Texas Flood Insurance Costs

Flooding is the costliest natural disaster in Texas, and understanding what drives Texas flood insurance costs is the first step toward protecting your property. Your location, home elevation, and building age all play major roles in determining your premiums.

We at Grimes Insurance Agency help homeowners navigate these costs and find ways to reduce them. This guide walks you through the factors affecting your rates and practical strategies to lower your premiums.

What Pushes Your Texas Flood Insurance Costs Higher

Texas flood risk has intensified significantly over the past decade, and your insurance costs reflect that reality. More than five million Texans live in flood-prone areas, and flood risk continues to rise as climate change brings heavier rainfall events and coastal erosion accelerates. Texas coastlines lose about four inches of land annually due to sea-level rise, which directly increases flood exposure inland and drives premiums upward. In 2025, neutral water conditions are expected to bring higher hurricane risk to Texas, meaning insurance carriers are pricing in greater likelihood of flood-related damage. This is not speculation-it is factual risk assessment that insurers use to calculate what you pay each year.

How Your Property Location and Elevation Shape Your Premium

Your exact address determines your flood insurance cost far more than any other factor. The National Flood Insurance Program uses Risk Rating 2.0, which calculates premiums based on property-specific characteristics rather than broad geographic zones. Foundation type, first-floor elevation relative to the Base Flood Elevation, distance to water sources, and building replacement cost all feed into your rate. A home elevated just one foot above the Base Flood Elevation can reduce annual premiums by up to 30 percent compared to a home at or below that level.

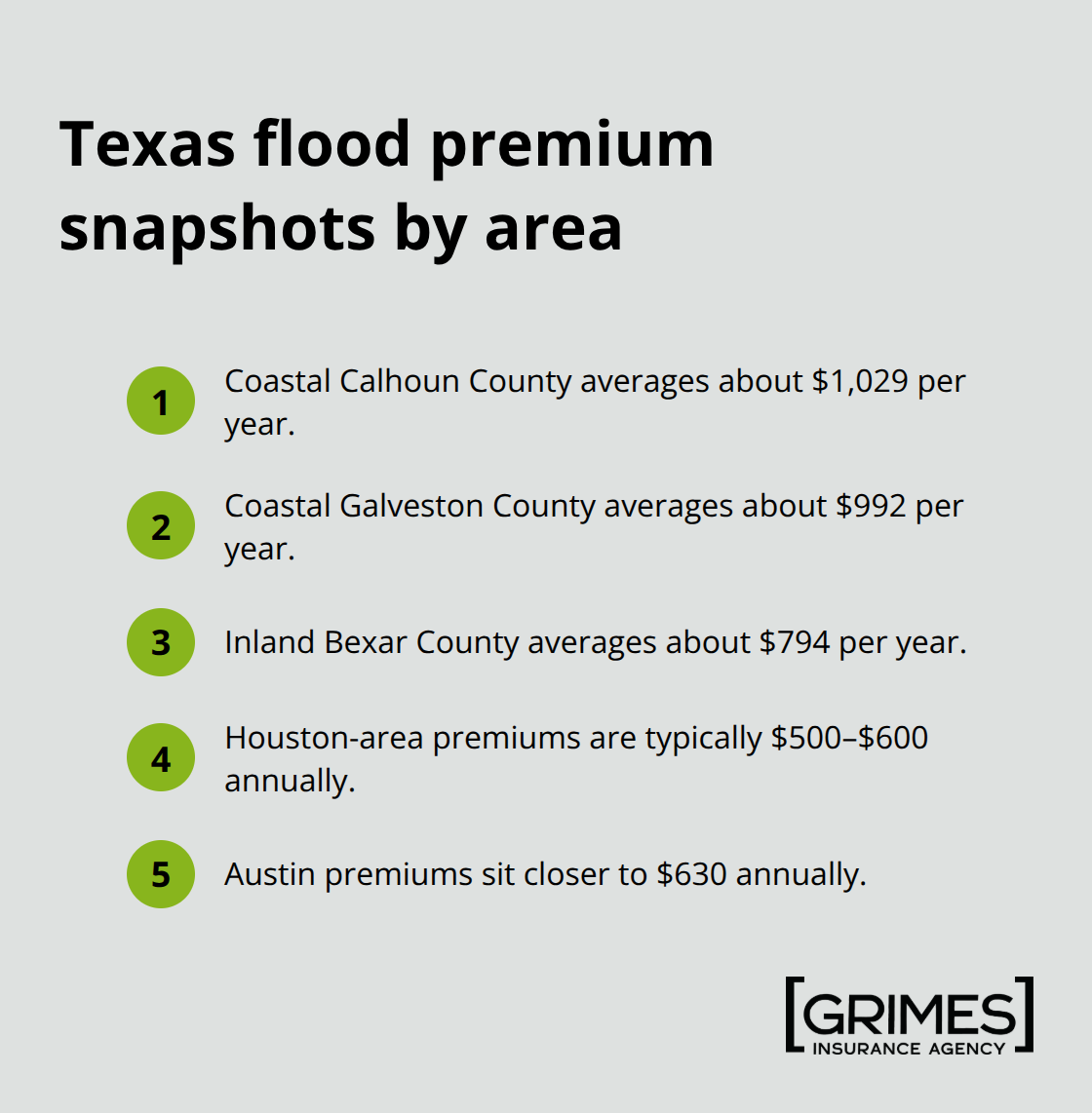

In Texas, coastal counties like Calhoun and Galveston average around 1,029 and 992 dollars per year respectively, while inland counties like Bexar average about 794 dollars per year. Houston-area premiums typically run 500 to 600 dollars annually, while Austin sits closer to 630 dollars. These differences exist because flood peril likelihood, building specifics, and distance to flood sources vary dramatically across the state.

Building Age and Construction Standards Impact Your Rate

Older homes consistently carry higher premiums because their construction methods and materials are more vulnerable to water damage. A basement in a flood zone raises premiums by roughly 15 to 20 percent due to increased flood risk and compliance requirements. Newer construction with flood-resistant features qualifies for lower rates under FEMA’s current rating methods.

The presence of proper flood vents can meaningfully lower your costs. An Elevation Certificate documents your property’s elevation and flood risk, informs mitigation actions, and can help lower premiums by accurately reflecting your building’s true risk profile. If your lowest floor sits below the Base Flood Elevation without an Elevation Certificate, expect premiums to be substantially higher.

What Comes Next: Taking Action on Your Costs

Your property’s characteristics lock in certain baseline costs, but you control several levers that directly reduce what you pay. The next section shows you exactly which mitigation steps produce the largest premium reductions and how to implement them effectively.

How to Cut Your Flood Insurance Premiums

Elevation Delivers the Biggest Savings

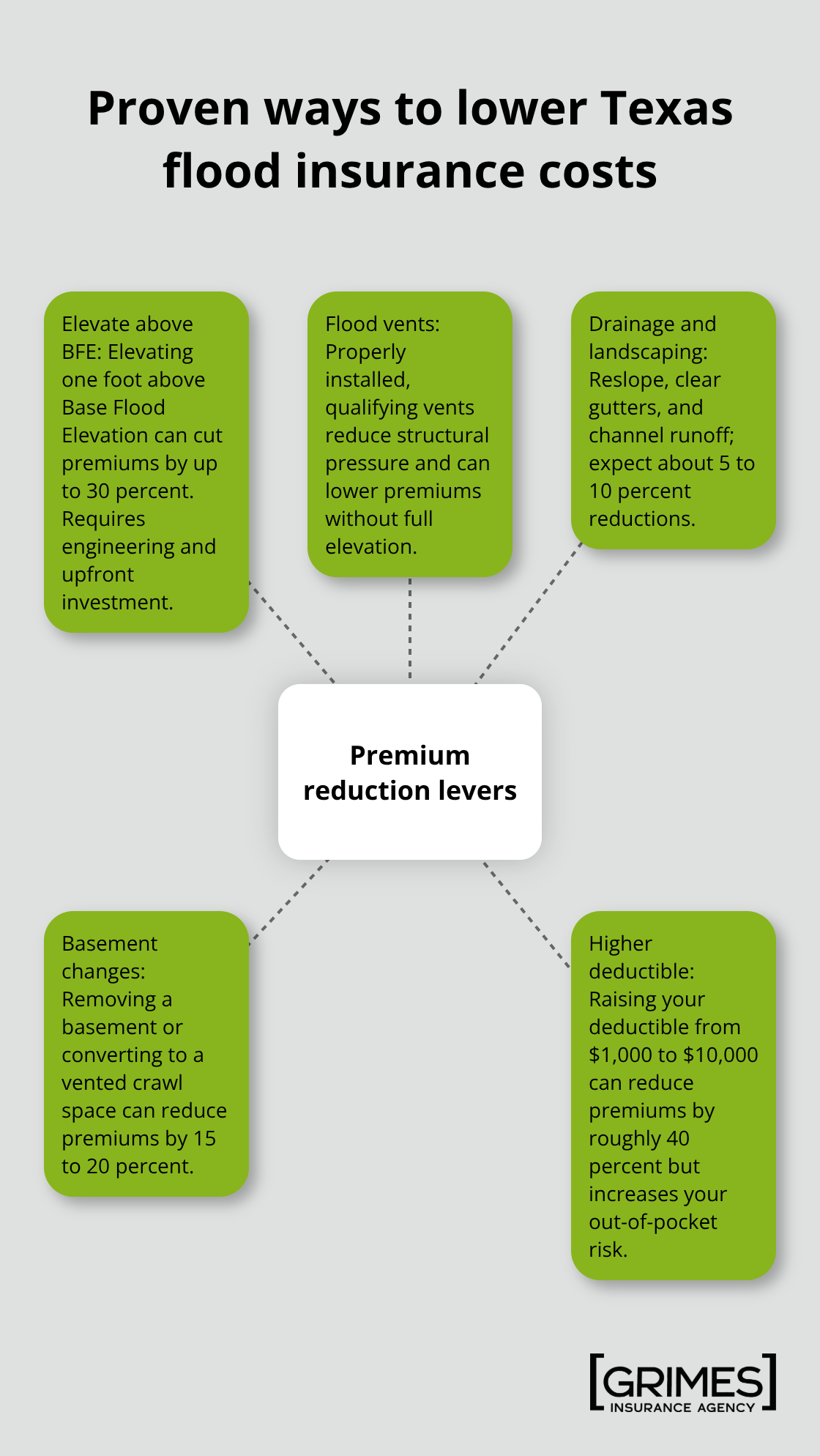

Elevating your home above the Base Flood Elevation produces the single largest premium reduction available to Texas homeowners. A one-foot elevation above Base Flood Elevation cuts annual premiums by up to 30 percent, according to NFIP guidance. For a Houston homeowner paying roughly 550 dollars annually, this translates to savings of 165 dollars per year. Full elevation of your structure requires professional engineering and construction, which costs money upfront, but the math works quickly when you factor in cumulative savings over five, ten, or fifteen years.

An Elevation Certificate documents your property’s exact elevation and becomes essential for claiming these discounts with your insurer. Many counties in Texas require this certificate before approving elevation work, so obtain one before starting any mitigation project.

Install Flood Vents When Elevation Isn’t Practical

If elevation feels too expensive or impractical, installing flood vents in foundation walls offers a meaningful alternative. Flood vents must meet specific criteria to qualify for premium reductions: at least 1 square inch of opening per square foot of enclosed area, at least two openings on two exterior walls, and the base of openings no higher than 12 inches above exterior grade. Garage doors and windows do not count as qualified vents.

When properly installed, flood vents allow floodwater to flow through your foundation rather than pushing against it, which reduces structural pressure and damage risk. This approach can lower premiums meaningfully without the expense of full elevation.

Drainage and Landscaping Changes Add Up

Proper drainage and landscaping changes cost far less than elevation but produce measurable results. Reslope ground away from your foundation, clear gutters and downspouts, and direct water toward street drainage to prevent pooling around your home during heavy rainfall. These actions alone rarely cut premiums by more than 5 to 10 percent, but they form the foundation for any comprehensive mitigation strategy.

Basement Elimination and Deductible Adjustments

If your home has a basement, eliminating it or converting it to a non-habitable crawl space with flood vents can reduce premiums by 15 to 20 percent, though this requires significant investment. Increasing your deductible from 1,000 dollars to 10,000 dollars reduces annual premiums by roughly 40 percent, but this strategy shifts risk to you rather than your insurer.

Combining Strategies for Maximum Impact

The best approach combines low-cost drainage improvements with either elevation or flood vents, then adjusts your deductible to match your financial capacity to absorb a loss. A licensed insurance agent can assess which mitigation steps make financial sense for your specific property, timeline, and budget. Once you understand which improvements fit your situation, the next step involves choosing between the National Flood Insurance Program and private flood insurance options-each carries different coverage limits, waiting periods, and cost structures that directly affect your total protection and out-of-pocket expenses.

NFIP vs. Private Flood Insurance: Which Works for Texas Homeowners

The National Flood Insurance Program dominates Texas because it offers the most accessible entry point for homeowners who need coverage quickly. NFIP policies cap dwelling coverage at $250,000 and contents at $100,000, which matches many Texas homes but falls short for properties worth significantly more. NFIP premiums in Texas average 879 dollars annually according to NFIP data, though your specific cost depends entirely on your property’s Risk Rating 2.0 factors. The program applies a mandatory 30-day waiting period before coverage activates, so purchasing now matters far more than waiting for storm season. NFIP policies pay claims based on actual cash value, meaning depreciation reduces what you receive after a loss.

How Depreciation Affects Your NFIP Payout

If your home suffers 50,000 dollars in flood damage but your roof was 15 years old, depreciation could cut your payout to 35,000 dollars or less. This gap between damage and reimbursement creates real financial risk that many homeowners underestimate. The actual cash value approach protects the insurer’s costs but leaves you responsible for the difference between what you receive and what reconstruction actually costs.

Private Flood Insurance Addresses NFIP’s Limitations

Private flood insurance addresses NFIP’s limitations directly. Private carriers offer higher coverage limits, often reaching 500,000 dollars or more for dwelling and contents combined. Critically, private policies frequently include replacement cost value coverage, which pays to rebuild without depreciation deductions. Private insurers also typically activate coverage in 5 to 7 days instead of 30, a meaningful advantage during hurricane season. Loss-of-use coverage through private insurers covers your living expenses if you must evacuate, something NFIP does not include.

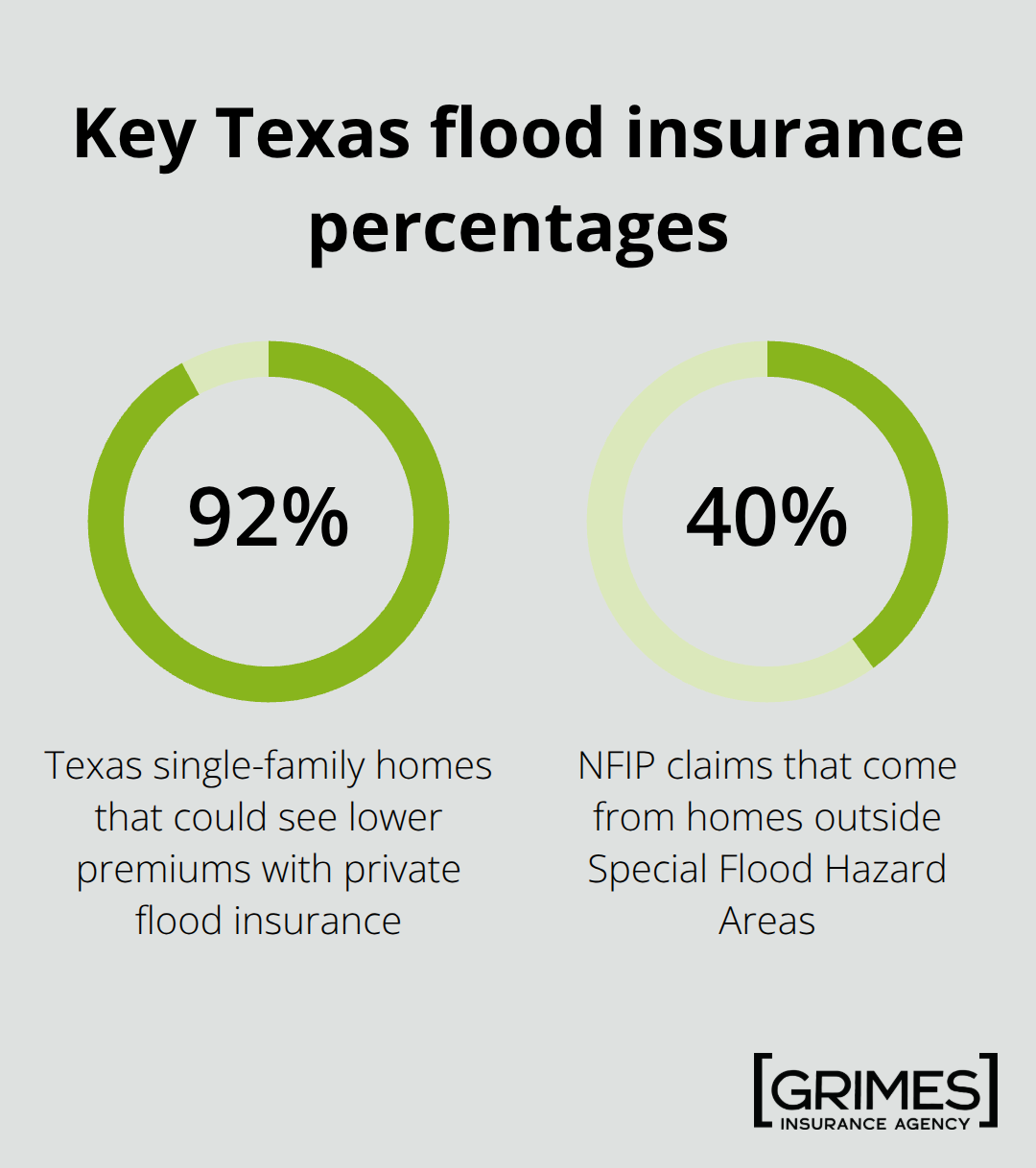

However, private insurers can decline renewal or cancel policies if they deem your property too high-risk after a major flood event, creating potential gaps in coverage. A 2017 Milliman study found that 92 percent of Texas single-family homes could qualify for lower premiums with private flood insurance compared to NFIP rates alone, yet most homeowners never compare quotes.

Combining NFIP and Private Coverage for Maximum Protection

The real advantage emerges when you combine both options strategically. Start with an NFIP policy to establish baseline coverage and satisfy mortgage lender requirements, then layer private flood insurance above NFIP limits to protect your full property value and access replacement cost benefits. This approach costs more upfront but eliminates the depreciation trap and covers your home’s true replacement cost. Obtaining quotes from both NFIP-participating agents and private flood carriers before committing to either program alone reveals which option fits your property and budget.

How Bundling and Flood Zone Status Affect Your Decision

Standard homeowners insurance never covers flood damage, so flood coverage remains completely separate from your primary home policy. Bundling flood insurance with your homeowners policy through the same carrier sometimes qualifies you for multi-policy discounts that reduce your total annual cost. Your lender requires flood insurance only if your property sits in a designated Special Flood Hazard Area, but 40 percent of NFIP claims come from homes outside these zones, proving that flood risk extends far beyond official high-risk maps. This reality makes flood insurance valuable regardless of your flood zone designation.

Final Thoughts

Texas flood insurance costs demand your attention because they reflect genuine risk to your property and finances. Location, elevation, building age, and your mitigation choices all determine what you pay annually, and understanding these factors puts you in control of your protection strategy. Whether you own your home outright or carry a mortgage, comparing NFIP and private options before purchasing prevents you from overpaying for inadequate protection.

Elevation, flood vents, and basement elimination produce the largest premium reductions, though they require upfront investment that pays dividends over time. Lower-cost improvements like drainage resloping and gutter maintenance form the foundation of any strategy, while increasing your deductible cuts premiums substantially if your financial situation allows it. An Elevation Certificate and assessment of your current deductible could unlock savings of hundreds of dollars per year without major construction.

We at Grimes Insurance Agency understand that navigating Texas flood insurance costs feels overwhelming when you face multiple quotes and coverage options. Our team works with multiple carriers to find you the best protection at the right price, whether that means NFIP coverage, private flood insurance, or a combination of both. Contact Grimes Insurance Agency to discuss your specific property, review your current coverage, and explore mitigation strategies that fit your budget and timeline.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation