Real Estate Investor Insurance: Tailored Coverage for Your Properties

Your rental properties generate income, but they also expose you to risks that standard homeowners insurance won’t cover. A single liability claim or vacancy can threaten your entire investment portfolio.

Real estate investor insurance fills these gaps with protection designed specifically for landlords and property investors. We at Grimes Insurance Agency help investors like you understand which coverages matter most for your unique situation.

Why Real Estate Investors Need Specialized Coverage

Standard Homeowners Policies Exclude Rental Activity

Homeowners insurance protects a primary residence and personal belongings, but it explicitly excludes rental income and tenant-related liabilities. If you rent out your property regularly, your standard homeowners policy will deny claims related to that rental activity. Insurers investigate how you use the property and refuse to pay if they discover undisclosed rental activity.

The Insurance Information Institute confirms that homeowners policies don’t adequately cover rental income or tenant-caused damages. Many accidental landlords discover this gap only after filing a claim, when the insurer denies coverage entirely. Switching to landlord insurance helps pay for property damage, injury and liability claims made against you, and could even include loss of rental income-it’s the only way to legally and reliably protect your investment.

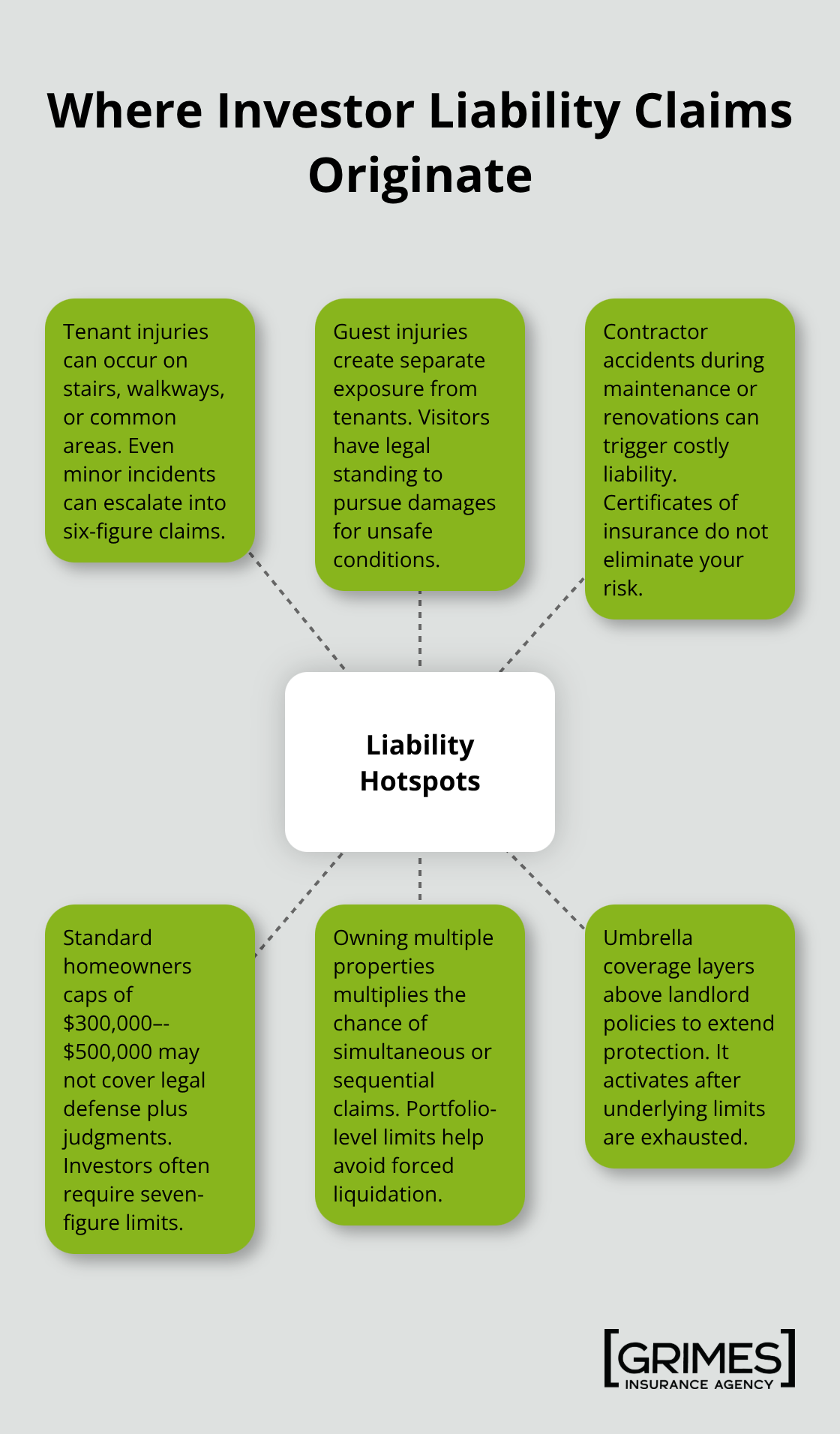

Multiple Properties Create Compounding Liability Risks

Each property you own creates separate liability risks. A tenant injured on one property, a guest hurt on another, and a contractor accident on a third-each event carries the potential for a lawsuit that could exceed standard coverage limits. Standard homeowners liability typically caps at $300,000 to $500,000 per occurrence, which barely covers legal defense costs in serious injury cases, let alone the actual judgment.

Real estate investors commonly face liability claims ranging from $500,000 to over $2,000,000, according to industry risk assessments. A minimum liability limit of $1,000,000 per occurrence and $2,000,000 aggregate is the baseline for investors with multiple properties. Umbrella policies layer on top of your landlord insurance to provide that additional protection without breaking your budget-they typically cost $150 to $300 annually for $1,000,000 in extra coverage. Without adequate liability limits across your portfolio, a single serious claim could force you to liquidate properties to pay a judgment.

Rental Income Loss Threatens Your Cash Flow

A fire, severe weather, or major plumbing failure can render a rental property uninhabitable for weeks or months. During that time, tenants move out, rent stops flowing, but your mortgage, property taxes, and maintenance costs continue. Loss of rents coverage compensates you for that income gap, typically covering 12 to 24 months of lost rental income depending on your policy.

Without this coverage, you absorb 100 percent of the lost income yourself-a devastating hit if you own multiple properties with thin margins. Properties in high-risk areas like Florida and California benefit especially from loss of rents coverage, given the frequency of hurricanes and wildfires. This protection keeps your portfolio solvent when disaster strikes, which is why understanding your specific coverage options matters before the next loss occurs.

Essential Coverage Types for Real Estate Investors

Landlord Insurance Forms Your Foundation

Landlord insurance forms the foundation of any real estate investor’s protection plan, and it differs fundamentally from homeowners coverage in ways that directly impact your claims. This policy covers the building structure, liability claims from tenants or guests, and rental income loss-three areas where homeowners insurance explicitly fails. When you purchase landlord insurance, you receive property damage protection on the rental building itself, liability coverage that starts at $1,000,000 per occurrence for most investors, and optional loss of rents coverage that replaces income during repairs.

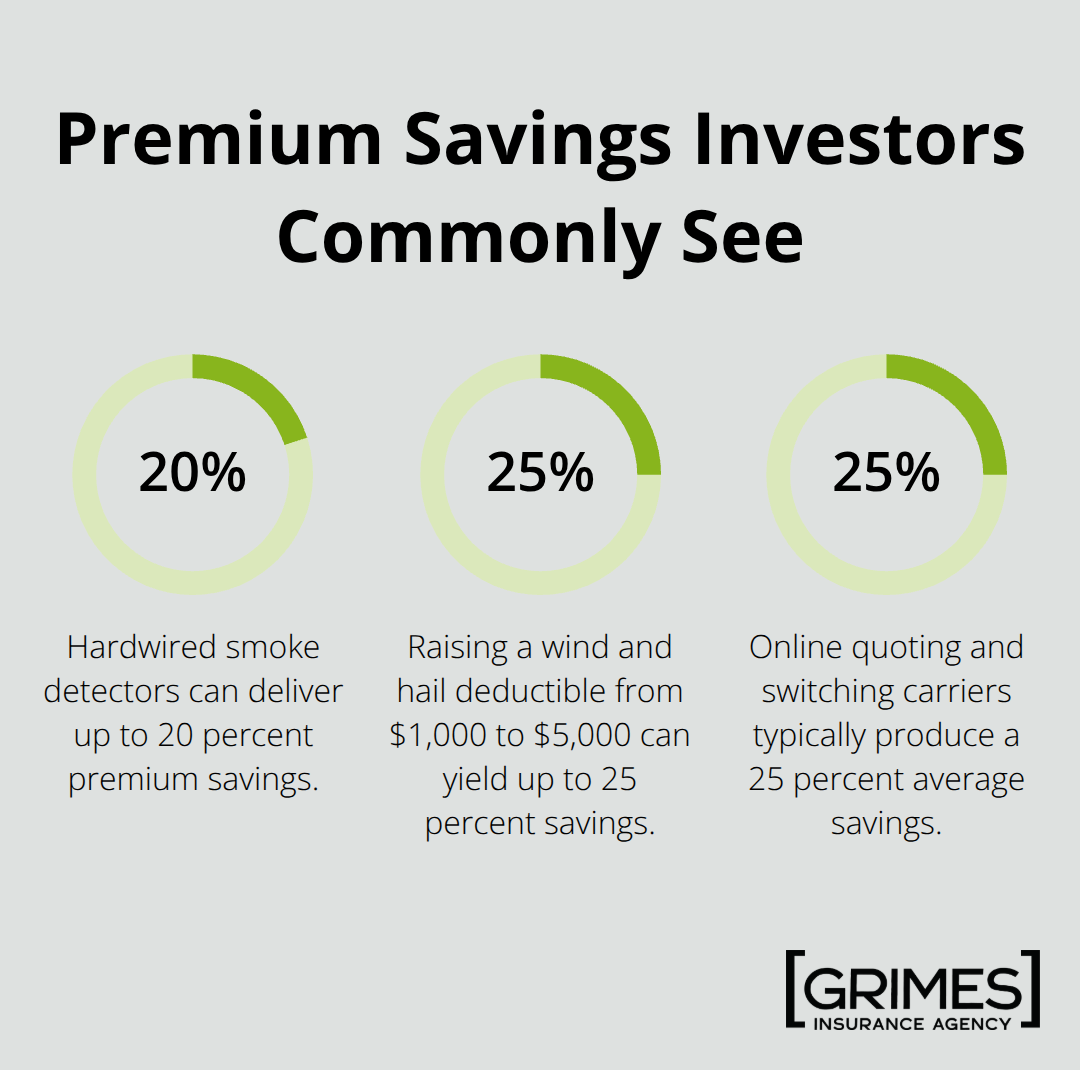

The cost varies based on property value, location, and your claims history. Upgrading your roof to impact-resistant materials reduces premiums by 10 to 20 percent depending on your carrier. Installing hardwired smoke detectors contributes additional savings of up to 20 percent. These discounts represent real money that compounds across multiple properties in your portfolio.

Umbrella policies protect against catastrophic claims

Umbrella policies sit above your landlord insurance and provide the second critical layer of protection that separates serious investors from those operating dangerously exposed. Umbrella limits typically range from $1 million to $25 million, depending on several variables, and the policy activates only when a liability claim exhausts your underlying landlord policy limits.

Real estate investors commonly face claims ranging from $500,000 to over $2,000,000, which means your baseline $1,000,000 landlord liability limit can disappear quickly in catastrophic injury cases. Without umbrella coverage, you remain personally liable for the excess amount-money that comes directly from your assets and future income. This gap between your primary coverage and potential claims represents the single biggest threat to your portfolio’s stability.

Loss of Rents Coverage Maintains Cash Flow During Repairs

Loss of rents coverage compensates you for rental income lost while a property becomes habitable again after fire, severe weather, or major system failures. This coverage typically spans 12 to 24 months of lost rent depending on your policy terms and location risk profile. Properties in Florida and California should prioritize this coverage given hurricane and wildfire frequency.

The coverage cost remains relatively modest compared to the financial devastation of losing months of income while carrying mortgage payments and property taxes. A single extended vacancy can wipe out your annual profit margin on that property. When you assess your portfolio’s vulnerability to income loss, loss of rents coverage shifts from optional to essential-especially if you depend on rental income to service debt or fund other investments.

How to Choose the Right Coverage for Your Portfolio

Document Your Properties and Their Specific Risks

Start by listing every property you own, its current replacement cost, the annual rental income it generates, and its specific risks. A single-family home in a low-risk area requires different coverage than a four-unit multifamily building in a flood zone or a short-term rental property. Your replacement cost should reflect current construction prices, not the purchase price from five years ago. Once you document these details, you can match each property’s profile to the appropriate coverage tiers. A $400,000 rental home needs different liability limits and property protection than a $1.2 million multifamily investment.

Properties in hurricane zones should include wind and hail deductibles separate from your standard deductible. Raising this deductible from $1,000 to $5,000 typically yields savings of up to 25 percent, but only if you can absorb that out-of-pocket cost after a loss. The goal is matching coverage depth to actual exposure, not purchasing the cheapest option available or over-insuring properties that carry minimal risk.

Compare Quotes Across Multiple Carriers

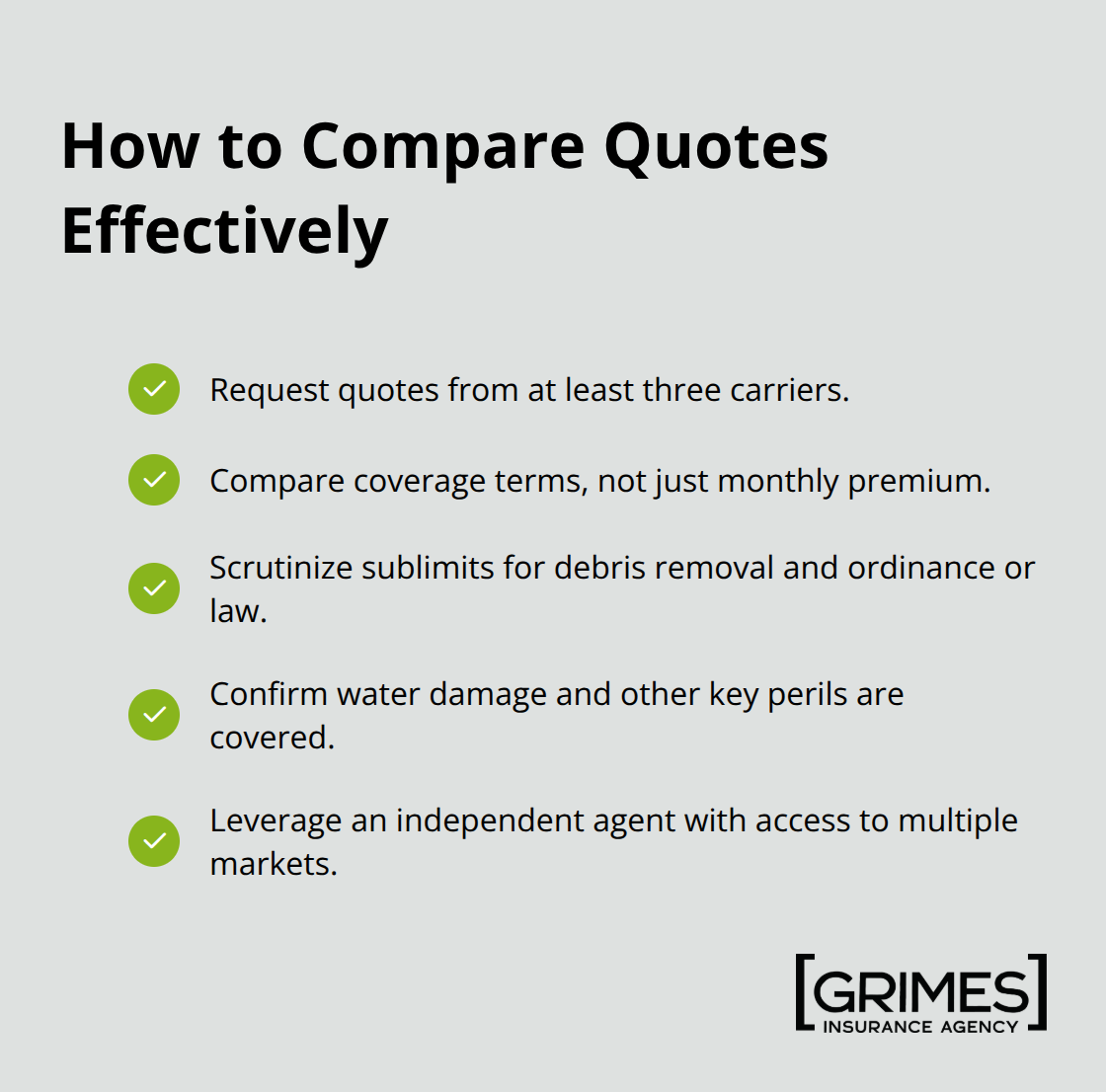

Comparing quotes across multiple carriers takes discipline but delivers measurable results. Online quoting platforms have streamlined this process-you can receive transparent quotes without paper applications and typically see a 25 percent average savings when switching carriers or implementing online policies. Request quotes from at least three carriers and examine the actual coverage terms, not just the premium.

A $50-per-month difference becomes meaningless if one policy denies claims for water damage while another covers it, or if one caps liability at $500,000 when you need $1,000,000. Pay particular attention to sublimits for debris removal and ordinance compliance-these hidden caps can leave you short thousands of dollars after a major loss. An independent agent who represents multiple carriers, rather than captive agents tied to a single company, can access the full market and identify which carriers best match your portfolio’s specific risks.

Work with an Agent Who Understands Your Portfolio

The agent you choose should ask detailed questions about your property management practices, tenant screening, maintenance standards, and claims history-these factors directly influence both premium and coverage availability. An independent agent can access multiple carriers to ensure you’re not forced into one-size-fits-all coverage. Working with an experienced agency helps you compare options and find tailored protection at competitive pricing.

Final Thoughts

Real estate investor insurance protects your assets and income in ways that standard homeowners policies simply cannot. Landlord insurance, umbrella policies, and loss of rents protection work together to shield your portfolio from the specific risks that come with owning rental properties. Without these layers, a single liability claim or extended vacancy can eliminate years of profit and force you to liquidate properties to cover losses.

Your coverage needs depend directly on your property types, locations, and risk exposure. A single-family home in a low-risk area requires different protection than a multifamily building in a hurricane zone or a short-term rental property. Properties in Florida and California face higher disaster frequency, which means loss of rents coverage becomes essential rather than optional, and your replacement costs, liability limits, and deductibles should reflect your actual exposure.

Contact Grimes Insurance Agency to discuss your real estate investor insurance needs and receive quotes from carriers that understand investment property risks. Our team accesses multiple carriers to ensure you receive the best protection and pricing for your specific situation. We ask detailed questions about your properties, management practices, and claims history to build a tailored program that matches your portfolio.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation