Affordable Home Insurance Tips for 2026: How to Save Without Sacrificing Coverage

Home insurance doesn’t have to drain your budget. We at Grimes Insurance Agency help homeowners find affordable home insurance tips for 2026 that actually work without leaving you underprotected.

The right strategy combines smart discounts, strategic deductible choices, and coverage that matches your real needs. This guide shows you exactly how to cut costs while keeping the protection your home deserves.

What Determines Your Home Insurance Rate

Insurance companies calculate your premium based on concrete property and personal data that directly predicts claim likelihood. Your home’s location is the single biggest driver of cost. A house in Colorado faces wildfire risk and hail exposure that dramatically increases premiums compared to a similar home in Kansas. According to Matic’s 2025 Predictions report, Colorado, Texas, and Georgia experienced steeper premium increases due to climate exposure and regulatory factors. Your home’s age and construction matter enormously too. A house built in the last ten years typically costs less to insure than a 1970s home with outdated electrical systems and plumbing. Insurance companies know older homes file more claims for water damage and electrical fires, so they price accordingly. Your roof’s age receives heavy scrutiny because it serves as your home’s first line of defense against weather damage. If your roof passes fifteen years old, expect higher premiums or outright denial from some carriers.

How Property Details Shape Your Quote

Home value directly correlates to your dwelling coverage limit, which sets your baseline premium. A $500,000 home costs more to insure than a $250,000 home because the replacement cost is higher. But here’s what most homeowners miss: you don’t insure your home’s market value, you insure its rebuild cost. Those are different numbers. Your rebuild cost excludes land value and includes only the expense to reconstruct the structure from the ground up. Insurance companies increasingly use property-level risk factors instead of assumptions. This means they check your electrical system’s age, your plumbing type, whether you have a monitored security system, and even your roof material. Matic’s 2025 Predictions report shows pricing will increasingly reflect actual property conditions rather than assumptions. If you upgrade to impact-resistant windows or install a new roof, your premium should drop once you notify your insurer. This is actionable: document any home improvements and contact your insurer immediately after completion to capture available discounts.

Your Claims History and Credit Impact

Your CLUE report, maintained by LexisNexis, tracks every insurance claim you filed for the past seven years. One water damage claim can stay on your record and affect your ability to obtain coverage elsewhere. This creates a real dilemma: filing a small claim might cost you more in future premium increases than the claim payout itself. Your credit score also affects your premium significantly. People with poor credit pay substantially more for homeowners insurance because insurers view credit as a predictor of claim behavior. Some states restrict this practice-California, Maryland, and Massachusetts don’t allow or restrict credit-based insurance scoring-but most states permit it. If your credit falls below 650, improving it will lower your insurance costs more than almost any other action you can take.

Why Location and Risk Assessment Matter Most

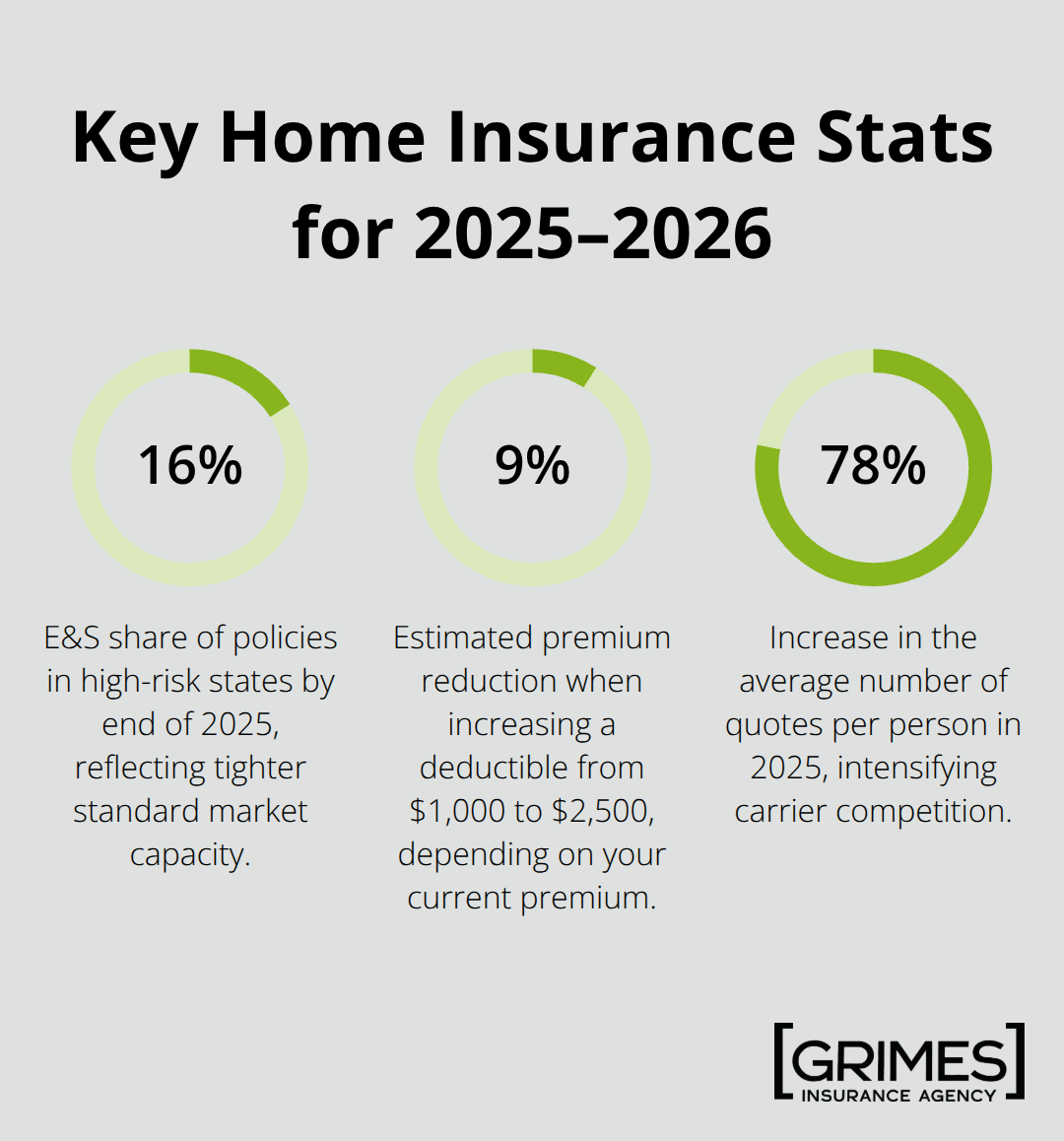

Geographic location determines not just your premium, but your access to coverage itself. In high-risk states like California, Florida, and Texas, Excess & Surplus (E&S) products accounted for 16% of policies by the end of 2025, up from under 2% in 2023. This shift means standard coverage becomes harder to find in certain ZIP codes, forcing homeowners into more expensive alternatives. Insurance companies assess your specific property’s risk profile using satellite imagery, drone assessments, and AI-driven inspections.

They’re no longer relying on neighborhood averages-they’re pricing based on your actual roof condition, your proximity to flood zones, and your home’s specific vulnerabilities. Climate-related insurance risks in high-risk states are expected to increase this year in states affected by severe weather. This shift toward precision pricing rewards homeowners who maintain their properties and punishes those who neglect them. Understanding these factors helps you identify which improvements will actually lower your costs. The next section shows you exactly which discounts and strategic choices will reduce your premium without leaving you exposed.

Cut Your Home Insurance Costs Without Cutting Coverage

Bundling your home and auto policies with the same insurer delivers the fastest path to meaningful savings. When you combine policies, insurers reward loyalty because they reduce their acquisition costs and administrative overhead. The math is straightforward: if your home premium runs $1,200 annually and your auto premium sits at $1,000, bundling might save you $440 across both policies in year one. Top carriers for bundling include USAA, Travelers, Progressive, Auto-Owners, and Nationwide, each offering multi-policy discounts that compound when you add additional coverage lines. Request quotes from at least three bundling-focused carriers and compare the total package price, not individual line items. Some insurers advertise aggressive home discounts but charge more on auto, so the bundled total tells the real story.

Strategic Deductible Selection

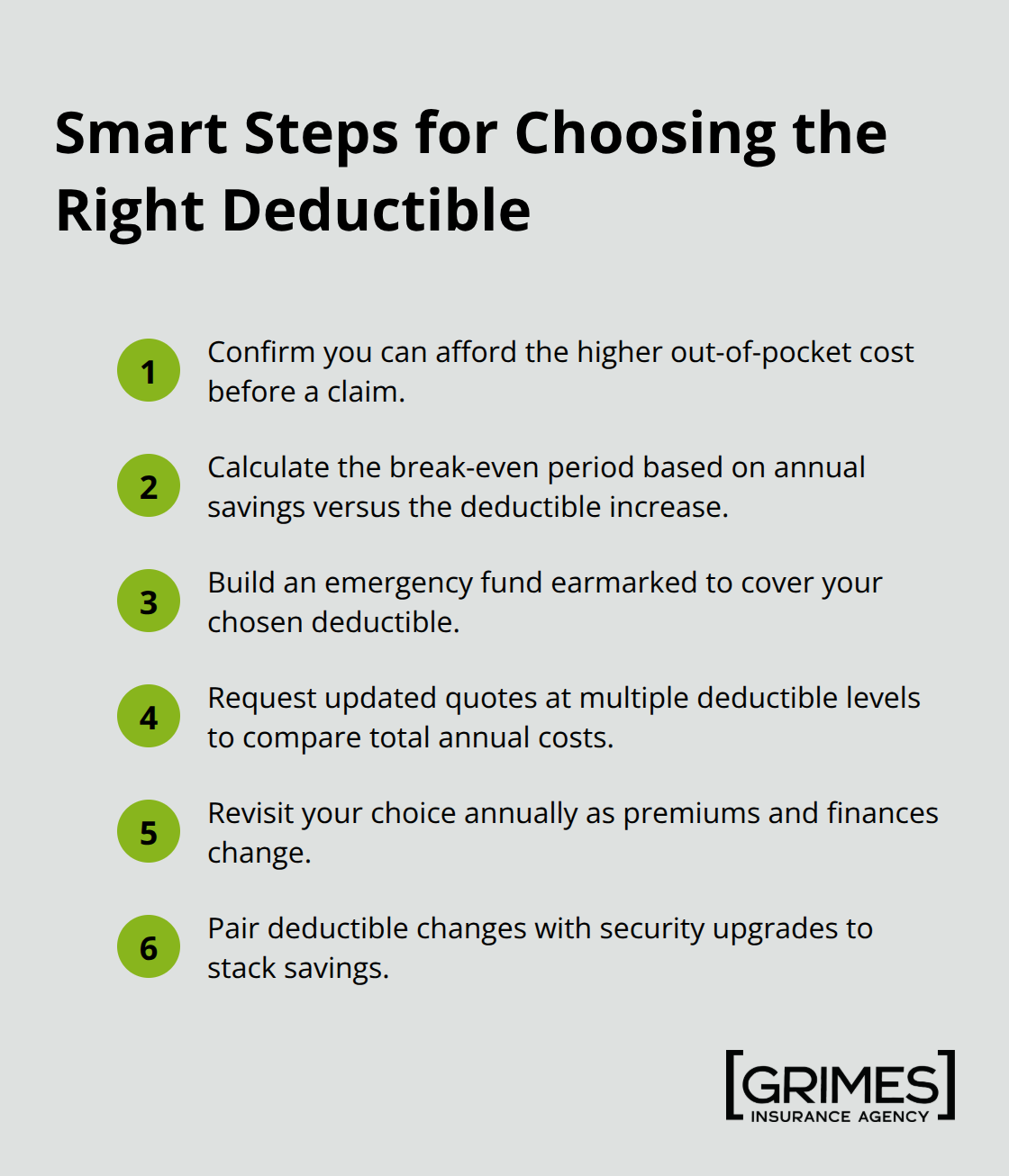

Your deductible choice directly controls your monthly premium without requiring home improvements or waiting for discounts to accumulate. Increasing your deductible from $1,000 to $2,500 reduces annual premiums by approximately 9% according to industry data, which translates to roughly $100 to $150 savings annually depending on your current premium. The critical decision point is whether you can actually afford to pay that higher deductible if a claim occurs. Calculate your break-even period before committing: if the annual savings are $120 and your deductible increases by $1,500, you break even after 12.5 years, making the move worthwhile only if you plan to keep the policy long-term.

Build an emergency savings fund to cover your chosen deductible and remove the risk that a claim forces you into financial hardship. Security upgrades like monitored alarm systems, smoke detectors, and water sensors trigger tangible discounts because they reduce claim frequency and severity. Carriers reward these improvements because they prevent losses rather than simply managing them after the fact.

Home Maintenance as Premium Reduction

Your roof age remains the single most scrutinized element in your premium calculation because weather damage represents the largest loss category for insurers. Replace an aging roof before it reaches 20 years old and you often qualify for a roof-replacement discount that offsets a meaningful portion of the replacement cost. Update your electrical system from outdated knob-and-tube or aluminum wiring to modern copper wiring and you reduce fire risk substantially, typically lowering premiums by 5% to 15% depending on the carrier. Plumbing upgrades from galvanized steel to copper or PEX plastic reduce water damage claims, another major loss driver. Contact your insurer before undertaking any major improvements and ask specifically which upgrades qualify for discounts. After completion, notify your insurer with photos or contractor documentation so the discount applies immediately to your next renewal. This proactive communication prevents the frustrating scenario where you invest $8,000 in a new roof but receive no premium reduction because the insurer wasn’t informed.

Loyalty, Credit, and Lesser-Known Discounts

Your insurance company wants to keep you as a customer because retention costs far less than acquiring new ones. Loyalty discounts grow over time, with some carriers offering increasing credits after three, five, and ten years of continuous coverage. A paid-in-full discount typically saves 5% to 10% annually if you pay your entire premium upfront rather than monthly installments, essentially rewarding you for giving the insurer your money earlier. Paperless billing discounts might seem small at 5% or less, but combined with loyalty and paid-in-full discounts, these stack into meaningful reductions. Your credit score directly influences your premium in most states, and improving it from 620 to 750 can lower your insurance costs more than almost any other single action. If your credit currently sits below 650, prioritize paying down debt and correcting reporting errors on your credit report because the premium savings will compound year after year. Occupation-based discounts exist for teachers, engineers, and firefighters at select carriers, so mention your profession when requesting quotes. Non-smoker discounts apply when all household residents avoid tobacco, and some carriers offer senior discounts for homeowners aged 65 or older. Ask your agent about every available discount beyond the standard ones, check carrier websites directly, and request rate matches if another insurer quotes lower. Shopping around yields substantially more options than in previous years, making comparison shopping more valuable than ever.

Essential Coverage You Cannot Afford to Skimp On

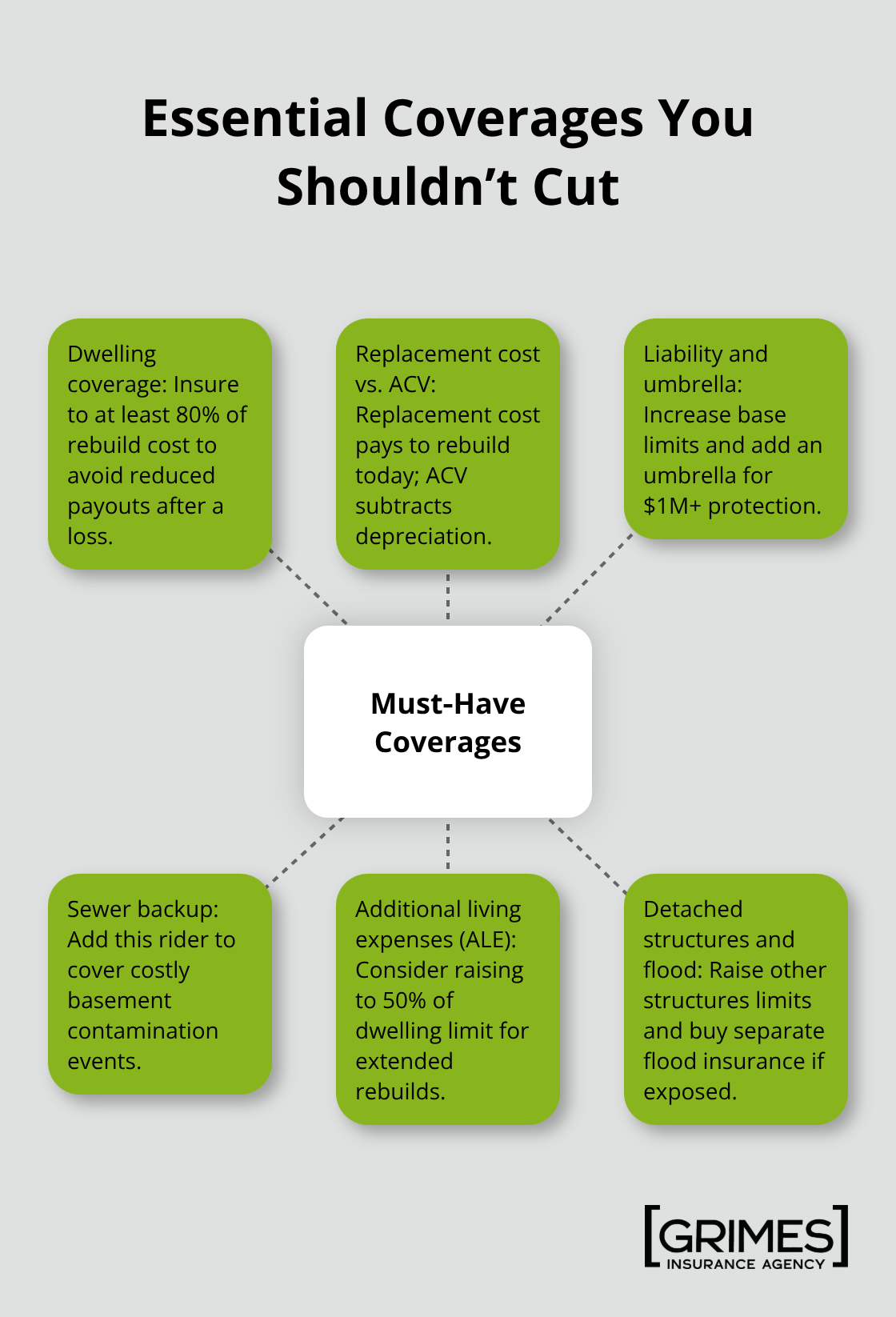

Your dwelling coverage protects the structure itself-the walls, roof, foundation, electrical systems, plumbing, and built-in appliances. This is non-negotiable coverage, yet many homeowners under-insure it to lower premiums. The 80% rule means an insurance company will pay the replacement cost of damage to a home as long as the owner has purchased coverage equal to at least 80% of its rebuild cost. Ignore this rule and insurers will reduce your payout proportionally after a total loss, leaving you thousands of dollars short. Your rebuild cost differs from your home’s market value because it excludes land and accounts only for construction expenses. A $400,000 home might have a $320,000 rebuild cost if your land represents significant value. Request your insurer calculate your rebuild cost using current construction prices in your area, not estimates from five years ago. Construction costs rose sharply through 2024 and continue climbing, meaning your old estimate likely undervalues your home.

Replacement Cost vs. Actual Cash Value

Actual cash value policies pay depreciated amounts for damaged items, while replacement cost coverage pays what it costs to rebuild today without depreciation penalties. Amica’s Platinum Choice policy includes replacement cost coverage as standard, illustrating how carrier-specific features dramatically affect your protection level. The difference matters enormously when a loss occurs. A ten-year-old roof that costs $12,000 to replace might receive only $4,000 under actual cash value coverage after depreciation. Replacement cost coverage pays the full $12,000, protecting you from bearing the depreciation burden yourself.

Liability Protection and Umbrella Policies

Personal liability coverage shields you when someone is injured on your property and sues for medical bills or lost wages. Standard policies include $100,000 to $300,000 in liability protection, but this proves inadequate if a serious injury occurs. A slip-and-fall accident resulting in permanent disability can generate lawsuits exceeding $500,000, leaving you personally liable for amounts above your policy limit. Umbrella policies extend your liability coverage to $1 million or more for relatively modest additional cost, typically $150 to $300 annually. Anyone with meaningful assets should purchase umbrella coverage because a liability judgment can attach to your bank accounts, investment accounts, and future wages.

Water Damage and Living Expense Coverage

Water damage claims represent the second-largest loss category in homeowners insurance after weather damage, yet standard policies exclude sewer backups, which occur increasingly as aging municipal systems fail nationwide. Adding sewer backup coverage costs $25 to $75 annually but protects against claims that easily exceed $25,000 when raw sewage floods your basement. Additional living expenses coverage pays your hotel, meals, and other costs if a covered loss forces you from your home during repairs. This coverage typically amounts to 20% to 30% of your dwelling coverage limit, which may prove insufficient if repairs take months.

A fire destroying your kitchen and primary bedroom might require six months of contractor work, generating $15,000 to $25,000 in living expenses that basic coverage won’t fully cover. Request that your insurer increase your additional living expenses coverage to at least 50% of your dwelling limit if you live in an area prone to extended reconstruction timelines.

Detached Structures and Flood Insurance

Other structures coverage protects detached buildings like sheds, garages, and pools, typically capped at 10% of your dwelling coverage. If your detached garage contains tools and equipment worth $8,000 but your other structures limit sits at $5,000, that gap means your own loss. Adjust this coverage upward if you have a substantial detached structure or valuable equipment stored outside your primary home. Standard homeowners policies exclude floods entirely, making separate flood insurance essential in any flood-prone area. The National Flood Insurance Program administers federal flood policies, but private flood insurers like Neptune Flood now offer alternatives that sometimes cost less with better coverage terms. Your mortgage lender requires flood insurance if your home sits in a high-risk flood zone, but you should purchase it voluntarily if you’re in moderate-risk areas because one flood claim can total your home’s value.

Final Thoughts

Your home insurance strategy for 2026 requires action on two fronts: finding the lowest possible premium and confirming you have adequate protection. Start by reviewing your current policy against your home’s current rebuild cost, not the estimate from three years ago, since construction costs continue rising and underinsuring by even 10% means insurers will reduce your claim payout proportionally after a total loss. Contact your insurer and ask about every discount you might qualify for beyond the standard ones-loyalty discounts grow over time, paid-in-full discounts save 5% to 10%, and paperless billing adds another small reduction that stacks into meaningful savings when combined with bundling or strategic deductible increases.

Shopping around every one to two years remains your most powerful cost-reduction tool because the average number of quotes per person rose 78% in 2025, meaning more carriers compete for your business than ever before. An independent insurance agent can compare multiple carriers simultaneously rather than forcing you to request quotes individually from each company, and we at Grimes Insurance Agency specialize in accessing multiple carriers to find the best protection and pricing for your specific situation. With over 75 years serving the Lubbock, Texas community, Grimes Insurance Agency understands how local risk factors affect your premium and which carriers offer the strongest coverage for your needs.

The cheapest premium isn’t always the best choice when a policy that saves you $300 annually but excludes sewer backup coverage leaves you exposed to a $25,000 loss. Balance affordability with adequate protection by confirming your dwelling coverage meets the 80% rule, your liability limits match your assets, and your deductibles are amounts you can actually afford to pay. Contact us to review your current policy and explore affordable home insurance tips for 2026 that work for your specific situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation