Homeowners Insurance Basics: Your Simple Starter Guide

Homeowners insurance basics don’t have to be confusing. Most homeowners either buy too much coverage or too little, simply because they don’t understand what they’re actually paying for.

We at Grimes Insurance Agency help homeowners cut through the noise and find the right protection for their homes and families. This guide walks you through what’s covered, how to pick the right limits, and where you can actually save money.

What Your Homeowners Policy Actually Protects

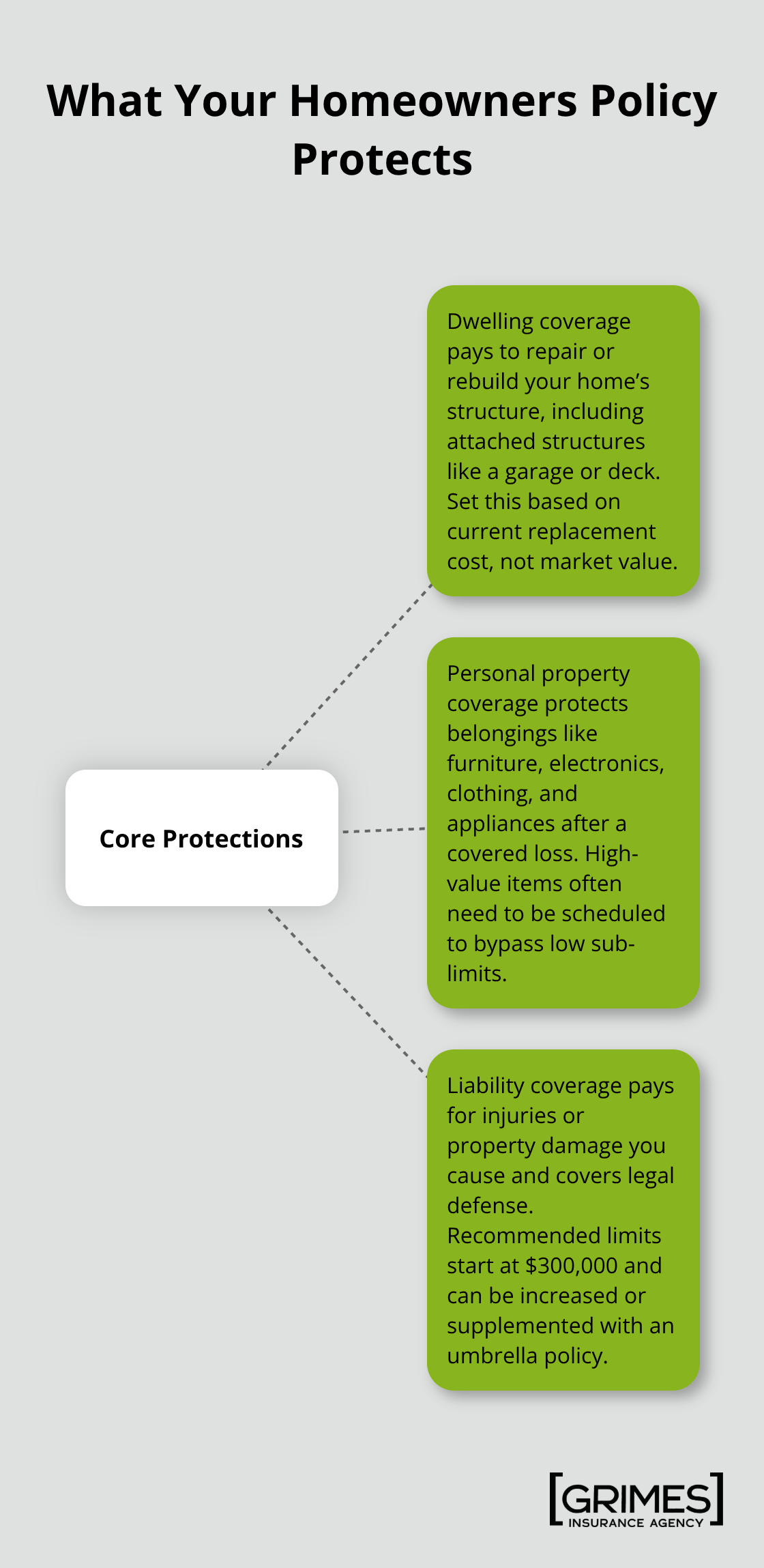

Dwelling Coverage: Protecting Your Home’s Structure

Your homeowners insurance policy covers three distinct areas, and most people misunderstand at least one of them. Dwelling coverage pays to repair or rebuild your home’s structure itself, including attached structures like a garage or deck. According to ValuePenguin, about 1 in 3 homeowners misunderstand key coverage components, which often leads to undervaluation of damages or claim denial when a loss occurs.

The dwelling coverage amount should reflect your home’s current replacement cost, not its market value. If you renovated your kitchen, added a new roof, or upgraded your HVAC system, your coverage limits may not account for those improvements, leaving you exposed if a fire or major damage happens.

Personal Property Coverage: Protecting Your Belongings

Personal property coverage is separate from dwelling coverage and protects your belongings-furniture, electronics, clothing, and appliances-if they’re stolen or destroyed by a covered disaster. This coverage typically maxes out at 50 to 70 percent of your dwelling coverage, which means if your home is insured for $300,000, your belongings might only be covered up to $150,000 to $210,000.

Expensive items like jewelry, artwork, or collectibles hit sub-limits, often capped at just $1,500 per item unless you add a scheduled personal property endorsement. This gap matters far more than most homeowners realize when they face a total loss.

Liability Coverage: Your Financial Protection Against Lawsuits

Liability coverage is where many homeowners make a critical mistake by keeping limits too low. The Insurance Information Institute recommends at least $300,000 in liability protection, yet many standard policies start at $100,000, which is inadequate for today’s litigation environment. This coverage pays if someone is injured on your property or if you accidentally damage someone else’s property, and it covers legal defense costs if you’re sued.

A neighbor’s child falls off your deck, a guest slips on your icy driveway, or your dog bites the mail carrier-liability coverage handles medical bills and legal expenses. Without adequate limits, a serious injury lawsuit could exhaust your coverage and expose your personal assets to judgment. Off-premises coverage extends liability protection worldwide, so you’re covered if your child accidentally breaks a window at a friend’s house or if you’re found responsible for injury to someone at a vacation rental.

Now that you understand what your policy covers, the next step is determining how much coverage you actually need.

How Much Coverage Do You Actually Need

Calculate Your Home’s True Replacement Cost

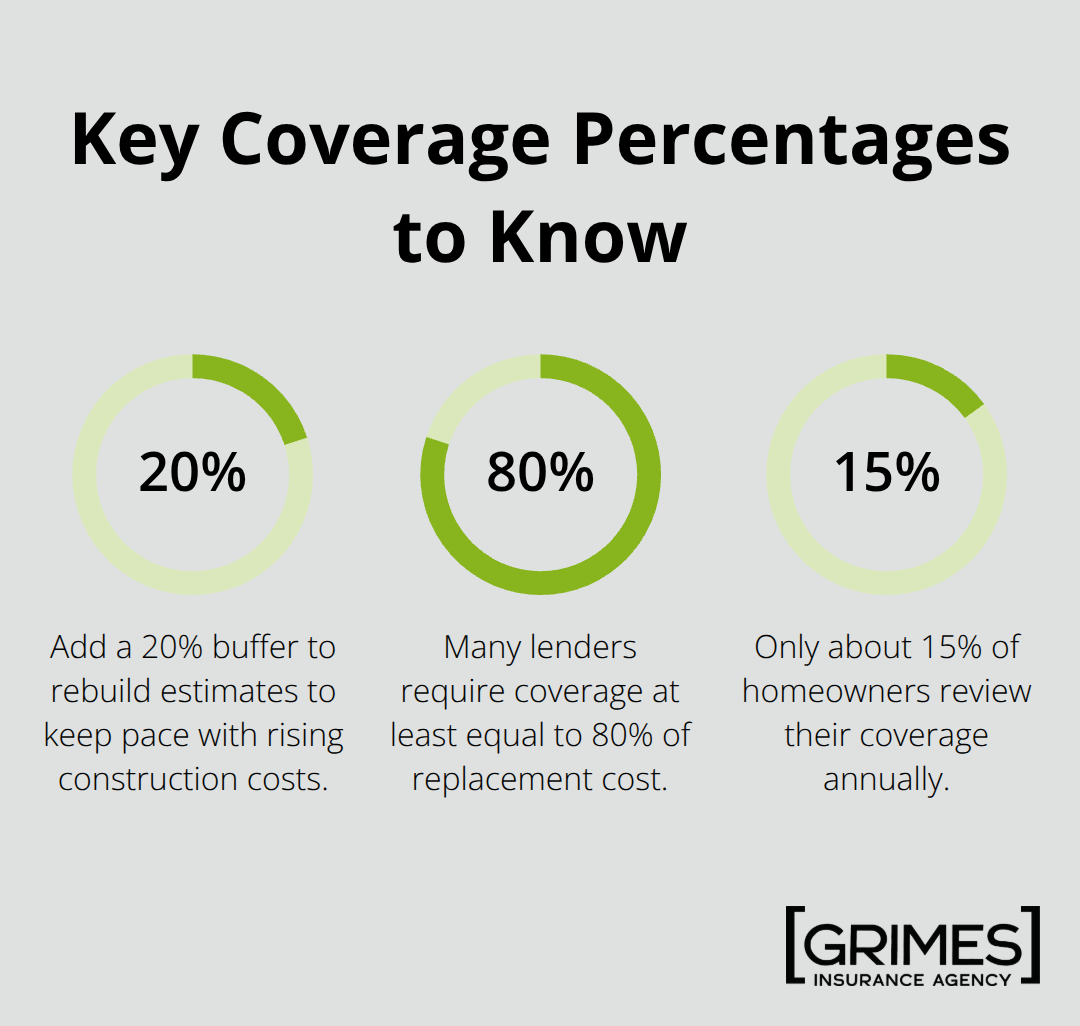

Picking coverage limits is where most homeowners get it wrong. You cannot use your home’s market value or what you paid for it fifteen years ago. The Insurance Information Institute recommends calculating replacement cost by multiplying your home’s square footage by average building costs per square foot in your area. In Texas, average construction costs run between $150 and $250 per square foot depending on your region and build quality, which means a 2,000-square-foot home could need $300,000 to $500,000 in dwelling coverage.

Get your home professionally appraised or contact three local contractors for rebuild estimates, then add 20 percent as a buffer because construction costs rise faster than inflation. Your mortgage lender requires you to carry coverage at least equal to 80 percent of your home’s replacement cost, but that minimum often leaves you dangerously underinsured if a total loss happens. ValuePenguin found that only about 15 percent of homeowners actually review their coverage annually, which means most people operate with limits that no longer match their home’s current replacement cost. If you renovated in the past five years, your coverage is almost certainly too low.

Inventory Your Personal Property and Set Realistic Limits

Personal property coverage needs its own calculation separate from dwelling limits. Walk through your home room by room and inventory what you own, then research replacement prices for furniture, electronics, appliances, and clothing using retailer websites or price comparison tools. The CFPB notes that cataloging belongings digitally and updating annually speeds claims and improves payouts significantly.

Your standard policy covers belongings at 50 to 70 percent of dwelling coverage, which creates a hard ceiling even if your actual belongings exceed that amount. High-value items like jewelry, art, or collectibles require scheduled personal property endorsements at their appraised replacement value, not the sub-limit cap. This gap matters far more than most homeowners realize when they face a total loss.

Set Liability Limits That Actually Protect Your Assets

Liability limits matter far more than most homeowners think because a single serious injury lawsuit can exceed your assets. The Insurance Information Institute recommends minimum $300,000 in liability coverage, and honestly, that should be your starting point, not your ending point. If you own a trampoline, have a pool, or live in a high-density neighborhood where children frequently cross your property, increase limits to $500,000 or $1,000,000.

An umbrella policy adds $1 million to $2 million in liability coverage for roughly $150 to $300 annually, making it one of the smartest purchases most homeowners never make. This extra layer protects your personal assets if a lawsuit exceeds your standard policy limits. Off-premises coverage extends liability protection worldwide, so you stay covered if your child accidentally breaks a window at a friend’s house or if you’re found responsible for injury to someone at a vacation rental.

With your coverage limits now set to match your actual risk and assets, the next step is finding ways to lower your premiums without sacrificing protection.

How to Actually Lower Your Premiums

Bundle Your Policies for Immediate Savings

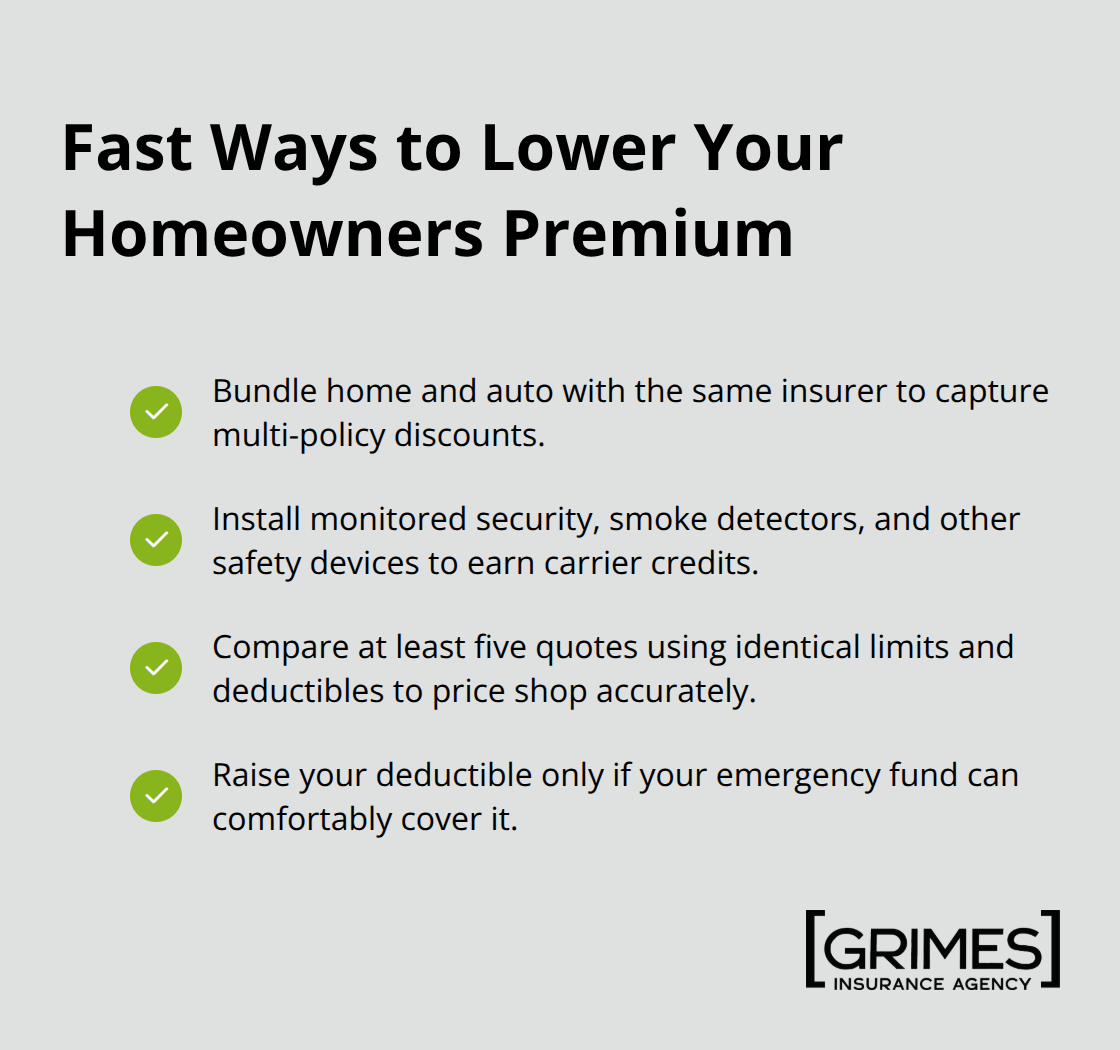

Bundle your policies with the same insurer, as getting coverage for multiple policies with the same insurer almost always garners a discount. Many homeowners assume their current insurer offers the best bundle rate, but that assumption costs them hundreds annually. You need to get quotes for bundled coverage from at least three different insurers before deciding, because the savings vary wildly depending on which company writes your auto policy and which writes your home policy.

Some carriers discount bundles aggressively while others barely move the needle, so the only way to know is to compare actual numbers side by side. Rates vary dramatically between insurers for the same coverage because each company weights risk factors differently and may have different exposure in your area. A carrier that just expanded into your region might offer aggressive rates to build market share, while another carrier might be pulling back from your area and raising prices.

Install Safety Features That Reduce Your Risk Profile

A monitored security system typically cuts your homeowners premium by 5 to 15 percent depending on the carrier and your location, while deadbolt locks, smoke detectors, and fire extinguishers earn smaller discounts of 2 to 5 percent each. Upgrading to impact-resistant windows and doors in high-wind areas can save 10 to 20 percent on premiums, which makes financial sense if you live in Texas where hail and severe weather are common. These improvements lower your risk profile in the insurer’s eyes, which translates directly to lower rates.

Document every safety improvement you make with photos and receipts, then contact your insurer to confirm they’ve applied the discount to your policy. Many homeowners install these features but never ask their insurer to adjust the premium, leaving free money on the table. Your insurer won’t automatically reduce your rate-you must request it.

Compare Quotes from Multiple Carriers

Comparing quotes from multiple carriers is non-negotiable if you want the best rate, yet most homeowners shop with only one or two insurers before making a decision. You should get quotes from at least five different companies using identical coverage limits and deductibles so you’re comparing apples to apples, not different protection levels that happen to have different prices. When you request quotes, ask each carrier specifically about discounts you qualify for based on your home’s age, construction type, claims history, and safety features.

These market dynamics shift annually, which is why shopping every two to three years makes sense even if you’re happy with your current insurer. Rates change based on carrier strategy, local loss experience, and competitive pressure in your area.

Adjust Your Deductible Strategically

Increasing your deductible from $500 to $1,000 typically lowers your premium by 10 to 15 percent, but only take this step if you have cash reserves to cover that deductible without financial strain when a claim happens. The goal is finding the lowest premium that doesn’t force you to compromise on coverage limits or leave you unable to pay your deductible when you need it. A higher deductible makes sense only if your emergency fund can absorb the cost without creating hardship.

Final Thoughts

Homeowners insurance basics rest on three core decisions: you must buy enough dwelling coverage to rebuild your home, protect your belongings at realistic replacement values, and maintain liability limits that safeguard your personal assets. Most homeowners get at least one of these wrong, which is why about 1 in 3 homeowners misunderstand key coverage components according to ValuePenguin. The difference between adequate protection and inadequate coverage often only becomes clear after a loss occurs, when it’s far too late to adjust.

You should calculate your home’s true replacement cost using local construction estimates, not market value or purchase price. Inventory your belongings and confirm your personal property limits match what you actually own. Review your liability coverage and honestly assess whether $100,000 or $300,000 better protects your assets and lifestyle, then shop quotes from at least five different carriers every two to three years because rates shift based on carrier strategy and local market conditions.

An independent insurance agent makes this process dramatically simpler. We at Grimes Insurance Agency access multiple carriers, which means we can show you options and pricing that a captive agent simply cannot match. We help you understand what you’re actually buying, identify gaps in your coverage, and find legitimate ways to lower premiums without sacrificing protection.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation