Flood Risk Assessment for Home Insurance: Ensuring Adequate Coverage

Flooding is one of the most common and costly natural disasters in the United States, yet most homeowners don’t realize their standard insurance won’t cover it. A flood risk assessment for home insurance is the first step toward protecting your property and finances.

At Grimes Insurance Agency, we help homeowners understand their actual flood exposure and find the right coverage. This guide walks you through evaluating your risk and selecting adequate protection.

How FEMA Flood Maps Shape Your Insurance Costs

Understanding Your Flood Zone Designation

FEMA flood maps form the foundation of flood insurance requirements and pricing, yet most homeowners never check theirs. Your address falls into one of four zones-High Risk (Zones A and V), Moderate Risk (Zone X), Low Risk (Zone X), or Undetermined Risk (Zone D)-and this designation directly affects whether your lender mandates flood insurance and what you’ll pay for it. High-risk zones like Zone A or coastal Zone VE require flood insurance if you have a federally backed mortgage, while moderate and low-risk zones are optional but strongly recommended since roughly one in three flood insurance claims come from areas outside high-risk zones according to FEMA data.

How Base Flood Elevation Affects Your Premium

The FEMA Flood Map Service Center lets you search by address in seconds to find your zone and base flood elevation, which is the height water is expected to reach during a standard flood event. Base flood elevation matters because it directly influences your insurance premium under FEMA’s Risk Rating 2.0 system-a home sitting three feet above the base flood elevation pays less than one sitting at or below it, even if both are technically in the same zone.

Your address determines more than just whether you need coverage; it shapes your entire insurance cost structure.

Newly Mapped Zones and Premium Increases

If you live in a newly mapped high-risk zone, you may qualify for discounts on your first year of coverage, but those discounts phase out quickly and premiums can increase annually until reaching full risk rates. Homes in moderate-risk zones often get overlooked by owners who assume they’re safe, but Hurricane Helene in September 2024 paid out significant NFIP claims, with many losses occurring outside traditional flood zones.

Factors Beyond the Map

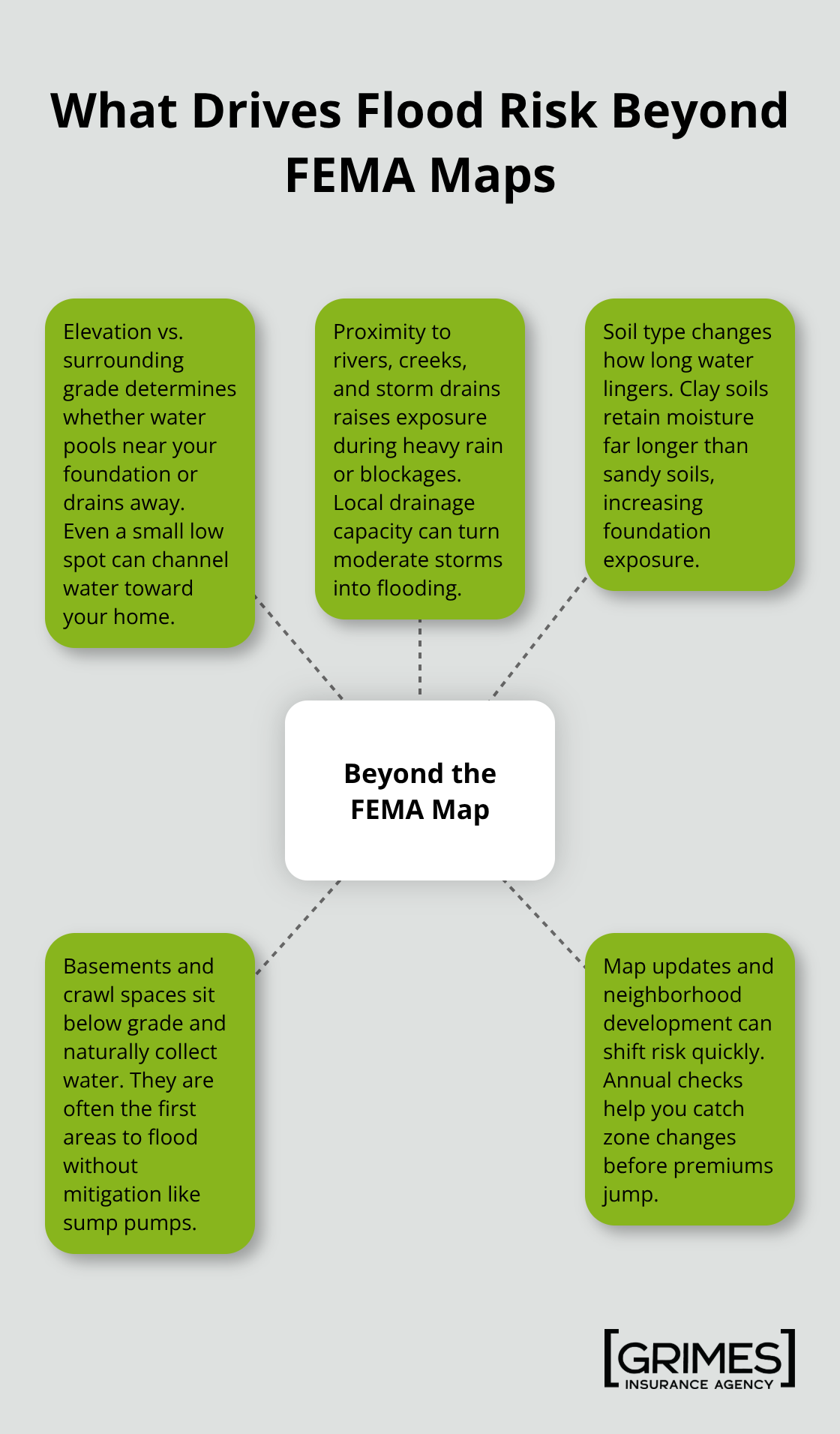

Elevation relative to surrounding grade, proximity to rivers or storm drains, soil type, and whether your home has a basement all factor into actual flood risk beyond what the map alone shows. Checking your flood map annually is critical because FEMA updates designations as development, drainage improvements, or climate patterns shift the hazard landscape. If your zone changes to higher risk, you need to know immediately so you can adjust coverage before new premiums take effect. The difference between checking your flood zone today versus next year could mean thousands of dollars in coverage gaps or unexpected premium jumps that catch you unprepared. Once you understand your zone and elevation, the next step involves evaluating your home’s specific vulnerabilities beyond what FEMA maps reveal.

What Makes Your Home Vulnerable to Flooding Beyond the FEMA Map

How Water Actually Moves Across Your Property

Your FEMA flood zone tells you the statistical risk, but it does not tell you how water actually moves across your specific property. Elevation relative to the surrounding grade, not elevation above sea level, determines whether water pools in your yard or drains away. Walk your property after a heavy rain and observe where water collects-that low spot near your foundation is a liability. If water sits within ten feet of your home, you need serious drainage work before worrying about insurance alone.

Drainage Systems That Protect Your Foundation

Check your gutters and downspouts right now; they should direct water at least five feet away from your foundation, not dump it against your house. Yard grading should slope away from your foundation at roughly five percent grade, which means dropping one foot in elevation for every twenty feet of horizontal distance. If your yard slopes toward your home instead of away, you are essentially inviting water inside during heavy rainfall. Inspect nearby storm drains to confirm they are not clogged, because a blocked drain system transforms moderate rain into standing water that threatens your foundation. Soil type matters too-clay soil holds water far longer than sandy soil, so a clay-heavy yard will retain moisture and increase foundation exposure even days after rain stops.

Basements and Crawl Spaces: Your Biggest Exposure

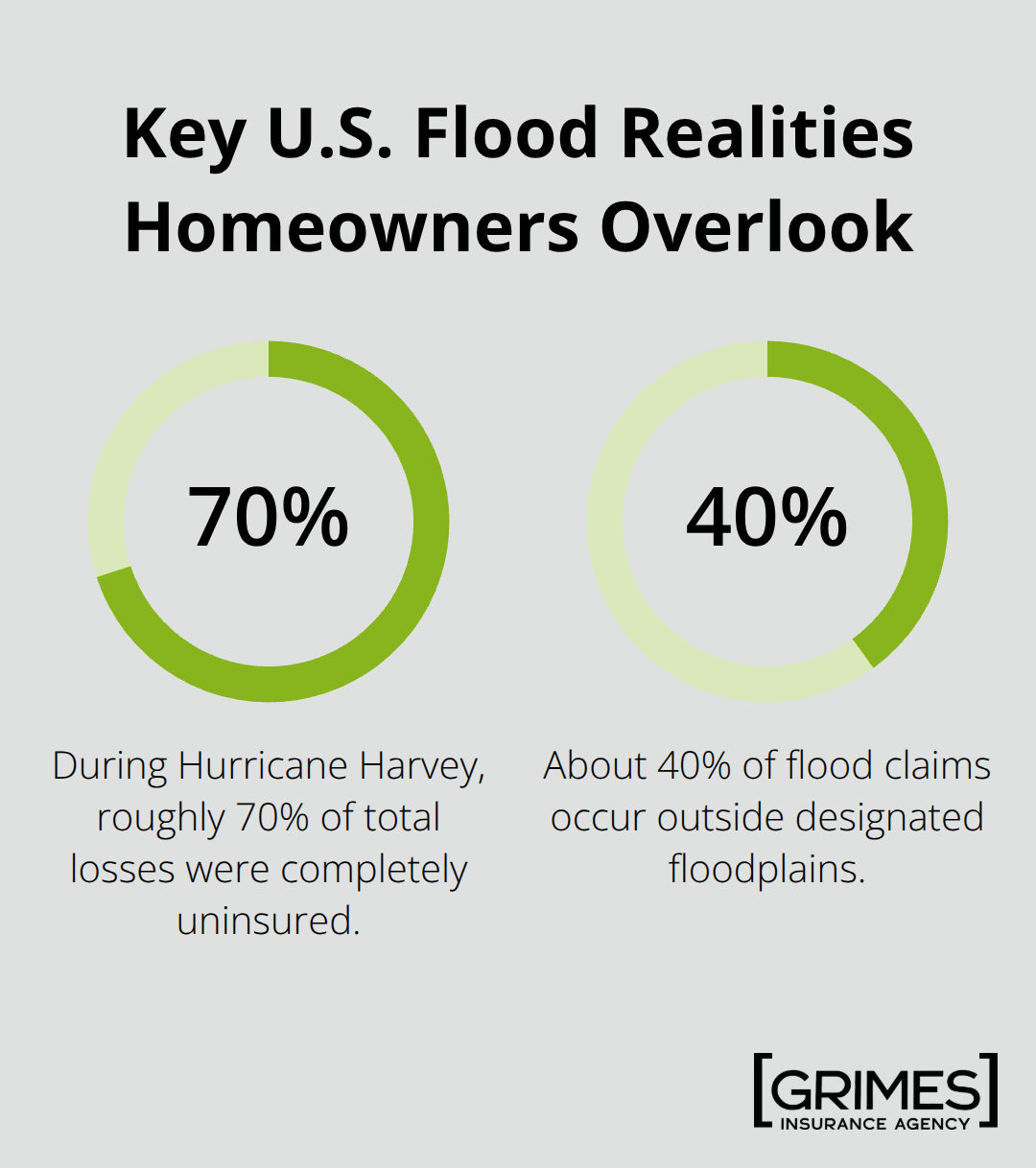

Historical flood data reveals what the future likely holds. The FEMA Historical Flood Data tool and services like FloodFactor show exactly which properties in your area have flooded before and how often. Properties that flooded once will flood again during similar weather events unless you install permanent mitigation. About 40% of flood claims occur outside designated floodplains, which means basements and crawl spaces are your biggest vulnerability because they sit below grade and collect water naturally. Homes built on slabs avoid this problem entirely.

Critical Systems and Permanent Mitigation

If you have a basement or crawlspace, a sump pump is not optional; it is mandatory protection that costs under two thousand dollars installed and prevents tens of thousands in damage. Seal foundation cracks with waterproof sealants immediately, as water finds every gap. Elevate HVAC units, electrical panels, and water heaters above the base flood elevation shown on your FEMA map-if the map says water reaches eight feet, your critical systems need to be at nine feet or higher. Contact a licensed contractor to assess your specific vulnerabilities and create a mitigation plan tailored to your property’s topography and exposure. Once you understand your home’s physical vulnerabilities, you can determine what insurance coverage actually protects you against the financial impact of a flood event.

Getting Adequate Flood Insurance Coverage

Your homeowners policy stops cold when water enters your home, which is why flood insurance exists as a separate purchase. Standard homeowners policies explicitly exclude flood damage, meaning a ten-thousand-dollar basement flood leaves you responsible for every penny of repair costs, demolition, and replacement. This gap between what people assume they’re covered for and what they actually own creates financial catastrophe across America. In 2017, Hurricane Harvey caused an estimated 125 to 190 billion dollars in losses, with roughly 70 percent of those losses completely uninsured according to industry analysis. That statistic repeats itself after every major flood event because homeowners either didn’t purchase flood insurance or underestimated their property’s replacement cost.

Why Standard Homeowners Insurance Fails You

Water damage from flooding sits outside every standard homeowners policy. Your insurer will cover a burst pipe inside your home but not water that enters from outside during a flood event. This distinction matters enormously when a heavy rainfall or storm surge saturates your foundation. The financial impact hits hard-a flooded basement requires removing drywall, flooring, insulation, and potentially studs if water damage reaches high enough. Reconstruction costs in most American markets exceed 150 to 200 dollars per square foot, meaning a 2,000-square-foot home would cost 300,000 to 400,000 dollars to fully rebuild.

Understanding NFIP Coverage Limits and Gaps

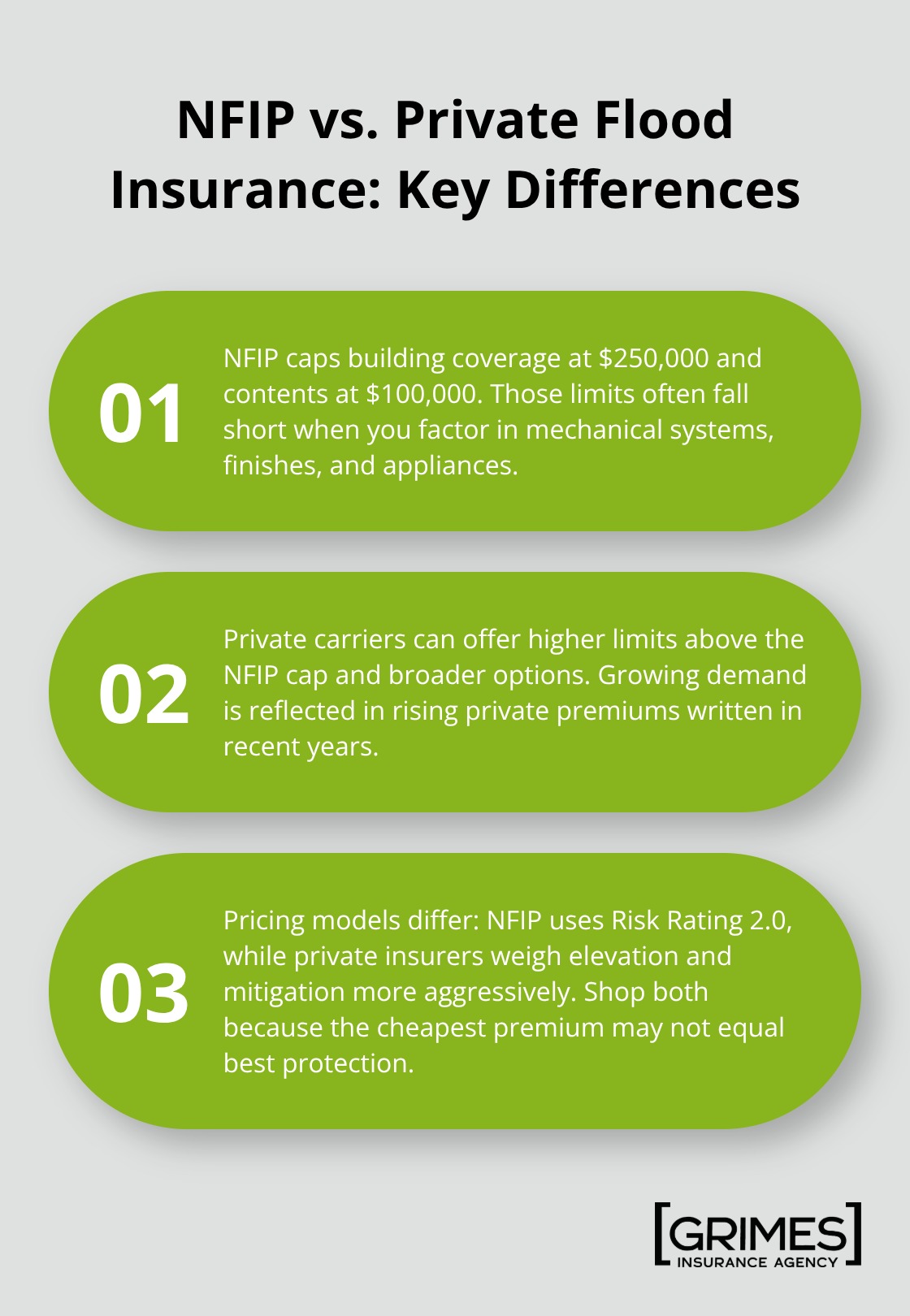

The National Flood Insurance Program, administered by FEMA, covers up to 250,000 dollars for building damage and 100,000 dollars for personal property. This sounds adequate until you calculate actual replacement costs. The NFIP’s 250,000-dollar building limit covers the shell but leaves you short on mechanical systems, appliances, flooring, and finishes.

Private flood insurance fills this gap, with carriers like AXA, Assurant, and Liberty Mutual offering coverage limits above the NFIP cap. Private premiums written for residential flood insurance reached 730 million dollars in 2024, up from 471 million in 2017, reflecting growing demand from homeowners recognizing NFIP limits as insufficient.

Calculating Your True Replacement Cost

Calculate your actual replacement cost by multiplying your home’s square footage by local reconstruction rates, then add ten to fifteen percent for site-specific factors like soil conditions or difficult access. If that total exceeds 250,000 dollars, you need adequate flood insurance coverage layered above your NFIP policy. The cost difference matters less than the coverage difference, and most homeowners can afford both policies for under 2,500 dollars annually depending on risk zone and elevation.

Comparing NFIP and Private Flood Insurance Options

NFIP pricing now uses Risk Rating 2.0, which considers your specific elevation relative to base flood elevation, the type of flood risk you face, and your home’s construction type. Private carriers often underwrite more aggressively on elevation and mitigation measures, meaning homes with sump pumps, elevated systems, or proper drainage might qualify for lower private rates than NFIP. Contact an insurance agent to quote both options because the lowest price isn’t always the best protection, and NFIP policies cannot be cancelled unilaterally like private policies can.

Final Thoughts

Check your FEMA flood zone using the Flood Map Service Center, evaluate your property’s drainage and elevation relative to surrounding grade, and calculate your actual replacement cost to complete your flood risk assessment for home insurance. Historical flood data in your area reveals patterns that FEMA maps alone cannot show, and properties that flooded once will flood again unless you install permanent mitigation like sump pumps, foundation sealing, or elevated critical systems. Confirm that your flood coverage limit matches your actual replacement cost, not just the NFIP’s standard 250,000-dollar building cap, because private flood insurance fills the gap and costs far less than the financial devastation of underinsurance.

Check whether your gutters direct water away from your foundation, your yard slopes away from your home, and nearby storm drains function properly. These drainage improvements often cost less than a year of flood insurance premiums but prevent water from entering your home in the first place. Your flood zone determines whether your lender mandates coverage, but your home’s elevation, basement exposure, and drainage systems determine whether you will actually experience a flood loss.

We at Grimes Insurance Agency have spent over 75 years helping homeowners in Lubbock and across Texas understand their actual flood exposure and find adequate coverage. Our independent agency accesses multiple carriers, meaning we can compare NFIP and private flood insurance options to match your specific risk profile and budget. Contact us to review your flood risk assessment and ensure your coverage protects what matters most.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation