Commercial Property Risk Assessment: A Local Guide

Texas businesses face real property threats year-round, from severe weather to theft and system failures. A solid commercial property risk assessment helps you spot vulnerabilities before they become costly problems.

We at Grimes Insurance Agency work with local business owners to identify these risks and build protection strategies that actually work. This guide walks you through the assessment process and shows you how to strengthen your defenses.

What Risks Threaten Texas Commercial Properties Most

Texas commercial properties face three major threats that drain finances fast: extreme weather, equipment failures, and criminal activity. The U.S. Fire Administration reported 116,500 non-residential building fires across the United States in 2021, causing roughly $3.7 billion in direct property damage. That same year, Texas experienced significant hail and wind damage that forced thousands of businesses to file claims. These aren’t rare events-they happen regularly, and properties without proper assessment pay the price through damage, downtime, and inflated insurance premiums.

Weather and Natural Disasters Hit Hard in Texas

Hail storms, tornadoes, and severe winds strike Texas regularly. The state sits in an active weather corridor where spring and early summer bring particularly dangerous conditions. Hail damages roofs, siding, and HVAC systems at a staggering rate, often costing tens of thousands to repair. Wind events tear off roof sections, shatter windows, and topple structures. Beyond immediate damage, these events trigger business interruption-your operations stop, revenue stops, but expenses continue. A thorough risk assessment identifies which parts of your building face the most vulnerability to weather impact. Roof condition, structural integrity, and window placement all matter. Older roofs with poor drainage systems fail faster during heavy rain. Buildings with inadequate bracing struggle in high winds. The goal isn’t to eliminate risk-it’s to know exactly what your exposure is and prepare accordingly.

Fire and Electrical Failures Demand Constant Vigilance

Fire risk in commercial properties stems from multiple sources: faulty electrical wiring, overloaded circuits, flammable material storage, and malfunctioning equipment. Electrical hazards appear everywhere-damaged insulation, loose wires, water leaks near electronics, and tangled extension cords create fire conditions that spread quickly. Equipment like ovens, HVAC systems, motors, and generators deteriorates over time and can ignite without warning. Thermal imaging and heat sensing tools detect hotspots before they become fires, revealing equipment on the verge of failure. Regular inspections catch these problems early. Fire suppression systems matter tremendously-automatic sprinklers reduce fire damage substantially, though credit depends on current maintenance and system design. Fire extinguishers need annual recharging and pressure checks. Smoke detectors must stay clean and functional. Blocked fire department connections and obstructed sprinkler heads render protection systems useless when you need them most. Exits must be clearly marked and free of debris so occupants can evacuate safely. A single electrical or fire incident can shut down your business for weeks or months while repairs happen and investigations conclude.

Theft, Vandalism, and Security Gaps Cost More Than You Think

Criminal activity targets commercial properties constantly-theft of inventory, equipment, and materials; vandalism that damages facades and signage; break-ins that compromise data and assets. Local crime statistics matter here. Texas cities vary widely in property crime rates, so understanding your neighborhood’s specific threats shapes your security strategy. Physical security upgrades like reinforced locks, access control systems, and surveillance cameras deter criminals and provide evidence if incidents occur. More cameras with advanced detection capabilities catch intruders and track suspicious activity. However, physical security alone isn’t enough anymore-digital threats are equally serious. Data breaches, ransomware attacks, and system compromises expose sensitive information and shut down operations. A comprehensive asset inventory covering both physical assets (buildings, inventory) and digital assets (databases, software) reveals what needs protection. Regular security audits test your current defenses and identify weaknesses. Employee training reduces human-factor breaches where staff inadvertently compromise security. Unauthorized access, whether physical or digital, creates liability exposure and operational chaos that extends far beyond the immediate loss.

Understanding these three threat categories sets the foundation for a structured risk assessment. The next section walks you through the specific steps to document your property, evaluate your building systems, and review your loss history so you can build a protection strategy tailored to your Texas location.

How to Build Your Risk Assessment from the Ground Up

Document Your Property and Assets Thoroughly

Create a complete inventory of everything your business owns and operates. Walk through your property with a camera or smartphone and photograph every area: the roof condition, exterior walls, windows, doors, HVAC equipment, electrical panels, fire suppression systems, inventory storage, and any specialized equipment. Document the age of major systems-when the roof was installed, when the electrical system last received upgrades, when HVAC units underwent service. Photograph any visible damage, water stains, rust, or deterioration. This visual record becomes your baseline for tracking changes over time and proves invaluable when filing insurance claims.

Create a spreadsheet listing all assets with replacement values. Include building components (roof, foundation, walls), equipment (machinery, computers, vehicles), inventory, and data systems. Assign realistic replacement costs to each item-don’t underestimate. A commercial roof replacement in Texas runs $15,000 to $50,000 depending on size and material. HVAC system replacement costs $8,000 to $25,000. Electrical panel upgrades cost $3,000 to $10,000. These numbers matter because they determine how much insurance coverage you actually need. Many Texas business owners underinsure their properties and discover the gap only after a loss occurs.

Evaluate Your Building Systems with Professional Inspection

Schedule a professional commercial property inspection to assess construction class, fire safety systems, electrical integrity, and equipment condition. An inspector trained in commercial standards identifies electrical hazards like damaged insulation, overloaded circuits, and loose wires that your staff might miss. They check whether fire extinguishers maintain proper pressure with current inspection tags, whether sprinkler systems have clear head spacing and open valves, and whether exits remain unobstructed. They use thermal imaging to detect equipment hotspots before failures occur.

Review Your Property’s Loss History and Local Crime Data

Pull your property’s loss history for the past five to ten years. What claims have you filed? Were they weather-related, equipment failures, theft, or liability incidents? What patterns emerge? If you filed three hail claims in five years, your roof vulnerability is obvious and your coverage needs adjustment. If you never filed a claim, that doesn’t mean your property is risk-free-it means you’ve been fortunate. Texas properties in high-wind or hail zones face regular exposure regardless of past claims.

Review your local area’s crime statistics through the Texas Department of Public Safety or your city’s police department. Understand whether your neighborhood experiences frequent theft, burglary, or vandalism. This shapes your security investment decisions. Properties in high-crime areas need more robust access controls and surveillance than those in safer zones.

Connect Assessment Findings to Coverage Decisions

The goal of this assessment process isn’t perfection-it’s accuracy. You need to know your actual exposures so you can protect against them intelligently and carry appropriate insurance coverage that reflects your real risk profile. Once you’ve documented your assets, evaluated your building systems, and reviewed your loss patterns, you have the foundation to identify which risks demand immediate attention and which ones require ongoing monitoring. The next section shows you exactly how to translate these findings into concrete mitigation strategies that reduce losses and strengthen your property’s resilience.

How to Turn Risk Assessment into Real Protection

Your risk assessment has identified the threats facing your Texas property. Now you need to act on those findings with concrete steps that actually reduce losses. Security upgrades, maintenance schedules, and insurance coverage adjustments aren’t optional add-ons-they’re the difference between a manageable loss and a business-ending catastrophe.

Strengthen Physical and Digital Security Together

Start with physical security because it delivers immediate, visible results. Install reinforced locks on all exterior doors and upgrade to access control systems that log who enters and when. Commercial-grade surveillance cameras with motion detection and cloud storage create a continuous record that deters criminals and provides evidence if incidents occur. Position cameras to cover entry points, inventory areas, and equipment storage zones. Advanced systems with thermal imaging capabilities detect unauthorized movement even in low light.

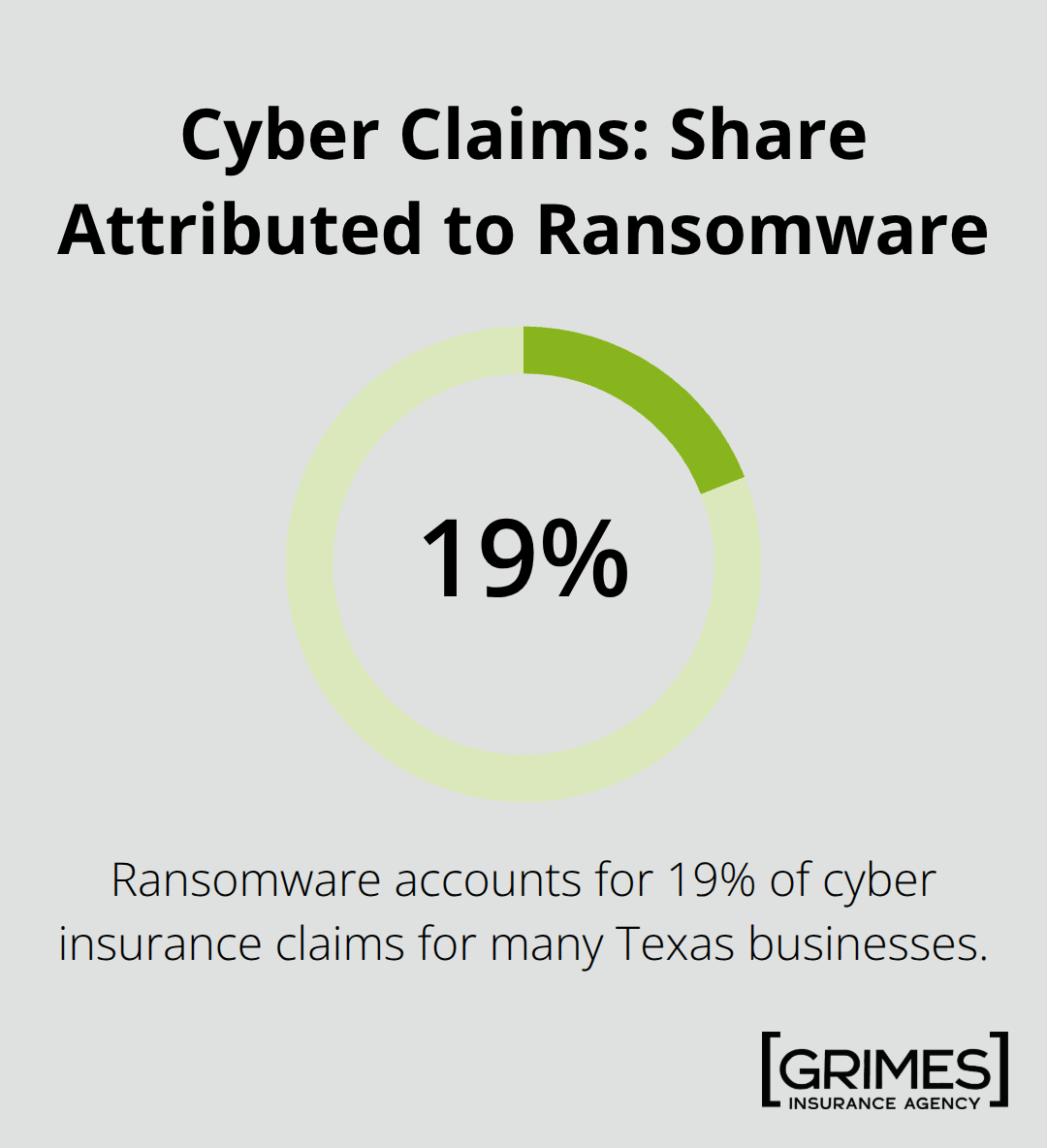

However, physical security alone fails without digital protection. Ransomware accounts for 19% of all claims made on cyber insurance in many Texas businesses. Implement firewalls, encryption for sensitive files, and strict access controls for your network. Require employees to use strong passwords and change them quarterly. Conduct regular security audits to test your defenses-don’t wait for a breach to discover gaps.

A security provider can assess your specific property, identify vulnerabilities you’d miss, and design a comprehensive plan covering both physical and digital threats. The cost of a professional assessment (typically $1,500 to $3,500 depending on property size) pays for itself through prevented losses.

Establish a Preventive Maintenance Schedule

Preventive maintenance runs parallel to security and protects your building systems from failure. Schedule professional inspections of your electrical system, HVAC equipment, and fire suppression systems at minimum annually, more frequently for aging systems. Document every service call, repair, and maintenance action in a log-this creates a clear record of your diligence and proves critical when filing claims.

Fire extinguishers need annual recharging and pressure verification. Sprinkler systems require annual inspection to confirm heads have proper clearance, valves are open, and caps are intact. Clean your roof gutters twice yearly to prevent water damage and ice dam formation during cold snaps. Check your roof condition every spring after winter weather and again in fall to catch storm damage early. Replace worn weather stripping around doors and windows-this simple $100 to $300 investment prevents water intrusion that leads to mold and structural damage.

Align Your Insurance Coverage with Actual Exposure

Insurance coverage must match your actual exposure. If your risk assessment revealed an older roof in a high-hail zone, your current coverage limits may fall short of replacement costs. Request a coverage review from your insurance agent to confirm your building coverage reflects current replacement values, not outdated estimates. Many Texas properties carry coverage based on five or ten-year-old valuations while construction costs have risen 20 to 40 percent. Underinsurance leaves you paying the difference out of pocket after losses.

Consider increasing deductibles on coverages where you can absorb the risk-this lowers your premiums and frees up budget for security and maintenance investments that prevent losses entirely.

Final Thoughts

A thorough commercial property risk assessment reveals exactly where your vulnerabilities lie and lets you invest in protection that actually matters instead of guessing. Your risk profile changes constantly as equipment ages, weather patterns shift, crime fluctuates in your neighborhood, and building systems deteriorate. You should schedule a comprehensive reassessment every two to three years, or immediately after major property changes, significant losses, or when you expand operations.

We at Grimes Insurance Agency understand that Texas business owners need coverage built on accurate risk assessment and tailored to your specific location and operations. Our team works with multiple carriers, which means we match your coverage to your actual needs instead of pushing one-size-fits-all solutions. We’ve spent over 75 years helping Lubbock and Texas businesses identify their real exposures and secure the right protection at competitive rates.

Contact Grimes Insurance Agency to schedule a coverage review based on your risk assessment findings. Bring your asset inventory, your loss history, and your questions so we can help you translate your assessment into a protection strategy that keeps your business running strong.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation