Lubbock Home Insurance Options: Local Coverage Made Easy

Finding the right Lubbock home insurance options shouldn’t feel overwhelming. Whether you’re a first-time homebuyer or looking to switch providers, understanding your coverage choices is the first step toward protecting what matters most.

At Grimes Insurance Agency, we’ve spent 75 years helping Lubbock residents navigate their insurance needs with clarity and confidence. This guide walks you through the coverage types available, why working with a local agent makes a real difference, and the mistakes to avoid when selecting your policy.

What Your Home Insurance Actually Covers in Lubbock

Dwelling Coverage: The Foundation of Your Protection

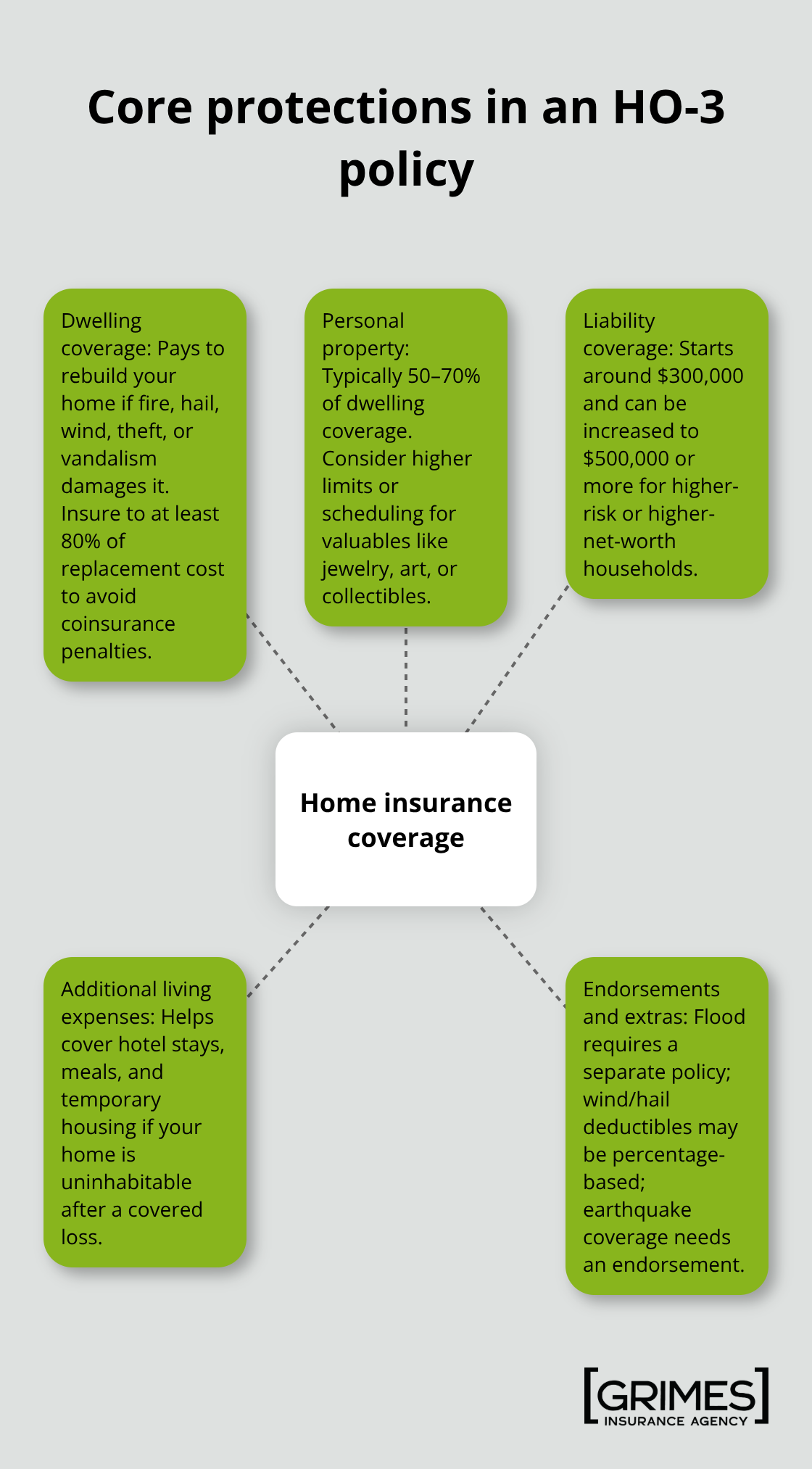

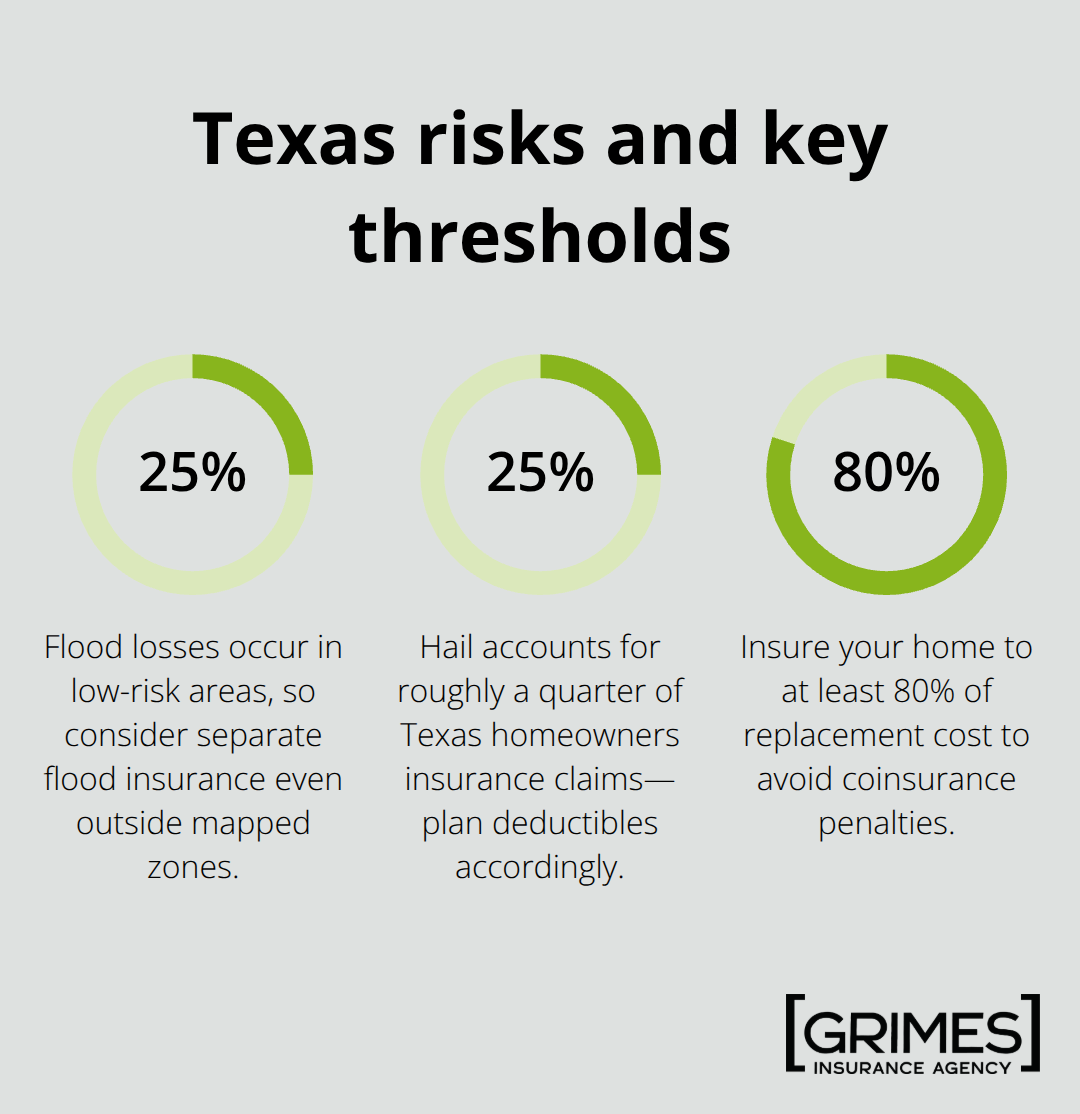

Your standard homeowners policy in Lubbock is almost certainly an HO-3 form, which covers four distinct areas of protection. The dwelling coverage pays to rebuild your house if fire, hail, wind, theft, or vandalism damages or destroys it. Most Lubbock homes need to be insured for at least 80 percent of their replacement cost to avoid coinsurance penalties. If your home costs $450,000 to rebuild but you only insure it for $300,000, the insurance company will reduce your payout proportionally on any claim.

This is why an accurate replacement cost estimate matters far more than your home’s market value. A local contractor can assess your rebuild costs, and you should add 10 to 15 percent for inflation since replacement costs rise yearly. This approach protects you from the financial shock of underinsurance when you need it most.

Personal Property and Liability: Protecting Your Belongings and Your Finances

Personal property coverage protects your belongings inside the home, typically capped at 50–70% of your dwelling coverage. For a $400,000 dwelling, this means roughly $200,000 to $280,000 for furniture, electronics, clothing, and other items. Most three-bedroom homes contain $100,000 to $150,000 in possessions, so you’ll likely need higher limits or scheduled endorsements for valuable items like jewelry, art, or collectibles.

Choose replacement cost coverage over actual cash value for personal property, even though it costs about 10 to 15 percent more annually. Actual cash value subtracts depreciation, leaving you with far less when you need to replace items.

Liability coverage protects you legally if someone is injured on your property or you accidentally damage someone else’s property. Standard liability starts at $300,000, but higher net worth or risk situations warrant $500,000 or more. Additional living expenses cover hotel stays, meals, and temporary housing if your home becomes uninhabitable after a covered loss.

Texas-Specific Risks That Require Extra Attention

Water damage from burst pipes or roof leaks is covered under standard policies, but flood damage from rising water or heavy rain requires separate flood insurance through the National Flood Insurance Program or a private carrier. About 25 percent of flood losses occur in low-risk areas, so don’t assume you’re protected just because your home isn’t in a mapped flood zone.

Wind and hail damage is common in Lubbock, with hail accounting for roughly 25 percent of Texas homeowners claims. Some insurers offer wind and hail deductibles as a percentage of your dwelling coverage instead of a flat dollar amount, meaning a 2 percent deductible on $150,000 coverage equals $3,000 out-of-pocket. Installing a Class 4 impact-resistant roof can lower your premiums through discounts offered by most carriers. Earthquake coverage requires a separate endorsement and isn’t included in standard policies.

Comparing Coverage and Costs Across Carriers

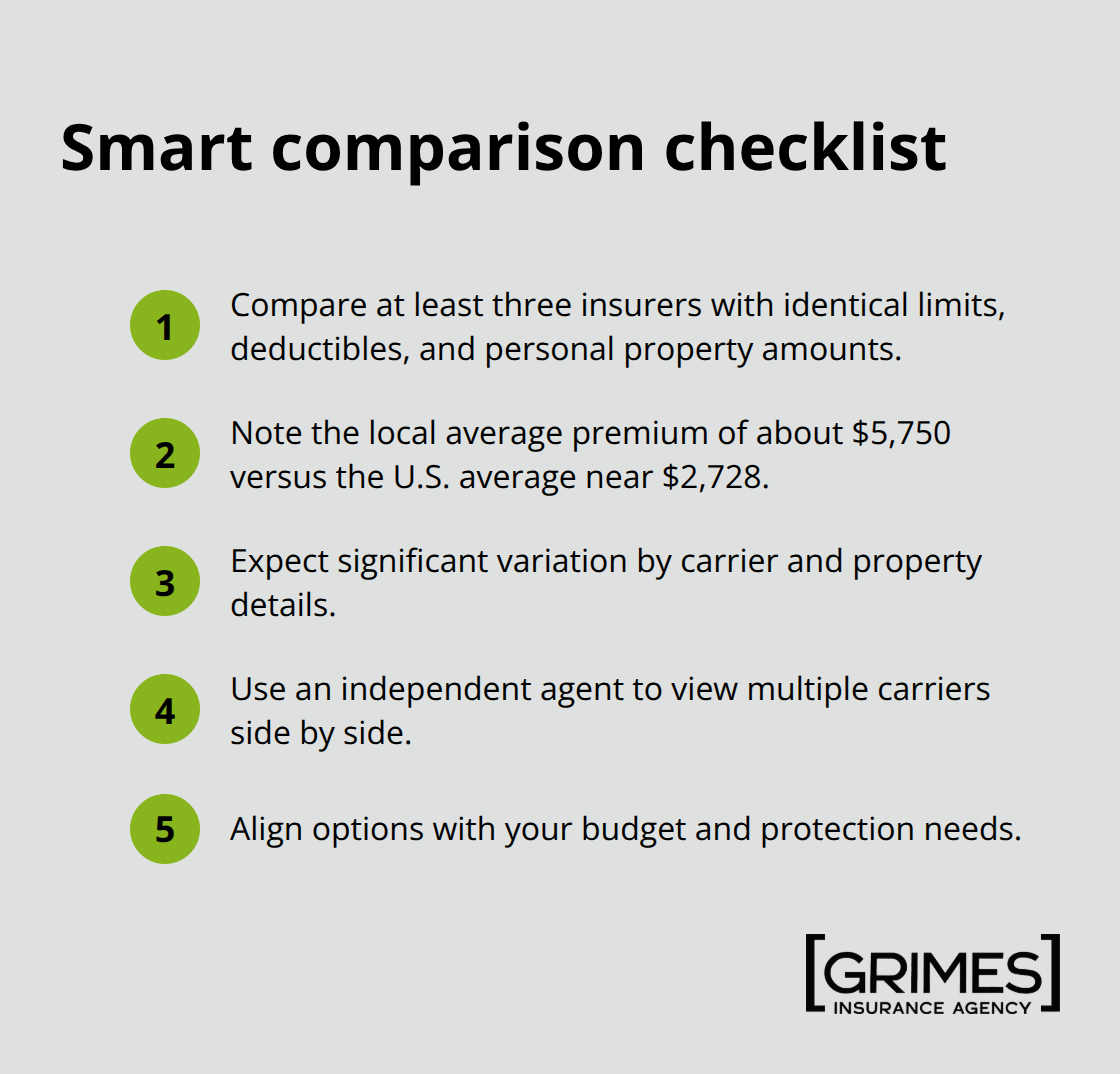

When you shop for coverage, compare at least three insurers with identical dwelling limits, deductibles, and personal property amounts to see real price differences. The average homeowners insurance cost in Lubbock is about $5,750 per year, well above the U.S. average of roughly $2,728, according to Quadrant Information Services data. However, rates vary significantly by carrier and your specific property details. An independent agent who represents multiple carriers can streamline this comparison process and help you identify which options align with your budget and protection needs.

Why a Local Agent Beats Shopping Solo

Multiple Carriers Mean Real Price Comparisons

Shopping for home insurance on your own means comparing websites one by one, each with different coverage definitions, exclusions, and pricing structures. An independent agent in Lubbock cuts through this friction by accessing quotes from multiple carriers simultaneously, showing you real price differences side by side. When you call a captive agent working for State Farm or Farmers, they can only quote their employer. An independent agent shows you what Mercury Insurance, Chubb, USAA, Nationwide, and others charge for identical coverage, revealing savings you’d never find alone. According to research, independent agents help customers access better pricing through multiple carrier comparisons-a meaningful difference on your annual premium when Lubbock’s average sits around $5,750 per year.

Local Knowledge Shapes Better Coverage Decisions

Local knowledge matters more than most homeowners realize. A Lubbock agent understands which carriers price favorably for hail damage claims, which ones offer the best wind deductible structures, and which companies handle flood endorsements efficiently through the National Flood Insurance Program. We at Grimes Insurance Agency know the specific weather patterns affecting properties in our area, the local construction standards that impact rebuild costs, and which endorsements matter most for your neighborhood. Our 75 years serving West Texans means recommendations grounded in actual claim history and local risk data, not generic national advice.

Unlocking Savings Tied to Your Situation

A local agent identifies savings opportunities tied to your specific circumstances. We know which carriers offer the eco-friendly discounts Farmers provides or the military benefits USAA extends, helping you access savings you wouldn’t discover on your own. An agent who has worked in Lubbock for decades also understands the claims process from the customer’s perspective, having seen how different insurers handle storm damage or water damage disputes in our community. This experience translates directly into better policy choices upfront, reducing disputes or coverage gaps when you actually file a claim.

The Advantage of Representation Across Multiple Companies

Grimes Insurance Agency represents many national carriers, which means you’re not locked into one company’s limited options or pricing. This carrier-agnostic approach gives you access to the full range of coverage options available in the market. Your policy reflects local weather risks and regional factors that matter in West Texas, not a one-size-fits-all template designed for national averages.

The mistakes Lubbock homeowners make often stem from incomplete information or coverage gaps that slip through when shopping alone. Understanding these pitfalls helps you avoid costly errors before they happen.

Mistakes That Cost Lubbock Homeowners Money

Underinsuring Your Home’s True Replacement Cost

Most Lubbock homeowners make one critical error that undermines their entire policy: they insure their home based on what they paid for it, not what it costs to rebuild. Understanding the difference between replacement cost value and market value is essential when purchasing home insurance. A home worth $300,000 on the market might cost $450,000 to reconstruct after a total loss because rebuild costs include labor, materials, and local factors that market value ignores. If you insure that $450,000 home for only $300,000, the Insurance Information Institute warns you’ll face coinsurance penalties on every claim. The insurance company calculates payouts proportionally, meaning a $50,000 fire damage claim gets reduced because you failed to insure at least 80 percent of replacement cost. This isn’t a penalty for being slightly under-it’s a mathematical reduction that compounds quickly. Lubbock’s average home insurance premium of $5,750 annually seems high until you realize the alternative: filing a $100,000 claim and receiving $66,000 because you underinsured by 20 percent.

Get a contractor’s estimate for your specific property and add 10 to 15 percent for inflation. This single step prevents the most expensive mistake homeowners make.

Overlooking Coverage Gaps and Exclusions

The second mistake involves accepting standard coverage limits without examining what they actually exclude. Your HO-3 policy caps personal property at 50 to 70 percent of dwelling coverage, meaning a $400,000 home gets only $200,000 to $280,000 for everything inside it. If you own jewelry, art, electronics, or collectibles worth more than this amount, you need scheduled personal property endorsements with current appraisals-not assumptions about what your insurer will cover.

Flood damage does not exist in standard policies; about 25 percent of flood claims occur in low-risk areas, so ignoring flood coverage because you’re not in a mapped zone is dangerous. Wind and hail deductibles often run as percentages rather than flat amounts, meaning a 2 percent deductible on $150,000 dwelling coverage equals $3,000 out-of-pocket, not $1,000. Many Lubbock homeowners discover these gaps only after filing claims.

Skipping Annual Policy Reviews

The third mistake is treating your policy as a set-it-and-forget-it document. Home values change, you make renovations, you acquire valuable items, and carrier pricing shifts annually. A policy that protected you adequately three years ago may leave you exposed today. Annual reviews-especially after home improvements or major purchases-take one hour and prevent thousands in losses. Market conditions and your circumstances evolve constantly, and your coverage should reflect those changes.

Final Thoughts

Your home represents your largest financial asset, and protecting it demands more than accepting the first online quote you find. Dwelling coverage must reflect your actual rebuild cost, not your home’s market value, and personal property limits need to account for everything inside your home with scheduled endorsements for high-value items. Flood insurance, wind deductibles, and liability limits should align with your specific situation and local risks rather than generic national standards.

We at Grimes Insurance Agency understand that Lubbock home insurance options must address the unique weather challenges and local market conditions that shape your decisions. Our 75 years serving West Texans means we’ve witnessed how hail, wind, and water damage actually affect properties in our community, and we represent multiple national carriers to give you access to real price comparisons and coverage options you won’t find by shopping alone. This carrier-agnostic approach means your policy reflects local risks and your personal circumstances, not a one-size-fits-all template.

A quote takes minutes, and the savings often exceed what you’d find independently. Whether you’re a first-time buyer, switching providers, or simply reviewing your current coverage, contact Grimes Insurance Agency to walk through your options with clarity and confidence.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation