Commercial Property Insurance Factors: What Affects Your Policy

Your commercial property insurance premium isn’t random. It’s calculated based on specific factors that insurers evaluate to determine your risk level.

At Grimes Insurance Agency, we’ve helped countless business owners understand what drives their costs. Building characteristics, location risks, and your business operations all play a role in shaping your final premium.

How Your Building’s Physical Characteristics Shape Your Insurance Cost

Construction Materials and Building Age

The physical structure of your property is one of the first things insurers examine when calculating your premium. A newer brick building with modern safety systems will cost significantly less to insure than an older wood-frame structure with outdated electrical wiring. Construction materials matter more than most business owners realize. Masonry, brick, concrete, and steel structures typically cost less to insure than wood-frame or vinyl-siding buildings because they resist fire and weather damage more effectively.

If your building was constructed before 1980, insurers often view it as higher risk due to potential issues like outdated plumbing, electrical systems, and roofing materials. The age of specific systems matters too. A roof that’s 20 years old signals trouble ahead, while a 5-year-old roof can actually lower your premiums. Square footage directly impacts your premium as well. A 5,000-square-foot warehouse will cost more to insure than a 2,000-square-foot office because there’s simply more property at risk.

Fire Protection and Safety Features

Fire protection features are your strongest lever for reducing costs. If your building sits within 1,000 feet of a fire station and near a fire hydrant, you’ll see lower premiums compared to rural locations. Installing sprinkler systems and fire alarms isn’t just about safety-it directly reduces what you pay. These loss-prevention measures signal lower risk to underwriters and demonstrate your commitment to protecting your property.

Claims History and Maintenance Practices

Your claims history over the past five years will follow you. File one claim, and expect your renewal premium to increase. File multiple claims, and some insurers may decline to renew your policy altogether. This is why maintenance and prevention matter. Regular inspections of your roof, electrical systems, and plumbing catch problems before they become expensive claims.

Security and Property Condition

Security features also influence your rate. Properties in high-crime areas with monitored alarm systems and surveillance cameras pay less than those without. The condition of your building’s exterior and interior-whether it’s well-maintained or showing signs of neglect-tells underwriters whether you manage risk responsibly or invite problems. Your property’s appearance and upkeep directly affect how insurers assess your overall risk profile.

Beyond your building itself, where your property sits matters just as much. Geographic location introduces a whole new set of risk factors that can shift your premium significantly.

Where Your Location Shapes What You Pay

Your zip code carries more weight in your insurance premium than most business owners realize. Geographic location determines exposure to natural disasters, crime patterns, and emergency services availability. These factors directly influence how much risk insurers assume when covering your property.

Natural Disaster Risk and Regional Exposure

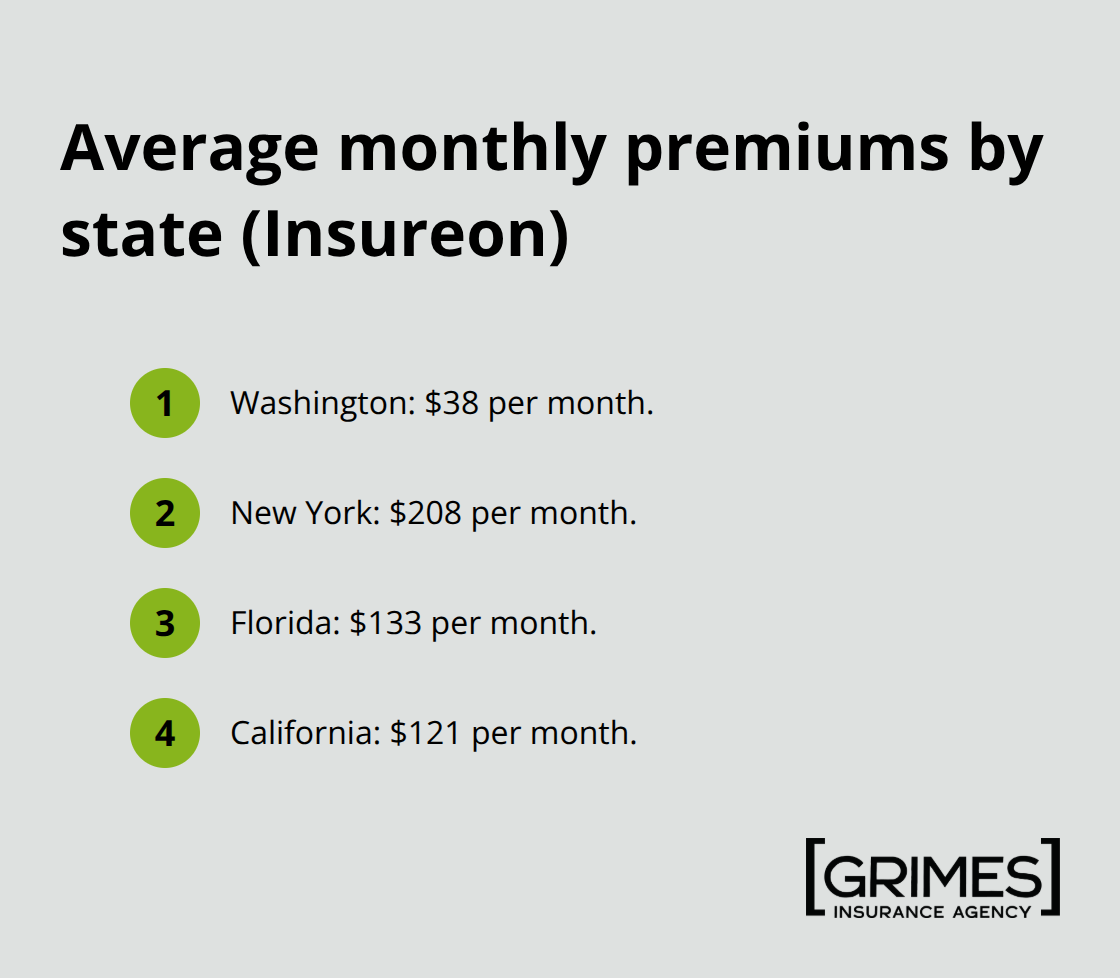

The difference between insuring a property in Washington state versus New York illustrates this reality. According to Insureon data, commercial property insurance averages about $38 per month in Washington but jumps to $208 per month in New York. Florida averages $133 per month while California sits at $121 per month.

These aren’t minor variations-your location can multiply your annual costs by five or more.

Natural disaster exposure drives much of this variation. In 2025, insured weather-related catastrophe losses in the U.S. reached $103.1 billion according to the Insurance Information Institute. Properties in hurricane-prone coastal areas, tornado corridors, and wildfire zones face steeper premiums because insurers know the damage risk is genuine and substantial. High-risk zones like coastal Louisiana demonstrate why location matters so significantly. If your business operates in a high-disaster zone, expect to pay more. Some areas face such concentrated risk that standard insurers pull back entirely, leaving you with limited options and higher costs through specialty carriers.

Crime Rates and Local Security Conditions

Crime rates and theft patterns in your neighborhood directly affect your premium. High-crime areas command higher rates because property loss and break-ins occur more frequently. Installing monitored alarm systems and surveillance cameras can offset some of this risk premium, but geography remains the underlying factor. Properties in safer neighborhoods with lower theft rates benefit from reduced premiums compared to those in high-crime zones.

Emergency Services and Fire Protection Access

Properties near fire stations and water sources benefit from lower premiums because firefighters respond faster and hydrants provide reliable water supply. If your property sits within 1,000 feet of a fire station, you have a tangible cost advantage. Rural locations far from emergency services face higher premiums because response times stretch longer and fire suppression becomes more difficult.

Building Codes and Local Regulations

Building construction codes and local regulations also influence your rate. Older structures in areas with strict modern building codes may require costly upgrades before insurers will cover them, or they’ll charge significantly more. Some jurisdictions have updated electrical codes, seismic requirements, or wind-resistance standards that older buildings don’t meet. Compliance costs get passed to you through higher premiums or coverage exclusions.

The combination of these geographic and environmental factors means two identical buildings in different locations can have dramatically different insurance costs. Your building’s location, age, and business type all influence what coverage you need and what you’ll pay for it. What happens inside your business operations, however, introduces another layer of complexity that insurers evaluate just as carefully.

How Your Business Type and Operations Drive Insurance Costs

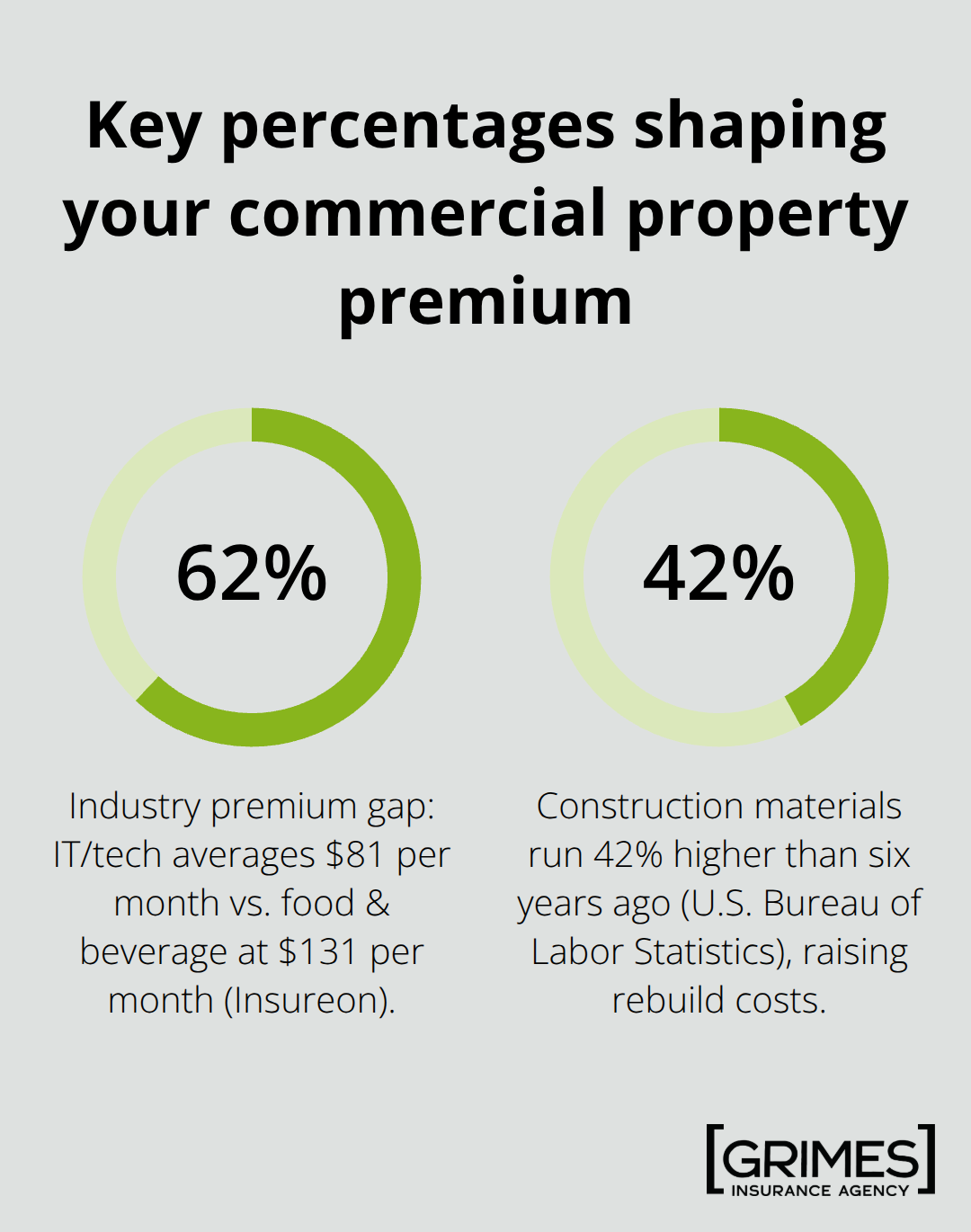

Your industry classification matters far more than most business owners realize. Insurance companies don’t treat all businesses the same, and the difference in premiums between industries can be staggering. According to Insureon data, IT and technology businesses average about $81 per month for commercial property coverage, while food and beverage operations average $131 per month. That’s a 62% difference for the same coverage level, driven entirely by industry risk.

Industry Risk and Claims Frequency

Restaurants face higher premiums because they generate frequent property claims through kitchen fires, equipment failures, and water damage from plumbing issues. A consulting firm with minimal physical assets and low fire risk pays substantially less. Your business type determines the baseline risk that insurers assign before they even evaluate your specific building or location. If you operate in construction, manufacturing, or hospitality, expect higher premiums than someone in professional services. The nature of your operations tells underwriters how often claims typically occur in your industry and how severe those claims tend to be.

Property Valuation and Inventory Levels

Revenue and inventory levels add another pricing layer that catches many business owners off guard. A retail store with $500,000 in inventory on hand at any given time needs significantly higher coverage limits than an office with minimal physical assets. Insurers calculate your replacement value based on what you actually have to replace if a total loss occurs. If your property valuation is too low, you face underinsurance that leaves gaps in your protection.

Construction costs have risen dramatically, with materials running about 42% higher than they were six years ago according to the U.S. Bureau of Labor Statistics. This means a building insured at $1 million five years ago might actually need $1.3 million in coverage today to fully rebuild at current costs. You must update your property valuations regularly to match current replacement costs, not historical purchase prices.

Occupancy Patterns and Employee Count

Employee count and occupancy patterns shift your premium significantly. A building with 50 employees working full-time creates more exposure to theft, accidents, and equipment wear than a small office with three people. Higher occupancy means more foot traffic, more potential for accidents, and greater demand on building systems. Properties with extended operating hours or high public access face steeper premiums than those with controlled access and limited occupancy.

Final Thoughts

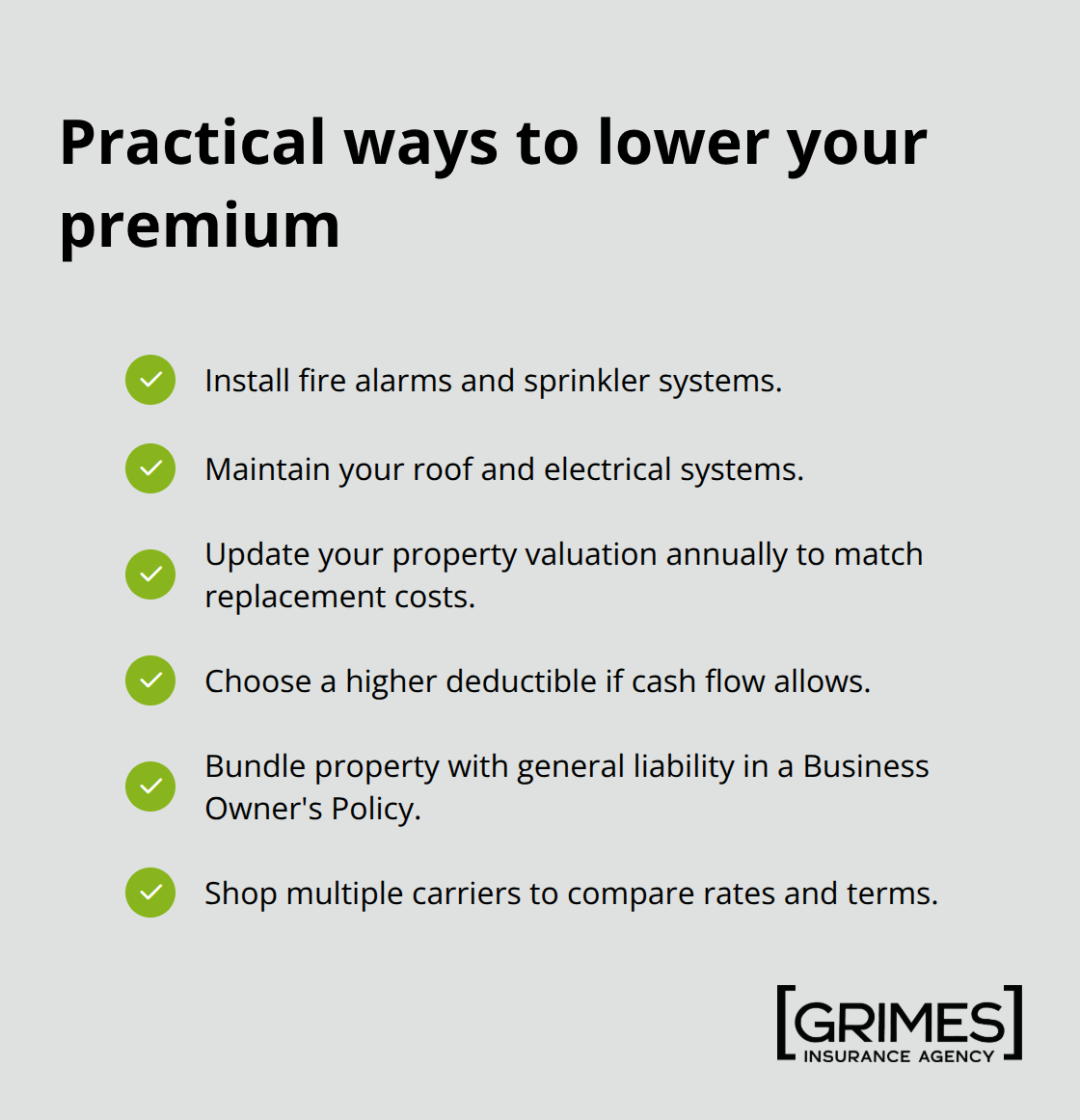

Your commercial property insurance factors determine what you pay, and many of these factors respond to your direct action. Install fire alarms and sprinkler systems, maintain your roof and electrical systems, update your property valuation annually to reflect current replacement costs (especially given that construction materials now run 42% higher than six years ago), and choose a higher deductible if your cash flow allows it. Bundling your commercial property coverage with general liability under a Business Owner’s Policy typically costs less than purchasing policies separately, and shopping around matters because underwriting standards vary significantly between carriers.

When comparing quotes, verify you’re evaluating identical coverage levels and limits, then check the insurer’s financial ratings and complaint history to gauge reliability beyond price alone. What one insurer declines another may approve at competitive rates, so don’t accept the first offer you receive. Your specific risk profile deserves a policy matched to your actual needs, not a generic solution that leaves gaps or wastes money on unnecessary coverage.

Contact Grimes Insurance Agency to discuss your commercial property insurance needs and receive an accurate quote tailored to your business. We work with multiple carriers to find the right coverage at the right price for your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation