Flood Insurance for Landlords: Protecting Rental Properties

Rental property owners face a harsh reality: standard homeowners insurance policies exclude flood damage entirely. This gap in coverage can devastate your finances when water damage strikes.

At Grimes Insurance Agency, we help landlords understand that flood insurance for landlords isn’t optional-it’s a business necessity. Your rental income and property value depend on it.

Why Flood Insurance Isn’t Optional for Landlords

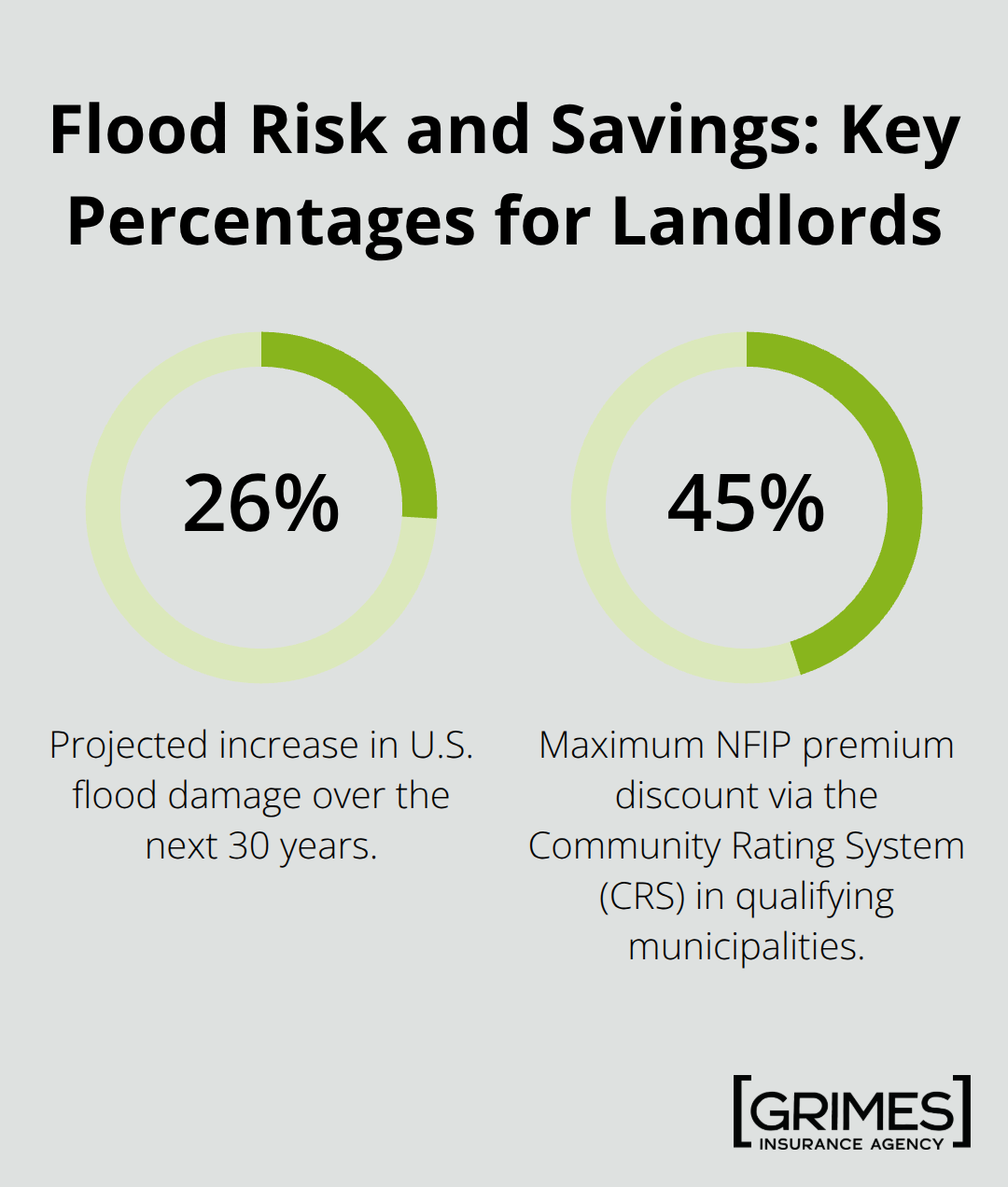

Standard landlord insurance policies create a dangerous blind spot for rental property owners. Your typical homeowners or landlord policy covers wind, hail, theft, and fire, but it does not cover flood damage. This isn’t a small limitation-it’s a complete coverage gap that leaves your property and income vulnerable. When heavy rain, river overflow, or storm surge damages your rental unit, your standard policy pays nothing. FEMA data shows that more than 40% of flood claims come from properties outside designated high-risk flood zones, meaning risk exists whether you live in a coastal area or inland. Climate change intensifies this threat; flood damage will rise by approximately 26% over the next 30 years according to federal projections.

If you own rental properties, you protect not just a structure but your cash flow. Tenant displacement after a flood costs you months of lost rent while repairs happen, and your standard policy provides zero coverage for that income loss.

How Floods Damage Your Bottom Line

Floods hit your finances in multiple ways that most landlords don’t anticipate. Beyond immediate property damage, you lose rental income the moment water enters the building. Your tenant evacuates, repairs begin, and you receive no rent checks while the property sits damaged. Private flood policies from some insurers offer loss-of-rent endorsements that cover this gap, but standard NFIP policies do not. Without this protection, a single flood event can wipe out six months to a year of profits depending on repair timelines. Roughly 2.4 million occupied rental units sit in FEMA Special Flood Hazard Areas, and flooding remains the most common and costliest disaster across all 50 states. Your property location matters less than you think; floods happen everywhere, and renters in flood-prone areas often have fewer financial resources to absorb losses, meaning they may break leases or require extended vacancy periods after water damage. Flood insurance premiums vary widely-from $600 annually for low-risk properties to $12,000 or more for coastal high-risk zones-but that expense is minor compared to the cost of repairing a flooded rental unit without coverage.

How Elevation Certificates Lower Your Premiums

An Elevation Certificate prepared by a licensed surveyor can significantly reduce your flood insurance premiums by documenting your property’s exact relationship to the base flood elevation. This single document often translates to hundreds of dollars in annual savings. Communities that implement flood mitigation measures offer Community Rating System discounts that can reduce NFIP premiums by up to 45%, so understanding your local flood preparedness programs matters. Mitigation investments like flood vents, elevated HVAC systems and electrical panels, or yard grading that slopes away from the building lower both your risk profile and your insurance costs. Private flood insurers increasingly use advanced risk modeling to assess properties more precisely than older methods, which can result in lower premiums as the market matures.

What Information You Need to Gather

The key is gathering your property information early so you can obtain accurate quotes and understand your true exposure. Collect your flood zone designation, construction date, building elevation, and any prior flood history. This documentation allows you to compare quotes across NFIP and private carriers and identify which coverage option fits your rental portfolio best. With this information in hand, you’re ready to evaluate the specific coverage options available to you.

Coverage Options for Your Rental Property

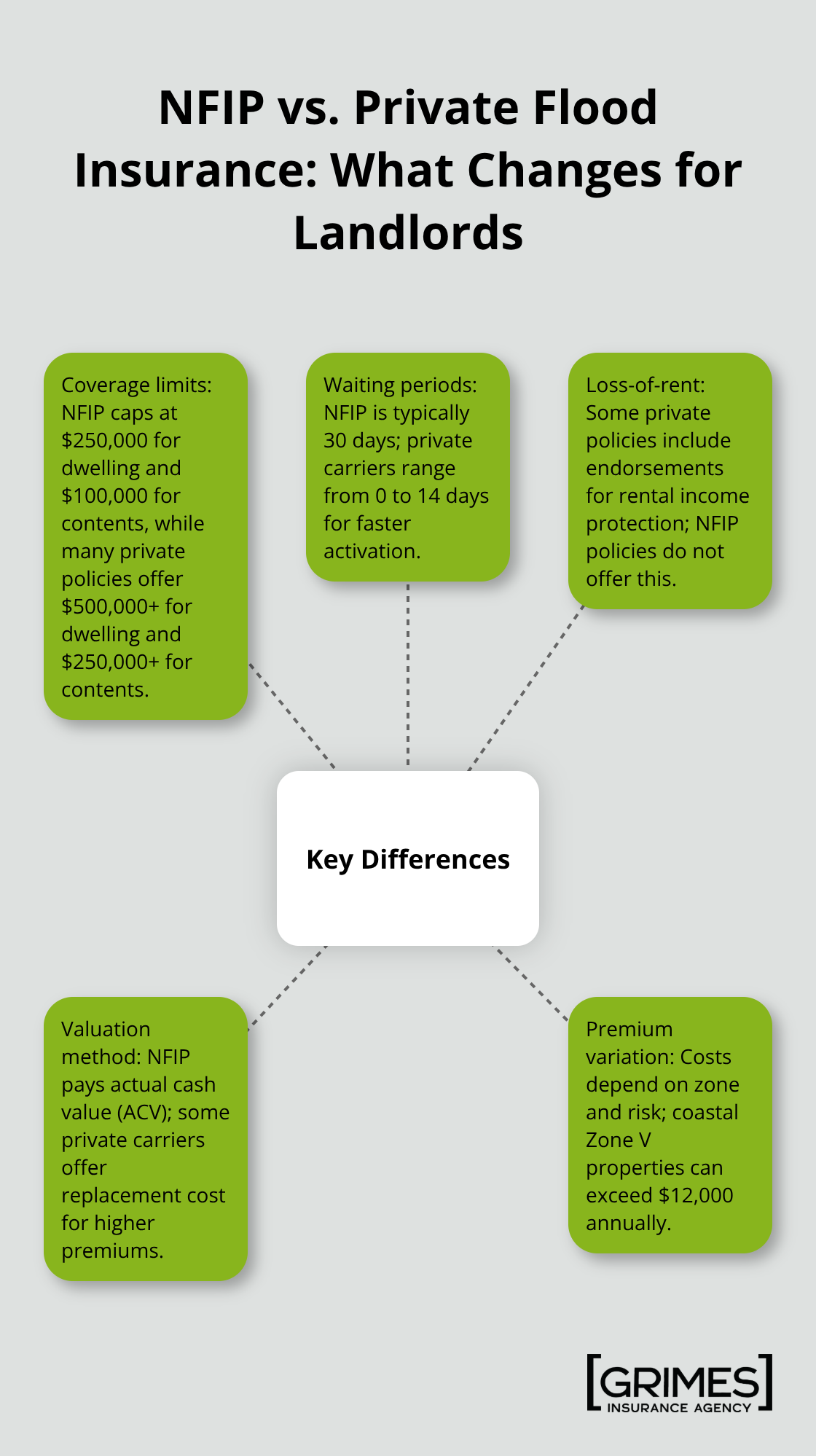

The National Flood Insurance Program and private flood carriers both serve landlords, but they differ significantly in coverage limits, waiting periods, and cost structure. NFIP policies cap dwelling coverage at $250,000 and contents coverage at $100,000, while private flood policies often reach $500,000 or higher for dwelling coverage and $250,000 or more for contents. For landlords with valuable rental properties or furnished units, this difference matters enormously.

Speed of Coverage Activation

NFIP policies typically enforce a 30-day waiting period before coverage activates, meaning you cannot buy protection during an active storm and have it take effect immediately. Private carriers can offer waiting periods as short as zero to 14 days, which gives you faster protection if you move quickly. This speed advantage matters most when storm forecasts threaten your area and you need immediate coverage.

Premium Costs Across Risk Zones

Annual premiums vary dramatically by flood zone and property characteristics. Low-risk Zone X properties pay roughly $600 to $1,200 per year through NFIP, while high-risk Zone A or AE properties climb to $1,500 to $5,000 or higher. Coastal high-risk Zone V properties can exceed $12,000 annually. The critical difference for rental income is that some private flood policies include loss-of-rent endorsements covering your lost income during repairs, while NFIP policies do not offer this protection at all. This gap can cost you thousands in unreimbursed lost rent after a single flood event.

How Payouts Work: ACV vs. Replacement Cost

NFIP pays actual cash value rather than replacement cost, meaning your 10-year-old roof damaged in a flood receives a payout reflecting depreciation, not the full cost to replace it. Some private carriers offer replacement-cost coverage, which eliminates this depreciation penalty but typically costs more. Understanding this distinction prevents you from expecting full replacement funds when your policy pays only depreciated value.

What Your Policy Covers and What It Excludes

Your flood insurance must cover the structure itself including plumbing, electrical systems, HVAC, and cabinets, plus you can add coverage for personal property like furniture and appliances. However, NFIP policies exclude pools, decks, fences, landscaping, and retaining walls entirely, so understand what sits outside your protection. Detached garages receive coverage under NFIP if listed, but verify this on your policy. Mold damage from flooding often falls outside coverage limits, creating a hidden liability that requires separate mitigation efforts.

Reducing Your Premiums Through Documentation and Discounts

An Elevation Certificate prepared by a licensed surveyor reduces your premium costs substantially because it documents your property’s exact elevation relative to the base flood elevation. Community Rating System discounts in municipalities that invest in flood mitigation can trim NFIP premiums by up to 45%, so check whether your rental location qualifies. Private flood insurers increasingly employ advanced risk modeling using AI and satellite data, which can result in lower premiums as their pricing matures and becomes more granular. Comparing quotes across both NFIP and private carriers takes effort but directly impacts your bottom line; a difference of $500 to $2,000 annually across multiple properties compounds significantly. Your insurance agent can request quotes from both NFIP through the Write Your Own program and private carriers licensed in your state so you can see the true cost and coverage differences for your specific rental properties. Once you understand which coverage option fits your portfolio, the next step involves assessing your property’s actual flood risk and gathering the documentation that insurers require to provide accurate quotes.

How to Get the Right Flood Insurance Quote for Your Rental

Identify Your Property’s Flood Zone

Start with FEMA’s Flood Insurance Rate Map or their free property-level flood risk tool to identify your rental’s flood zone designation. This step takes minutes and determines whether your property sits in a high-risk Special Flood Hazard Area or lower-risk zone, which directly affects your premium costs. FEMA maps show zone letters like A, AE, V, VE for high-risk areas or B, C, D, and X for moderate to low-risk zones. Know your zone before contacting an insurance agent because zone designation shapes your entire quote comparison. If your property has a federally backed mortgage and sits in an SFHA, flood insurance is mandatory regardless of cost, so understanding this requirement upfront prevents surprises during the underwriting process.

Prepare Your Property Documentation

Gather your property’s construction date, building elevation, square footage, number of stories, and any prior flood history or claims. Contact a licensed surveyor to obtain an Elevation Certificate if you don’t already have one, as this document can reduce your NFIP premium by unlocking flood insurance discounts. Document whether your rental has flood vents, elevated utilities, or other mitigation features because these reduce your risk profile and lower quotes from private insurers. Photograph your property’s drainage patterns, proximity to water sources, and any past water damage, as this documentation helps agents request accurate quotes and supports claims if flooding occurs later.

Request Quotes from Multiple Carriers

Contact insurance agents who represent multiple flood insurance providers.

Request quotes from both the National Flood Insurance Program through the Write Your Own program and private flood carriers licensed in your state. Compare the dwelling coverage limits, contents coverage limits, waiting period length, annual premium, deductible options, and whether the policy includes loss-of-rent endorsements. A private policy offering $500,000 dwelling coverage with a loss-of-rent endorsement might cost $1,200 annually while NFIP offers $250,000 dwelling coverage without rental income protection for $1,100, making the private option worth the extra $100 per year when you factor in potential lost rent during repairs.

Evaluate Coverage Details and Exclusions

Review policy exclusions carefully, particularly around mold coverage and exterior features like pools or decks, since these gaps can create unexpected out-of-pocket costs after a flood event. Ask your agent whether your municipality qualifies for Community Rating System discounts, which can trim NFIP premiums by up to 45% in communities implementing flood mitigation measures. Private flood insurers increasingly employ advanced risk modeling using AI and satellite data, which can result in lower premiums as their pricing matures and becomes more granular. Comparing quotes across both NFIP and private carriers takes effort but directly impacts your bottom line; a difference of $500 to $2,000 annually across multiple properties compounds significantly. Your insurance agent can request quotes from both NFIP and private carriers licensed in your state so you can see the true cost and coverage differences for your specific rental properties. Once you’ve compared options and selected your coverage, your agent will guide you through the application process, and your policy will activate after the waiting period expires, providing your rental property with the protection it needs against flood damage and the income loss that follows.

Final Thoughts

Flood insurance for landlords protects your rental income and property value when water damage strikes, and standard landlord policies refuse to cover this risk. A single flood event can eliminate months of rental income, force expensive out-of-pocket repairs, and leave your investment vulnerable to losses that your existing coverage ignores. The data confirms what many landlords overlook: floods happen in all 50 states, and more than 40% of claims come from properties outside high-risk zones, meaning your location offers no safety guarantee.

You have real choices that fit your specific rental portfolio. The National Flood Insurance Program offers affordable baseline protection with coverage limits up to $250,000 for dwelling and $100,000 for contents, while private flood carriers provide higher limits, faster coverage activation, and loss-of-rent endorsements that reimburse your lost income during repairs. This flexibility lets you customize your protection to match your financial needs rather than accepting a one-size-fits-all solution.

Contact Grimes Insurance Agency today to discuss your flood insurance options and secure your rental investment against future losses. Our team specializes in real estate investor insurance and can connect you with multiple carriers to find the coverage that fits your properties and budget. We help landlords in Lubbock and beyond protect what matters most.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation