How to Reduce Flood Insurance Premiums: Tips for Texas Homeowners

Flood insurance premiums in Texas can drain your budget fast, especially if you live in a high-risk area. The good news is that several proven strategies can meaningfully lower what you pay each year.

We at Grimes Insurance Agency help Texas homeowners reduce their flood insurance costs through smart mitigation choices and competitive rate shopping. This guide walks you through the most effective ways to protect your home while keeping premiums manageable.

Why Flood Risk Matters More in Texas Than You Think

Texas Flood Geography Creates Two Major Danger Zones

Texas faces flood risk far beyond what most homeowners realize. The state’s geography creates two major danger zones: the coastal areas and Flash Flood Alley, a central-north region where heavy rains concentrate and overwhelm drainage systems.

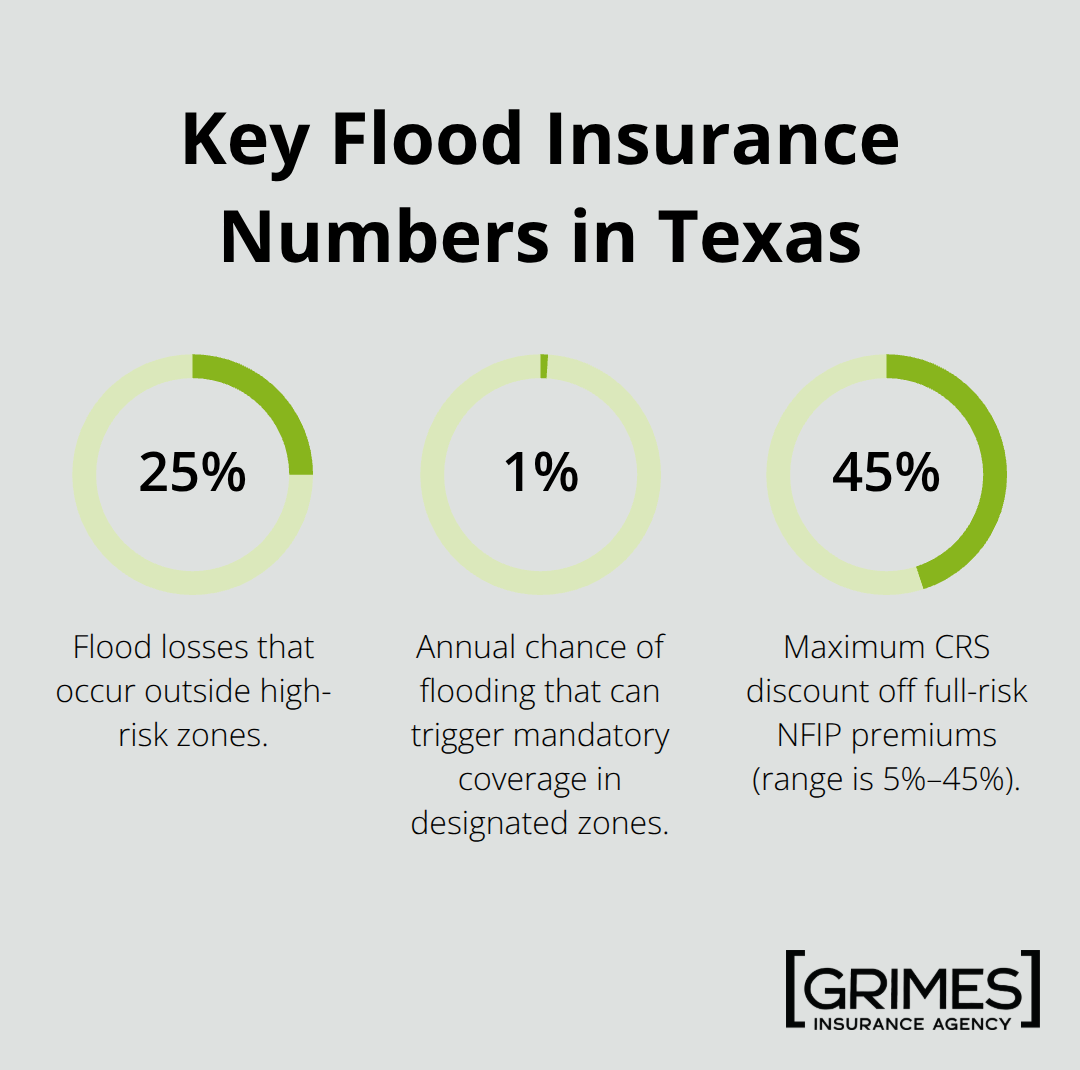

Almost every major Texas city sits in a high flood risk area, which means your location matters enormously for insurance costs. The National Flood Insurance Program reports that about 25 percent of flood losses occur outside high-risk zones-a statistic that catches many Texas homeowners off guard.

How Flood Zone Designation Drives Your Premiums

Flood zone assignment drives your premiums more than almost any other factor. If your home sits in a designated flood zone with a 1 percent annual chance of flooding, your lender likely requires flood insurance whether you want it or not. Standard homeowners insurance does not cover flood damage under any circumstances, which is why this separate policy becomes non-negotiable for most Texas properties. The proximity of your home to rivers, bays, or coasts, combined with local flood frequency data from FEMA, determines your initial premium baseline. Homes in Flash Flood Alley or coastal regions face steeper rates because historical flood patterns prove the risk is real and measurable.

FEMA’s Elevation Estimates Often Miss the Mark

FEMA estimates first-floor height using satellite imagery and algorithmic data, but these estimates often contain errors. If FEMA underestimates your home’s elevation, you overpay; if they overestimate it, your policy costs less than it should. This is where an Elevation Certificate from a licensed surveyor becomes valuable, providing precise measurements that can lower premiums by $800 to $1,500 annually in Houston when corrections are submitted.

The Elevation Certificate Investment Pays for Itself

The investment in an Elevation Certificate typically costs around $600 in Houston, making it a one-time expense that pays for itself quickly if your home sits higher than FEMA’s estimate. Homes with steps to the front door, crawlspace vents, or locations in high-risk zones like Meyerland, Bellaire, and parts of Katy are the best candidates for certificate benefits. The key insight is that flood zone assignment and elevation data directly control your premiums, and challenging inaccurate FEMA data produces measurable savings that compound year after year.

These foundational factors set the stage for the practical mitigation strategies that actually lower what you owe each month.

How to Strengthen Your Home and Shop Smart for Better Rates

Elevation Improvements Deliver the Biggest Premium Cuts

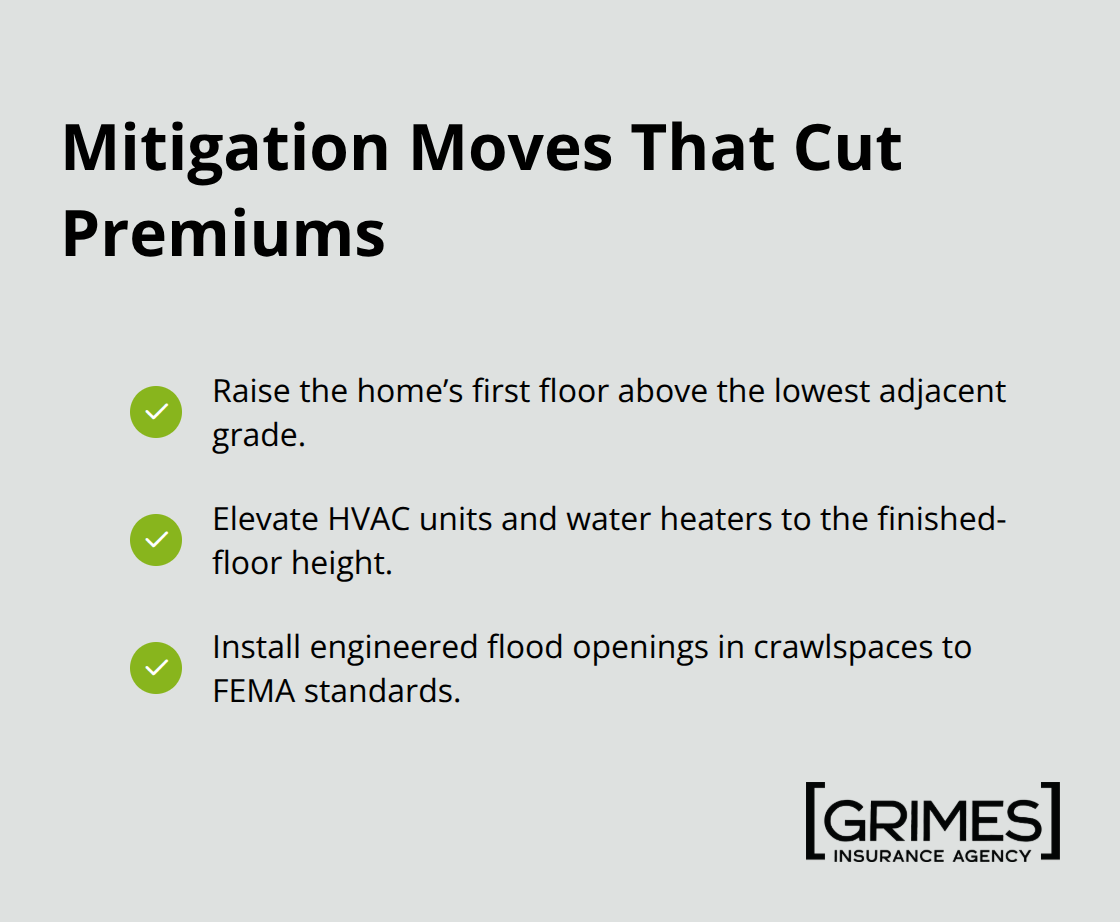

The most effective way to lower flood insurance premiums is to reduce the risk FEMA sees in your property. Elevation improvements stand out as the single most powerful mitigation strategy because they directly lower your first-floor height relative to the base flood elevation, which is the primary driver of NFIP pricing. Raising your home’s first floor above the lowest adjacent grade, elevating critical machinery and equipment like HVAC units and water heaters to match floor height, or installing properly engineered flood openings in crawlspaces all trigger measurable premium reductions.

The NFIP Flood Insurance Mitigation Discount Tool uses FEMA data and modeling to assess your property and shows you exactly which improvements qualify for savings before you spend money on construction. After completing any mitigation work, run the tool again to capture your new discount eligibility and get an updated premium estimate.

Compare Multiple Carriers to Find Real Savings

The second critical action is to stop accepting the first quote you receive and instead compare offerings from multiple carriers. Private flood insurance companies like Ace, Hiscox, NFS, Edge, and Lloyd’s of London now compete directly with the NFIP, and their underwriting criteria and pricing vary significantly depending on your flood zone and property specifics. A policy that costs $2,400 annually through the NFIP might cost $1,800 with a private carrier, or vice versa-the only way to know is to shop.

Accessing quotes from both NFIP and private carriers allows you to compare coverage terms and premiums side by side rather than defaulting to whatever your lender suggests. This comparison takes time but produces tangible results for most Texas homeowners.

Check Your Community’s CRS Status for Automatic Discounts

Additionally, check whether your city or county participates in the Community Rating System, a voluntary FEMA program that grants discounts ranging from 5 percent to 45 percent off full-risk NFIP premiums based on local floodplain management practices. As of October 2025, more than 1,500 communities nationwide participate, and Texas homeowners in CRS-eligible jurisdictions benefit automatically if their property complies with local floodplain regulations. Verifying your community’s CRS status and class rating takes minutes and could produce savings without any investment in your home.

These three strategies-mitigation improvements, multi-carrier shopping, and CRS verification-form the foundation of a smart premium reduction plan. The next step involves understanding how professional guidance and local expertise help you navigate these options and avoid costly mistakes.

Why Local Agents Outperform Online Quotes for Flood Insurance

Accurate Property Data Determines Discount Success

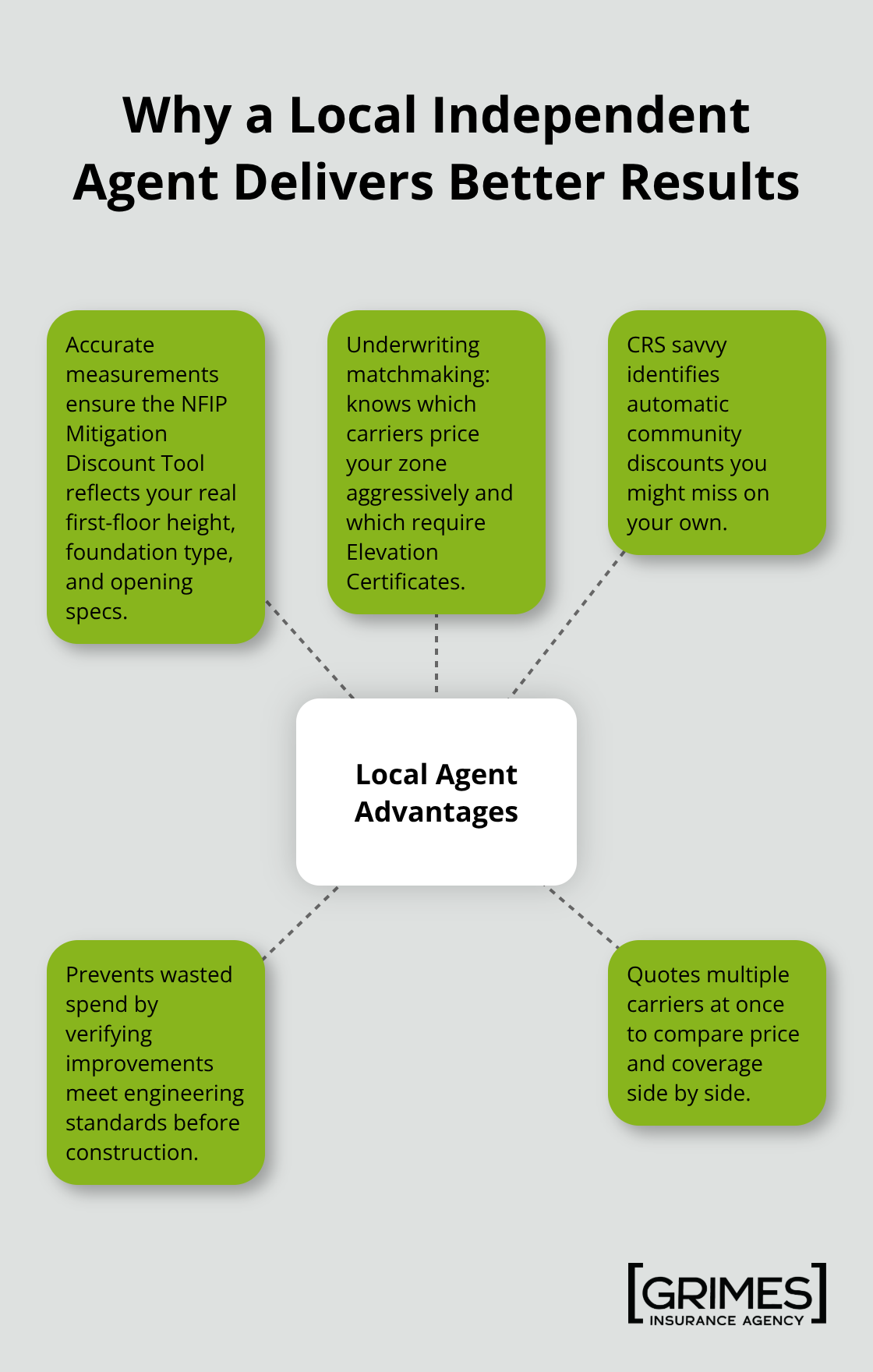

The mitigation strategies and carrier shopping methods outlined above work only if you execute them correctly, and that’s where most Texas homeowners stumble. The NFIP Mitigation Discount Tool requires accurate property data-first-floor height, foundation type, machinery elevation, and flood opening specifications. Inaccurate measurements waste your money on improvements that don’t trigger discounts. A homeowner who elevates equipment to the wrong height or installs flood openings that fail to meet engineering standards loses thousands in wasted construction costs and misses the premium reductions they expected.

Carrier Underwriting Criteria Vary Dramatically

Comparing private carriers against NFIP sounds straightforward until you realize that underwriting criteria differ wildly. A property that qualifies for a 20 percent discount with one carrier might not qualify at all with another. You need someone who knows which carriers underwrite which zones aggressively, which ones demand Elevation Certificates, and which ones offer the best terms for Texas flood risk. This knowledge separates a mediocre quote from a genuinely competitive one.

Local Expertise Identifies Hidden Savings

An independent agent with deep local knowledge outperforms online quote tools and direct NFIP applications. When properties sit in Meyerland or Bellaire-areas where FEMA’s satellite estimates consistently miss crawlspace vents and elevation details-an experienced agent knows immediately that an Elevation Certificate will likely save $800 to $1,500 annually. That same agent can guide you to qualified surveyors and help interpret results before submission. Local agents also understand CRS status for Texas communities and flag automatic discounts you’d miss on your own.

We at Grimes Insurance Agency represent multiple carriers including Ace, Hiscox, NFS, Edge, and Lloyd’s of London alongside NFIP access. This means we can run your property through underwriting criteria for each carrier simultaneously rather than forcing you to shop one quote at a time. Our team verifies property details against NFIP requirements before you invest in mitigation work, preventing costly mistakes that drain your budget.

The Measurable Difference in Outcomes

A homeowner who shops alone might obtain three quotes and miss their community’s CRS discount entirely. A homeowner working with an agent who knows Texas flood zones obtains quotes from multiple carriers, receives clear guidance on whether an Elevation Certificate makes financial sense before ordering it, and captures every available discount their property qualifies for. The difference in annual savings often reaches thousands of dollars through combinations of mitigation improvements, carrier selection, and discount verification.

Final Thoughts

Reducing flood insurance premiums in Texas requires three coordinated actions: making smart mitigation improvements to your home, comparing quotes across multiple carriers, and verifying that your community qualifies for CRS discounts. An Elevation Certificate costs $600 and pays for itself within months if your home sits higher than FEMA’s satellite estimate. Elevating critical equipment or installing flood openings triggers measurable premium reductions through the NFIP Mitigation Discount Tool, while shopping private carriers against NFIP often reveals price differences of $600 to $1,200 annually.

The challenge lies in executing these strategies correctly without wasting money on improvements that miss discount thresholds or submitting property data that triggers underwriting rejections. A local independent agent makes the difference between mediocre results and genuine savings because they understand how flood risk varies across regions, which carriers underwrite aggressively in your zone, and which mitigation improvements actually qualify for discounts before you spend construction dollars. We at Grimes Insurance Agency have served Texas homeowners for over 75 years and know exactly which combination of strategies applies to your property.

Contact Grimes Insurance Agency to review your current flood insurance situation and identify how to reduce flood insurance premiums for your specific home. We represent multiple carriers and can run your property through underwriting criteria simultaneously, verify whether an Elevation Certificate makes financial sense for your home, and confirm your community’s CRS status. This consultation identifies the exact strategies that produce the largest reduction in what you pay annually.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation