insurance companies that participate in what’s called the Write-Your-Own program, plus NFIP Direct itself. You don’t purchase directly from the government-you work with an insurance agent or company that sells NFIP coverage. The critical advantage here is pricing consistency. No matter which of these 47+ carriers you approach, NFIP rates remain identical across all providers for the same property. A home in a specific flood zone with particular characteristics costs the same premium whether you purchase from one carrier or another. This eliminates shopping around for a better rate within the NFIP system, so your focus shifts to coverage adequacy and service quality instead.

Private Flood Insurance as an Alternative

Private flood insurance operates differently. Private carriers offer higher building limits beyond NFIP’s $250,000 cap and contents limits exceeding $100,000. They set their own rates, which vary by insurer and can sometimes undercut NFIP premiums, particularly for lower-risk properties. However, private policies come with longer waiting periods or different terms, so comparing both options matters for your specific situation.

What You’ll Pay for Coverage

The average NFIP premium runs about $870 per year according to FEMA data under Risk Rating 2.0, though this varies substantially based on your property’s flood risk, construction type, and replacement cost. Properties in higher-risk areas see premiums climb significantly, with some increasing as much as 18% annually as Risk Rating 2.0 adjusts individual policies. Your elevation, whether you’ve obtained an elevation certificate documenting your home’s height relative to flood levels, and critical system upgrades like elevated water heaters or electrical panels all reduce your premium.

Steps to Purchase Your Policy

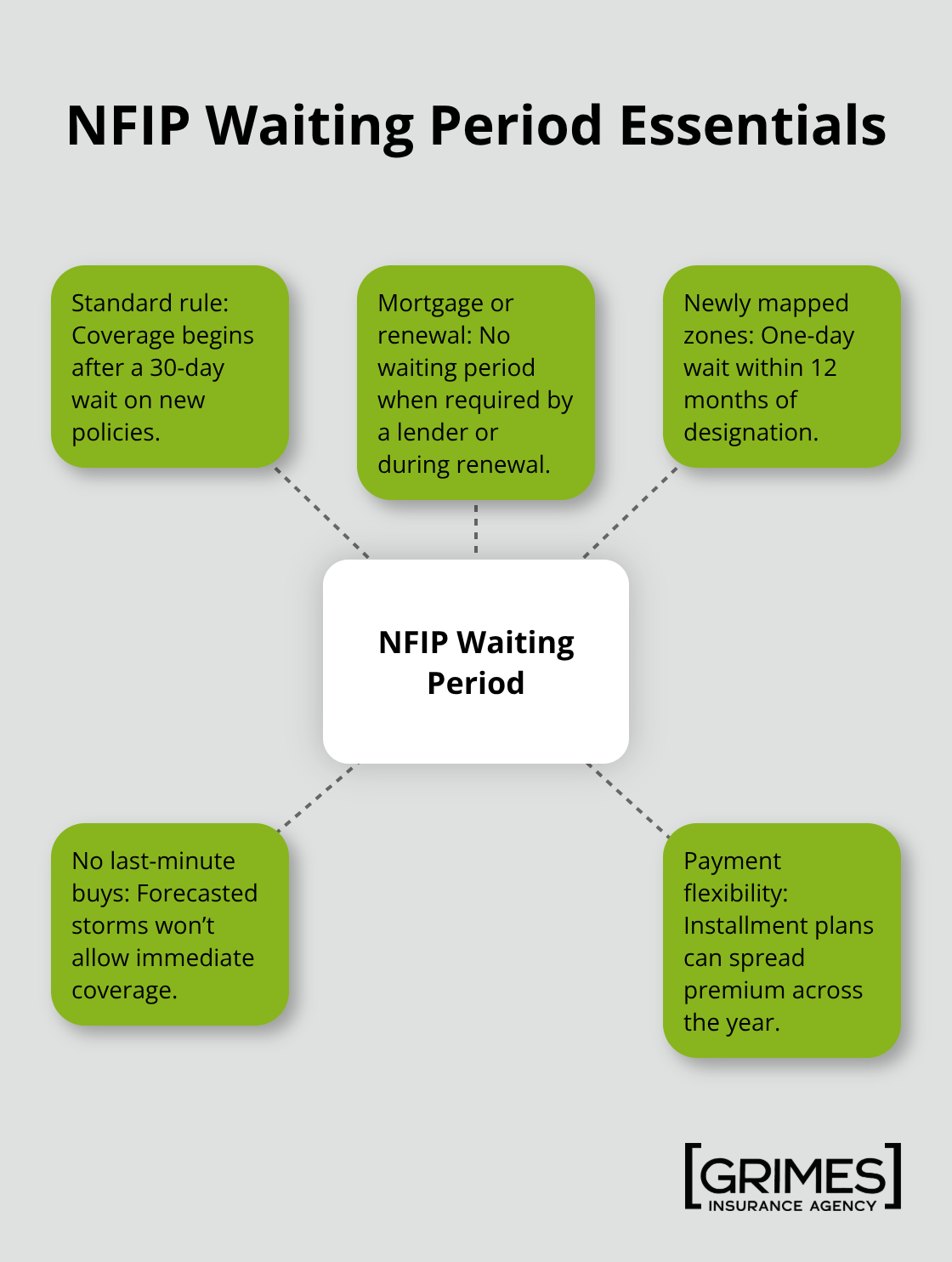

To purchase coverage, start with a personalized quote through the NFIP Quote Tool at floodsmart.gov, which gives you a concrete number before committing to anything. Once you have your quote, contact an insurance agent or your current insurer to finalize the purchase. NFIP policies typically require a 30-day waiting period before coverage begins, though exceptions exist: no waiting period applies if you’re purchasing to satisfy a mortgage requirement or renewing an existing policy, and a one-day wait applies for newly designated flood zones within 12 months. This waiting period matters enormously-if a storm is forecast, you cannot purchase coverage and have protection in time. NFIP offers installment payment plans to spread your premium across the year, making the cost more manageable than a lump sum.

Preparing Your Documentation

After purchasing your policy, document your home’s contents with photos and videos, store copies in a waterproof location, and keep originals in a safe deposit box. This documentation accelerates your claim if flooding occurs and helps you recover the full value of your belongings.

Final Thoughts

Flood insurance for homeowners protects you from losses that standard policies ignore, and the 30-day waiting period makes timing critical. If you wait until a storm arrives, you cannot purchase coverage in time, leaving your home and finances exposed to catastrophic damage that averages over $66,000 per claim. The decision to act now determines whether you recover quickly after a flood or face years of financial hardship.

Start by obtaining a personalized quote through the NFIP Quote Tool, then compare options between NFIP and private carriers to find coverage matching your home’s replacement value. Document your belongings with photos and videos stored in a waterproof location, and verify whether your lender requires flood insurance based on your property’s location. Since 40% of NFIP claims originate from properties outside designated high-risk zones, flood risk exists in neighborhoods most people consider safe.

We at Grimes Insurance Agency help homeowners secure the right flood insurance for their families and properties. Contact Grimes Insurance Agency today to discuss your flood insurance needs and receive a quote tailored to your home.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation