Business Insurance for Home-Based Businesses: Protecting Your Work-from-Home Setup

Your home-based business is growing, but your homeowners insurance isn’t protecting it. Standard policies explicitly exclude business activities, leaving your equipment, inventory, and liability exposure completely uncovered.

At Grimes Insurance Agency, we’ve seen too many home entrepreneurs discover this gap only after a problem occurs. Business insurance for home-based businesses fills those holes and gives you the protection your operation actually needs.

Why Your Homeowners Policy Won’t Protect Your Business

Standard Homeowners Coverage Excludes All Business Activity

Your homeowners insurance policy has one job: protecting your home and personal belongings. It does not protect your business. The Insurance Information Institute confirms that a typical homeowners policy provides only about $2,500 coverage for business equipment, with liability and lost income excluded entirely. If a client visits your home office and trips over your desk chair, your homeowners policy won’t cover their medical bills or legal fees. If your laptop gets stolen or your office furniture is damaged, you pay out of pocket. The exclusions are explicit and intentional-insurers designed homeowners policies for residential use only, not commercial operations. This gap exists regardless of whether you work part-time or full-time from home, and it doesn’t matter how small your business is. The moment you start generating income from your residence, your standard homeowners policy treats that activity as outside its scope.

Your Equipment and Inventory Face Total Loss Without Protection

Home-based business owners commonly hold thousands of dollars in equipment, inventory, and supplies with zero coverage under their homeowners policy. A consultant’s high-end laptop, a freelancer’s software licenses, a small retailer’s inventory stored in a spare bedroom-none of these receive protection. A house fire, theft, or water damage wipes out your operational assets without any insurance recovery. Professional liability matters too. If you provide advice or services to clients and they claim you caused them financial harm through negligence or an error, your homeowners policy won’t defend you in court or pay any judgment. Most home-based entrepreneurs operate with significant financial exposure. The cost of business insurance falls far below the risk of losing everything you’ve invested in your operation.

Client Visits Create Unprotected Liability Exposure

When someone visits your home for work purposes, your homeowners liability coverage becomes questionable or nonexistent. If a client injures themselves on your property during a business meeting, your insurer may deny the claim because the injury occurred during a commercial activity. Slip-and-fall accidents, allergic reactions, or property damage caused by a visiting client all fall into this gray zone. Your homeowners policy was designed for social guests, not business visitors. Even a single incident results in a five-figure medical bill or legal judgment that you personally must pay. Home-based business liability coverage specifically addresses this exposure by protecting against third-party bodily injury and property damage claims arising from your business operations. Without it, you remain personally liable for any damages, and your homeowners policy won’t step in to help.

Why Business Insurance Becomes Your Next Essential Step

The protection gap between homeowners insurance and business reality is substantial. Your operation needs coverage that actually recognizes what you do and the risks you face. The types of business insurance available for home-based entrepreneurs address each of these gaps directly-from liability protection for client visits to equipment coverage to professional liability for the advice or services you provide. Understanding what each coverage type does positions you to make informed decisions about your protection strategy.

Coverage That Actually Protects Your Home Business

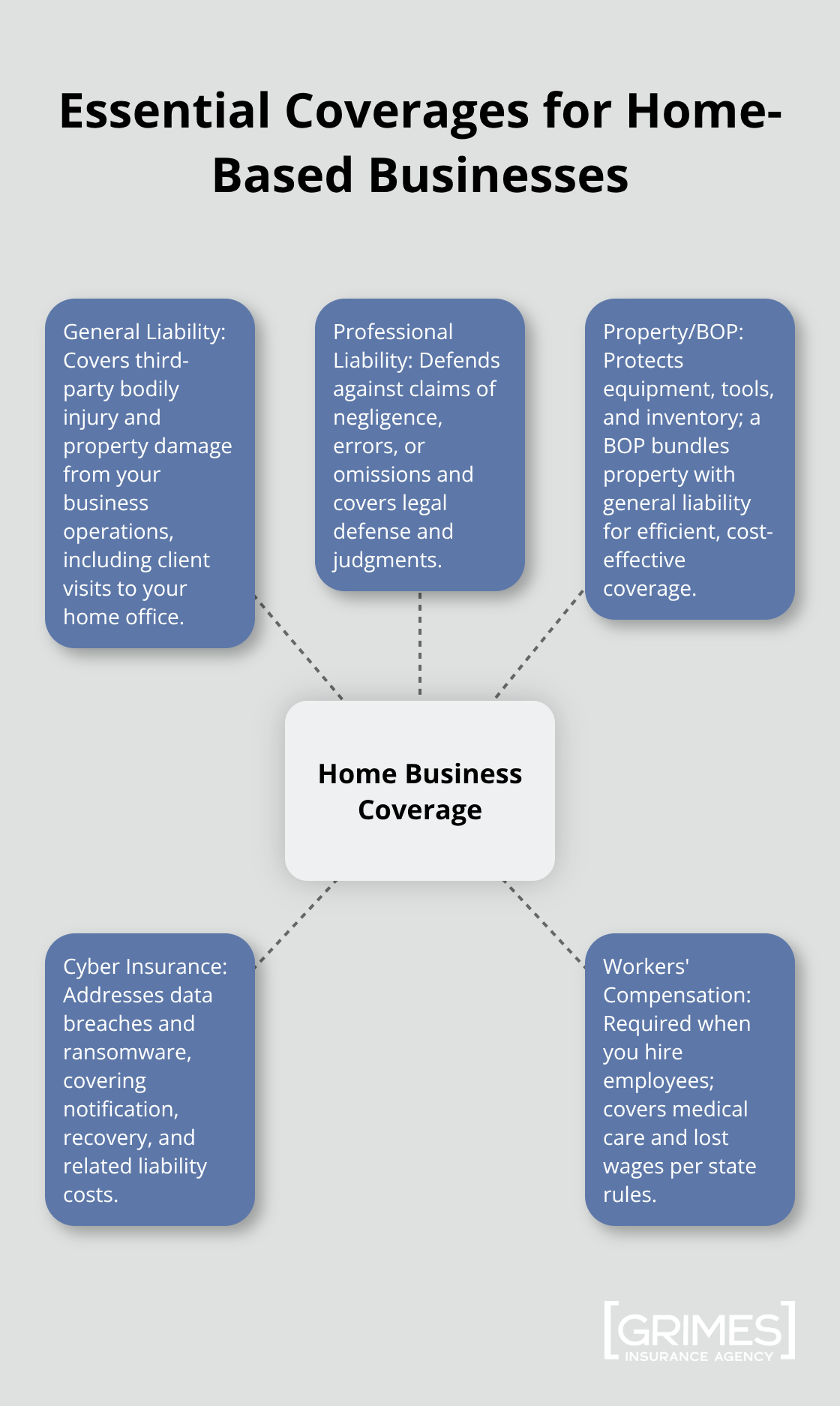

General Liability: Your Foundation Against Client-Related Claims

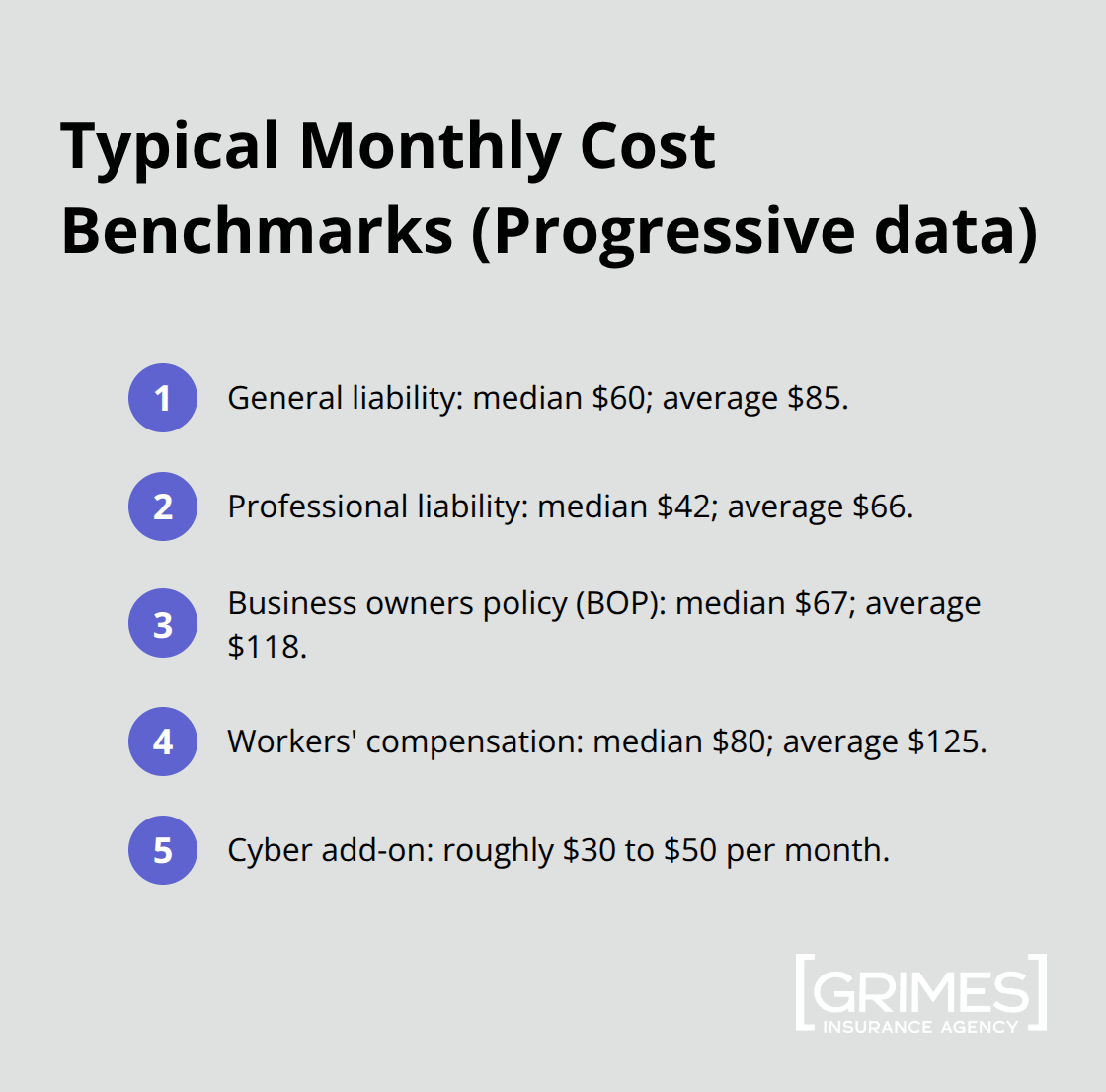

General liability coverage forms the foundation of protection for any home-based business. This coverage helps financially protect your business from certain third-party claims and lawsuits that arise from your business operations, which is exactly what your homeowners policy refuses to cover. When a client visits your home office and sustains an injury, or when your business equipment damages their property, general liability steps in to cover medical expenses, legal defense costs, and court judgments up to your policy limits. Progressive’s 2024 data shows median monthly costs for new general liability customers at $60, with average costs across all customers running $85 per month. For home-based operations, premiums often stay lower than office-based businesses because on-site risk is reduced. The type of work you do matters significantly-a financial consultant pays substantially less than a contractor or landscaper operating from home due to different exposure levels. Most home-based businesses should carry at least $1 million in liability coverage, though some professionals in higher-risk fields benefit from $2 million coverage.

Professional Liability: Defending Against Negligence Claims

Professional liability insurance addresses a different but equally critical exposure: claims that you made a mistake or provided negligent advice that caused a client financial harm. Unlike general liability, which covers physical injury or property damage, professional liability covers the cost of defending yourself against negligence allegations and paying any resulting judgment. If you work as a consultant, accountant, designer, IT specialist, or any professional providing advice or services, this coverage prevents a single client complaint from destroying your business. The median monthly cost for professional liability runs $42, with average costs at $66 per month according to Progressive data. Some professions benefit from customized endorsements-IT consultants can add software copyright infringement coverage to address common digital risks specific to their work.

Property Coverage: Protecting Equipment and Inventory

Property coverage protects your actual business equipment and inventory stored at home. A business owners policy, or BOP, bundles general liability with property coverage in one package, typically costing around $67 per month at median rates and $118 at average rates. This coverage protects computers, printers, office furniture, specialized equipment, tools, and inventory from theft, fire, water damage, and other covered perils. The Insurance Information Institute notes that homeowners policies provide only about $2,500 for business equipment, leaving you drastically underinsured if your operation contains valuable gear or significant inventory. With a BOP, you set coverage limits that actually reflect what you own and what it would cost to replace. If your home contains $15,000 in equipment and supplies, you can obtain coverage that matches that value rather than hoping $2,500 suffices. Bundling these coverages into a single BOP typically costs less than purchasing general liability and property coverage separately, making it the practical choice for most home-based entrepreneurs.

Cyber Insurance and Workers’ Compensation: Addressing Digital and Employment Risks

Cyber insurance deserves serious consideration if you handle client data, process payments, store customer information, or rely heavily on digital systems to operate. This coverage protects against data breaches, ransomware attacks, and other technology-related losses that can cripple a home-based operation. Small-business policies increasingly include cybersecurity coverage as a standard or optional add-on, recognizing that remote workers face genuine digital risks. Workers’ compensation becomes mandatory if you hire employees to work from your home, even part-time.

State requirements vary significantly, so verify your specific state’s rules before hiring anyone. The median monthly cost for workers’ compensation runs $80, with average costs at $125 per month. If you operate as a sole proprietor with no employees, you may not legally need workers’ compensation in many states, though some states require coverage even for solo operators in certain professions.

Building Your Protection Strategy

The combination that works best for most home-based businesses consists of general liability plus professional liability, packaged as a BOP with optional cyber coverage added. This approach covers liability from client visits, protects your equipment and inventory, defends against negligence claims, and addresses digital threats-the four primary exposures facing home entrepreneurs. The exact coverage you need depends entirely on your specific business type, the equipment you own, whether you have employees, and the risks inherent in your profession. Identifying gaps in your current protection requires an honest assessment of what could go wrong in your operation and what financial impact each scenario would create. An independent insurance agent can help you evaluate these exposures and recommend coverage that matches your actual business model rather than a generic package that leaves you underprotected.

Where Most Home-Based Businesses Fall Short on Coverage

The Three Critical Mistakes Home Business Owners Make

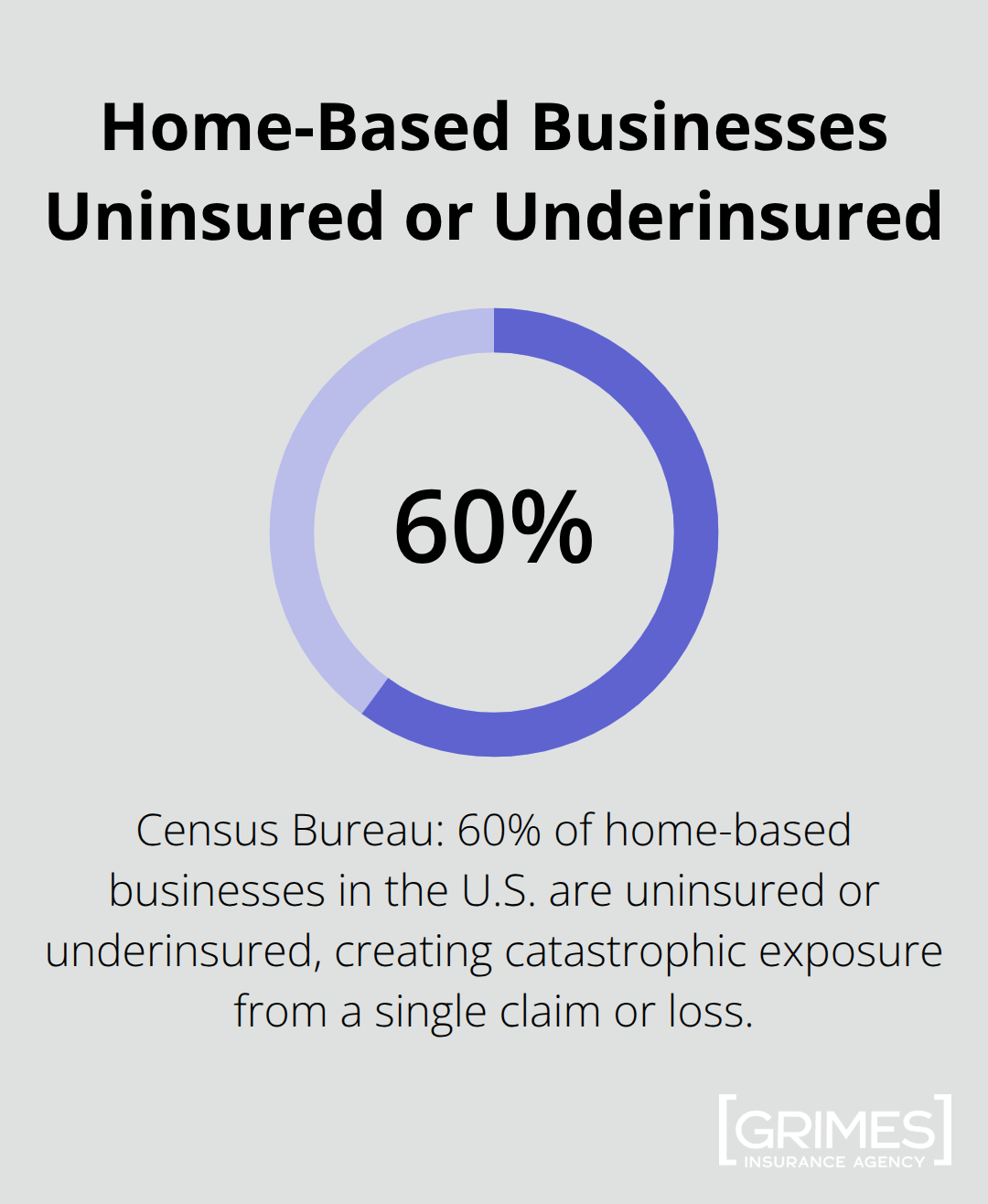

Most home-based business owners make one of three critical mistakes when buying insurance: they dramatically underestimate what their equipment and inventory actually costs, they set liability limits too low based on false assumptions about their risk, or they completely ignore cyber threats despite handling sensitive client data. The Census Bureau reports that about 60 percent of home-based businesses are uninsured or underinsured, which means they face catastrophic financial exposure from a single claim or loss. This isn’t a theoretical problem-it happens constantly, and the financial consequences are severe.

Underestimating Equipment and Inventory Costs

Your actual equipment and inventory almost always exceed what you think it costs. A consultant might own a laptop, external hard drives, specialized software licenses, a printer, office furniture, and filing cabinets totaling $12,000 to $18,000, yet their homeowners policy caps business property at $2,500. A freelancer storing materials or finished goods faces similar gaps. When you add up computers, monitors, cameras, tools, supplies, and inventory, home-based operations commonly contain $10,000 to $40,000 in physical assets. A single fire or break-in destroys your ability to operate. The fix is straightforward: inventory everything you own related to your business, get replacement cost quotes from retailers, and set your business property coverage limits to match that total. Don’t guess-measure. If you own $25,000 in equipment, buy $25,000 in property coverage. The premium difference between a $5,000 limit and a $25,000 limit is minimal because the underwriting cost stays roughly the same; you’re simply adjusting the maximum payout amount.

Setting Liability Limits Too Low

Liability limits present the second critical gap. Many home-based entrepreneurs buy a $300,000 or $500,000 general liability limit because it sounds adequate, then face a single claim that exceeds it. A client visits your home office, slips on a staircase, and requires emergency surgery costing $150,000 in medical bills plus ongoing care. A legal judgment could easily reach $300,000 to $500,000 depending on your state and the severity of the injury. You need minimum coverage of $1 million per occurrence and $2 million aggregate-meaning $1 million per single incident and $2 million total across all claims in a policy year. This is the standard threshold where professional liability and general liability together create genuine protection. Higher-risk professions like contractors or landscapers should seriously consider $2 million per occurrence. The cost difference between $500,000 and $1 million coverage runs only $15 to $30 per month for most home-based businesses, making the upgrade financially absurd to skip.

Overlooking Cybersecurity Threats

Cybersecurity represents the third major gap that home-based businesses routinely overlook. If you process credit card payments, store customer email addresses, maintain client lists, handle medical or financial information, or access your employer’s systems from home, you face data breach risk that standard business policies don’t address. A ransomware attack that encrypts your files and forces you to pay hackers to restore access, or a data breach where customer information gets stolen, creates liability and operational costs that blow through standard coverage limits. Cyber insurance covers notification costs, credit monitoring services for affected customers, recovery expenses, and liability claims from customers whose data you lost. The median cost for cyber coverage adds roughly $30 to $50 monthly to your policy. For any home-based business handling client or customer data, this coverage isn’t optional-it’s a business expense you should view the same way you view internet service or software subscriptions.

Final Thoughts

Your home-based business operates in a protection gap that standard homeowners insurance refuses to fill. Business insurance for home-based businesses addresses the three exposures that matter most: liability from client visits, property damage to your equipment and inventory, and professional negligence claims. A business owners policy bundled with cyber coverage creates the foundation you need, with liability limits set at $1 million per occurrence and $2 million aggregate.

Assess your actual exposure by listing every piece of equipment and inventory you own, calculating replacement costs, and imagining the financial impact if a client sued you for negligence or your business data was compromised. Each scenario reveals a coverage gap that your homeowners policy won’t address. Set your property coverage limits to match your actual equipment value rather than hoping the $2,500 your homeowners policy provides will suffice.

We at Grimes Insurance Agency help Lubbock-area business owners identify protection gaps and find coverage that matches their actual operations. Contact Grimes Insurance Agency to review your current protection and build the business insurance strategy your home-based operation needs.