How to Evaluate Home Insurance Quotes: Making an Informed Decision

Home insurance quotes can look confusing at first glance. Comparing coverage types, deductibles, and endorsements across different insurers takes time and attention to detail.

At Grimes Insurance Agency, we help clients evaluate home insurance quotes every day. We’ve put together this guide to show you exactly what to look for when reviewing quotes, spotting hidden costs, and making a decision that actually protects your home.

What Your Home Insurance Quote Actually Covers

A home insurance quote breaks down into four core protection areas, and understanding each one directly affects what you’ll pay and what happens when you file a claim. Dwelling coverage protects the structure itself-your walls, roof, and built-in systems. Personal property coverage pays for your belongings inside the home. Liability coverage protects you if someone is injured on your property and sues. Additional living expenses cover temporary housing if your home becomes uninhabitable after a covered loss.

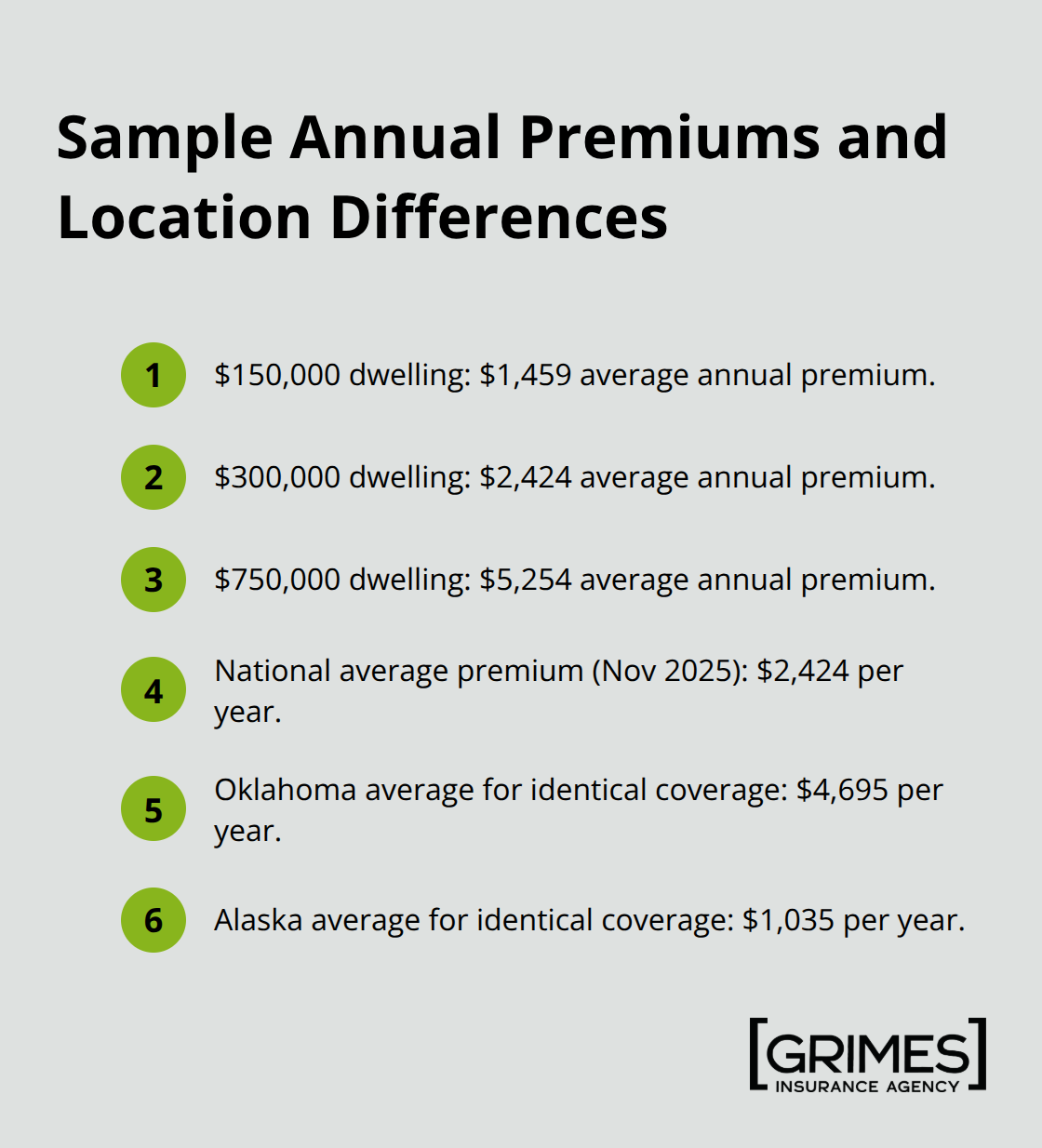

According to Bankrate data, dwelling coverage level drives the largest premium difference: a $150,000 dwelling averages $1,459 annually, while a $300,000 dwelling averages $2,424, and a $750,000 dwelling runs $5,254. Never lower dwelling coverage to cut costs. Your dwelling limit becomes the foundation for calculating other coverage limits, so underinsuring creates a domino effect of inadequate protection. The national average premium sits around $2,424 per year as of November 2025 according to Bankrate, but location matters enormously-Oklahoma averages $4,695 annually while Alaska averages $1,035 for identical coverage.

How Deductibles Shape Your Real Cost

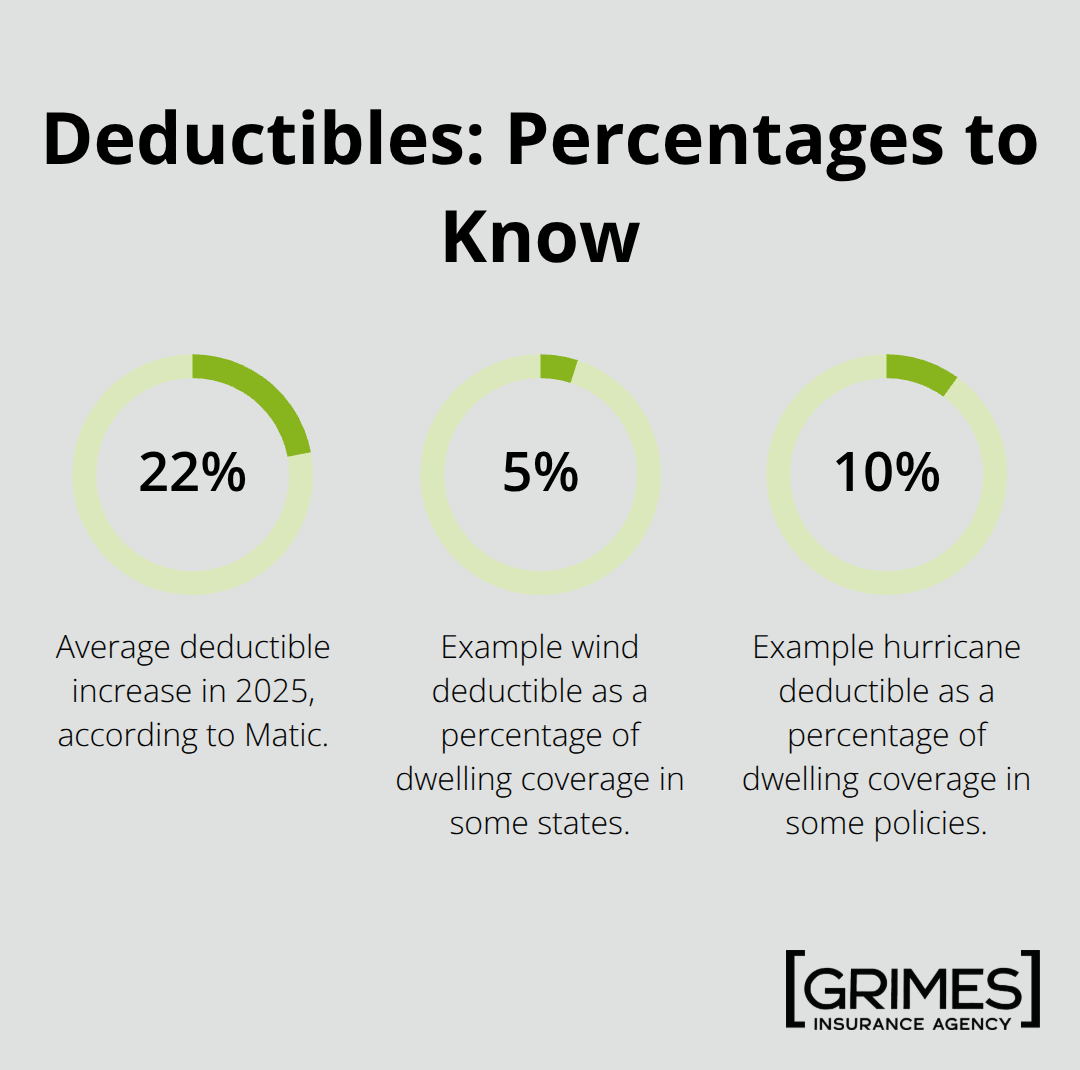

Your deductible is the amount you pay out-of-pocket when you file a claim, and it directly controls your premium. Higher deductibles lower your annual premium but increase what you owe after a loss. Bankrate shows that a $1,500 deductible costs approximately $2,366 yearly, a $2,000 deductible runs $2,212, and a $5,000 deductible drops to $1,989. The average deductible rose 22 percent in 2025 according to Matic, meaning more homeowners are choosing higher deductibles to manage affordability.

The math matters here: if you choose a $5,000 deductible to save $377 annually compared to a $1,500 deductible, you need to stay claim-free for at least 13 years just to break even. Try matching your deductible to your emergency savings capacity, not just chasing the lowest premium. Some states impose separate wind or hurricane deductibles that apply only to storm damage, so verify your insurer’s structure-a wind deductible might be 5 or 10 percent of your dwelling coverage rather than a fixed dollar amount.

Endorsements Add Targeted Protection

Endorsements are add-ons that extend coverage beyond the standard policy. Water backup coverage protects against sewer backups or sump pump failures-common claims that standard policies exclude. Service line coverage pays to repair underground water or electrical lines on your property. Ordinance or law endorsements cover the cost of rebuilding to current building codes when your home is damaged, since your original construction likely met older standards.

These endorsements cost more but address real risks. The decision should match your specific property: homes in flood-prone areas benefit from water backup coverage, older homes benefit from ordinance coverage, and homes with aging underground utilities benefit from service line coverage. Review endorsements annually because many homeowners pay for coverages that no longer fit their situation after renovations or property changes. Once you understand what your quote covers and how deductibles and endorsements affect your total protection, you’re ready to compare multiple quotes side-by-side to spot real differences in price and coverage.

Comparing Quotes Side by Side

Request Matching Coverage from Multiple Insurers

You need at least three quotes from different insurers if you want to understand your actual options and pricing. The variation across carriers is dramatic: for identical coverage on the same home, premiums can swing by hundreds of dollars annually simply because each insurer uses different risk models and underwriting criteria. When you request quotes, specify matching dwelling coverage, personal property limits, liability amounts, and deductibles across all three so you compare apples to apples. Many homeowners request quotes without specifying these details, then wonder why the numbers look so different.

Provide your property’s exact replacement cost, your location, the age and construction type of your home, and your roof age because these factors drive pricing dramatically. Request that each quote includes the declarations page with all terms, conditions, exclusions, and coverage specifics so you can actually read what you’re comparing.

Understand What Price Differences Actually Mean

Price differences reveal how insurers view your specific risk profile, and understanding those differences matters more than chasing the lowest number. An insurer quoting significantly lower than others might use outdated risk assessment methods, might avoid your area due to recent claims patterns, or might offer lower limits than you think. Conversely, a higher quote might reflect an insurer’s investment in modern satellite imagery and AI-driven assessment tools that catch real risks you should know about.

Ask each insurer directly why their quote differs from competitors, and pay attention to whether they can explain their reasoning with concrete factors tied to your property. This conversation often reveals whether an insurer truly understands your home’s specific risk profile or simply plugged numbers into a generic formula.

Evaluate Claims Handling and Financial Stability

Customer service quality and claims handling speed separate good insurers from mediocre ones, yet most people ignore this until they need to file a claim. Call the insurer’s claims line and time how long you wait before speaking to someone. Ask how they handle initial damage assessment, whether they use their own adjusters or third parties, and how long claim resolution typically takes.

Check AM Best ratings for financial stability because an insurer with cheap premiums means nothing if they cannot pay your claim. Read recent customer reviews on independent sites and specifically look for patterns about claims experience rather than generic complaints about price increases. These patterns tell you whether an insurer actually delivers when homeowners need them most-and that matters far more than saving a few dollars on your annual premium.

Watch for These Warning Signs in Home Insurance Quotes

Suspiciously Low Premiums Demand Investigation

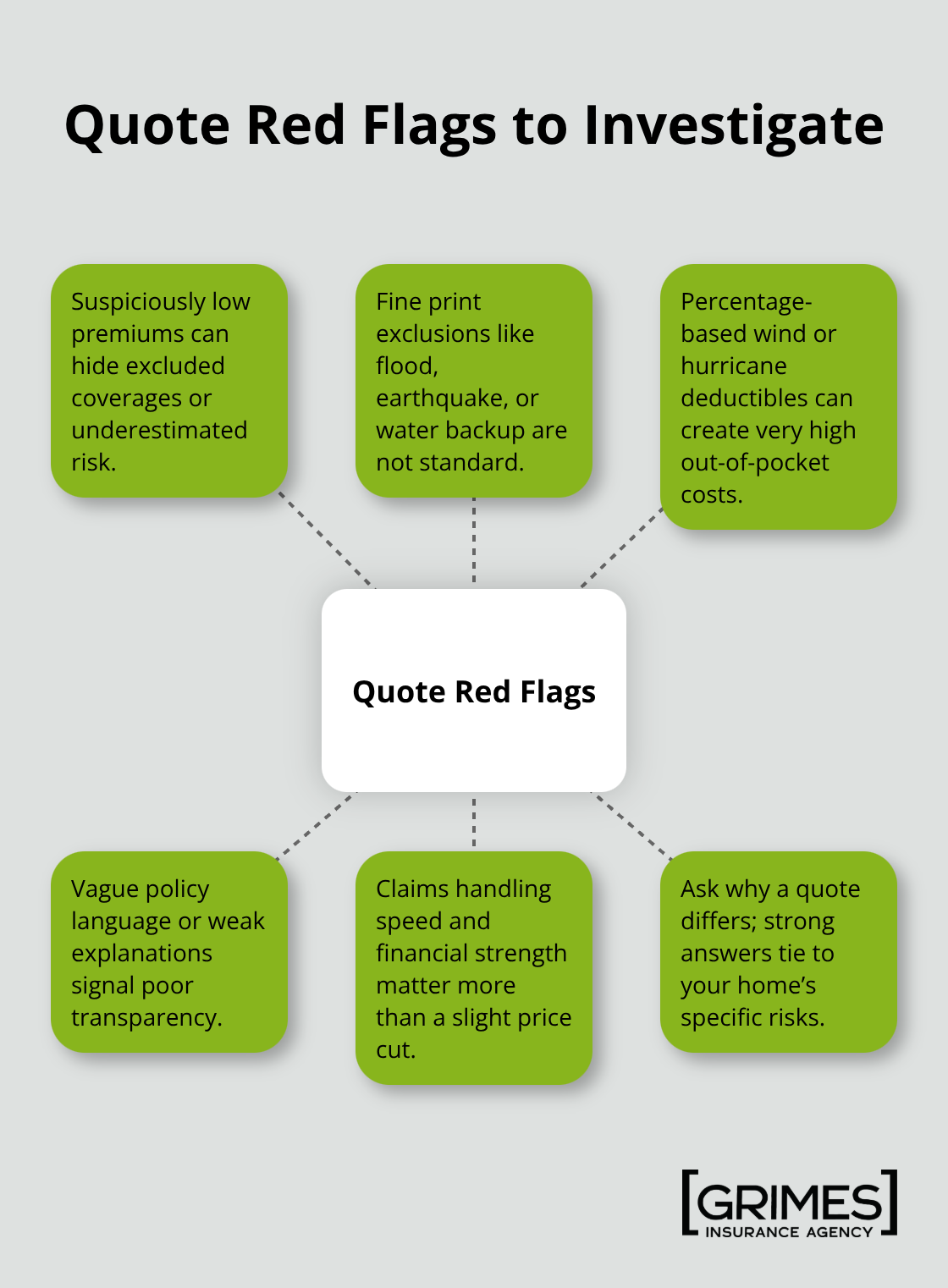

A premium that sits $800 below competitors for identical coverage should trigger immediate investigation, not excitement. Something is wrong when one insurer quotes substantially lower than the rest. They may be underestimating your risk through outdated assessment methods, excluding coverage you believe you have, or deliberately undercutting to win your business before raising rates sharply at renewal.

Roof age now creates a $155 price gap between newer roofs and 11-15 year old roofs as of 2025, up from just $49 in 2022 according to Matic data. An insurer quoting substantially below market likely isn’t factoring in your actual roof condition or is using satellite imagery less effectively than competitors. Request a detailed explanation of how they calculated the quote and specifically ask what they assessed about your roof, electrical system, and plumbing. If they cannot answer with concrete details about your property, that signals a problem.

Coverage Details That Disappear in Fine Print

Missing coverage details in your quote means you are comparing incomplete information. Some insurers bury exclusions in fine print or simply omit them from the initial quote summary. Flood damage isn’t covered by standard policies, yet many homeowners assume it is until they file a claim. Earthquake coverage, water backup from sewer lines, and damage from poor maintenance are commonly excluded.

Request that every quote explicitly state what isn’t covered, not just what is. Ask directly whether the quote includes replacement cost value or actual cash value for personal property because that difference can mean thousands of dollars in a claim. Verify the liability limit because most homeowners policies allow you to choose a minimum of $100,000 and a maximum of $500,000.

Deductible Structures That Hide Real Costs

Unclear terms and conditions in the policy language itself indicate an insurer that doesn’t prioritize transparency. Read the declarations page for each quote and flag any language you don’t understand immediately. Call the insurer and ask them to explain it in plain English. If they struggle to explain their own policy or use vague answers, that signals they may not handle claims clearly either.

Some insurers structure wind or hurricane deductibles as a percentage of dwelling coverage rather than a fixed dollar amount, which dramatically affects your actual out-of-pocket cost in a claim. A 5 percent wind deductible on a $400,000 dwelling means you pay $20,000 out of pocket for wind damage, not $2,500. This detail matters enormously yet gets buried in policy documents. Ask your insurer to calculate your exact deductible amount for wind or hurricane claims so you know precisely what you owe before you sign anything.

Final Thoughts

Evaluating home insurance quotes requires you to balance coverage that protects your home, premiums you can afford, and an insurer you trust when claims happen. Most homeowners focus only on price, then regret that decision when they discover missing coverage or slow claims handling after a loss. The quotes you’ve gathered now contain all the information you need to make a smarter choice.

Start by eliminating quotes with suspiciously low premiums or vague coverage details, as those red flags signal problems that will surface later. Next, narrow your remaining quotes to those with matching dwelling coverage, deductibles, and liability limits so you’re truly comparing identical protection. Check AM Best ratings for financial stability and read customer reviews specifically about claims experience, not just price complaints.

Your final decision should reflect your specific situation: if you have strong emergency savings, a higher deductible makes sense to lower your annual premium; if you live in an area prone to wind or water damage, endorsements for those risks are not optional; if your roof is aging, expect higher premiums and verify the insurer assessed it accurately. Contact Grimes Insurance Agency and let our local experts handle the heavy lifting-we’ll request quotes from multiple insurers with matching coverage, explain what drives the price differences, and help you select a policy that protects what matters most without overpaying for unnecessary coverage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation