Flood Insurance vs Homeowners Insurance in 2026: Which Do You Need?

Most homeowners think one insurance policy covers everything. That’s a costly mistake.

We at Grimes Insurance Agency see this confusion constantly. Homeowners insurance and flood insurance serve completely different purposes, and understanding the difference between flood insurance vs homeowners insurance in 2026 could save you thousands in uncovered damages.

What Homeowners Insurance Actually Protects

The Three Core Coverage Areas

Homeowners insurance covers three broad categories of risk, and understanding exactly what falls under each one matters more than most people realize. The policy protects your home’s structure against specific perils like wind, hail, and fire-if a tornado tears off your roof or hail punches holes in your siding, homeowners insurance pays for repairs up to your policy limits. The policy also includes personal liability protection, which covers medical bills and legal costs if someone is injured on your property and sues you.

If a guest slips on your driveway and breaks their leg, your liability coverage handles their medical expenses and attorney fees up to your coverage limit, typically ranging from $100,000 to $300,000 for standard policies.

Additional Living Expenses Coverage

Homeowners insurance covers additional living expenses if your home becomes uninhabitable after a covered loss. If a fire makes your house unlivable, the policy pays for temporary housing, meals, and other necessary expenses while repairs happen. This protection prevents financial strain during the recovery period.

What Homeowners Insurance Excludes

Flood damage from heavy rainfall, overflowing rivers, or storm surge is not covered by standard homeowners policies. Earthquake damage is excluded. Damage from poor maintenance, wear and tear, or gradual deterioration falls outside the policy. Most standard homeowners policies also cap coverage for valuables like jewelry, electronics, and firearms at $1,500 to $2,500 per item, which means high-value items require additional riders to protect them fully. Water backup from sewer or drain failures isn’t covered unless you add a specific endorsement.

Understanding the Cost and Boundaries

On average, homeowners insurance costs between $800 and $1,500 annually, though rates vary significantly based on your home’s age, location, and construction materials. Homeowners insurance protects against sudden, accidental damage from specific perils, but it has real boundaries. Those boundaries create gaps that other types of coverage, particularly flood insurance, are designed to fill-which is why understanding what flood insurance covers becomes essential for complete protection.

What Flood Insurance Actually Covers

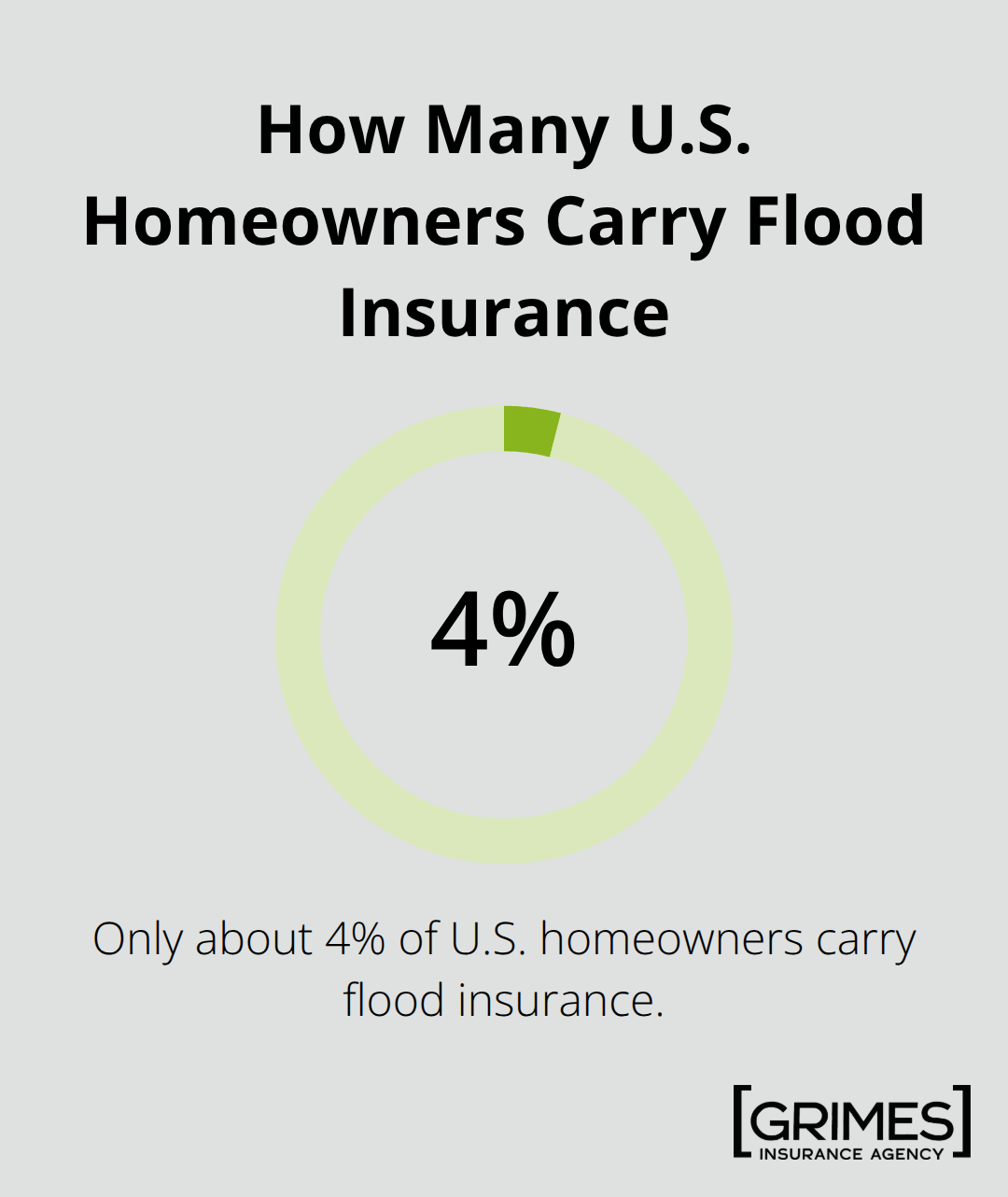

Flood insurance fills the gap that homeowners insurance leaves wide open. The National Flood Insurance Program, managed by FEMA, covers structural damage to your home caused by floodwaters-damage to your foundation, walls, electrical systems, plumbing, and HVAC equipment. It also covers personal belongings inside your home, up to $100,000 under the standard NFIP policy for residential contents. A single heavy rainfall event or overflowing river can destroy thousands of dollars worth of furniture, appliances, electronics, and clothing that homeowners insurance won’t touch. The coverage applies whether you live in a designated high-risk flood zone or not, which matters because roughly five times more homeowners experience flooding than home fires, yet only about 4% of U.S. homeowners carry flood insurance.

Flood insurance premiums vary dramatically by location and risk level. In low-risk areas, flood insurance costs less than $400 annually, making it surprisingly affordable protection. In high-risk zones like Plaquemines Parish, Louisiana, premiums exceed $5,400 per year-a reality that demonstrates why location matters enormously when assessing your actual exposure.

Waiting Periods Create Real Timing Risks

The NFIP imposes a 30-day waiting period before coverage begins, which means you cannot purchase a policy today and claim damages tomorrow. This delay creates vulnerability if you wait until storm season arrives or after heavy rain forecasts appear. Private flood insurance providers are re-entering the market in 2026 and often offer shorter or no waiting periods, higher coverage limits beyond the NFIP’s $250,000 cap for residential structures, and coverage for basements and detached structures that standard NFIP policies limit significantly.

Basement Coverage Gaps Demand Attention

Basements present a particular problem under traditional flood policies because coverage for below-ground areas is restricted, yet flooding often damages basement contents, mechanical systems, and foundation integrity most severely. If your home has a finished basement with stored valuables or critical systems, private flood insurance deserves serious consideration. Your mortgage lender may require flood insurance if your property sits in a high-risk zone, and that requirement appears in your loan documents and on official FEMA flood maps.

Finding Your Flood Zone Status

The key actionable step is to check your property’s flood zone status using FEMA’s Flood Map Service Center by entering your address-this free tool tells you exactly what risk category your home occupies and informs whether your lender will demand coverage. Understanding your specific flood zone status shapes every decision that follows about which coverage type fits your situation best.

Do You Actually Need Both Policies

Flood damage destroys homes that homeowners insurance won’t touch, and that gap between coverage types creates real financial exposure for most homeowners. Standard homeowners policies explicitly exclude flooding caused by heavy rainfall, overflowing rivers, storm surge, or any water that comes from outside your home’s structure. This exclusion exists because flood risk concentrates geographically, making it economically impossible for standard homeowners insurers to price the coverage fairly across their entire customer base.

Why Standard Policies Leave You Exposed

If you live anywhere near a river, in a low-lying area, or in a region with heavy seasonal rainfall, you face flood risk regardless of whether your property sits in an official high-risk zone. FEMA data shows that roughly five times more homeowners experience flooding than home fires over any 30-year period, yet this risk doesn’t translate into coverage under standard policies. Your mortgage lender will require flood insurance if your property falls within a designated high-risk flood zone, and that requirement appears explicitly in your loan documents. However, mortgage lenders cannot force you to buy flood insurance if your property sits outside a high-risk zone, which creates a dangerous gap where homeowners skip coverage they actually need.

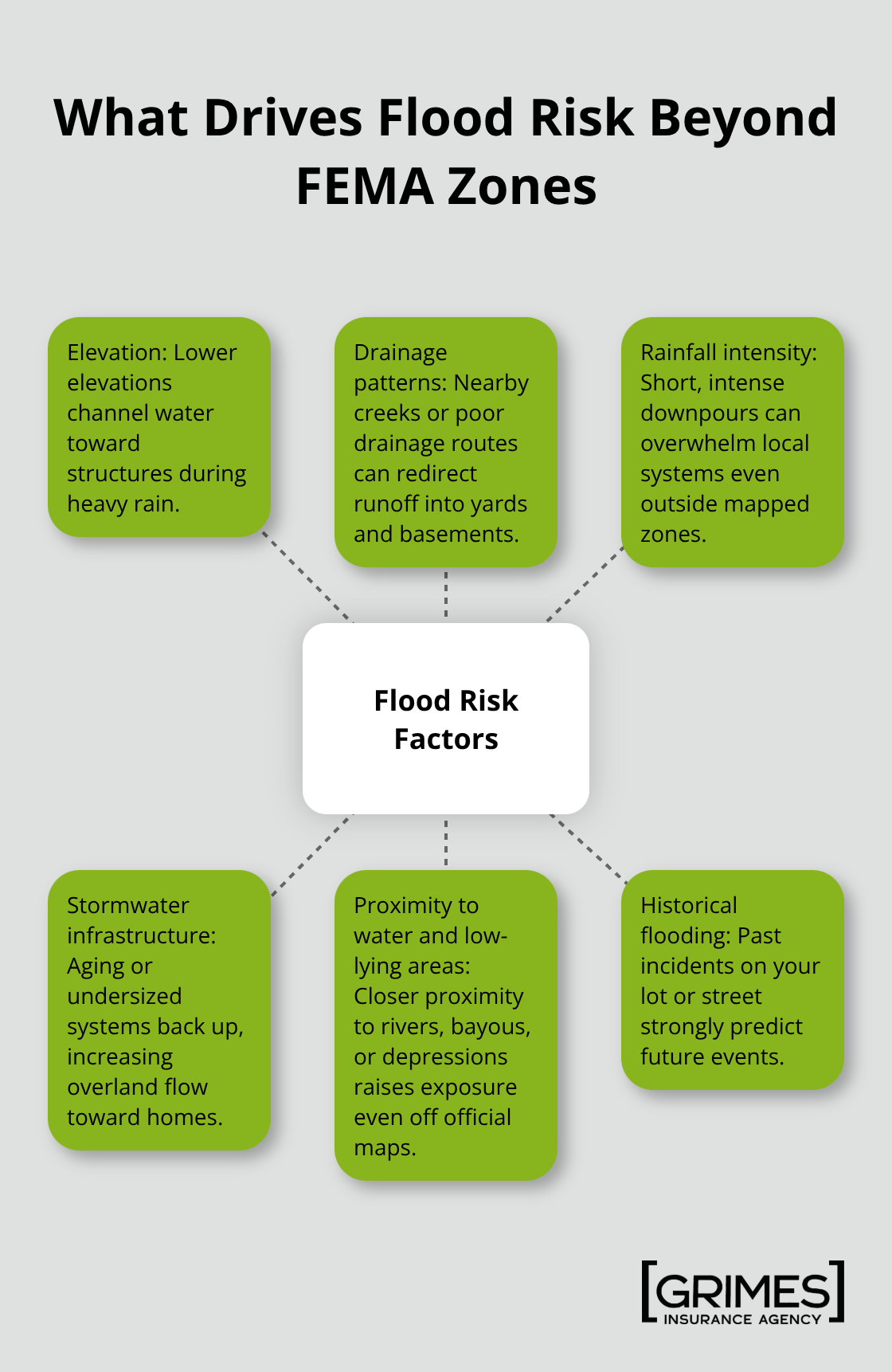

Properties Outside High-Risk Zones Still Flood

Properties located outside designated flood zones experience flooding regularly. FEMA reports that a large portion of flood claims come from areas outside high-risk zones, which means your location on an official flood map tells only part of the story about your actual exposure. Your elevation, proximity to drainage patterns, local rainfall intensity, and aging stormwater infrastructure all influence flood risk independently of FEMA’s zone designations.

Assess Your Real Flood Risk

Check your specific flood zone status using FEMA’s Flood Map Service Center, then assess whether your property has experienced flooding historically or sits in an area prone to water accumulation. If your lender requires flood insurance, you must carry it to maintain your mortgage. If your lender does not require it, carrying both policies still makes financial sense because the cost of flood insurance in low-risk areas runs less than $400 annually according to FEMA data, while a single flooding event can cost tens of thousands in uninsured damages.

Compare Your Coverage Options

Comparing flood insurance policies available in 2026 gives you better pricing and coverage terms tailored to your specific situation. A licensed insurance agent can review your property’s characteristics, compare multiple carriers, and help you understand whether NFIP coverage, private flood insurance, or a combination of both fits your actual risk profile and budget constraints. Evaluating flood risk independently rather than relying solely on mortgage requirements makes sense because lenders set requirements based on designated zones, not on the full picture of your property’s vulnerability.

Final Thoughts

Homeowners insurance and flood insurance serve fundamentally different purposes, and understanding the distinction between flood insurance vs homeowners insurance in 2026 protects your financial security. Homeowners insurance covers sudden damage from wind, hail, and fire, while flood insurance specifically covers water damage from heavy rainfall, overflowing rivers, and storm surge. Standard homeowners policies explicitly exclude flooding, which means a single heavy rain event can leave you with tens of thousands in uninsured damages if you lack flood coverage.

Your actual flood risk depends on far more than your FEMA flood zone designation. Properties outside designated high-risk zones experience flooding regularly, and FEMA data confirms that a large portion of flood claims originate from areas outside official flood zones. Your elevation, proximity to drainage patterns, local rainfall intensity, and stormwater infrastructure all influence whether water reaches your home during heavy weather, so checking your specific flood zone status using FEMA’s Flood Map Service Center takes minutes and provides the baseline information you need to assess your exposure accurately.

We at Grimes Insurance Agency recommend comparing your options with a licensed insurance agent who can evaluate your property’s specific characteristics and connect you with multiple carriers. An independent agent accesses both NFIP and private flood insurance options, helping you understand which coverage type or combination fits your risk profile and budget. Contact us today to review your current coverage and discuss whether flood insurance gaps exist in your policy.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation