Is Minimum Car Insurance Coverage Ever Enough?

Are you carrying minimum car insurance because it is genuinely the right choice for your situation or because it is the cheapest option available?

And if you caused a serious accident tomorrow, do you know whether your minimum coverage actually protects you from the financial consequences?

Every week, our Grimes Insurance Agency team works with West Texas drivers who discover, often after a claim, that their minimum coverage left them personally responsible for thousands of dollars they were not prepared to pay.

The gap between what minimum coverage promises and what it actually delivers is one of the most expensive surprises.

We have been helping drivers navigate it since 1948, and we see the same pattern repeatedly: minimum coverage made sense at the time, and then circumstances changed.

In this article, you will learn:

- What Texas minimum auto coverage actually includes

- When it may be sufficient

- When it clearly is not

- How to evaluate which option makes sense for your specific situation.

What Texas Minimum Car Insurance Actually Covers

Liability coverage pays for damage and injuries you cause to other people. It does not cover your own vehicle, injuries, or any damage to your property. Anything above those limits becomes your personal financial responsibility.

Texas requires all drivers to carry minimum liability coverage (commonly known as 30/60/25). This includes at least $30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $25,000 for property damage. Anything above those limits becomes your personal financial responsibility.

Texas minimum limits are a legal floor, meaning they have not changed. They were set decades ago and have not kept pace with the actual cost of vehicles, medical care, or legal judgments.

For instance, a newer vehicle can easily exceed the $25,000 property damage limit. A single emergency room visit can exceed the $30,000 per-person bodily injury limit. When the damages exceed your limits, you are personally liable for the difference.

If you want to understand exactly what separates minimum liability from full protection, read Liability vs Full Coverage Car Insurance Explained for a direct side-by-side comparison.

When Minimum Auto Coverage May Be Sufficient

Minimum coverage is a legitimate choice in specific, narrow circumstances. Being honest about whether those circumstances apply to your situation is the right way to evaluate it. Let’s look at a few:

You own your vehicle outright, and its value is low.

If your car is worth $3,000 to $4,000 with no loan, the financial loss from a total loss would be manageable. Paying for collision and comprehensive on a low-value vehicle may cost more annually than the coverage is worth.

You have sufficient personal assets to cover a gap.

If your savings or assets can cover a liability judgment that exceeds your policy limits, having minimum coverage is less risky.

Your driving is limited and low-risk.

A retired driver covering a few thousand miles annually in a low-traffic area faces different exposure than a daily commuter in heavy traffic.

You are in a temporary financial situation.

Sometimes, minimum coverage is a short-term decision while finances stabilize. It is better than driving uninsured.

When Minimum Car Insurance Coverage Is Not Enough

For most Texas drivers, minimum coverage creates real exposure that is worth understanding before a claim makes it visible. Let’s review a few examples:

You drive a financed or leased vehicle.

Your lender requires full coverage for financed or leased vehicles for the life of the loan or lease. Minimum coverage violates your loan agreement and can trigger force-placed insurance, which is more expensive and covers only what the lender needs.

You have assets worth protecting.

If you own a home, have retirement savings, or carry significant assets, a liability judgment above your policy limits can attach to those assets. Minimum liability limits of $30,000 per person provide thin protection against a serious injury claim.

You live in West Texas.

Lubbock and the surrounding Texas Panhandle face severe hail seasons. A single hail event can cause $3,000 to $8,000 in damage to a vehicle. Minimum coverage does not include comprehensive coverage, meaning every hailstorm is a personal expense rather than a covered claim.

You share the road with uninsured drivers.

Texas has one of the highest rates of uninsured drivers in the country. If one hits you, minimum coverage does not protect your vehicle or injuries. Uninsured motorist coverage is a separate add-on that minimum policies do not include.

Learn more about uninsured motorist coverage and how it can protect you in an accident:

The Cost of Being Underinsured

A serious at-fault accident involving injuries and significant vehicle damage can exceed Texas’s minimum limits by tens of thousands of dollars. When that happens, you become personally responsible for the difference. Depending on the circumstances, that liability can put your savings, assets, and future income at risk until the debt is satisfied.

The annual premium difference between minimum liability coverage and full protection is often $600 to $1,200. While minimum coverage may save money upfront, a single uncovered claim can exceed those savings many times over.

For many Texas drivers, the biggest drawback of minimum coverage is that the financial risk often outweighs the premium savings.

How to Choose the Right Car Insurance Coverage Level

Drivers often fall into one of the two categories: carrying minimum coverage where it genuinely makes sense, or carrying minimum coverage because it offers the lowest premium, but exposes them to greater financial risk.

The right coverage level is different for everyone and depends on various factors. Consider your vehicle’s value, loan status, assets, driving patterns, and where you live.

Opting for full coverage might be more expensive, but so is being caught unprepared.

Before your next renewal, ask yourself:

- Is my vehicle financed?

- Could I afford to replace my vehicle out of pocket?

- Could my assets absorb a judgment above my limits?

Most drivers who discover they are underinsured wish they had asked those questions before a claim was settled for them.

So, is minimum car insurance ever enough?

For some Texas drivers, yes. If you own an older vehicle outright, have limited exposure, and understand the financial risks involved, minimum coverage may be a reasonable choice.

For many drivers, however, minimum coverage leaves important gaps that can become expensive after an accident, hailstorm, or other unexpected event. The key is understanding not just what Texas requires, but what level of protection makes sense for your specific situation.

Grimes Insurance Agency has been helping West Texas drivers find the right coverage level since 1948. Whether minimum coverage is enough or you need broader protection, our team can help you understand your options and make an informed choice.

Before requesting a quote, read about the Insurance Quote Process at Grimes Insurance Agency so you know exactly what to expect.

Frequently Asked Questions

What are the minimum car insurance requirements in Texas?

Texas requires liability coverage of $30,000 per person for bodily injury, $60,000 per accident, and $25,000 for property damage, written as 30/60/25. This is the legal minimum to drive in Texas.

Does minimum coverage pay for damage to my own vehicle?

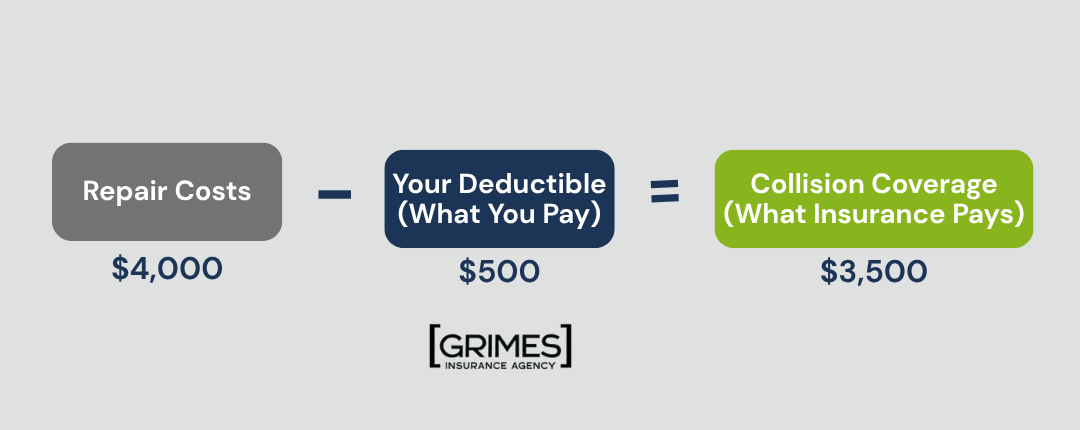

No. Minimum liability coverage only pays for damage and injuries you cause to others. Damage to your own vehicle requires collision and comprehensive coverage, which are not part of minimum liability.

Can I carry minimum coverage on a financed vehicle?

No. Lenders require full coverage, including collision and comprehensive, for the life of the loan or lease.

How much does full coverage cost compared to minimum coverage in Texas?

Minimum liability coverage in Texas averages $700 to $900 annually. Full coverage averages $2,200 to $2,800 annually, depending on your vehicle, driving record, and location.

What happens if the damages in an accident exceed my minimum limits?

You are personally liable for the difference. A judgment above your policy limits can attach to your bank accounts and future earnings until satisfied.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.