Home Insurance Coverage Limits: How Much Protection Do You Need

Most homeowners underestimate how much protection they actually need. We at Grimes Insurance Agency see this mistake repeatedly, and it costs people thousands when disaster strikes.

Your home insurance coverage limits determine what you’ll receive if something happens. Getting this right isn’t complicated, but it does require honest assessment of your situation.

What Coverage Limits Actually Mean

Understanding the Basics

Coverage limits are the maximum amounts your insurance company will pay for specific types of damage or liability claims. This is fundamentally different from your deductible, which is what you pay out of pocket before insurance kicks in. A $300,000 dwelling limit means your insurer will pay up to $300,000 to rebuild your home after a covered loss-but only if you actually carry that much protection. Many homeowners confuse these two concepts, thinking a high deductible means they have low coverage, when in reality they’re independent decisions that work together. Your deductible might be $1,000, $2,500, or $5,000, but that doesn’t tell you anything about your coverage limits.

How Location Affects Your Costs

The average homeowners policy costs vary significantly by location based on geography and risk factors. Your ZIP code influences everything from fire station proximity to natural disaster frequency, and these factors directly impact your premium.

The Six Core Coverage Types

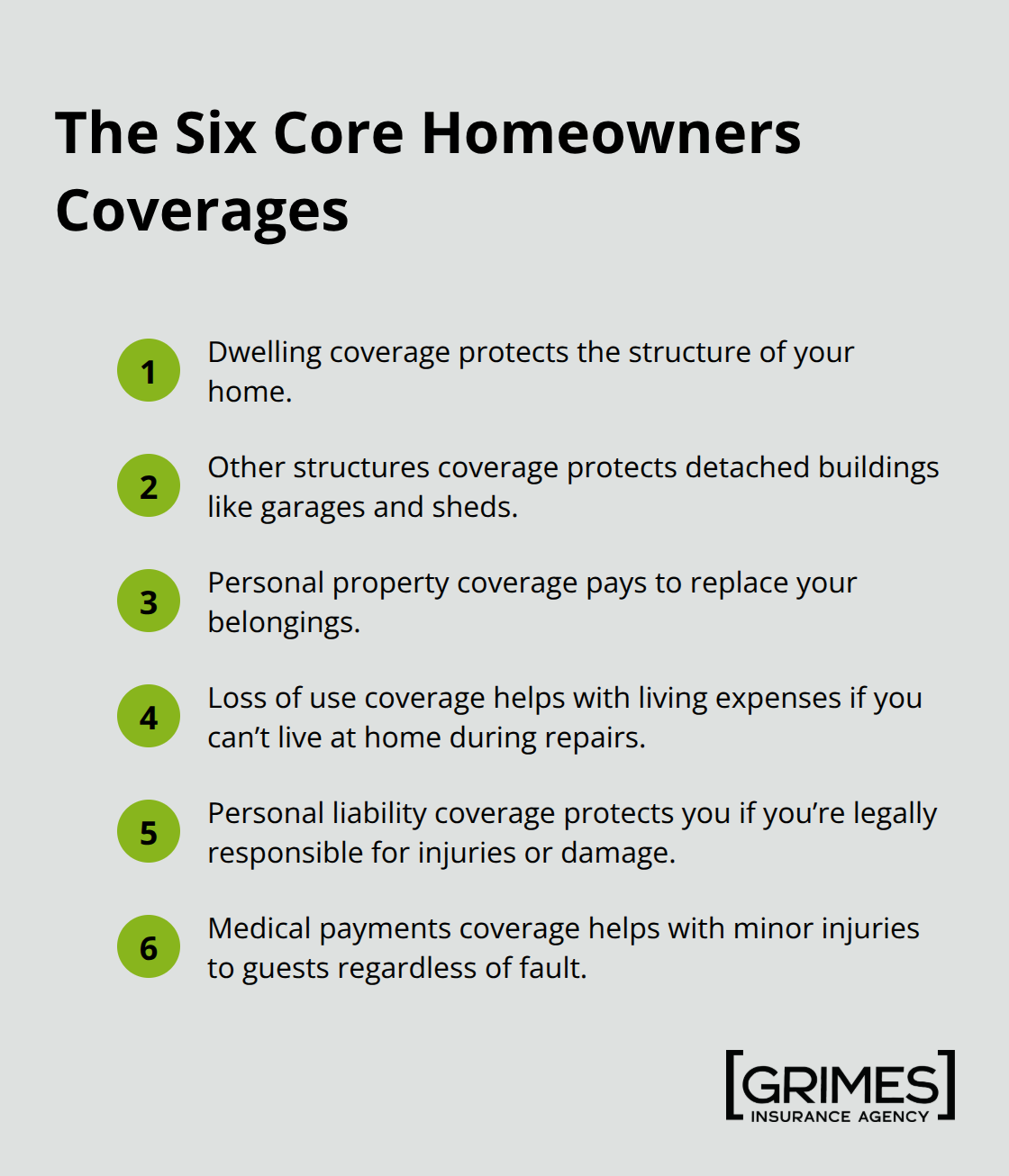

Home insurance policies typically include six basic coverages: dwelling, other structures, personal property, loss of use, personal liability, and medical payments. Your dwelling limit becomes the foundation for most other coverages since they’re calculated as percentages of that number. Other structures coverage typically runs about 10% of your dwelling limit, so a $300,000 dwelling limit usually provides $30,000 for detached garages and sheds.

Personal property coverage commonly sits between 50% and 70% of dwelling coverage, meaning you’d have roughly $150,000 to $210,000 for your belongings under that same scenario. Personal liability coverage usually starts at $100,000 per occurrence, though you should evaluate whether higher limits or an umbrella policy makes sense for your asset protection.

Why Replacement Cost Matters More Than Market Value

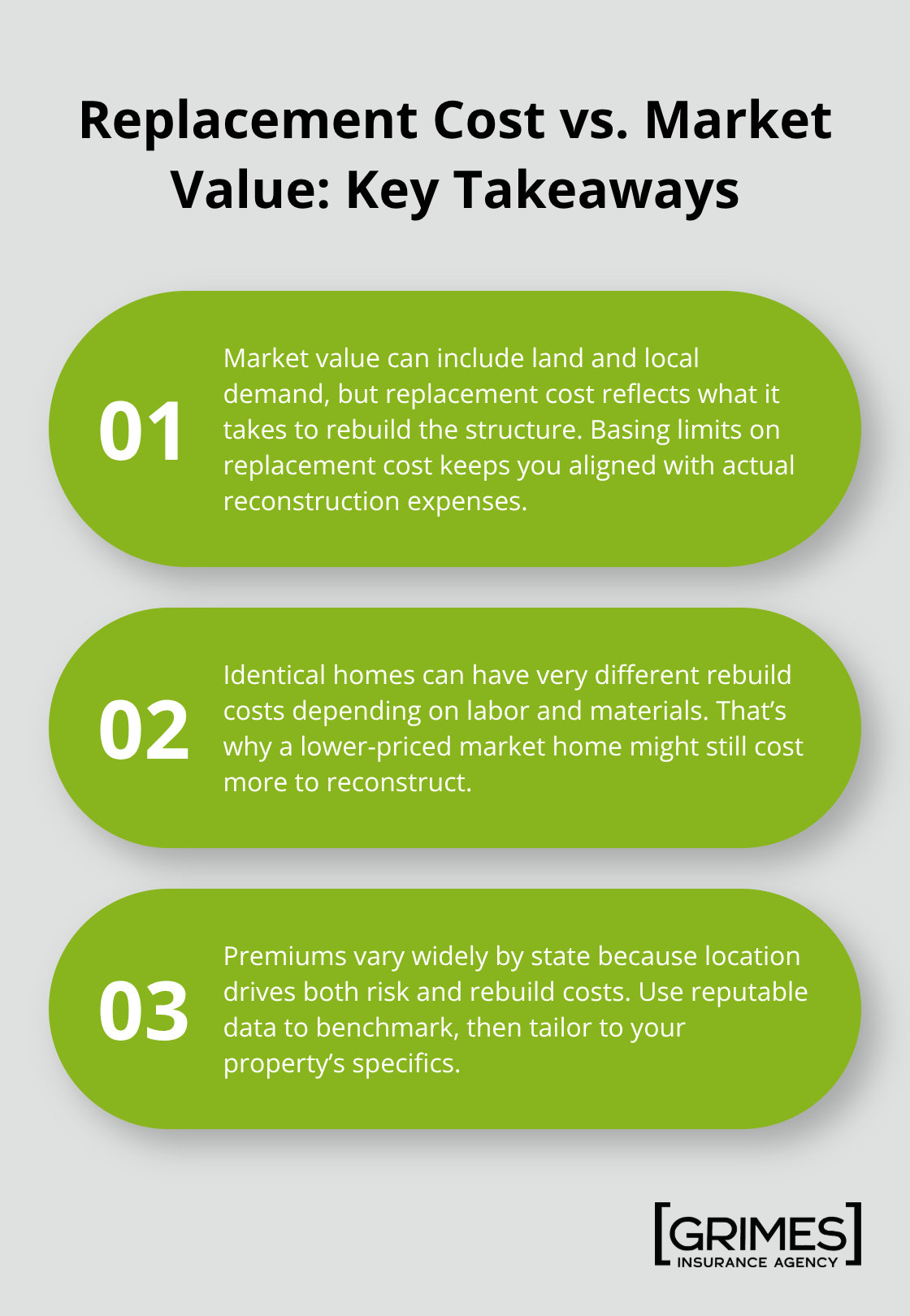

The critical mistake happens when homeowners base dwelling coverage on their home’s market value rather than its replacement cost. A $600,000 home might only cost $400,000 to rebuild because land value isn’t included in reconstruction costs. This gap shows why shopping around and understanding replacement cost matters far more than matching your Zillow estimate. The difference between what your home sells for and what it costs to rebuild creates significant confusion when you’re trying to select appropriate limits.

Understanding these distinctions sets you up to make informed decisions about your specific situation. The next step involves looking at your individual circumstances-your home’s actual rebuild costs, your personal assets, and your liability exposure-to determine what protection truly fits your needs.

What Drives Your Coverage Needs

Replacement Cost vs. Market Value

Replacement cost is the only number that matters when you determine your dwelling limit, and it has nothing to do with what Zillow says your home is worth. A $600,000 home in a market with expensive land might cost only $400,000 to rebuild because land value doesn’t factor into reconstruction. Conversely, a $400,000 home in an area with high labor and material costs could require $500,000 to properly rebuild. According to Bankrate’s November 2025 data, the average homeowners policy with $300,000 in dwelling coverage costs about $2,424 annually, but that same coverage in Oklahoma averages $4,695 while Alaska averages $1,035-showing how dramatically location influences both replacement costs and premiums.

How Location Shapes Your Replacement Cost

Your location affects replacement cost through local labor rates, material availability, and building code requirements. A contractor in a rural area charges differently than one in a major metropolitan region, and older homes often trigger more expensive code upgrades during reconstruction. To find your actual replacement cost, multiply your home’s square footage by the local cost per square foot, then adjust for your specific features like foundation type, materials, and architectural complexity. This number becomes your dwelling limit foundation, and underestimating it creates serious consequences. The 80% rule requires you to carry at least 80% of your replacement cost to avoid coinsurance penalties that reduce your payout after a loss. If your replacement cost is $400,000 and you only carry $300,000 in coverage, you’re underinsured and will face reduced claim payments.

Tailoring Liability Coverage to Your Assets

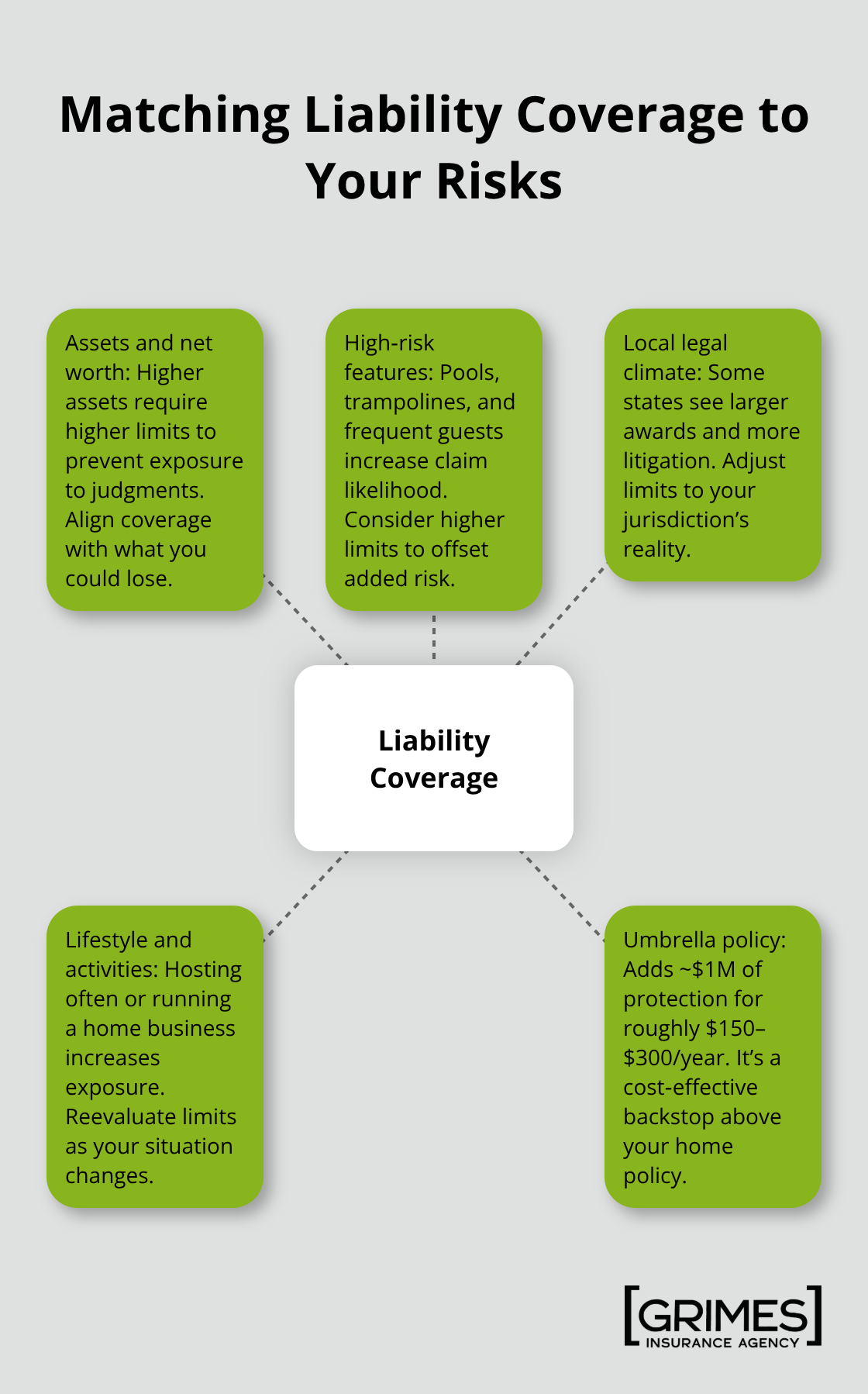

Your personal liability exposure depends on your assets and circumstances, not generic recommendations. Personal liability coverage typically starts at $100,000 per occurrence, but if you own significant assets, have frequent visitors, or own a pool or trampoline, higher limits make sense. Your location matters here too-states like California and New York see higher liability awards than rural areas, which should factor into your decision. If you have $500,000 in savings and investments, carrying only $100,000 in liability coverage leaves most of your wealth exposed to a lawsuit. Consider an umbrella policy that sits above your homeowners liability coverage, typically offering $1,000,000 in additional protection for $150 to $300 annually.

Personal Property and Special Coverage Needs

For personal property coverage, create a detailed inventory of your belongings and calculate replacement cost for each category rather than guessing at percentages. If you have expensive jewelry, artwork, or collections, standard personal property coverage may cap individual items at $1,500 to $2,500, requiring scheduled personal property endorsements for adequate protection. Loss of use coverage, typically set at 20% to 30% of your dwelling limit, covers hotel stays and meals if you can’t live in your home during repairs-but verify this amount matches your actual living expenses if you were displaced.

Your specific situation determines what protection actually fits, and that assessment requires honest evaluation of your home’s rebuild costs, your personal assets, and your liability exposure. The next step involves calculating these numbers precisely so you can select coverage limits that truly protect your family and finances.

How to Calculate the Right Coverage Limits for Your Home

Start with Replacement Cost, Not Market Value

Multiply your home’s square footage by your local cost per square foot to establish a baseline figure that beats guessing. According to Bankrate’s November 2025 data, homes in Oklahoma with $300,000 dwelling coverage cost an average of $4,695 annually, while the same coverage in Alaska averages $1,035. This massive difference reflects how local labor rates and material costs shape replacement expenses. Your contractor charges differently depending on region-a 2,000-square-foot home in Denver costs far more to rebuild than the identical structure in rural Kansas. After calculating your baseline, adjust upward for specific features: older homes trigger expensive code upgrades during reconstruction, complex architectural designs cost more than simple rectangular structures, and foundation type matters significantly. A home on a concrete slab costs less to rebuild than one requiring a full basement.

Account for Your Home’s Unique Features

If your home deviates from local averages (custom materials, high-end finishes, or unusual design), quick online calculators will underestimate your true replacement cost. This is when you need professional help: hire an appraiser or obtain quotes from local contractors who understand your area’s building codes and material availability. Many homeowners carry $300,000 in dwelling coverage when they actually need $450,000, and that $150,000 gap creates catastrophic problems after a total loss. The 80% rule requires you to carry at least 80% of your replacement cost, and falling short triggers coinsurance penalties that reduce your entire claim payout. If your actual replacement cost is $500,000 and you only insure for $300,000, you’re violating the 80% rule and will face reduced payments even for partial losses.

Create a Detailed Personal Property Inventory

Spend an afternoon photographing and listing everything in your home-furniture, electronics, clothing, kitchen items, tools. This inventory reveals whether standard coverage limits work or whether you need higher limits or scheduled personal property endorsements. Most homeowners carry personal property coverage at 50% to 70% of their dwelling limit without knowing what that actually covers. If you own a $5,000 bicycle, $8,000 in jewelry, or valuable artwork, standard policies cap individual items at $1,500 to $2,500, leaving you massively underprotected. Schedule these items separately for full replacement cost coverage.

Match Liability Coverage to Your Assets and Risks

Evaluate your specific liability exposure honestly instead of accepting generic $100,000 limits. If you own significant assets (savings, investment accounts, real estate equity), that wealth remains vulnerable to lawsuit judgments unless your liability coverage matches your net worth. A pool or trampoline on your property dramatically increases liability risk, as does frequently hosting guests or running a home-based business. Carrying $100,000 in liability coverage when you have $500,000 in assets is financially reckless. An umbrella policy adds $1,000,000 in coverage for roughly $150 to $300 annually, making it the cheapest insurance you can buy relative to the protection it provides.

Verify Your Loss of Use Coverage Matches Your Needs

Calculate what a temporary rental plus meals would cost in your area if you couldn’t live at home for six months, then verify your policy covers that amount. Loss of use coverage should match your actual living expenses if displaced-20% to 30% of dwelling coverage works for some families but not others. This protection covers hotel stays and meals if you can’t occupy your home during repairs, and underestimating it leaves you paying out of pocket for temporary housing during reconstruction.

Final Thoughts

Getting your home insurance coverage limits right protects your family and finances when disaster strikes. Base your dwelling limit on replacement cost, not market value, then set other coverages as percentages of that foundation. Most homeowners underestimate what they need, and that mistake costs thousands when they file a claim.

Your situation is unique, which means generic recommendations fail. A detailed inventory of your belongings reveals whether standard personal property limits work or whether you need scheduled endorsements for expensive items. Your liability exposure depends on your assets and circumstances, not cookie-cutter $100,000 limits that leave most homeowners underprotected. An umbrella policy costs $150 to $300 annually and adds $1,000,000 in coverage, making it the smartest protection you can buy relative to its cost.

We at Grimes Insurance Agency help homeowners in Lubbock and beyond select appropriate home insurance coverage limits for their specific situations. Our independent agency accesses multiple carriers, so you receive the best protection and pricing rather than settling for one company’s recommendations. Contact us to review your current coverage and calculate the limits that actually fit your needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation