The Importance of Flood Insurance in Lubbock: Safeguarding Your Home

Flooding poses a real threat to Lubbock homeowners, and most don’t realize their standard homeowners policy won’t cover water damage. The importance of flood insurance in Lubbock can’t be overstated when you live in an area prone to heavy rainfall and flash flooding.

We at Grimes Insurance Agency help homeowners understand their flood risk and find the right protection. This guide walks you through what flood insurance covers, how to assess your needs, and why acting now matters for your home’s safety.

Understanding Flood Risk in Lubbock

Why Lubbock Homeowners Face Real Flood Risk

Lubbock sits in a region where flash flooding and heavy rainfall create genuine hazards that most homeowners underestimate. The city experiences unpredictable weather patterns that can dump significant rainfall in short periods, overwhelming drainage systems and causing water to spread across neighborhoods quickly. Areas within Lubbock’s flood zone include Primrose Pointe, McAlister Park, Kings Park, Melonie Park, Ballenger, Bayless Atkins, and the Lubbock County Courthouse area.

But here’s the critical reality: about 40% of flood insurance claims come from outside high-risk flood zones, meaning your home faces flood risk even if current maps don’t mark your property as high-risk. During Hurricane Harvey in 2017, more than half of flooded homes sat outside the official floodplain, proving that flood maps lag behind actual risk. Lubbock’s inland location does not provide safety-flash floods and rapid urban development increase runoff significantly, putting properties throughout the city at genuine risk.

The Gap Your Homeowners Policy Leaves Open

Standard homeowners insurance explicitly excludes flood damage, and this isn’t a minor detail tucked into fine print. Your policy covers fire, theft, wind, and hail, but water damage from rising water, overland flooding, or heavy rainfall falls completely outside coverage. Insurance companies treat flood as a separate peril that requires its own dedicated policy.

This means a typical flood event costing $21,000 to $26,000 in repairs (including flooring, mold remediation, and wall work) would come directly from your pocket without flood insurance. Federal disaster loans average under $10,000, leaving homeowners far short of actual repair costs. The solution is straightforward: you need a separate flood insurance policy to cover what your homeowners insurance won’t.

What You Actually Need to Protect Your Home

A dedicated flood policy fills the protection gap that your standard homeowners coverage leaves open. Understanding what flood insurance covers-and what it doesn’t-helps you make informed decisions about your home’s safety. The right flood policy protects both your home’s structure and your personal belongings, but only if you understand the specifics of your coverage before disaster strikes.

What Flood Insurance Actually Covers

Your Home’s Structure and Building Systems

NFIP flood policies protect your home’s structure up to $250,000 and your personal belongings up to $100,000 for standard one- to four-family homes. The dwelling coverage pays for repairs to your foundation, electrical systems, plumbing, HVAC equipment, built-in appliances, and permanent fixtures that floodwaters damage. If your home’s replacement value exceeds $250,000, private flood insurers may offer higher limits and replacement cost value instead of actual cash value-a significant advantage for older homes that depreciate quickly under NFIP’s standard approach.

Personal Property and Belongings

Personal property coverage reimburses you for clothing, furniture, electronics, and other belongings that flooding destroys, but this coverage excludes items stored in basements, vehicles, detached structures like garages, and valuables such as precious metals or important documents. Many homeowners fail to document their belongings before a flood occurs, which slows the claims process considerably. You should photograph and video your possessions and store an inventory digitally to speed up claims substantially when disaster strikes.

Temporary Housing and Living Expenses

Additional living expenses coverage pays for temporary housing, meals, and other costs if your home becomes uninhabitable after a flood. NFIP policies typically cap this benefit while private policies may offer more generous limits, so you should compare flood insurance policies before selecting your coverage.

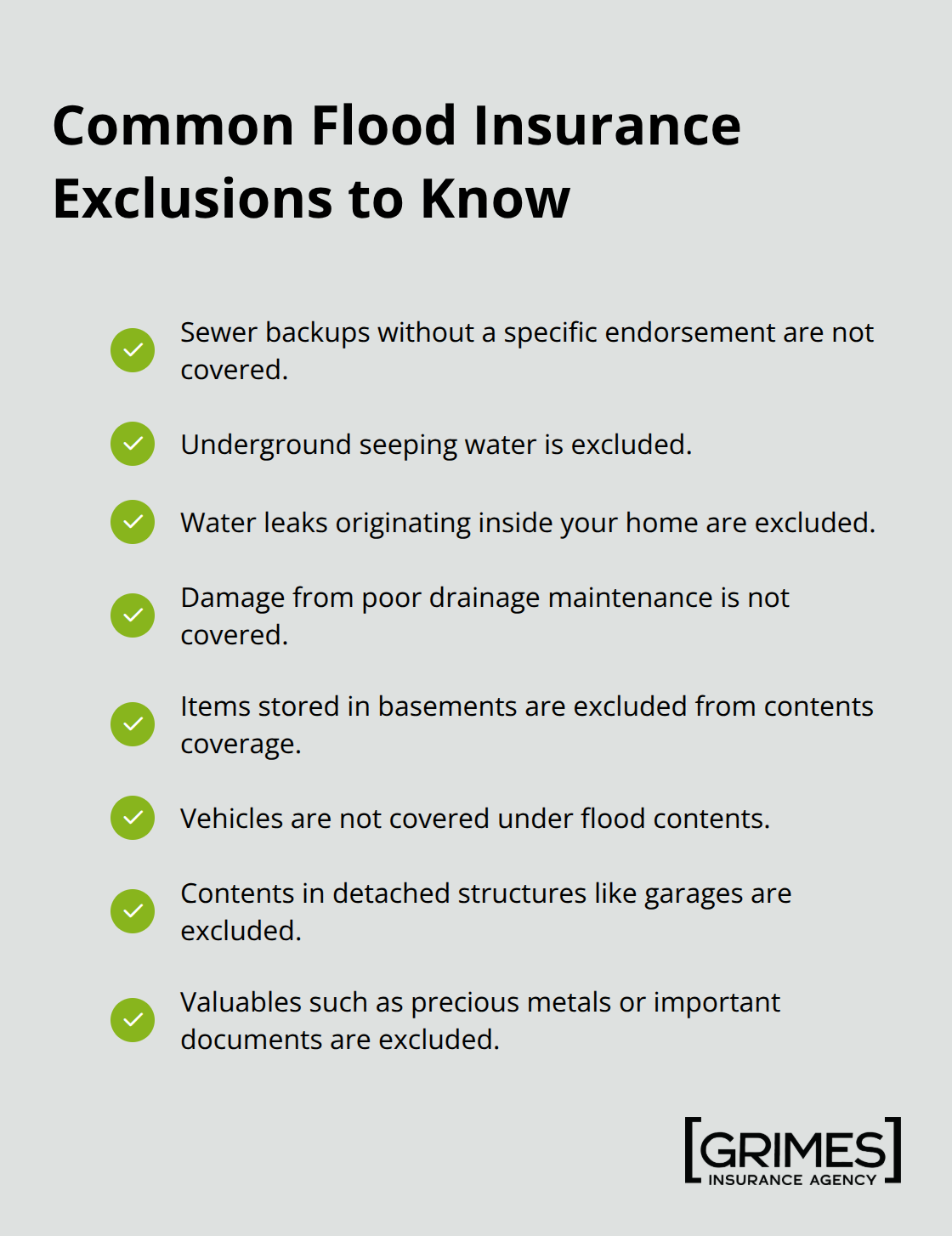

What Flood Insurance Explicitly Excludes

Your flood insurance does not cover sewer backups unless you purchase a specific endorsement, underground seeping water, water leaks originating inside your home, or damage from poor drainage maintenance on your property. This distinction matters because homeowners often assume flood insurance covers all water damage, then discover their claim gets denied. You should review your policy details carefully before disaster strikes and ask about endorsements that fill common gaps.

Timing, Cost, and Coverage Decisions

The 30-day waiting period before coverage becomes effective means you must purchase a policy well before storm season arrives-waiting until severe weather threatens leaves you unprotected. If your lender requires flood insurance, that mandatory coverage typically starts immediately for certain policy changes, but standard new policies still observe the waiting period. Comparing quotes from multiple providers reveals significant price differences; the average flood insurance policy in Texas costs less than $700 annually, though Lubbock properties average around $795 per year, and policies outside designated floodplains often cost around $300 per year. Higher deductibles lower your premium substantially, so choosing a $2,500 or $5,000 deductible instead of $1,000 can reduce your annual cost meaningfully if you can absorb that out-of-pocket expense during a claim. The average flood repair costs between $21,000 and $26,000, so understanding exactly what your policy covers prevents financial devastation after a loss. With these coverage details in mind, the next step involves assessing your specific flood risk and selecting the right policy limits for your home’s unique situation.

Choosing the Right Flood Insurance for Your Lubbock Home

Assess Your Property’s Flood Risk Level

Start with FEMA’s flood map service center to determine whether your home sits in a designated high-risk zone or moderate-to-low risk area. This distinction affects your premium and coverage options significantly. Properties in high-risk Special Flood Hazard Areas pay approximately $900 to $1,200 annually, while moderate-to-low risk zones average around $671 per year according to NFIP data. Even if FEMA maps show your Lubbock home outside the floodplain, understand that about 40% of flood claims occur in unmapped areas, so risk assessment extends beyond official designations.

Your property’s elevation, distance to drainage systems, and local rainfall patterns all influence actual flood exposure.

Compare NFIP and Private Flood Insurance Options

Once you know your risk level, you can decide between NFIP policies capped at $250,000 for dwelling coverage and $100,000 for contents, or private flood insurance that often provides higher limits and replacement cost value pricing. Private policies may cost more upfront but reimburse replacement costs instead of depreciated value, protecting older homes far more effectively when repair bills exceed $21,000 to $26,000. NFIP coverage works well for standard homes in moderate-risk areas, while private insurers serve homeowners with high-value properties or those outside traditional flood zones who want stronger protection.

Select Coverage Limits and Deductibles That Fit Your Situation

Coverage limits and deductibles require honest self-assessment about what you can afford out-of-pocket and what financial loss would devastate your household. Selecting a $5,000 deductible instead of $1,000 reduces your annual premium meaningfully, saving hundreds of dollars yearly if you can absorb that expense during a claim. Many Lubbock homeowners wrongly assume they need maximum coverage limits when a $100,000 contents policy actually covers most standard household belongings unless you own valuable art collections or extensive jewelry. Calculate your home’s actual replacement cost by listing major systems, fixtures, and contents, then match that figure to appropriate coverage limits rather than guessing.

Plan Your Purchase Timeline

The 30-day waiting period before coverage activates means you must purchase your policy well before storm season, ideally by spring in Texas. If your lender requires flood insurance, that mandatory coverage typically starts immediately for certain policy changes, but standard new policies still observe the waiting period. Waiting until severe weather threatens leaves you completely unprotected, so act early to avoid coverage gaps.

Work with a Licensed Insurance Agent

A licensed agent who understands Lubbock’s specific flood patterns can compare flood insurance policies from multiple carriers simultaneously, revealing price differences that often exceed $300 annually for identical coverage. An experienced agent identifies endorsements you actually need (such as sewer backup protection or increased coverage for detached structures) rather than selling unnecessary add-ons that inflate premiums. We at Grimes Insurance Agency can help you navigate these decisions and find the right protection for your home’s unique situation.

Final Thoughts

Flood insurance protects your Lubbock home from financial devastation that standard homeowners policies simply won’t cover. Typical flood repairs cost $21,000 to $26,000, while federal disaster loans average under $10,000, leaving homeowners far short of actual expenses. About 40% of flood claims occur outside designated floodplains, which means your property faces genuine risk regardless of current FEMA maps-the importance of flood insurance in Lubbock extends well beyond mapped flood zones.

Your next step involves determining your home’s actual flood risk by checking FEMA’s flood map service center, then comparing NFIP and private flood insurance options to find coverage limits and deductibles that match your situation. A licensed insurance agent can reveal significant price differences between carriers and identify endorsements your specific property actually needs. We at Grimes Insurance Agency can help you assess your flood risk and secure the coverage your home deserves.

Waiting until severe weather threatens leaves your family unprotected and forces you to absorb repair costs entirely from your own resources. Lubbock’s flash flood risk and heavy rainfall patterns demand proactive protection, not reactive scrambling after water damages your foundation, electrical systems, and personal belongings. Contact Grimes Insurance Agency today to get started before the next storm arrives.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation