Homeowners Insurance Texas Guide: What Homeowners Should Know

Homeowners insurance in Texas isn’t one-size-fits-all. Your coverage needs depend on where you live, what your home is worth, and the specific risks your property faces.

We at Grimes Insurance Agency help Texas homeowners navigate these decisions every day. This guide walks you through state requirements, policy types, and practical ways to save on premiums.

What Texas Homeowners Must Know About Insurance Requirements

Homeowners insurance in Texas isn’t legally mandated by the state, but your mortgage lender will require it before you close on your home. This requirement exists because lenders have a financial interest in protecting their investment. If your home burns down or suffers major damage and you have no insurance, the lender loses money. Most lenders demand replacement cost coverage, which means your dwelling coverage must be high enough to rebuild your home at current construction prices, not just match its market value. This distinction matters significantly in Texas, where rebuild costs have climbed sharply due to material inflation and labor shortages following severe weather events. If your coverage falls short of the rebuild cost, you’ll face a gap that your insurance won’t cover and your lender won’t accept.

Why Texas Premiums Rank Among the Nation’s Highest

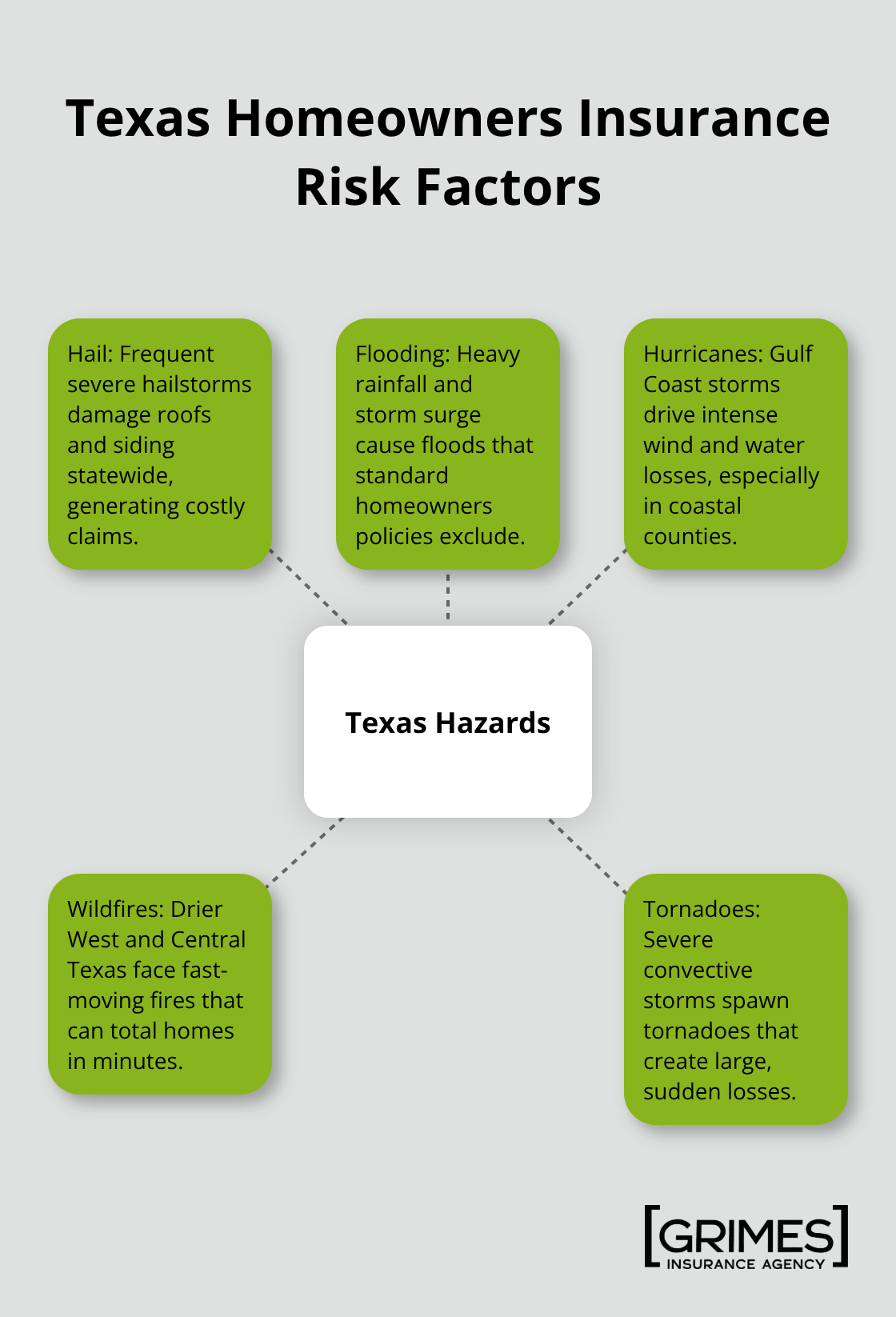

Bankrate’s 2026 data shows Texas ranks third nationally for highest homeowners premiums, averaging around $3,800 annually, with coastal areas pushing $4,500 or higher. This elevated cost reflects the state’s genuine hazards: hail damage, flooding, hurricanes, wildfires, and tornadoes all drive claims and premiums upward. Your specific location within Texas heavily influences what risks matter most and what coverage you actually need. The state’s weather patterns and construction costs create real exposure that insurers must price accordingly.

How Location Determines Your Real Coverage Needs

Coastal properties face hurricane and wind damage that inland homes don’t experience, making windstorm coverage either mandatory through a separate policy or provided by the Texas Windstorm Insurance Association for high-risk zones. West and Central Texas homeowners deal with severe hail and wildfire exposure that can total a home in minutes. Harris County and other coastal areas sometimes exclude wind damage entirely from standard policies, forcing you to purchase separate windstorm coverage.

Flood risk doesn’t follow standard homeowners policy boundaries. The National Flood Insurance Program covers flooding from heavy rainfall and storm surge, but standard policies exclude this completely. If you’re in a flood zone or have a mortgage, your lender will require flood insurance. Even if you’re outside a designated flood zone, flooding happens regularly in Texas during severe weather events, and many homeowners discover too late that their standard policy provides zero protection. Your zip code determines both your premium and the specific endorsements you must add to stay adequately protected.

How Building Age and Materials Affect Your Rate

Homes built before 1980 with original roofing materials and outdated electrical wiring carry significantly higher premiums because they present greater loss risk. A roof older than 20 years substantially increases your rate, while impact-resistant roofing materials and newer construction can reduce premiums by 10 to 15 percent. Brick or concrete block construction costs less to insure than wood frame homes in high-wind areas.

The materials your home is made from and the condition of critical components like your roof directly affect your insurability and price. This is actionable: upgrading to impact-resistant roofing or adding storm shutters can lower your premium while protecting your home from the hail and wind damage that Texas regularly experiences. These improvements address the specific threats your region faces and signal to insurers that you’ve taken steps to reduce loss potential.

Understanding these requirements and risk factors sets the foundation for selecting the right policy type. Texas offers several homeowners insurance options, each designed to address different coverage levels and property situations.

Policy Types That Match Texas Homeowners

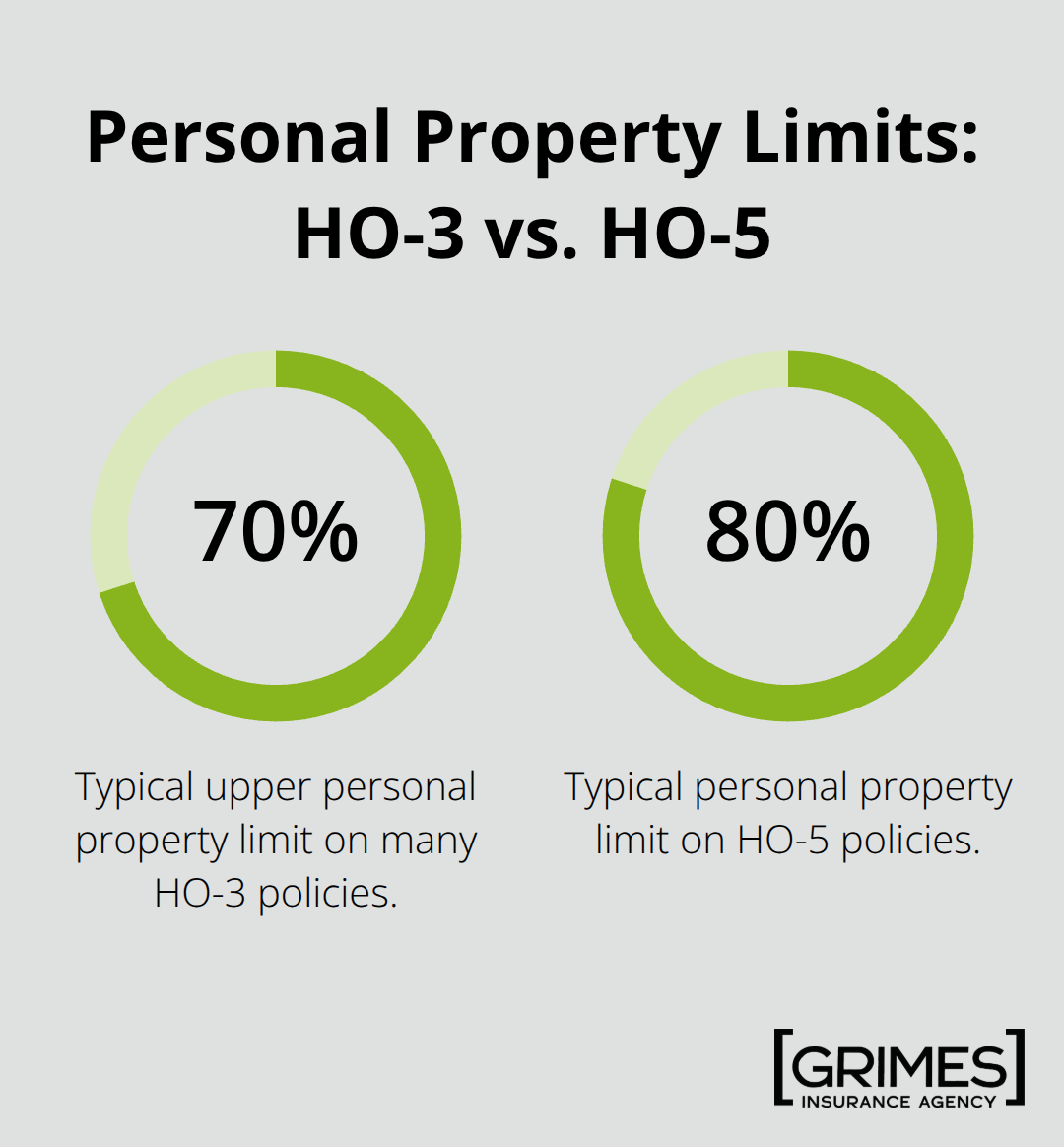

Most Texas homeowners carry an HO-3 policy, the standard form that covers dwelling, personal property, liability, and additional living expenses. An HO-3 provides open-peril coverage on your home structure, meaning damage from most causes is covered unless specifically excluded. Personal property coverage typically maxes out at 50 to 70 percent of your dwelling limit, which creates a real problem in Texas where hail and wind regularly destroy household contents. If your dwelling coverage is $300,000, your personal property limit sits at $210,000-often insufficient when a hail storm totals electronics, furniture, and appliances. You must calculate what your belongings actually cost to replace, not assume the standard percentage works. Wind and hail deductibles on HO-3 policies typically run 2 to 5 percent of dwelling coverage rather than a flat dollar amount, meaning a $500,000 home with a 2 percent deductible leaves you paying $10,000 out of pocket after a hail claim. This percentage deductible structure hits Texas homeowners harder than homeowners in other states because severe weather is routine here.

How HO-5 Policies Protect You Better in Texas

HO-5 policies eliminate the percentage deductible trap. They replace the percentage structure with a standard flat deductible that applies to wind and hail claims just like other losses. HO-5 also covers personal property on a replacement cost basis with higher limits, typically 80 percent of dwelling coverage instead of 70 percent.

If you own a home valued over $500,000, have significant personal property, or live in a high-hail or high-wind zone, an HO-5 justifies the premium difference. The flat deductible approach means you know exactly what you’ll pay out of pocket, and the higher personal property limits better match what Texas homeowners actually own.

When You Need Specialized Coverage

High-value homes and unique properties-those with custom construction, expensive finishes, or special systems-require specialized coverage that standard policies simply don’t address. Older homes with historical value, homes with detached structures, properties with home-based businesses, and residences with art collections or jewelry exceeding standard limits all need customized endorsements or dedicated policies. These properties present risks and values that HO-3 and HO-5 forms don’t fully capture. A specialized policy accounts for the specific characteristics of your home and protects assets that standard coverage leaves exposed.

Finding the Right Coverage for Your Property

An independent insurance agent can evaluate whether your property fits standard coverage or requires specialized protection. This assessment prevents you from paying for unnecessary coverage or facing denial when you file a claim. The next step involves comparing what different carriers offer and understanding how to select coverage amounts that actually protect your investment.

How to Calculate What Your Home Actually Costs to Rebuild

Start with a hard number, not an estimate. Your dwelling coverage must equal your home’s replacement cost at current Texas construction prices, not its market value. A $400,000 home in suburban Dallas might cost $550,000 to rebuild today because materials and labor have climbed sharply since 2021. The Texas Department of Insurance HelpInsure tool lets you input your home details and see sample replacement cost estimates from major carriers, providing you with a realistic baseline before you shop. Many homeowners underbuy coverage by $50,000 to $100,000, thinking market value and rebuild cost are the same-they discover the gap when filing a claim.

Your personal property limit deserves the same precision. Walk through your home and catalog what you actually own, not what you think you own. Furniture, electronics, clothing, tools, and kitchen items add up fast. If you own jewelry, art, or collectibles worth more than $2,500, those items hit coverage limits on standard policies and need separate endorsements. The Texas Windstorm Insurance Association website and your carrier’s appraisal tools help you document values. Once you know what you need to protect, comparing quotes becomes straightforward because you’re comparing identical coverage amounts across different carriers.

Shop for Quotes from Multiple Carriers

Get quotes from at least three carriers, not one or two. State Farm, Allstate, USAA for military families, Farmers, and Travelers all operate in Texas and offer different pricing on identical coverage. When you request quotes, specify the exact dwelling amount, personal property limit, deductible, and any endorsements you need like flood or windstorm coverage. Ask each carrier about their wind and hail deductible structure, because this varies significantly and impacts your out-of-pocket costs after a storm. A 2 percent wind deductible on $500,000 dwelling coverage means you pay $10,000 after hail damage, while a flat $1,500 deductible saves you money.

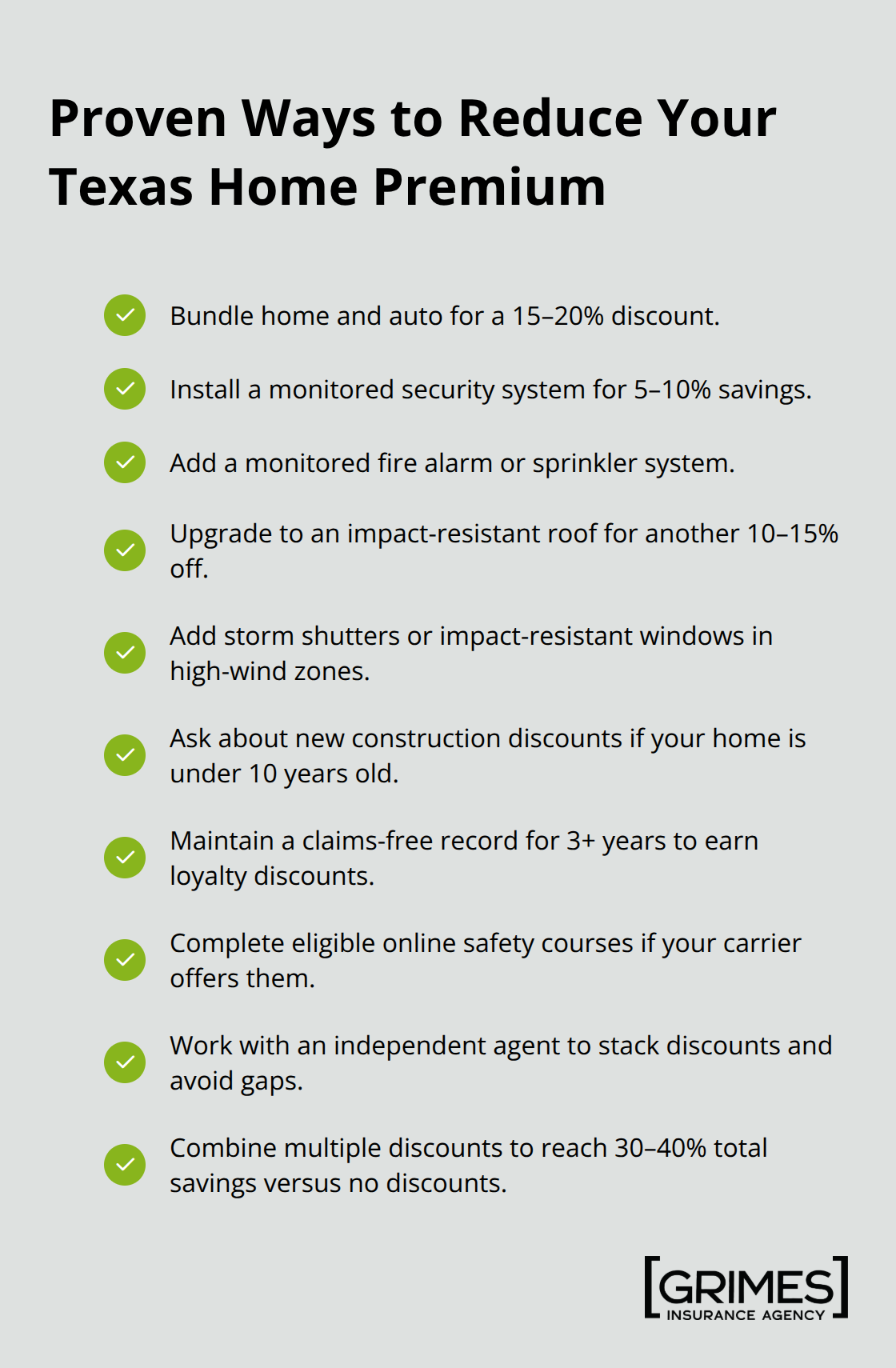

Bundling home and auto insurance typically reduces your home premium by 15 to 20 percent according to industry data, so always quote both policies together. Verify that you’re comparing replacement cost coverage, not actual cash value, because lenders require it and actual cash value leaves you underprotected. A local independent agent can pull quotes from multiple carriers simultaneously and ensure you’re comparing apples to apples, saving hours of phone calls and preventing mistakes. The premium difference between carriers for identical coverage often exceeds $500 annually, making shopping worth your time.

Unlock Discounts That Lower Your Rate

Install a monitored security system if you don’t have one. This single upgrade typically reduces your premium by 5 to 10 percent because it lowers theft and break-in claims. A monitored fire alarm or sprinkler system provides additional discounts. Upgrade your roof to impact-resistant materials rated for hail, and your premium drops another 10 to 15 percent.

In Texas, this isn’t optional thinking-it’s practical economics because hail damage happens regularly. Add storm shutters or impact-resistant windows in high-wind zones, and carriers reward you further.

If your home is newer than ten years old, ask about new construction discounts. A claims-free history over three years qualifies you for loyalty discounts that compound with other reductions. Some carriers offer discounts for completing online safety courses or bundling multiple policies. The combination of bundling, security system installation, and a good claims history can reduce your premium by 30 to 40 percent compared to a basic policy with no discounts.

Choose Your Deductible Wisely

Higher deductibles lower premiums, but only increase your deductible if you can comfortably pay it out of pocket after a loss. A $2,500 deductible saves more premium than a $1,000 deductible, but you must have that cash available when you file a claim, or you’ll face financial stress precisely when your home needs repairs. Your deductible choice directly affects both your monthly payment and your financial readiness for a claim.

Final Thoughts

Texas homeowners insurance requires action, not passive understanding. You now know that replacement cost coverage must match current rebuild prices, not market value, and that location determines which risks matter most for your specific property. Shopping multiple carriers for identical coverage typically saves $500 to $1,000 annually, while bundling home and auto policies cuts premiums by 15 to 20 percent.

Calculate your home’s actual replacement cost using the Texas Department of Insurance HelpInsure tool, then request quotes from at least three carriers with exact coverage amounts and deductibles specified. Ask about bundling discounts, security system credits, and roof upgrade incentives-these reductions compound to lower your premium significantly. A local independent agent accesses multiple carriers simultaneously and understands county-specific risks that online quotes miss, saving you hours while preventing costly mistakes.

We at Grimes Insurance Agency have spent over 75 years helping Texas homeowners navigate these decisions and find coverage that protects their investment. Contact Grimes Insurance Agency to discuss your specific situation with agents who understand Lubbock and the surrounding region. Your home is your largest investment, and protecting it with the right coverage at the right price matters.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation