Business Insurance Planning for Entrepreneurs: Essential Steps for Success

Running a business means facing risks you might not expect. At Grimes Insurance Agency, we’ve helped countless entrepreneurs navigate business insurance planning by identifying gaps in their protection.

The right coverage protects your assets, your employees, and your bottom line. This guide walks you through the essential steps to build an insurance strategy that actually fits your business.

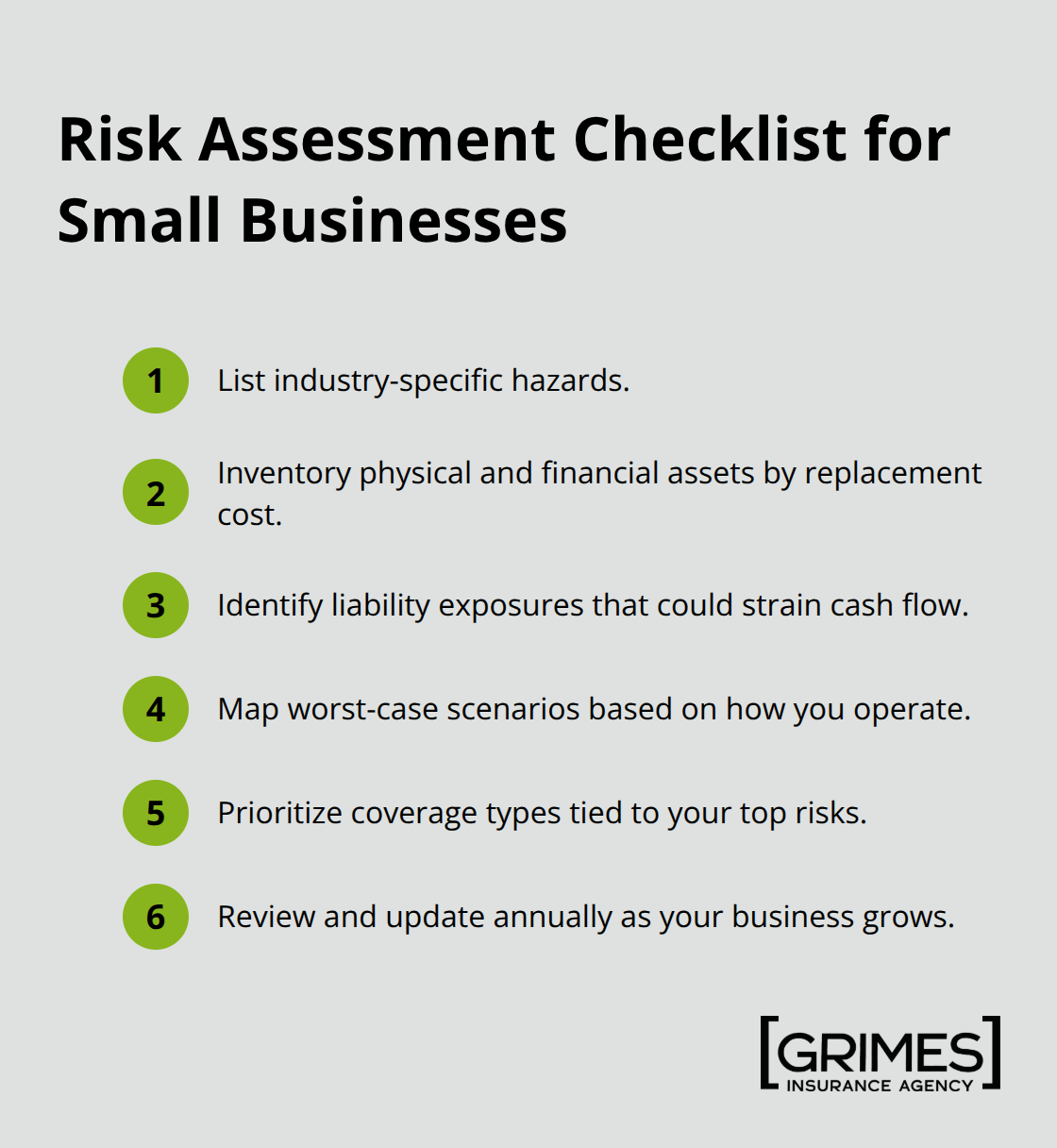

Assess Your Business Risks and Insurance Needs

Start by mapping what could actually hurt your business financially. This means listing the specific hazards tied to your industry, the physical and financial assets you’d struggle to replace, and the liabilities that could drain your cash flow or force you to shut down. Your risk assessment should identify worst-case scenarios specific to how you operate. A retail shop faces different threats than a consulting firm. A contractor with equipment and employees faces different exposure than a home-based service business. Ask what would happen if a customer got injured on your premises, if your inventory burned down, if a client sued you for errors in your work, or if a key employee couldn’t work.

These scenarios point directly to the types and amounts of coverage you actually need.

What Your Industry Exposes You To

Retail businesses need strong property coverage because inventory represents real dollars sitting in a building vulnerable to fire, theft, and weather. Service providers like accountants, consultants, and contractors need professional liability coverage because a mistake or negligence claim can cost thousands in legal fees and settlements. Manufacturers and product sellers need product liability protection because a defective item causes injury, triggering expensive claims. Contractors and trades need workers’ compensation because injuries on job sites happen regularly and state law often requires it. Your specific industry determines which coverages matter most. Don’t purchase insurance based on what another business uses-purchase based on what actually threatens yours. A local independent agent understands regional risks and industry-specific exposures that generic online quotes miss.

Evaluate Your Assets and Liabilities

Calculate your business assets honestly. List equipment, vehicles, inventory, and fixtures at what it would cost to replace them today, not what you paid years ago. Property coverage should match your actual asset value-the replacement cost of your building, equipment, inventory, and tools. Underinsuring saves premium money today but leaves you exposed; overinsuring wastes money. For workers’ compensation, payroll determines your premium, and most states require it if you have employees.

Determine Coverage Amounts Based on Business Size

Coverage amounts should reflect what you’d realistically need to pay out of pocket or what would force closure. A $1 million general liability limit makes sense for a business with high customer traffic and significant injury risk. A $500,000 limit might work for a small service business with minimal physical exposure. Small home-based operations typically need lower limits than established retail locations with dozens of daily customers. As your business grows and adds staff or equipment, your coverage amounts need to grow with it. Annual reviews catch gaps that emerge as your business changes. This ongoing assessment prevents the costly mistake of outgrowing your protection without realizing it.

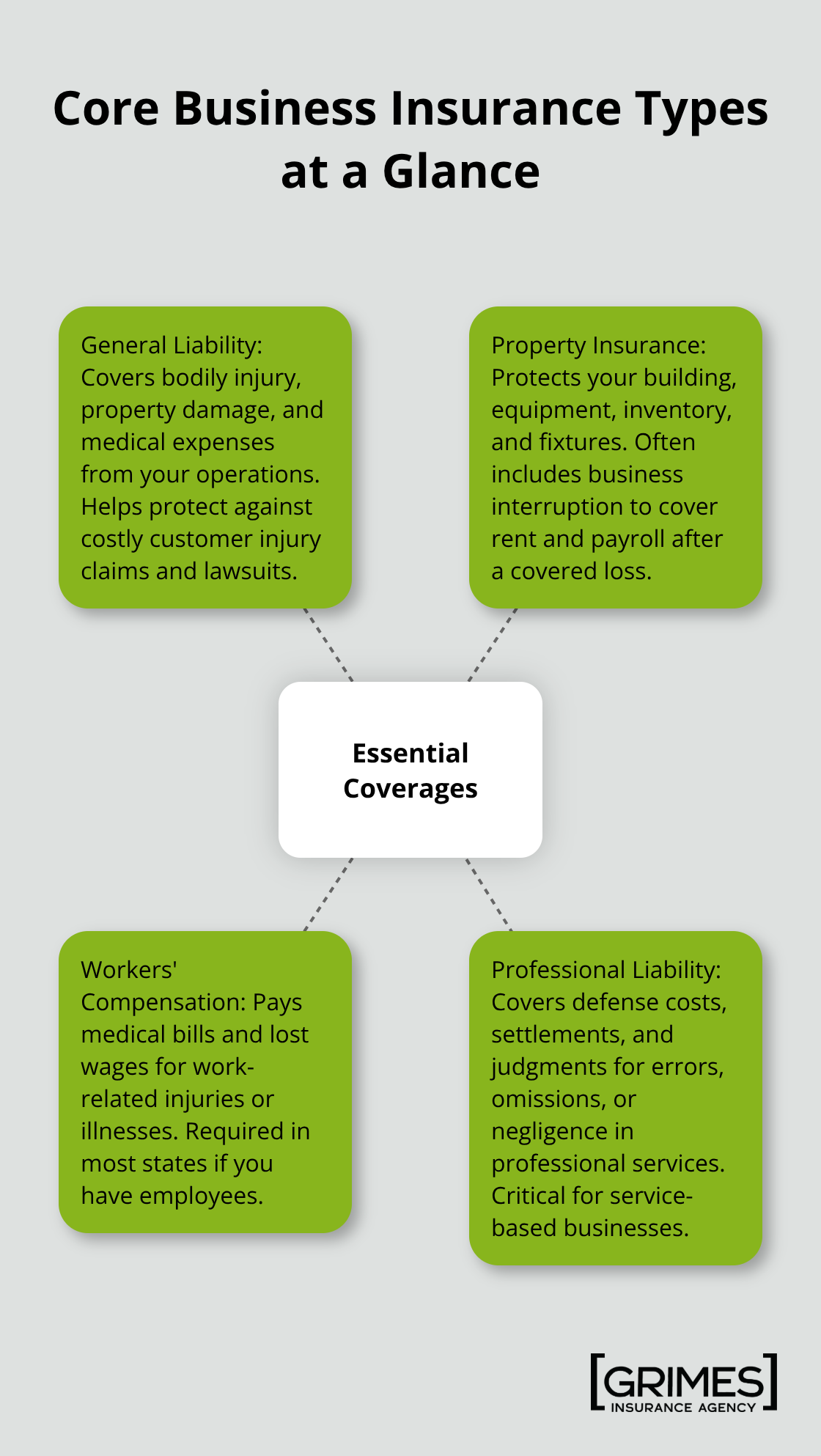

Types of Business Insurance Every Entrepreneur Should Consider

General Liability Insurance Protects Against Customer Claims

General liability insurance is non-negotiable for any business that interacts with customers or the public. This coverage pays for bodily injury, property damage, and medical expenses when someone gets hurt or their property is damaged because of your business operations. If a customer slips in your retail space and breaks an arm, general liability covers their medical bills and any lawsuit settlement. A $1 million general liability limit costs far less than defending even one serious claim out of pocket.

Property Insurance Safeguards Your Physical Assets

Property insurance protects the physical assets that keep your business running-your building, equipment, inventory, and fixtures. Fire destroys inventory or a storm damages your roof, and property insurance pays to rebuild or replace what you lost. Retail businesses and manufacturers should prioritize this coverage because inventory represents significant capital tied up in a single location. Property coverage also includes business interruption protection, which covers rent and payroll during the time your business cannot operate after a covered loss. This protection helps you survive the gap between disaster and reopening.

Workers’ Compensation Covers Employee Injuries

Workers’ compensation insurance is legally required in most states if you have employees, and it covers medical expenses and lost wages when an employee gets injured or becomes ill from work. This coverage also protects you from employee lawsuits over workplace injuries.

Professional Liability Shields Service-Based Businesses

Professional liability insurance, also called errors and omissions insurance, protects service-based businesses from claims that your work caused financial loss or harm to a client. Accountants, consultants, attorneys, contractors, and designers all face exposure to negligence claims when clients believe professional mistakes caused them damage. Unlike general liability, which covers bodily injury and property damage, professional liability specifically covers the cost of defending yourself against claims that your professional services failed to meet standard care. The coverage also includes settlement costs and judgments.

Scaling Coverage as Your Business Grows

As your business grows and you add employees, your coverage amounts and types need to expand as well. A home-based solo consultant needs lower limits than an established firm with multiple staff members handling client work. Your next step involves selecting the right insurance provider-one that understands your industry and can match you with carriers offering the protection your business actually needs.

How to Choose the Right Business Insurance Provider

Finding the right insurance provider matters more than most entrepreneurs realize. Online quote tools and national carriers offer convenience, but they often miss industry-specific risks and leave coverage gaps. A local independent agent understands regional hazards-flooding in coastal areas, wildfire exposure in certain regions, or industry-specific liability patterns in your market-that national carriers overlook. Independent agents also access multiple carriers rather than steering you toward one company’s limited product line.

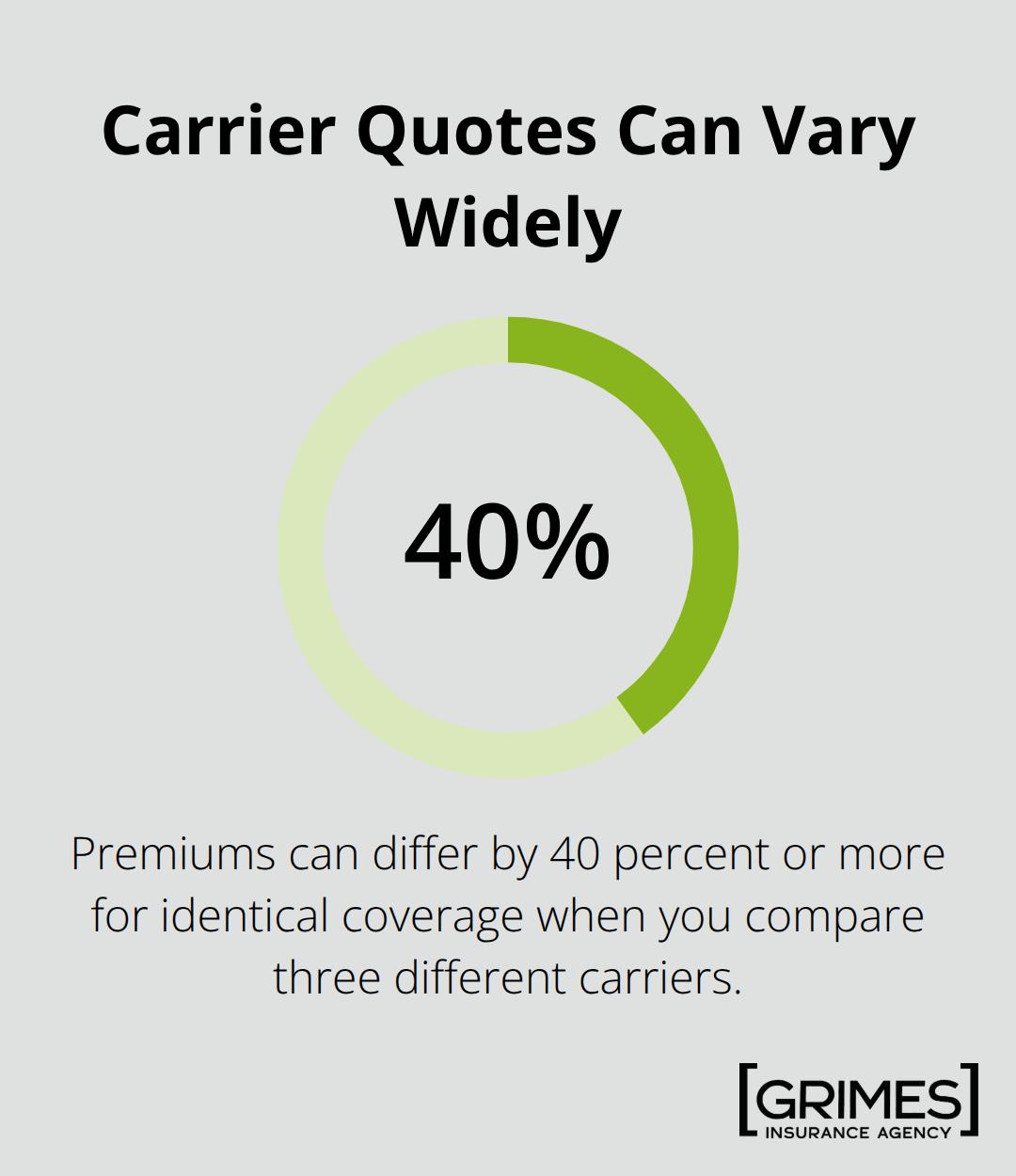

Compare Rates Across Multiple Carriers

When you shop with three different carriers for the same business, premiums can differ by 40 percent or more for identical coverage. An agent who represents multiple companies can show you these differences and explain what you’re actually paying for, not just the lowest price.

This matters because rates and available coverage vary significantly between insurers. Ask potential agents whether they represent one carrier or multiple carriers-the answer tells you whether they work to serve you or a specific company’s interests.

Verify Financial Strength and Claims Support

Financial stability of your insurance carrier matters when you actually need to file a claim. Before signing with any provider, check the insurer’s financial strength ratings through A.M. Best or Standard & Poor’s, which rate how likely an insurance company is to pay claims. You want A-rated or better carriers that have demonstrated ability to handle claims quickly.

When you evaluate an agent, ask directly about their claims support process. Do they handle the claims process with you, or do you contact the carrier alone? A good agent acts as your advocate during claims, helping coordinate between you and the insurer, explaining coverage limits, and pushing for faster resolution. Request references from existing clients and ask specifically about their claims experience, not just general satisfaction. An agent who has handled claims successfully for similar businesses in your industry brings valuable experience.

Select an Agent Who Understands Your Industry

A consultant’s liability insurance exposure looks completely different from a contractor’s or a retailer’s. If an agent recommends identical coverage to every small business regardless of industry, that’s a red flag. The right provider asks detailed questions about your operations, your customer base, your equipment and inventory, and your growth plans before making recommendations (this conversation should take at least 30 to 45 minutes for a thorough assessment). Quick quote processes feel efficient but typically mean coverage gaps you’ll discover too late. During your evaluation, also confirm that the agent understands your specific industry and can match you with carriers offering the protection your business actually needs.

Final Thoughts

Business insurance planning for entrepreneurs isn’t a one-time task you complete and forget-it’s an ongoing process that protects your investment, your employees, and your ability to recover when unexpected events strike. The steps outlined in this guide give you a framework to build protection that actually matches your business, not generic coverage that leaves gaps. A single lawsuit, property damage, or employee injury claim can exceed hundreds of thousands of dollars, while business interruption from a disaster forces many small businesses to close permanently.

Start by assessing your specific risks, mapping your industry hazards, calculating your asset values, and determining realistic coverage amounts based on your business size and growth trajectory. Then evaluate the four core insurance types that most entrepreneurs need: general liability to cover customer claims, property insurance to protect your physical assets, workers’ compensation to cover employee injuries, and professional liability if you provide services. Finally, choose an insurance provider who understands your industry and represents multiple carriers rather than pushing one company’s limited options.

At Grimes Insurance Agency, we’ve spent over 75 years helping entrepreneurs in Lubbock and beyond build insurance strategies tailored to their actual risks. As an independent agency, we access multiple carriers to find you the best protection at competitive rates, and we understand that your business is unique and deserves coverage that reflects your specific operations and growth plans. Contact Grimes Insurance Agency today to discuss your coverage needs and get started protecting what you’ve built.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation