How to Protect Commercial Properties Effectively: Essential Strategies for Landlords

Commercial property owners face real threats every day-from break-ins and fires to liability claims that can drain resources fast. The difference between a protected investment and a vulnerable one often comes down to preparation and the right coverage.

We at Grimes Insurance Agency help landlords understand how to protect commercial properties effectively through smart planning and comprehensive insurance solutions. This guide walks you through the essential strategies that matter most.

Real Threats That Hit Commercial Properties Hard

Break-Ins and Theft Drain Resources Fast

Break-ins and theft cost commercial properties an estimated 12 to 14 billion dollars annually in the United States. Most incidents occur at properties with weak perimeter security or poor access controls. Properties with clear entry points, inadequate lighting, and no integrated surveillance systems become targets.

The commercial security system market was valued at USD 210.6 billion in 2024 and is projected to reach USD 374.1 billion by 2030, reflecting how seriously property owners take these threats.

Start with a comprehensive site assessment that evaluates your perimeter continuity, identifies all entry points, and maps out vehicle and pedestrian traffic patterns. Properties with multiple buildings, numerous access points, and shared roadways face compounded risk because each gap creates an opportunity. Biometric access systems and cloud-based surveillance platforms with AI-powered video analytics now allow real-time threat detection and reduce false alarms that drain resources. Gate selection matters too; prioritize gates that offer flexibility, durability, and compatibility with future site changes so you adapt without disrupting operations.

Fire and Natural Disasters Accelerate Damage

Fire and natural disasters present equally serious threats, especially as climate impacts accelerate. The United States experienced 27 billion-dollar weather disasters in 2024 alone, driving property damage and insurance costs higher across commercial portfolios. Coastal properties face heightened threats from rising sea levels, saltwater corrosion, and storm surges that threaten both value and safety. Flooding and excess moisture heighten mold risk and structural damage, increasing maintenance costs and reducing property appeal to tenants.

Weatherproofing, reinforced roofing, flood barriers, and storm-resistant windows reduce claims and signal to insurers that you take risk seriously, often resulting in lower premiums. Schedule regular inspections on HVAC systems, fire suppression equipment, parking areas, lighting, and exterior structures. Address compliance with ADA accessibility standards, fire and safety codes, and signage requirements without relying on tenants to flag violations.

Liability Claims From Injuries Escalate Quickly

Liability claims from injuries on premises rank third among major threats, and they escalate quickly when clear hazards exist. Weak lighting in common areas, deferred maintenance on stairs or roofs, and unclear emergency protocols all increase injury risk and litigation exposure. Social inflation pushes litigation costs higher, meaning a single injury claim costs significantly more than it did five years ago.

Proactive maintenance on all building systems protects both occupants and your bottom line. The next section covers how the right insurance coverage works alongside these physical protections to create a complete defense strategy.

How to Spot and Fix Security Gaps Before They Cost You

Map Every Entry Point on Your Property

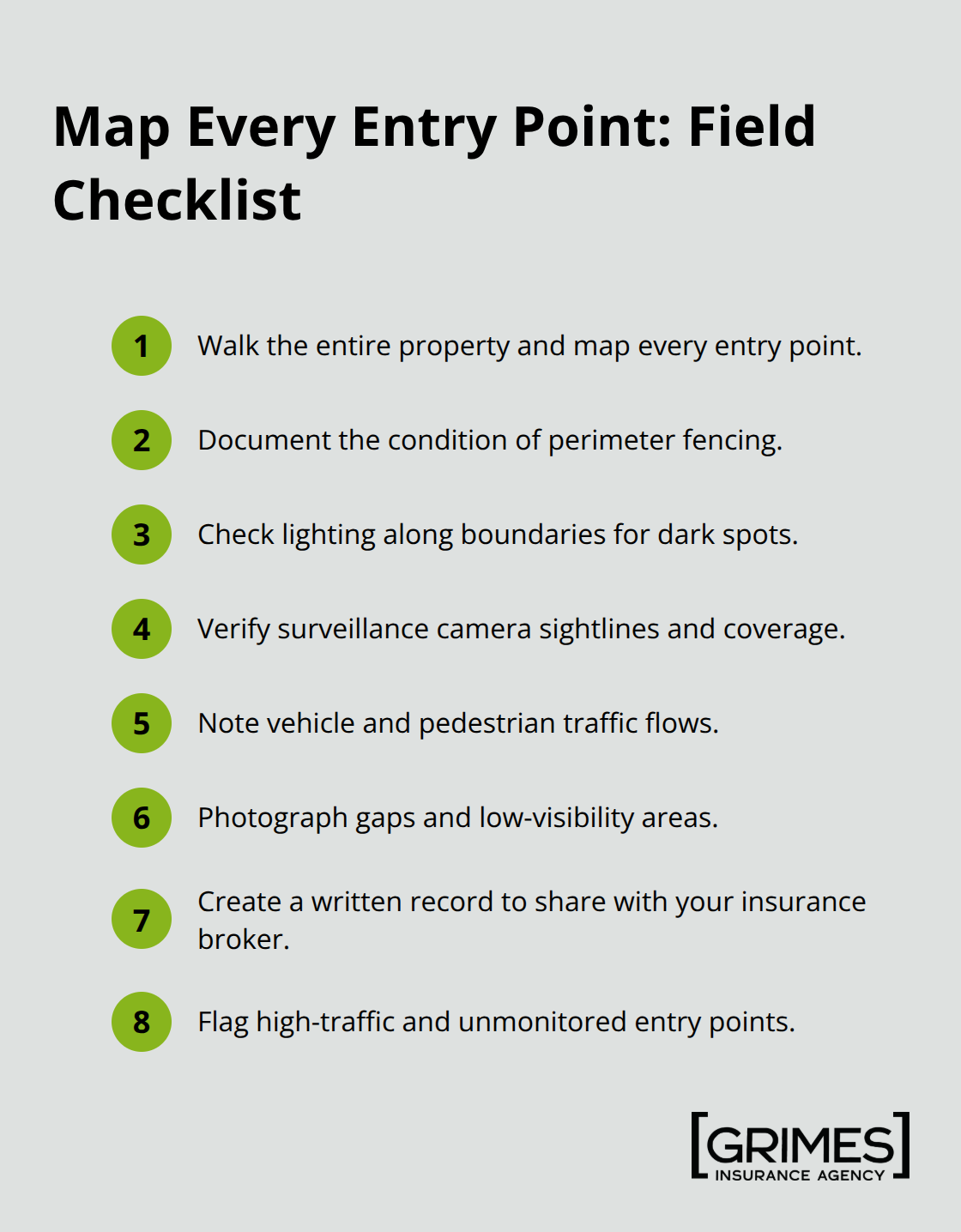

Start with a site assessment that covers everything. Walk your entire property and map every entry point, from main gates to loading docks to roof access. Document the condition of perimeter fencing, lighting along boundaries, and sightlines from your surveillance cameras. Note where vehicles move through your property and where pedestrians walk. Properties with multiple buildings or shared roadways create blind spots that criminals exploit, so photograph and measure distances between buildings, fence discontinuities, and areas where visibility drops. This isn’t theoretical work; you need a written record you can reference later and share with your insurance broker.

Many landlords skip this step and only react after a break-in or injury occurs, which means they’ve already lost ground. Your assessment should identify which entry points see the most traffic and which ones sit unmonitored.

Prioritize Fixes by Risk Level

After you’ve mapped vulnerabilities, prioritize fixes by exposure and likelihood. Reinforce main gates first because they control the largest volume of traffic and set the tone for security. High-traffic gates need robust access controls that don’t slow operations, while secondary entrances may need reinforcement or closure entirely. If your property has loading areas or service entrances, these typically rank as the highest-risk zones because they blend legitimate traffic with potential unauthorized access. Properties near busy roadways or with high vehicle traffic need vehicle barriers or bollards to separate pedestrian zones from traffic zones, reducing both collision and intentional vehicle-based threats.

Deploy Technology That Works in Real Time

Install biometric access systems or cloud-based platforms with AI-powered video analytics to detect threats in real time rather than reviewing hours of footage after an incident. Address lighting gaps in parking areas and along perimeter fences because poor visibility invites break-ins and increases injury risk during emergencies. These upgrades signal to insurers that you take risk seriously, often resulting in lower premiums. Work with your insurance broker to align these improvements with your coverage requirements; many carriers offer premium discounts for documented security upgrades.

Maintain Systems on a Regular Schedule

Schedule regular inspections of fire suppression systems, HVAC equipment, and emergency exits at least quarterly. Don’t wait for a system failure or compliance violation to act. A phased approach works better than trying to fix everything at once, so develop a prioritized action plan that spreads costs over time while addressing your highest-risk exposures first. This foundation of physical security and maintenance sets the stage for selecting the right insurance coverage that protects what you’ve built.

Insurance Coverage That Matches Your Property’s Real Exposure

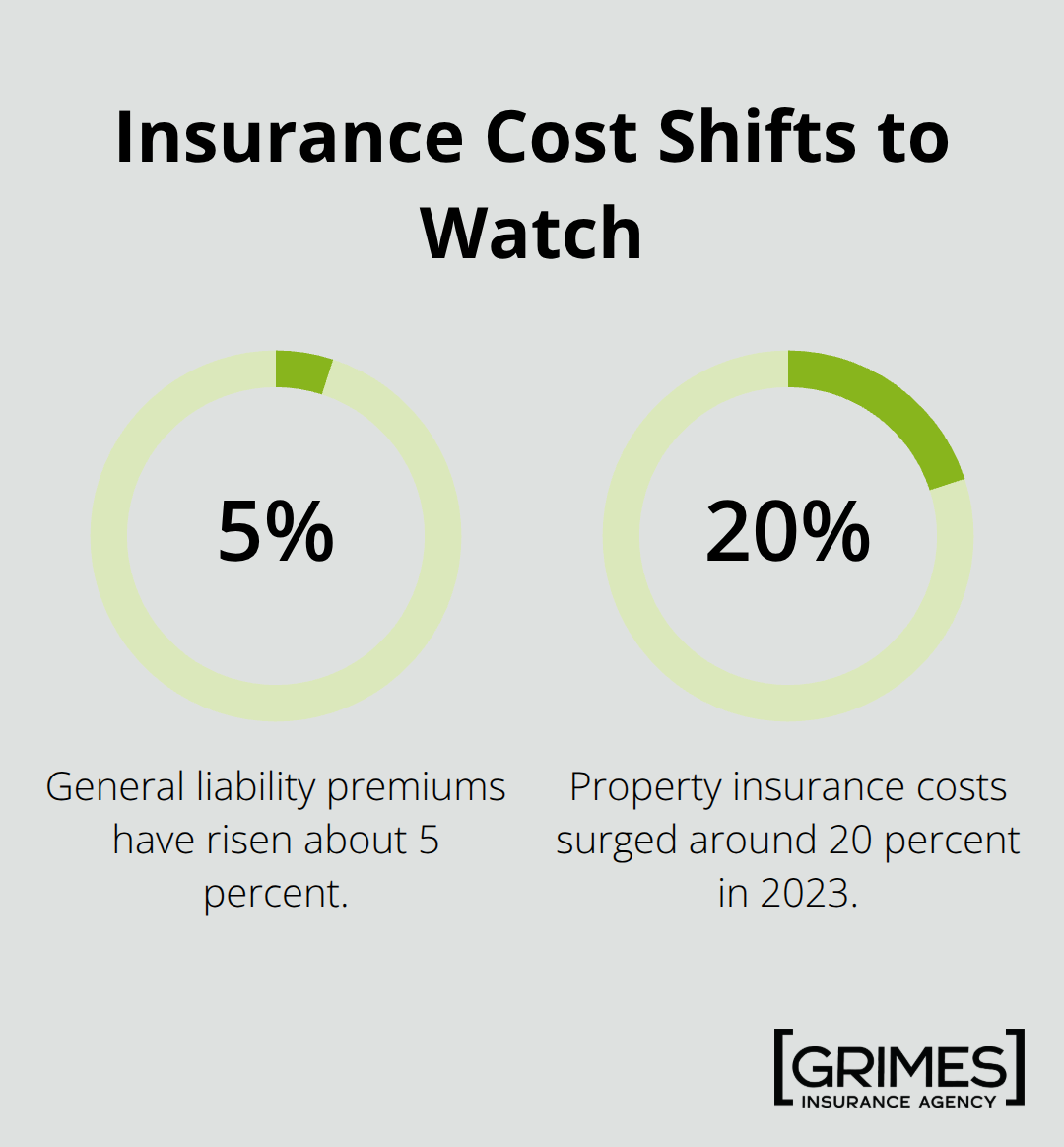

Commercial property insurance protects the physical structure, equipment, and fixtures on your premises, but coverage limits matter more than most landlords realize. General liability premiums have risen about 5 percent, and property insurance costs surged around 20 percent in 2023 as insurers tightened policies and raised minimum coverage requirements.

Your property value isn’t static, so coverage limits that worked three years ago no longer reflect rebuilding costs driven by inflation and supply chain disruptions. Review your policy annually with your broker and increase limits to match current replacement costs for the building, roofing systems, HVAC equipment, and any tenant improvements you’ve financed. Underinsurance leaves you exposed; a fire that destroys 40 percent of your structure could wipe out years of profit if your limit falls short of actual rebuilding expense.

What Your Property Insurance Must Actually Cover

Property insurance covers the building structure, permanent fixtures, and equipment you own, but exclusions vary widely between carriers. Standard policies exclude flood damage, which requires a separate flood insurance policy through the National Flood Insurance Program or private carriers, and many exclude earthquake damage unless you add an endorsement. If your property has a flat roof, some carriers impose stricter maintenance requirements or charge higher premiums because flat roofs face greater exposure to pooling water and weather damage. Document all property improvements, equipment installations, and upgrades with photos and receipts because these increase your insurable value and help insurers understand your actual replacement costs if a loss occurs.

Liability Coverage Protects Against Injury Claims

Liability coverage protects you when a tenant, customer, or visitor suffers an injury on your property and sues for damages. General liability policies typically cover bodily injury and property damage claims, with standard limits ranging from 1 million to 5 million dollars depending on property size and risk profile. However, social inflation drives litigation costs higher than they were five years ago, so a single injury claim now costs significantly more to defend and settle. Review your liability limits every two years, especially after property improvements or changes in tenant mix that increase foot traffic or operational complexity.

Business Interruption Coverage Protects Revenue During Shutdowns

Business interruption insurance reimburses lost rental income when a covered event forces tenants to vacate or prevents them from operating. A fire that closes your building for four months doesn’t just mean repair costs; it means four months of zero rent while your mortgage, property taxes, utilities, and debt service continue. This coverage pays the difference between actual rental income and normal income during the interruption period, plus some policies cover extra expenses needed to resume operations faster. If your property houses essential services like healthcare or data centers, business interruption coverage becomes even more valuable because downtime cascades into tenant losses that trigger additional liability claims.

Alternative Risk Transfer Options for High-Risk Properties

Parametric insurance offers another approach, paying a fixed amount when a specific trigger occurs-such as a hurricane of a certain intensity hitting your county-without requiring you to prove actual losses. This speeds claims payment and works well for properties in high-risk climate zones where traditional coverage has become expensive or hard to obtain. Consider alternative risk transfer options such as captives or parametric insurance for greater flexibility and cost control, especially if your portfolio spans multiple regions or includes properties with elevated climate exposure.

Final Thoughts

Protecting commercial properties effectively requires three interconnected layers: physical security upgrades, regular maintenance systems, and comprehensive insurance coverage. A reinforced gate means little without liability coverage for injuries that still occur on your property, and a fire suppression system matters only if your business interruption insurance covers lost rent during repairs. The most successful landlords treat property protection as an ongoing process, not a one-time project.

Schedule quarterly inspections of critical systems, review insurance limits annually as replacement costs climb, and adjust security measures when tenant mix or traffic patterns change. Document everything with photos and receipts because this record protects you during claims and helps insurers understand your actual exposure. Rising insurance costs and tightening coverage requirements mean landlords who stay proactive pay less and recover faster when losses occur.

Contact Grimes Insurance Agency to review your current coverage against your property’s actual replacement costs and risk profile. We at Grimes Insurance Agency have over 75 years of experience helping real estate investors in Lubbock, Texas and beyond secure comprehensive protection across multiple carriers. Our team specializes in real estate investor insurance and understands the specific gaps that leave landlords exposed.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation