How Does Grimes Insurance Agency Handle Claims?

A storm damages your roof. Someone hits your car. A pipe bursts in your home. Suddenly, you’re dealing with adjusters, policy language, timelines, and questions you weren’t expecting.

For many people, filing a claim is an uncommon experience. Most policyholders go years without experiencing a loss that requires one.

When a claim does become necessary, uncertainty about the process can make an already stressful situation feel even more overwhelming.

At Grimes Insurance Agency, we have helped West Texas policyholders through claims since 1948. We understand the insurance providers we work with and where clients often need support during the insurance claim process.

By the end of this article, you will understand exactly how the claims process works, what Grimes Insurance Agency does at each step, and how we help you make sense of it all.

What Happens When You File With Grimes Insurance Agency?

Grimes Insurance Agency is an independent insurance agency and not a carrier. The insurance company (Progressive or Allstate, for example) pays the claim. What we do is guide you through the insurance claims process, review your coverage before the adjuster arrives, and help you understand your options if questions come up during the claim.

Without an agent, policyholders (that’s you) handle coverage questions and communication with the insurance carrier themselves.

But with Grimes, you have someone who reviews your coverage before the adjuster arrives and provides support and transparency through each stage of the claim. Think of us as the bridge between you and your carrier.

Read more about the benefits of working with an independent insurance agent to understand how Grimes Insurance is different from individual carriers.

Let’s walk through the five steps of how a claim works with Grimes Insurance Agency.

Step One: Report the Incident to Grimes Insurance Agency

The first step is to contact our agency as soon as possible after a loss.

The sooner you report a loss, the easier it is to document the damage and establish a clear timeline.

Hail damage from a storm? House flooded from a burst pipe? Fender bender in the parking lot?

Whatever the incident, reaching out is simple. Call us at 806-762-0544.

When you call, have the following ready if possible:

- The date and location of the incident

- A description of what happened

- Any photos or documentation you have gathered

- Your policy number

Step Two: Grimes Insurance Agency Reviews Your Coverage

Once you report the incident, we review your policy to confirm what is covered and your deductible.

This step matters more than most people realize. Policy language is specific and has many moving parts. Sometimes, what looks like a straightforward claim might actually have rules or limits that affect how much money you get paid.

For example, hail damage does not always mean a full replacement. Deductibles, exclusions, and policy limits may affect what is ultimately paid.

We review those details before the adjuster’s visit so you understand how coverage may affect the claim outcome.

Step Three: The Carrier Assigns an Adjuster

After the claim is filed with the carrier, an adjuster is assigned to evaluate the loss. The adjuster’s job is to assess the damage and determine what the carrier owes under the policy terms.

For property claims, like home, commercial, or auto, the adjuster typically inspects the damage in person. For smaller claims, a virtual or photo-based assessment may be used.

The adjuster works on behalf of the insurance carrier. Their job is to evaluate the loss based on the policy and the damage they observe. Your job is to ensure the loss is fully documented and nothing is overlooked.

Document everything before any repairs or replacements. Save photos, videos, estimates, receipts, repair invoices, and notes about when the damage happened.

The more information you have, the easier it is to show the full extent of the loss.

We help explain what the adjuster is reviewing and how your policy may apply. It can be difficult to understand what happens during a review and why certain details are important. Our job is to help you make sense of what the adjuster is looking at, why it matters, and the role your policy plays in what they find.

Step Four: Settlement and Resolution

Once the adjuster completes their assessment, the carrier issues a settlement offer. This is the amount they are willing to pay based on their evaluation of the loss and your policy terms.

The First Settlement Offer is Not Always Final

If an offer does not reflect the damage or policy coverage, you do not have to accept it immediately. Sometimes, settlement disagreements come down to missing information, repair estimates, documentation, or differences in how damage was evaluated.

In those situations, we help you review the settlement, explain options, and find ways to increase the settlement if possible.

What to Do While the Claim Is in Process

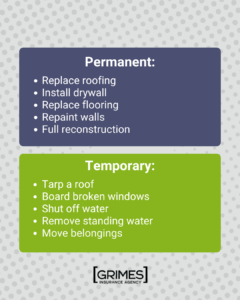

Do not make permanent repairs before the adjuster inspects the damage. Making permanent repairs before inspection can complicate the assessment. If temporary repairs are necessary to prevent further loss (boarding broken windows, tarping a damaged roof, etc.), ensure you document and keep all receipts and related records. Those records may become important later in the claims process.

Keep records of every communication with the carrier, such as the date, the name of the person you spoke with, and what was discussed. That record matters if a dispute arises later.

Call Grimes Insurance Agency at any time if the process feels unclear. We are here to help provide support while your claim moves forward.

What You Know Now and What to Do Next

Filing a claim is easier when you understand the process and know where to turn for support.

Now you know how the claims process works, where Grimes Insurance Agency fits in, and what support looks like when a claim is filed.

If you need to file a claim now, contact our office, and we will help you understand the next steps. If you are reviewing coverage before something happens, now is the time to ensure your policy is prepared to perform when you need it most.

If you aren’t currently working with us and want to know if your coverage is built to last (before you ever need to file a claim), request a quote at Grimes Insurance Agency. With access to many insurance carriers, we can help you find the perfect insurance fit, and even save you money in the process.

Frequently Asked Questions

Do I call Grimes Insurance Agency or the carrier to file a claim?

Call Grimes Insurance Agency first. We will review your coverage and guide you through the reporting process with the carrier. You can reach us at 806-762-0544 during business hours.

How long does the claims process take?

It depends on the complexity of the loss. Simple auto or property claims like a fender bender can be resolved in a few days, while intermediate claims like major roof damage can take a few weeks. Larger commercial claims or disputed settlements can take longer.

What if I need to file a claim outside of business hours?

Most carriers have 24-hour claims lines. Contact your carrier directly for after-hours emergencies, and call our office the next business day so we can get involved.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.