What is Commercial Property Insurance in 2025? Key Insights for Business Owners

Your business faces real risks every day. From severe weather to theft, unexpected events can devastate your operations and finances.

We at Grimes Insurance Agency help business owners understand what is commercial property insurance in 2025 and why it matters for protecting your assets. This guide covers the coverage you need, current market trends, and how to find the right protection for your specific situation.

What Commercial Property Insurance Covers in 2025

Commercial property insurance protects three distinct areas of your business, and understanding what falls under each one matters because underinsurance in any category can cripple your operation.

Building Structure and Permanent Fixtures

The first layer covers your building structure itself-the walls, roof, foundation, and permanent fixtures like HVAC systems, electrical wiring, and plumbing. If your business owns the building, this protection is essential. If you lease, your landlord’s policy covers the structure, but you still need coverage for improvements you’ve made to the space.

Business Personal Property and Equipment

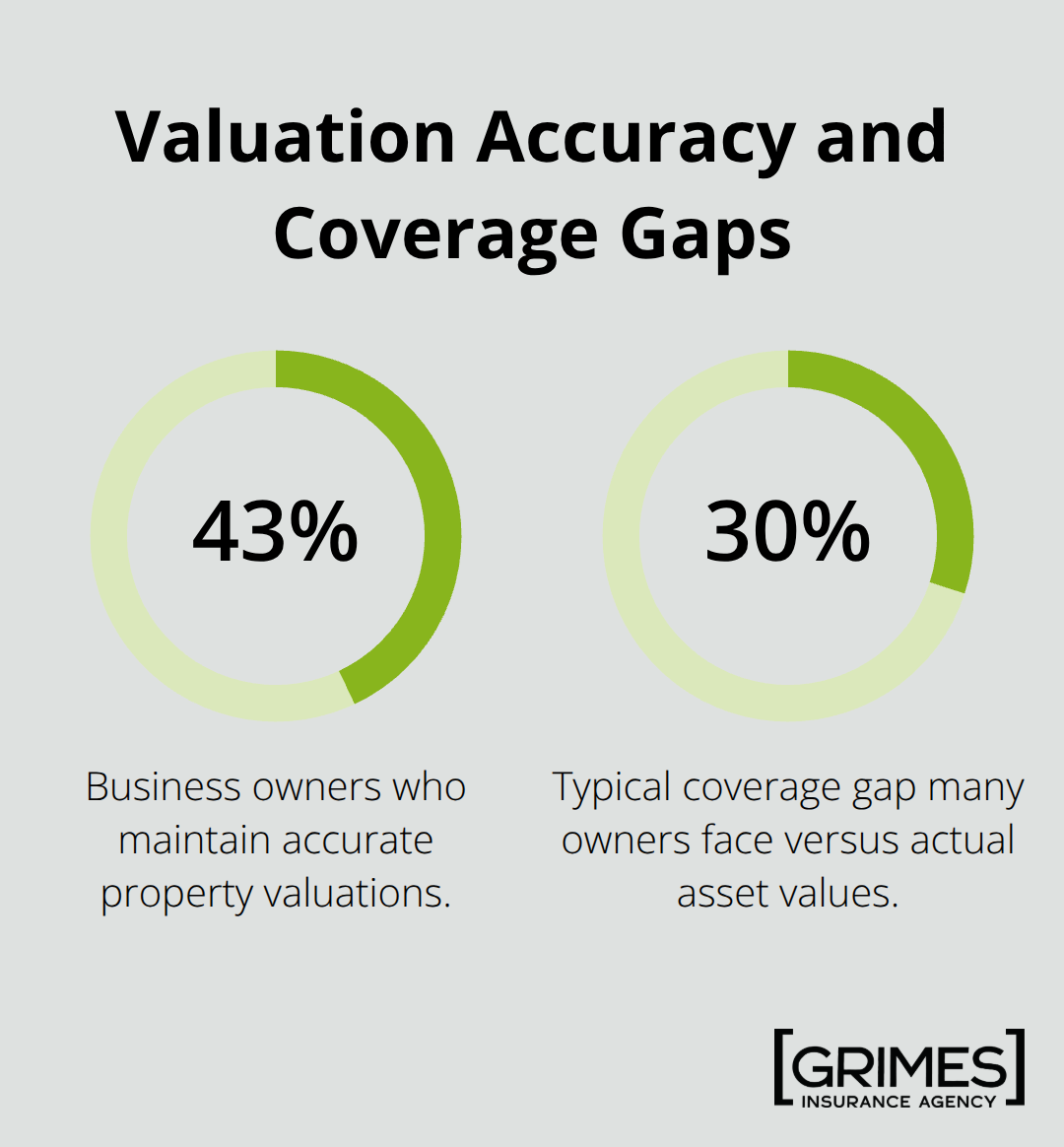

The second layer protects business personal property and equipment: all the items you could theoretically pack up and move if your business relocated. This is where most business owners face a serious problem. Only 43% of business owners maintain accurate property valuations, which means many operate with coverage gaps exceeding 30% of their actual asset values. With inflation running at 2.7% as of late 2024, your equipment and inventory values have climbed, making this year an ideal time to conduct a professional appraisal and update your fixed-asset records.

Loss of Income and Business Interruption

The third layer covers loss of income and business interruption-the revenue you lose when an insured event forces you to temporarily close or reduce operations. This coverage continues paying your operating expenses and lost profits while you rebuild, which can be the difference between surviving a disaster and filing for bankruptcy.

Why Accurate Valuations Stop Underinsurance

Get a professional appraisal if you haven’t updated your property values in the past two years. Work with an appraiser who understands replacement cost, not just current market value. Document everything: equipment serial numbers, purchase dates, and cost. When renewal time arrives, submit this clean package to your carrier-it removes guesswork from underwriting and can help you secure flat or lower renewal rates.

For business interruption coverage specifically, calculate your daily operating expenses and monthly profit accurately. This number should reflect payroll, rent, utilities, insurance premiums, and loan payments that continue even when you’re not generating revenue. Underestimating this figure leaves you exposed to significant financial hardship. With property values trending in the 1%–3% range for 2025, you need to align your coverage limits with current asset values to avoid gaps in protection, especially after asset additions or renovations.

Why Your Business Can’t Afford to Skip Commercial Property Insurance in 2025

Natural Disasters Strike Harder Than Ever

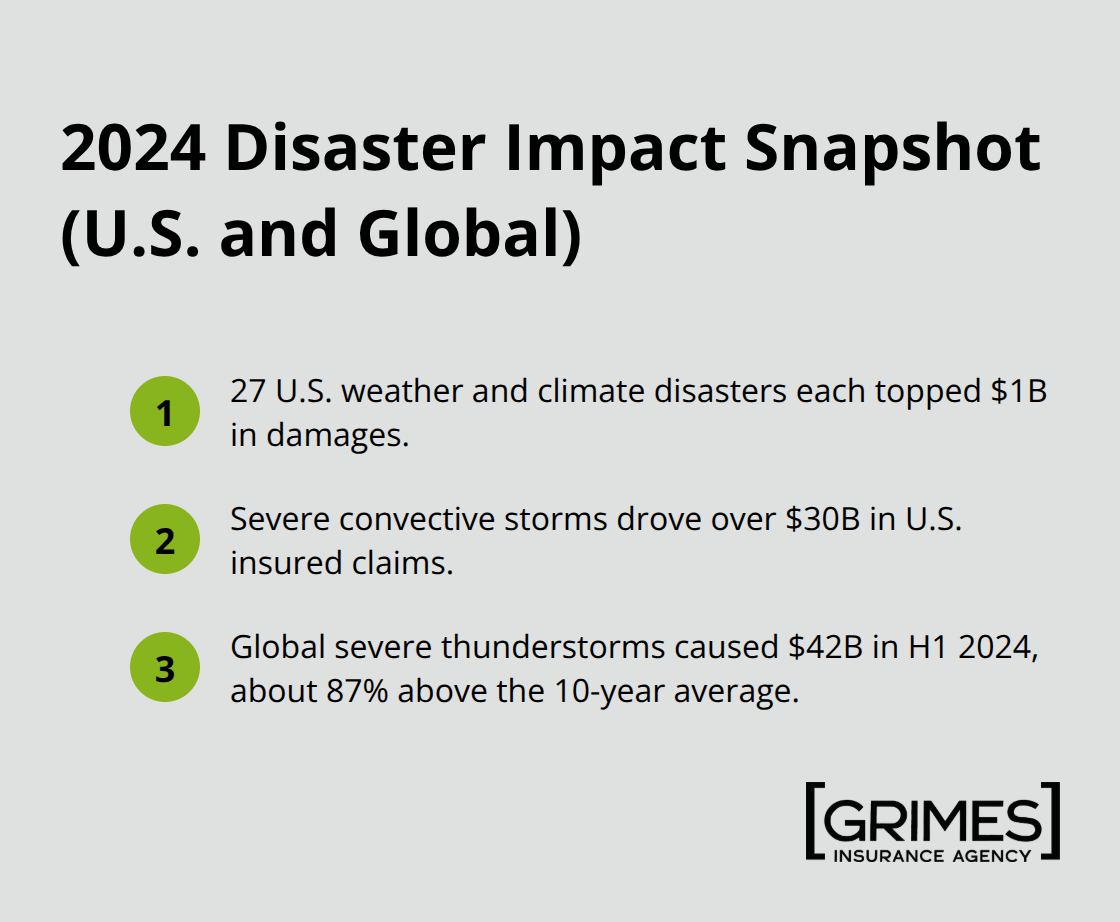

Natural disasters hit harder than ever, and the numbers prove it. In 2024, there were 27 individual weather and climate disasters with at least $1 billion in damages in the United States. Severe convective storms alone generated more than $30 billion in U.S. insured claims in 2024, while globally, severe thunderstorms in the first half of 2024 caused $42 billion in damages-about 87% above the 10-year average.

If your business sits in a hurricane zone, wildfire region, or hail corridor, you face real exposure.

The recent Los Angeles wildfires illustrate how quickly insured losses can reach tens of billions of dollars. Without commercial property insurance, a single weather event wipes out equipment, inventory, and your ability to operate.

Theft and Vandalism Drain Your Cash Reserves

Theft and vandalism add another layer of risk that many business owners underestimate. Criminal activity doesn’t announce itself, and your standard liability policy won’t cover stolen inventory or vandalized storefronts. Property insurance protects against break-ins, employee theft, and malicious damage-losses that can drain your cash reserves fast if you’re self-insured.

Business Interruption Coverage Keeps You Operating

More importantly, business interruption coverage keeps you afloat when disaster forces you to close temporarily. Your rent, payroll, insurance premiums, and loan payments don’t pause because a storm damaged your building. That’s where business interruption coverage matters most. It covers your operating expenses and lost profits while you rebuild, turning a potential bankruptcy into a manageable setback.

The 2025 Market Rewards Prepared Business Owners

The 2025 market actually favors prepared business owners. Global commercial property insurance rates declined modestly in early 2025 according to Aon’s Q1 2025 Market Overview, and capacity remains generally ample for standard property lines. Policyholders with clean loss histories and strong risk controls can expect single-digit rate changes or even flat renewals.

This advantage goes to businesses that prepare properly. Start your renewal process 90 to 120 days before your policy expires and submit a clean, evidence-based application package that includes updated valuations, documentation of risk mitigation measures, and precise property details. Carriers reward this preparation with better terms.

High-Risk Regions Require Strategic Mitigation

If you operate in a high-risk region-coastal areas prone to hurricanes, wildfire zones, or hail corridors-you’ll face tighter capacity and higher costs, but mitigation efforts still matter. Engineers’ reports showing that you’ve invested in disaster-resistant improvements, updated property records, and solid modeling data significantly influence pricing and terms. Businesses that treat their renewal as a strategic process, not an administrative checkbox, secure the best coverage at competitive rates. Understanding how carriers evaluate your specific risk profile helps you position your business for favorable terms when renewal time arrives.

How the 2025 Property Insurance Market is Shifting

Premium Growth Slows Dramatically

The property insurance market in 2025 looks fundamentally different from 2023 and 2024, and business owners who understand these shifts can capture real savings. Premium growth has decelerated dramatically-after increases exceeding 20% in 2023 and moderate growth of 8% to 12% in 2024, the market now stabilizes with single-digit rate changes for businesses with clean loss histories. Property insurance market stabilization in 2025 confirms that wide portions of the market are now characterized by ample capacity, strong competition, and flat-to-modestly-down pricing, with some exceptions. This means your renewal conversation this year can produce flat rates or actual decreases if you prepare properly.

The shift away from across-the-board rate hikes reflects carrier growth goals and favorable reinsurance renewals, but capacity remains selective. Standard property risks in non-catastrophe zones see the most pricing relief, while coastal hurricane zones, wildfire regions, and hail corridors continue facing tighter capacity and higher costs. Your location and risk profile now matter more than ever in determining what you’ll pay.

Risk Controls Drive Better Terms

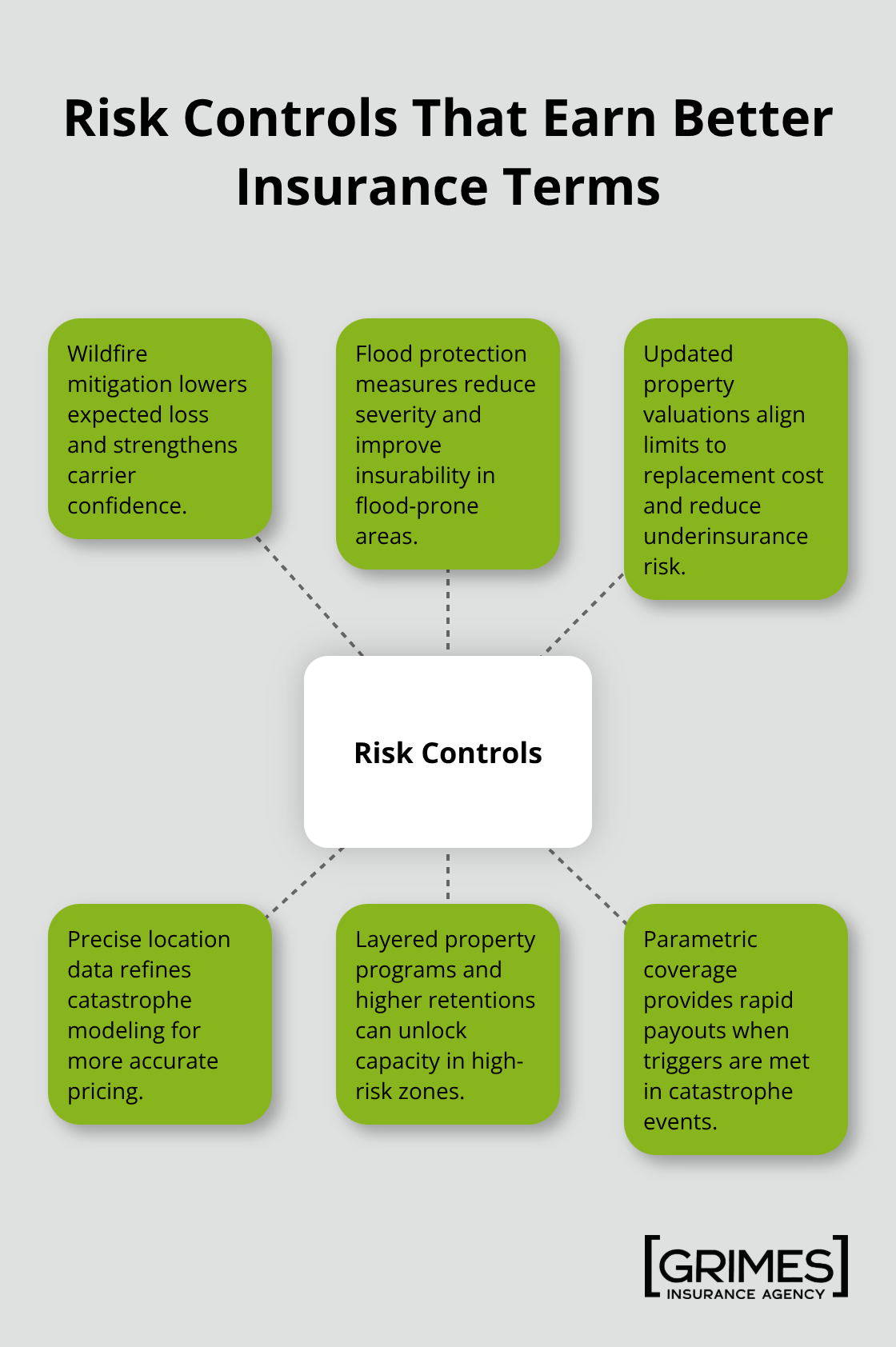

Customized coverage solutions replace one-size-fits-all policies, and this shift directly impacts your bottom line. Carriers increasingly reward documented risk controls-engineers’ reports showing wildfire mitigation, flood protection measures, updated property valuations, and precise location data now meaningfully influence both pricing and terms. If you operate in a high-risk zone, layered property programs with higher retentions can unlock coverage that standard policies won’t provide, though this requires working with a broker who understands catastrophe exposure modeling.

Alternative risk transfer solutions like parametric coverage offer businesses in vulnerable areas a way to maintain operations when traditional insurance becomes scarce. These alternatives provide flexibility that standard policies cannot match in catastrophe-prone regions.

Technology Transforms Risk Assessment and Claims

Technology has transformed how carriers assess risk and process claims. Telematics systems now track driver behavior in commercial auto fleets, helping reduce claim frequency and lower premiums, while digital property valuation tools and AI-powered underwriting accelerate decisions. These innovations mean carriers can evaluate your specific exposure more accurately than ever before.

Preparation Determines Your Renewal Outcome

Start your renewal 90 to 120 days early and compile a complete application package with current appraisals and risk mitigation documentation. Work with your broker to explore both standard and alternative solutions that match your specific exposure. Carriers in 2025 actively compete for well-managed risks, and your preparation determines whether you capture that competition in your favor or watch it pass to a competitor.

Final Thoughts

Commercial property insurance in 2025 protects your business from threats that can shut you down overnight-whether a hurricane destroys your building, a break-in empties your inventory, or a fire forces temporary closure. The market conditions right now favor business owners who take action, with carriers offering competitive rates and ample capacity for well-prepared risks. Start by conducting a professional property appraisal to establish accurate replacement values for your building, equipment, and inventory, then calculate your true daily operating expenses and monthly profit to set appropriate business interruption limits.

If you operate in a high-risk zone like a hurricane corridor or wildfire region, work with a broker who understands catastrophe modeling and can layer coverage strategically. The businesses capturing the best rates in 2025 submit clean applications with current valuations, documented risk controls, and precise property details. Schedule a conversation with an insurance professional at least 90 to 120 days before your renewal date and compile your property documentation, recent appraisals, and any risk mitigation measures you’ve implemented.

We at Grimes Insurance Agency have spent over 75 years helping business owners in Texas understand what is commercial property insurance in 2025 and secure the right protection at competitive rates. Our team accesses multiple carriers, which means we can compare options and find coverage that matches both your needs and your budget. Contact us to review your current coverage and explore how the 2025 market can work in your favor.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation