Texas Homeowners Insurance Basics: Essentials For Local Residents

Texas homeowners face unique insurance challenges that most homeowners in other states don’t encounter. From hurricanes to hail storms, the weather alone makes adequate coverage non-negotiable.

At Grimes Insurance Agency, we help local residents understand the Texas homeowners insurance basics they need to protect their homes and finances. This guide walks you through coverage types, how to choose the right policy, and why regular reviews matter.

Why Texas Homeowners Can’t Skip Insurance

Texas homeowners operate in a high-stakes insurance environment that makes skipping coverage financially reckless. The state sits directly in the path of hurricanes, experiences hail storms that cause billions in damage annually, and faces flash flooding that strikes without warning. Your home represents the largest asset most people own, yet many Texas residents either underinsure or skip coverage entirely because they misunderstand what actually happens when disaster strikes.

Your Home Faces Real Weather Threats

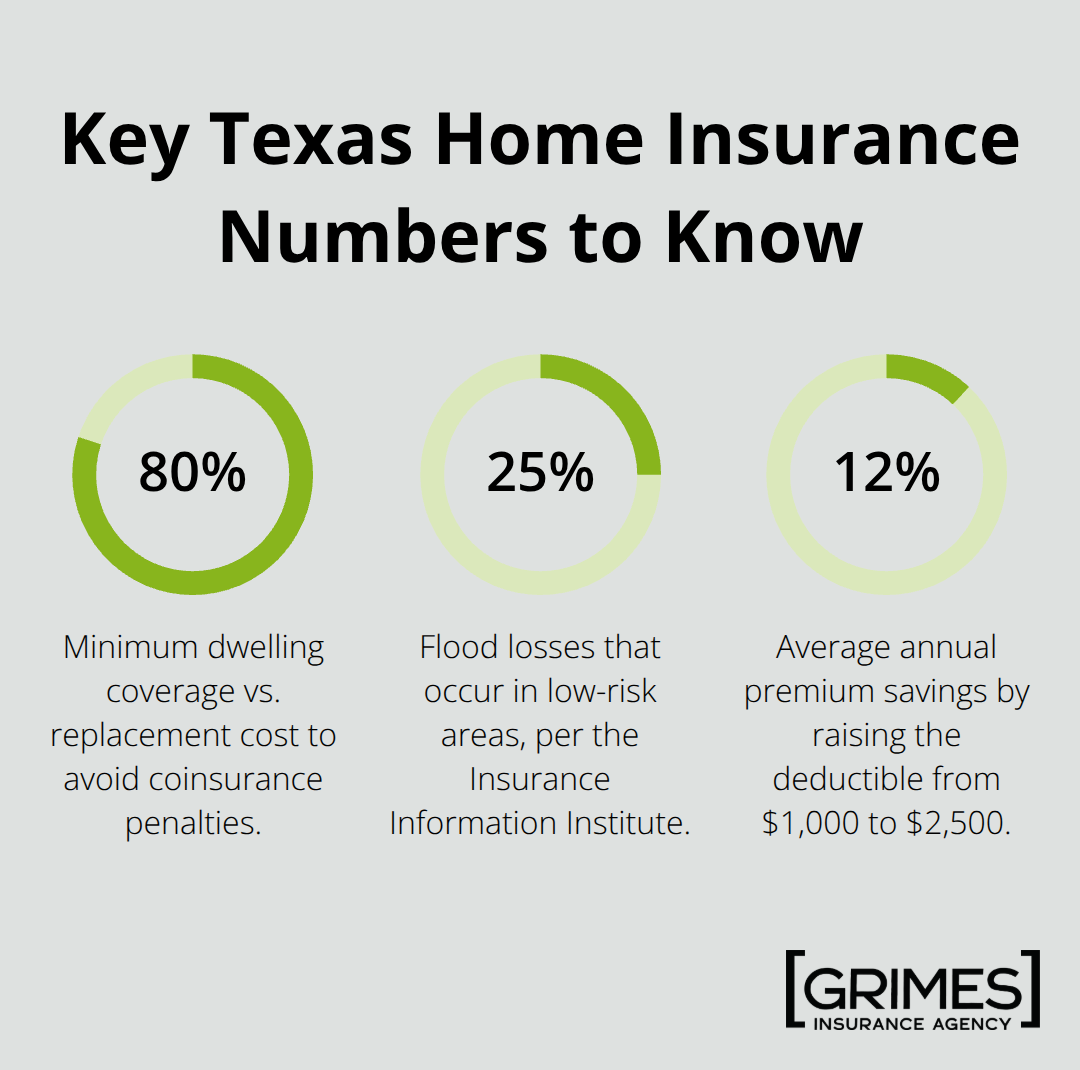

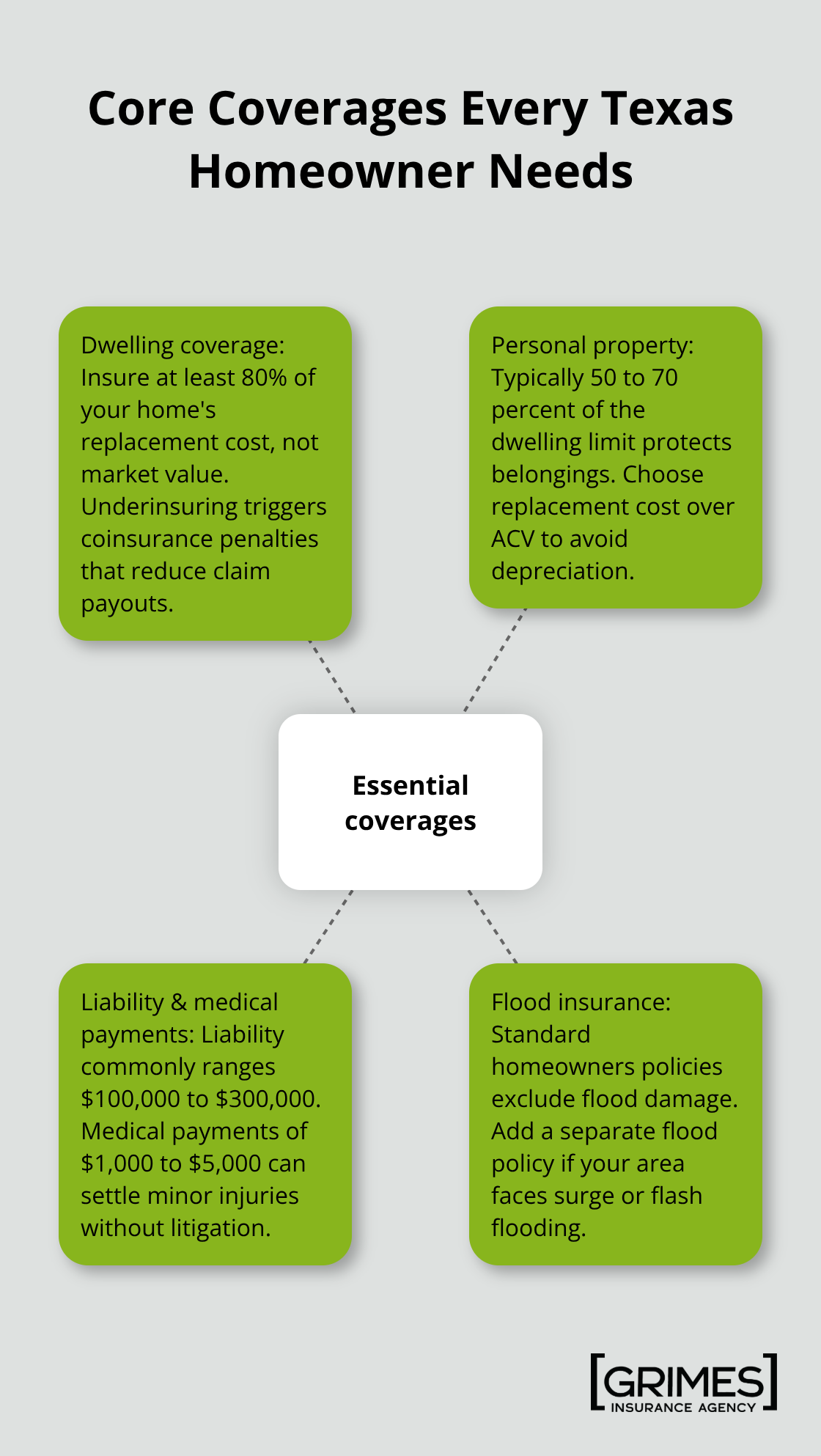

Texas weather doesn’t just damage roofs and siding. Hail storms in the Panhandle and North Texas regularly produce stones the size of baseballs that total vehicles and shatter skylights. Gulf Coast residents deal with storm surge and wind speeds exceeding 150 mph during major hurricanes. Inland areas face flash flooding that can total a home in minutes, and standard homeowners policies don’t cover flood damage at all. The Insurance Information Institute reports that about 25 percent of flood losses occur in low-risk areas, meaning your location alone doesn’t determine your exposure. If your mortgage lender required flood insurance as a condition of your loan, that’s a clear signal your property sits in a vulnerable zone.

Without proper coverage, a single hail storm or flooding event can wipe out your entire net worth, leaving you personally liable for reconstruction costs that often exceed $300,000 to $450,000 for a typical Texas home.

Liability Claims Can Destroy Your Finances

Someone gets injured on your property, sues you, and suddenly you face legal bills and medical costs that dwarf your annual income. A slip-and-fall claim from a guest, a dog bite incident, or a neighbor’s child injured in your pool can easily exceed $100,000 in damages. Without liability coverage, the judgment comes directly from your personal assets, your bank accounts, and potentially your future wages. Texas courts award significant damages in personal injury cases, and a single verdict can bankrupt you even if you own your home outright. Your mortgage lender requires homeowners insurance specifically because they understand this risk. Lenders know that an uninsured home threatens their collateral, so they mandate coverage as a condition of the loan. This requirement exists to protect both you and the lender from catastrophic loss.

Understanding Your Lender’s Requirements

Most mortgage lenders won’t close on a home without proof of active homeowners insurance. The lender’s name typically appears on your policy as a loss payee, which means they receive notice if your coverage lapses or if you cancel the policy. Lenders set minimum coverage amounts based on the home’s value and loan amount, and these minimums often fall short of what you actually need to rebuild. Your lender cares about protecting their investment in your property, not about your complete financial security. This gap between what lenders require and what you truly need is where many Texas homeowners make costly mistakes. Understanding this distinction helps you make informed decisions about coverage levels that actually protect your wealth.

What Coverage Do You Actually Need in Your Texas Home

Dwelling Coverage Sets Your Financial Foundation

Dwelling coverage forms the foundation of any Texas homeowners policy, and this is where most residents make their first critical mistake. Your dwelling coverage should equal at least 80 percent of your home’s replacement cost, not its market value or what you paid for it years ago. A typical Texas home costs between $300,000 and $450,000 to rebuild from scratch when you factor in labor, materials, and current construction prices. If your home would cost $400,000 to rebuild but you only insure it for $300,000, your insurer will apply coinsurance penalties that reduce claim payouts proportionally, leaving you to cover the gap from your own pocket.

The Insurance Information Institute recommends hitting that 80 percent threshold specifically to avoid this trap. Work with a contractor or use region-specific online calculators to determine your actual replacement cost, then add 10 to 15 percent for inflation since rebuilding takes time and prices shift. This single decision determines whether a major loss leaves you financially whole or devastated.

Personal Property Coverage Protects What’s Inside

Personal property coverage protects your belongings inside the home, and it typically caps out at 50 to 70 percent of your dwelling limit. For a $400,000 home, that means roughly $200,000 to $280,000 in coverage for everything inside: furniture, electronics, clothing, kitchenware, and all other contents. Most households drastically underestimate what they own until they actually inventory room by room and discover a three-bedroom home easily contains $100,000 to $150,000 in items.

Choose replacement cost coverage for personal property rather than actual cash value, which depreciates items and leaves you with pennies on the dollar after a loss. Replacement cost costs 10 to 15 percent more annually but provides dramatically better protection when you need it. For high-value items like jewelry, art, or collectibles, scheduled endorsements with current appraisals protect you against sublimits that standard coverage imposes.

Liability and Medical Payments Shield Your Assets

Liability and medical payments coverage rounds out the essential protections by covering injuries someone else sustains on your property. Liability coverage typically ranges from $100,000 to $300,000 in coverage, and this is your financial shield against slip-and-fall claims, dog bite incidents, or pool accidents that result in lawsuits. Medical payments coverage, usually $1,000 to $5,000, pays a neighbor’s minor medical expenses without requiring them to sue you, which often prevents small incidents from escalating into major claims.

Texas courts award substantial damages in personal injury cases, so adequate liability limits protect your home, savings, and future wages from a single catastrophic claim. The gap between what lenders require and what you truly need becomes even more apparent when you consider liability exposure. Your policy limits should reflect the real risks your property presents and the assets you have to protect.

Picking the Right Policy Without Overpaying

Calculate Your True Replacement Cost

Start with your home’s actual rebuild cost, not what you paid for it or what it would sell for today. Contact a local contractor and request a rebuild estimate that includes labor, materials, permits, and current pricing in your area. If a contractor estimate proves difficult to obtain, the Replacement Cost Estimator from the National Association of Insurance Commissioners can help. Once you have that number, multiply it by 0.80 to find your minimum dwelling coverage target. A $400,000 rebuild cost means you need at least $320,000 in dwelling coverage to avoid coinsurance penalties. Add 10 to 15 percent more to account for inflation during the months your home gets rebuilt, since prices shift between now and when you actually file a claim.

Document Your Personal Property

Create a detailed room-by-room inventory of your belongings with photos, dates of purchase, and estimated replacement values. This inventory prevents the underinsurance trap that catches most Texas homeowners. Your inventory becomes your claim documentation if disaster strikes and serves as proof of what you owned before the loss.

Compare Quotes from Multiple Carriers

Gather quotes from at least three carriers using identical coverage limits and deductibles so you can compare quotes without overpaying. Get quotes from both independent agents and direct carriers, since independent agents can access multiple companies while direct carriers show you only their own rates. A typical Texas homeowner with $300,000 in dwelling coverage pays around $2,110 annually, but rates vary dramatically between carriers-Travelers and USAA often come in cheaper depending on your eligibility, while other carriers charge significantly more for identical coverage.

Verify Financial Strength and Adjust Deductibles

Before committing to any carrier, verify their financial strength through A.M. Best or S&P ratings, since a low premium means nothing if the company can’t pay claims after a major disaster. Raise your deductible from $1,000 to $2,500 if you can afford the out-of-pocket hit after a loss, since this single move typically saves about 12 percent on annual premiums according to NerdWallet.

Stack Discounts Aggressively

Bundling homeowners with auto insurance yields 5 to 10 percent savings, maintaining a claims-free history saves another 5 to 15 percent, and installing monitored burglar alarms or sprinkler systems earns additional discounts. Paying your annual premium upfront rather than monthly installments often saves another 5 to 10 percent. These discounts compound quickly when you apply them strategically across your coverage options.

Final Thoughts

Texas homeowners insurance basics rest on three core principles: insure your dwelling for at least 80 percent of its replacement cost, select replacement cost coverage for your belongings, and maintain liability limits that protect your actual assets. Most Texas residents make costly mistakes by underinsuring their dwelling, skipping flood coverage, or choosing actual cash value to save a few dollars monthly-a false economy that costs thousands when claims fall short. Your next step involves gathering quotes from multiple carriers with identical coverage limits and deductibles so you can compare rates without overpaying.

Annual policy reviews matter because your home’s replacement cost rises with inflation, your belongings accumulate over time, and your liability exposure shifts as your life changes. Review your policy every year or after major life events like home renovations, purchasing expensive items, or significant property changes. Verify financial strength ratings before committing to any carrier, raise your deductible if you can afford the out-of-pocket cost, and bundle your homeowners policy with auto insurance to stack discounts that compound quickly.

We at Grimes Insurance Agency help Texas residents navigate these decisions with access to multiple carriers and local expertise. Contact us to review your current coverage and confirm your policy actually protects what matters most.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation