Home Insurance Discounts Texas: How To Save On Your Premiums

Texas homeowners pay an average of $1,200 annually for home insurance, but most don’t realize how many discounts they’re leaving on the table. We at Grimes Insurance Agency help homeowners cut their premiums significantly by taking advantage of home insurance discounts in Texas that insurers rarely advertise.

The difference between paying full price and getting the right discounts can easily reach $300 to $500 per year. This guide walks you through the specific discounts available to you and the concrete steps to claim them.

Home Insurance Discounts That Save You the Most Money in Texas

Bundle Your Policies for Immediate Savings

Bundle your home and auto policies with the same carrier to receive discounts with many Texas insurers. This ranks as one of the fastest ways to lower costs without changing your coverage. Most Texas insurers apply the multi-policy discount automatically when you combine policies, but verify the discount appears in your policy documents before renewal. If bundling with your current insurer doesn’t beat standalone quotes from competitors, switch carriers. The savings only matter if they’re real.

Security Systems That Insurers Reward

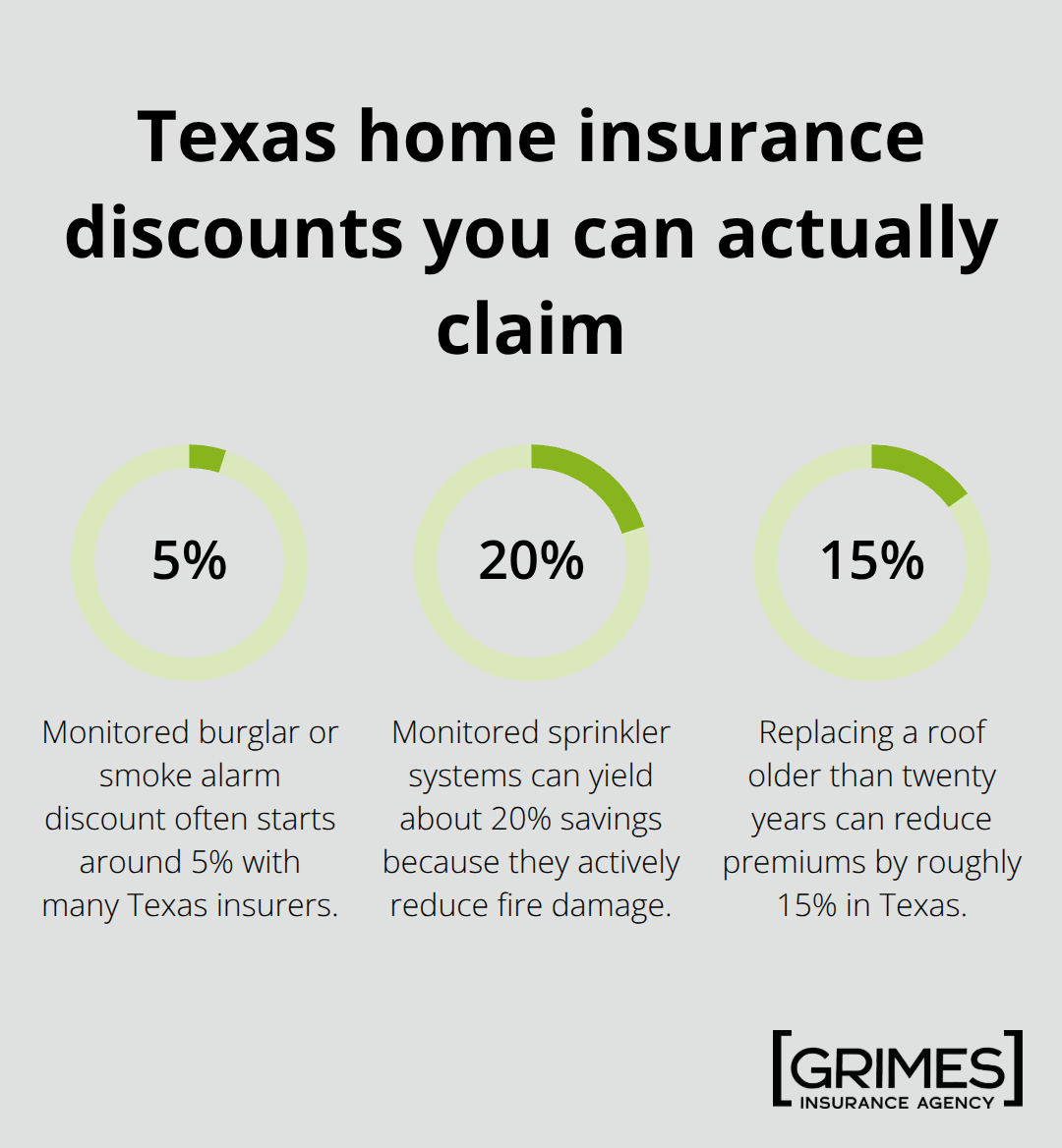

Monitored burglar alarms and smoke alarm systems qualify for discounts starting around 5 percent, though some insurers offer substantially more. The Texas Department of Insurance notes that monitored sprinkler systems can yield 15 to 20 percent savings because they actively prevent or reduce fire damage rather than just detect it. Your alarm system must meet your insurer’s standards to qualify, so contact your carrier before installing anything new. Smart home devices like leak detection systems also count toward discounts with many carriers, but ask which specific devices qualify before purchasing. The difference between a basic alarm and a monitored system often justifies the monthly cost through premium reductions alone.

Claims History as Your Strongest Asset

Staying claim-free for the past five years qualifies you for a meaningful discount with most Texas insurers. The Texas Department of Insurance emphasizes that this discount rewards responsible homeowners and directly reduces your renewal premium. Filing a small claim under your deductible rarely pays off, since one claim can wipe out years of claim-free savings and follow you for years. Many insurers track claims through the CLUE report, which potential future buyers see when purchasing your home, so frequent claims also complicate selling. Your claims history matters more than any single discount because it affects your insurability across the entire market, making it the foundation for long-term savings.

What Really Drives Your Texas Home Insurance Rates

Weather Risk Sets Your Premium Foundation

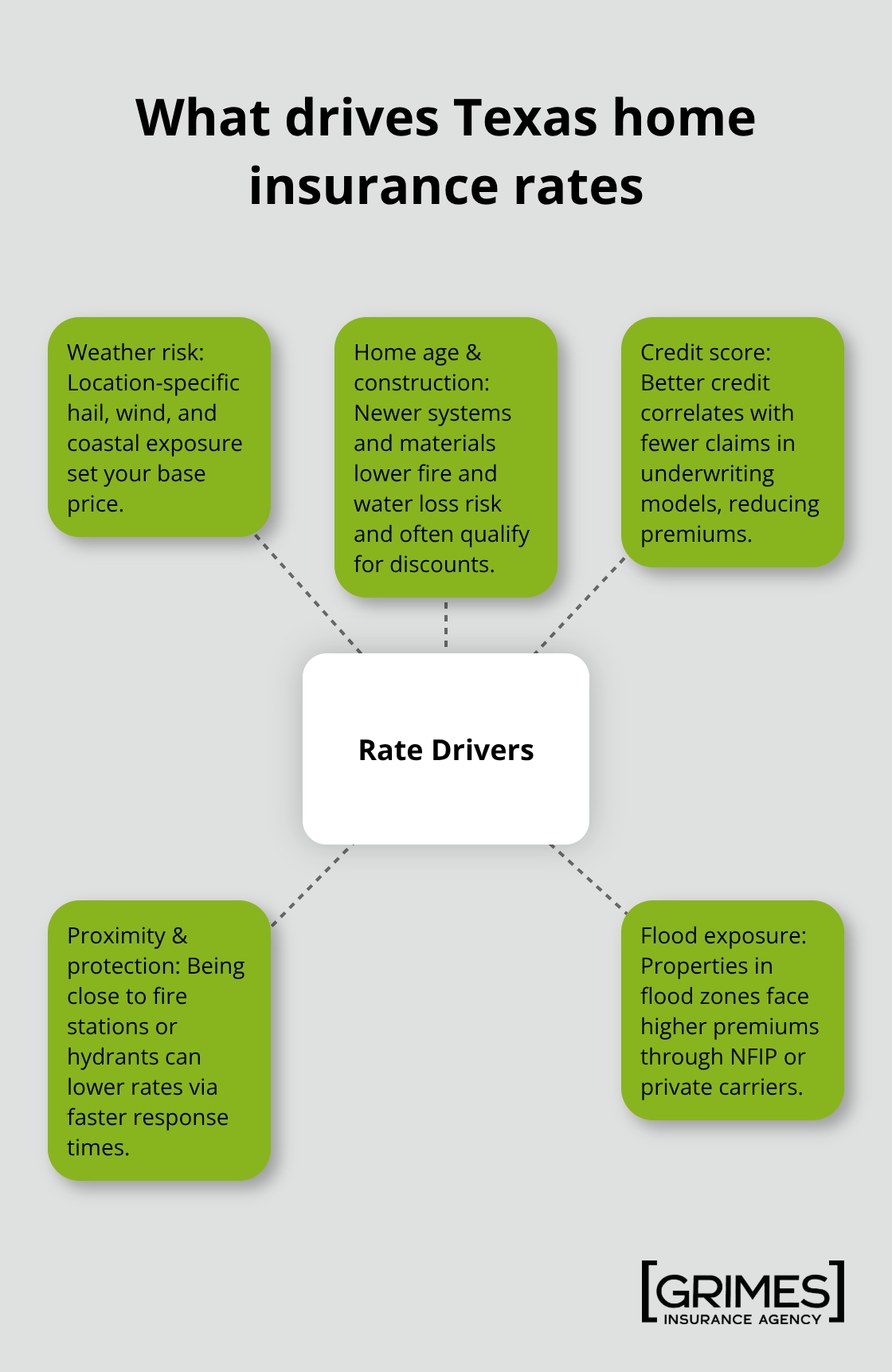

Weather risk in Texas is the single most important factor determining your premium, and insurers price it aggressively based on your exact location. Homes near the Gulf Coast or in hail-prone areas like the Texas Panhandle pay substantially more than homes in safer regions because the risk of catastrophic loss is genuinely higher. Your proximity to a fire station or hydrant directly reduces your rate because response time matters in fire claims. Insurers also consider whether your neighborhood sits in a flood zone, even if you don’t think flooding is likely-the NFIP and private carriers charge dramatically more for flood-exposed properties.

Home Age and Construction Quality Impact Costs

Home age and construction materials affect your rate because newer homes have updated electrical systems, plumbing, and roofing that reduce fire and water damage risk. Homes built or substantially renovated within the last five years qualify for new home discounts that can reach 8 to 15 percent according to the Texas Department of Insurance. If your roof is over fifteen years old, expect higher premiums regardless of its condition, and upgrading to impact-resistant materials in a hail-prone area can lower your rate.

Credit Score Influences Your Rate More Than You Think

Your credit score directly impacts pricing with most Texas insurers because payment history correlates with claims frequency in their underwriting models. A 50-point improvement in your credit score can reduce your premium by 5 to 10 percent. If your credit is poor, fixing it should be your first priority before shopping for insurance, since the savings will compound across your entire policy term and may exceed the value of any single discount.

Location Decisions Have Long-Term Financial Consequences

If you’re shopping for a home, location should influence your decision as much as the house itself because a $50,000 difference in purchase price could easily cost you $200 to $300 annually in higher insurance premiums over thirty years. Understanding these rate drivers positions you to make smarter choices about where you live and what improvements deliver the highest return on your insurance investment-which leads directly to the actionable steps that actually lower your costs.

Actionable Steps to Lower Your Home Insurance Costs

Compare quotes from multiple carriers

Shopping around takes thirty minutes but saves most Texas homeowners $300 to $500 annually. The Texas Department of Insurance recommends comparing quotes every three years at minimum, though market conditions shift faster in Texas due to weather volatility. When you request quotes, provide identical coverage limits and deductibles across all carriers so you’re comparing apples to apples.

Many homeowners make the mistake of lowering coverage to reduce premiums, which leaves them underinsured when a claim hits. Instead, focus on comparing the same dwelling limit, personal property coverage, and liability limits across at least three carriers. If your current insurer’s quote is significantly higher than competitors offering identical coverage, switch carriers. Some insurers charge more simply because you haven’t shopped in years, and they’re betting you won’t bother looking elsewhere.

Request All Available Discounts Explicitly

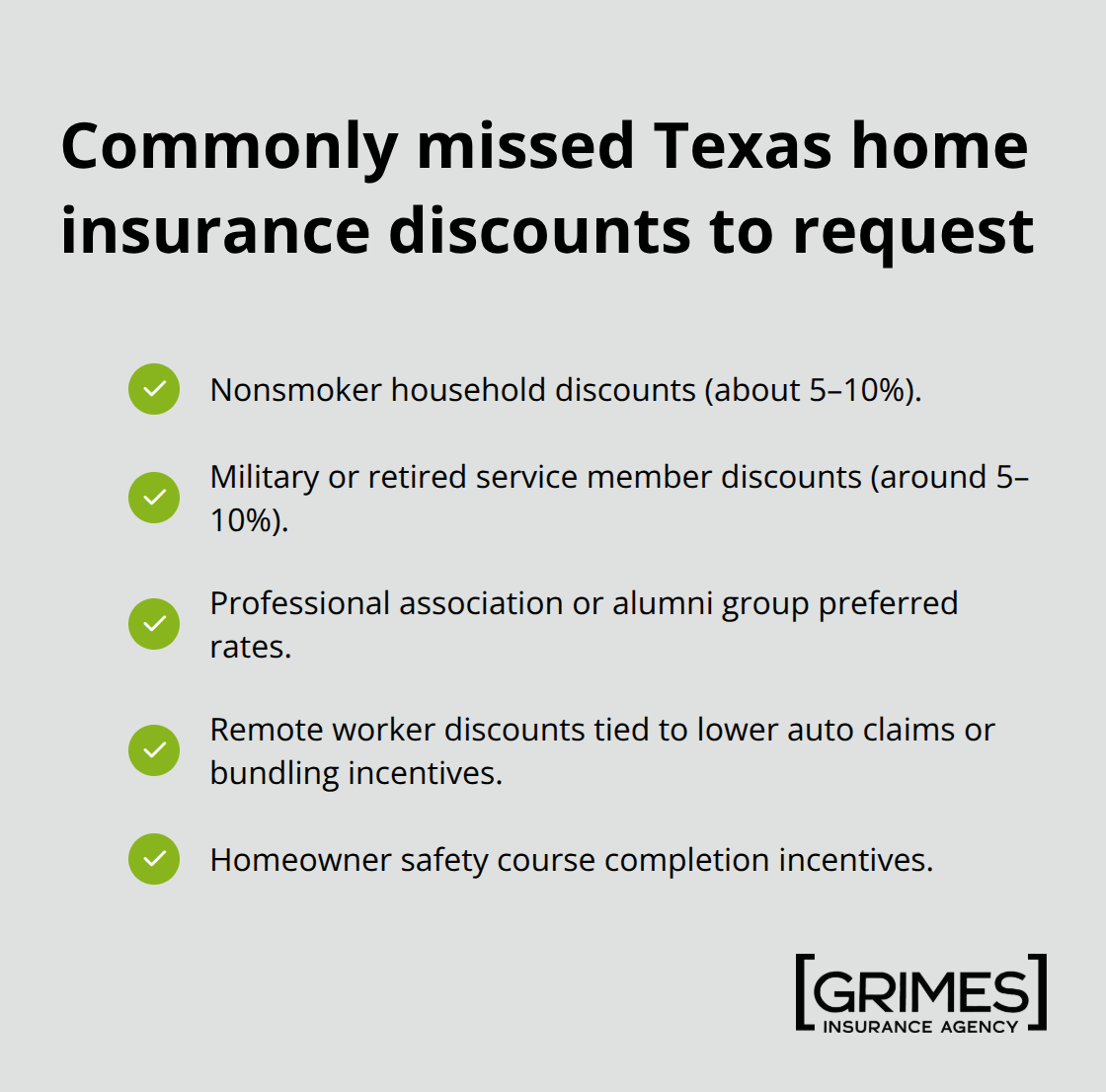

Ask each carrier about discounts before finalizing your quote, since some discounts don’t appear automatically and require you to request them explicitly. Lesser-known discounts often outpace the standard ones everyone mentions. Nonsmoker discounts exist with several Texas carriers and can reach 5 to 10 percent if no household member smokes.

Military service members and retirees qualify for discounts around 5 to 10 percent depending on the insurer, and some professional associations or alumni groups offer preferred rates to members. Remote workers may qualify for discounts because reduced commuting means lower auto insurance claims, which some insurers extend to home policies as bundling incentives. Ask your insurer whether completing a homeowner safety course qualifies you for a discount, as some carriers reward this proactively.

Invest in Home Improvements That Reduce Risk

Home improvements matter most when you report them to your insurer. Upgrading electrical wiring, replacing plumbing, installing a new roof, or adding impact-resistant materials can lower your rate significantly, but only if you notify your insurer. The Texas Department of Insurance emphasizes that major renovations should trigger a policy review because they reduce risk and often qualify for additional discounts.

Create a documented record of improvements with photos and receipts, then contact your agent to request a rate review. Roof age is tracked carefully by insurers, and replacing a roof older than twenty years can reduce your premium by 10 to 15 percent, making the investment financially sensible beyond just maintenance. These upgrades directly lower your risk profile in the eyes of underwriters, which translates to real savings at renewal.

Final Thoughts

The home insurance discounts Texas homeowners qualify for add up quickly when you take action on bundling policies, installing monitored security systems, and maintaining a clean claims history. Weather risk, home age, and credit score determine your baseline rate, but these three discount categories directly counteract those factors and put savings back in your pocket. That $300 to $500 annual difference between paying full price and getting smart discounts represents money you’ve already earned through responsible homeownership.

A local agent matters because they know Texas-specific risks and which carriers offer the best rates for your exact situation. An independent agent accesses multiple carriers simultaneously, eliminating the need to contact each insurer separately and compare quotes manually, while also catching discounts you’d miss on your own. They understand how weather exposure, home age, and location affect pricing in your neighborhood far better than generic online tools.

Your next step is straightforward: request quotes from at least three carriers with identical coverage limits, then contact Grimes Insurance Agency to compare what you’ve found. We’ll identify discounts you missed and show you exactly how much you can save by switching or adjusting your current policy. The thirty minutes you invest in this process pays dividends for years.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation